.520ZBritish firms’ cash hoard is over £500bnBy Michael Burke

The source of the current crisis is the unwillingness of private firms to invest. Instead, they are hoarding cash that could otherwise be invested. The latest data shows that this cash hoard stood at £501.9 billion at the end of 2013. It has almost certainly risen since.

The latest ‘flow of funds’ data from the Office for National Statistics (ONS) provide comprehensive data for the financial flows between each sector of the economy. They show how the cash mountain has been created. Via the banks, these data show how the incomes of firms (mainly profits) or of individuals (mainly wages) can become savings and may be used for investment.

If a capitalist economy is functioning in the textbook manner, firms will generate profits which they use for their own investment. Through bank borrowing they will also be able to use the savings of private individuals to supplement that investment. It is the supposedly efficient and large-scale way that this takes place that gives the capitalist economy its particular power, and the pre-eminence of the private sector within that, including the banks.

But this is not what is happening in the British economy. The ONS chart below shows the savings and investment levels private non-financial firms (all private corporations excluding banks, insurers and so on, or PNFCs). These are shown from 1997 onwards as a proportion of GDP.

Over a prolonged period from 2001 to 2013 private firms in Britain have been net savers. Far from borrowing from another sector such as households (or from overseas, or government), private firms have been saving not borrowing. The peak level of this net saving was 4.3% of GDP in 2011. The recent high-point for firms’ borrowing was a not very high level of 2.8% of GDP in 2000. The difference between those two levels is 7.1% of GDP. This is significantly greater than the actual annual contraction in output during the recession and entirely accounts for it.

At the same time private firms have been cutting their levels of investment. Firms’ productive investment (Gross capital formation) peaked at 12.4% of GDP in 1998. It fell to 7% at the low-point of the recession in 2009, and the rebound since has only been to 9.2% of GDP. This is actually below the level of capital consumption in the economy (the capital consumed in the course of production). As a result British firms are not net producers of capital.

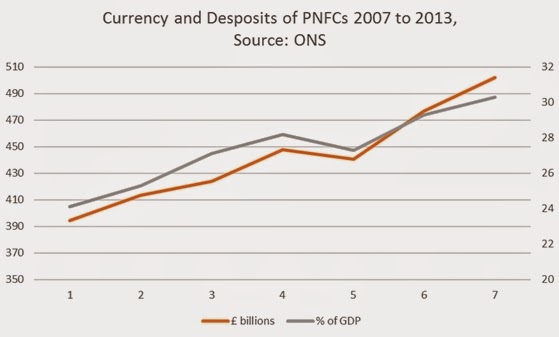

It is the savings of private frims which have produced the cash mountain. The growth of the cash hoard is shown in Fig.2 below both in terms of billions of pounds and in propprtion to GDP.

A number of reasons have been advanced for the growth in the cash mountain, including increasing complexity of global supply chains, greater uncertainty and other factors. They are generally unconvincing, not least because the growth in the cash hoard has coincided with both record shareholder returns and senior management rewards.

Companies in Britain and in the Western economies generally are content to retain or even increase high debt levels in order to fund share buybacks and extraordinary boardroom pay. They are not prepared to invest even their own profits, much less borrow to invest.

The cash hoard is directly related to profitability. Firms will not invest while they do not anticipate sufficent returns on that investment. As a result, the cash hoard will grow until they do.

Yet it is clear that the idea that ‘there is no money left’ for investment is false. The money is simply in the hands of those who refuse to invest it. What is required are measures that will wrest it from them in order to fund investment.

Recent Comments