Alan Milburn’s report ‘Young people and work: interim report’ has received widespread coverage and considerable acclaim.

But this praise is misplaced. It represents the mistaken acceptance of a string of assertions on NEETs (people Not in Education, Employment or Training) that are not supported by Milburn’s own evidence. These false assertions matter because they are paving the way for a severe changes in the system of benefits for young people, which will have far-reaching consequences for them and for society in general.

This article will argue the following points:

The number of NEETs is not out of control, it is below the 25yr average (when records began)

The number has not been rising until very recently; it has been stable at a low level

Nearly 50% of NEETs don’t claim benefits, so the genuine problem of lack of work has nothing to do with benefits

Another 20% have such severe disabilities that even DWP doesn’t expect them to work

This means that 2/3rds of all NEETS cannot be affected by benefit cuts, yet this is the aim of the report

The most recent data, produced since the report, does show a rise (still well within pre-existing ranges). But this is evidence of a change in objective circumstances for youth employment and training, not any adverse change in pay, or benefits.

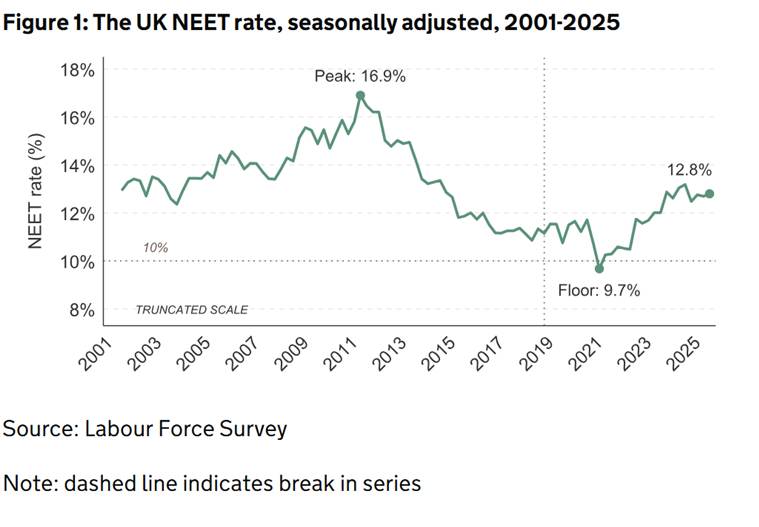

Chart 1. The rate of NEETs in the British economy

Fig.1 above shows the proportion of young people who are NEETs. The proportion is a more meaningful figure than recent headline-grabbing reports that the total has topped 1 million, as the number of young people has been growing over time.

What the very first chart of the report shows is that there is no new crisis of NEETs at all. If we disregard the exceptional period of lockdown the low-point for the proportion of NEETs is 11%. The high is 16.9%. The 12.8% in Milburn’s report is very far from a surge. It is actually below the long-term average.

There is another feature of the chart which is worth discussion. Milburn argues that he does not want a ‘blame game’, so barely discusses causes of the NEETs problem at all. But, accepting that there is a concern with any high level of people who could be in work, education or training and are not, then it is a glaring error to avoid discussion of causes.

Fig. 1 shows a sustained fall in the proportion of NEETs from 2011 until progress was halted in 2019. The report has nothing to say about this fall, which might be of interest to anyone addressing the issue.

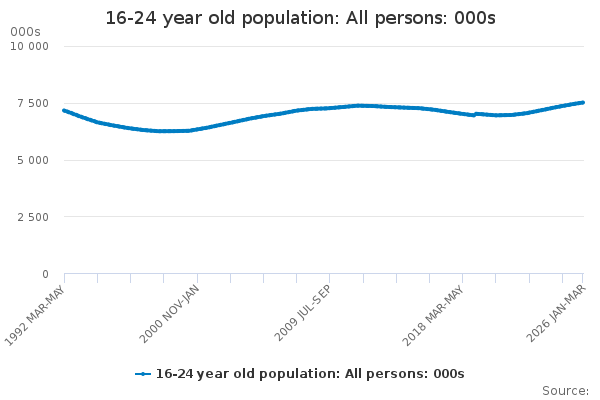

Chart 2. Population of 16 to 20 year olds

Source: ONS

One of the key factors producing a rise in NEETS is simply the rise in their total, without the employment or training and education to harness their potential. Between June 2011 and June 2020 youth numbers fell by 429,000, which largely accounts for the earlier fall.

Currently there are 7.5 million 16-24 year olds in Britain. On known demographics, the Office for National Statistics projects this total will rise by 100,000 a year over the next 3 years and will then begin a gradual decline. This poses a challenge in the short-term, but the current panic over the number of NEETs is false. It is firstly a demographic blip.

However, Milburn’s report does not treat it as such, instead preferring to categorise it as a major structural problem requiring urgent remedy. But a central part of the recommended policy response will be reduced welfare available to 16-24 year olds, both in terms of eligibility for benefits and the level of support provided by those benefits. Welfare costs are cited early in the foreword to the report and mentioned 53 times in total.

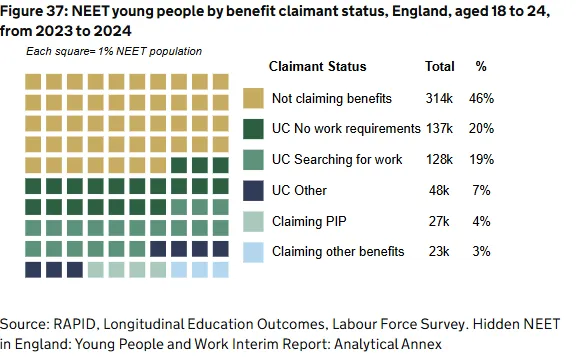

But it is precisely in the area of benefits that Milburn’s report gets itself into the biggest muddle. Chart 3. Below shows NEETs by benefits status and is also taken from the Milburn report.

Chart 3. NEET young people by benefit claimant status

The first point to note is that 46% or nearly half of all NEETs are not in receipt of any benefits at all. Therefore, any policy claiming to tackle the issue of NEETs that relies primarily on benefit cuts, as Milburn suggests, is likely to fail given that any cuts will not affect nearly half of all NEETs.

That likelihood gets closer to a certainty once the second category of NEETs is considered. 20% of them have no DWP requirement to search for work at all. These are mainly people who are so severely disabled that they are exempt from searching for work. There are other categories of people under the same heading, such as women in the later stages of pregnancy.

Taking these two categories together, people not receiving benefits and those receiving benefits without a requirement look for work, amounts to 66% of all NEETs. So, two-thirds of all NEETs cannot directly be affected by any cuts to benefits in any way.

On another interpretation, Milburn intends to propose benefits cuts for young people regardless of these facts. In that case the panic over NEETs would simply be a pretext for cuts to benefits for all young people, primarily and overwhelmingly who are not NEETs.

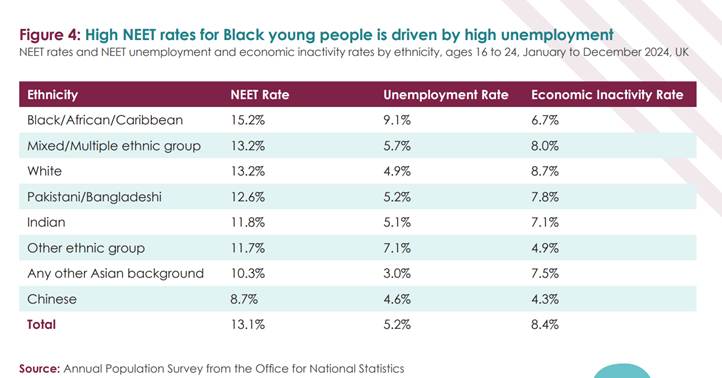

One key consequence of any attack on young people in general or NEETs in particular is that this would fall disproportionately on young Black people. This is shown in Chart 4 below.

In summary, the evidence from the Milburn report itself is that the panic over NEETs is spurious. Milburn’s conclusions do not follow from the evidence at all. Instead, the aim to generate a panic over NEETs to launch a widespread attack on the support provided to young people in general. There is no attempt to address the causes of young people being denied education, employment or training to improve their opportunities and outcomes.

Britain is both a declining economic power and an increasingly dangerous and reckless military one, in a subordinate relationship with the United States. In that sense, it serves as an example for NATO member states to one degree or another. These two contrasting trends are economically and politically linked. An examination of them highlights important observations about key aspects of the current situation in Britain, and potentially offers insights into broader trends across the NATO bloc.

There is now a war drive underway in NATO, encouraged by Trump. This is an extension of NATO expansion that has been ongoing since 1952, and especially since the collapse of the Soviet Union. It has taken a decisive new turn under the Biden and Trump II presidencies.

As a result, there is not only growing propaganda regarding external threats, but also Trump’s demand for increased military spending by other NATO members is largely being met. Alongside this, considerable effort is being made to promote the supposed economic benefits of increased military spending. As will be shown, these claims are illusory—the economic impact of increased military spending will be the opposite of what its supporters claim. It will likely entrench Britain’s economic stagnation, or worse.

Economic Stagnation

The relative decline of British capitalism is not a new story. In 1820, Britain accounted for 9.8% of global output (Maddison data); today, it accounts for just 2.1% of world GDP (World Bank). The gradient of decline in recent years suggests that Britain’s relative economic decline is now at risk of becoming absolute. This reflects both a long-term secular slowdown and a shift into a new, lower gear of economic deceleration. The economy is approaching outright stagnation.

To illustrate: in the decade to 1965, the British economy grew by 37% in real terms. In the decade to the first quarter of 2025, it grew by just 14%, representing an annual average growth rate of little more than 1%—a trend that has persisted in recent years, excluding the effects of the COVID-19 lockdown. Aside from temporary booms such as the North Sea oil windfall (which soon turned to bust), the growth rate has been in near-continuous decline since the post–World War II recovery.

There is no mystery behind this stagnation. Britain has long maintained one of the lowest rates of investment (Gross Fixed Capital Formation, GFCF) in the G7. This has declined erratically but steadily, falling from 23% of GDP in 1970 to 17% of slowing GDP in 2024 (Office for National Statistics, ONS data). Fixed capital formation is necessary to maintain an economy’s productive capacity. Economic growth requires an increase in fixed capital formation. Since capital is consumed in the production process, the most appropriate measure of whether the stock of fixed capital (the “means of production”) is expanding or contracting is net fixed capital formation, which deducts the capital consumed from total new investment.

Prior to the Global Financial Crisis (2007–2008), Britain’s net fixed capital stock grew at an annual average rate of 2.5%, according to ONS data. Since the crisis (excluding the crash itself), this rate has slipped to 1.5%. Just as Britain’s relative economic decline has become a commonplace, so too has the widespread understanding that this is led by the decline of British manufacturing. This sectoral decline is driven by weak investment, particularly in net fixed capital formation.

Although the Bank of England and others describe the weakness in output and productivity growth as a “puzzle,” the ONS data are clear and decisive. In real terms, the manufacturing stock of fixed assets was £271 billion in 1995. By 2023, it had reached just £274 billion—barely any increase at all. The means of production in British manufacturing are not expanding. The fact that real manufacturing output has increased by just over 50% in the same 28-year period shows that there is no productivity puzzle, at least in terms of capital productivity. What is missing is growth in the real level of fixed manufacturing assets.

A Call to Arms

This structural, long-term weakness of the British economy has not been corrected by the prolonged period of austerity, which the Starmer government has continued. Manufacturing and industrial production in aggregate (which also includes energy, water, gas, and oil production), as well as GDP, have all grown at an annual average pace of 1% or less since austerity was first implemented in 2010.

Under strong pressure from Trump, the Labour government under Starmer has committed to reaching the US President’s target of spending 5% of GDP on the military among G7 countries. In reality, the figure will be somewhat lower. Widespread reports suggest that Britain, like other NATO members, will increase strictly military spending to 3.5% of GDP. The remainder will be allocated to military-related infrastructure (road and rail links, barracks, and similar projects). Much of this spending is likely to be on projects that would not otherwise have been undertaken and may be exclusively for military use, offering little utility to the productive sectors of the economy.

Military spending currently stands at 2.3% of GDP. The increase on the narrower measure will amount to a rise of 1.2% of GDP, or approximately £35 billion—an amount expected to grow over time. Announcements of increased military spending have been accompanied by a flurry of PR about the supposed economic benefits of this new expenditure, with promises that the benefits will be spread across the country. These claims are misleading. The spending will require large government outlays that yield almost nothing in terms of economic recovery. As a result, the net effect is likely to be the opposite of what its supporters claim. The British population will be worse off due to increased military spending, as resources will be diverted from other essential areas of government expenditure.

Why Military Spending Cannot Drive Economic Recovery

There are both theoretical and practical reasons for arguing that increased military spending will not lead to economic recovery. The theoretical issues will be addressed first, as they apply not only to Britain but to all countries, including the United States.

Both consumption and investment require prior production. What has not been produced—either by human labour or by nature—cannot be consumed. Likewise, investment requires production to proceed it. In Adam Smith’s famous example, investment in the creation of a pin requires digging coal, building an ironworks, smelting iron, and so on before the pin can be produced. But each of these steps—the capacity to produce coal, iron, or a factory—requires investment. Production and investment form a circular system.

There are only two broad categories for allocating production: consumption or investment. But of the two, only investment can augment the means of production. Consumption, by definition, uses up production and therefore cannot expand it.

Investment is the decisive factor in economic growth (and ultimately in prosperity, however it is shared). There is a widespread fallacy that consumption can lead to growth. But consumption is not an input to production—it is an outcome of it. Claims that consumption can “induce” or lead to growth require a mystification of the production process, where producers anticipate demand, consumption occurs, and production follows.

Under certain conditions, production can indeed be induced in this way, and it may be sensible for policymakers to attempt to stimulate it when there is spare capacity in the economy and consumption can rise to match it. But in all cases, investment in the productive capacity of the economy must occur first.

The corollary is that production is required for both investment and consumption. As investment either replaces or augments the means of production, it creates the conditions for maintaining or increasing production, which is the basis for prosperity. That increased production can then be directed either toward consumption or further investment. Therefore, while the sustainable satisfaction of human needs (consumption) is—or ought to be—the purpose of economic policy, the necessary means to achieve it is investment.

The definition of investment is that it adds to or replaces the existing means of production. Anything that increases the level of fixed assets in the economy is properly categorised as investment (Adam Smith’s term for the level of fixed assets was simply “stock”). Modern economic literature often uses a different definition of investment—an outlay for which there is a financial return. This is incorrect; it should be an economic return. There is no greater economic return from a toll road than from a road built without charges, and training a teacher for a publicly owned school is as economically productive as for a privately owned one. Either definition—financial or economic—can be used in examining military spending.

Despite the best efforts of its supporters, increased military spending is not investment. This is true even for military hardware. Missiles, bombs, and fighter jets are not additions to the means of production—they are designed to destroy it, along with human lives. Military hardware is the opposite of investment; it is the means of destruction. It is true that the production of military hardware requires a vast number of inputs from other sectors of the economy, just like Adam Smith’s pins—but on a much larger scale. This applies to all sophisticated production in a modern, advanced economy.

But there are no other parallels with productive sectors. In strict economic terms, military spending is consumption. This is because military hardware does not add to the means of production or the productive capacity of the economy. In this regard, a missile, fighter plane, or bullet is distinct from a desktop computer, lathe, or microchip. The latter can be used as inputs into the production of other goods or services; military hardware cannot.

Because it is not an input into production, military spending can only be categorised as consumption. It is not even beneficial consumption. Other items categorised as consumption—such as spending on health, education, or social welfare—are vital to the well-being of society. Not all consumption is equal. Some is essential to human development; military consumption is often wasteful or destructive.

This same point—that military spending does not constitute investment and therefore cannot contribute to growth—can also be illustrated using Keynesian economic terms in general usage.

The Military Spending Multiplier

There is an entire body of thought devoted to promoting military spending as an economic benefit, dubbed by its supporters as military Keynesianism. [1] The idea is a vulgarisation of Keynes’ work, suggesting that any type of government spending is beneficial to the economy—and given that military spending also enhances national power and prestige, it should be prioritised.

Fortunately, Keynesian economic analysis itself provides a strong rebuttal to these claims. Central to this rebuttal is the widespread assertion that military spending is jobs-rich. All types of government spending require labour inputs. Military spending is not unique in this respect, although many of its advocates rarely suggest that increased NHS spending or investment in green infrastructure creates jobs at all. Yet, since military spending does not add to the productive capacity of the economy, the labour used in the manufacture of weapons is the equivalent of Keynes’ metaphorical digging holes and filling them in again—it has zero net economic benefit.

In times of high unemployment, even digging holes and filling them in can stimulate wider job creation (which was Keynes’ ironic point). But if the aim is to create better, higher-skilled, higher-wage jobs, there are far more effective ways to spend public money.

The military budget is already one of the largest areas of government expenditure—£53 billion in 2022/23—behind only the Departments of Welfare, Health, and Education.[2] It exceeds the combined spending of the Departments of Housing, Transport, and Work & Pensions. In terms of direct employment, the Ministry of Defence employs just under a quarter of a million military and civilian staff. However, claims that military spending is jobs-rich rely heavily on assumptions about the impact of MoD procurement on job creation in private sector arms industries and related services.

It would be easy to get bogged down in technical analysis here. Thankfully, this work has already been done—in a study for the Scottish Government on employment multiplier effects. This analysis examines the structure of the economy and the relationships between inputs and outputs, including labour. It applies to individual sectors and includes detailed tables for each economic sector.[3]

The key conclusion is clear: military spending has one of the lowest employment multipliers of all economic categories. It ranks 70th out of 100 in terms of employment generated. Health ranks number 1. Sectors ranging from agriculture to energy, food manufacturing, chemicals, iron and steel, computers, and construction all have higher employment multipliers than military spending. Investment in health is two and a half times more jobs-rich than investment in the military.

A recent example illustrates this point. The British government hailed a deal with Norway to construct anti-submarine vessels, claiming it was the largest of its kind in history—worth £10 billion. Yet it was extremely vague on job creation, which can be verified. Officials stated only that the deal would secure 4,000 jobs well into the 2030s. [4] “Secure” is government-speak for no net new jobs created. A similar pattern is evident in many recent announcements about military projects. While ministers are eager to promote the supposed economic benefits of military spending, including claims about job creation across various sectors, none of the specific announcements include figures for net new jobs. There is a very good reason for this.

‘Military Keynesianism’ – A Casualty of War

The idea of military Keynesianism fell into disrepute partly because its advocates not only prioritised military spending but treated it as an exception. In no other sector of the economy did they argue that increased government spending would yield similar benefits.

The decisive turning point came in the real world, when the ideas behind military Keynesianism—and its left-wing variant, the permanent arms economy—were tested to destruction during the Vietnam War. At that time, US governments granted themselves unlimited public and covert budgets to fight the war, nearly bankrupting the federal government in the process. This also led to the collapse of the Bretton Woods economic system and unleashed a wave of global inflation.

A contrary example comes from Britain’s own history. After World War II, West Germany was not allowed to rebuild its armed forces. It was obliged to use its (much smaller) Marshall Plan funds for economic regeneration, leading to a prolonged period of public investment-led growth known as the German economic miracle. Britain, by contrast, faced no such restrictions and spent freely on the military, particularly in support of the Korean War. There was no British economic miracle. In time, Britain became known as the sick man of Europe.

In the present era, the diminished military weight of Western Europe has triggered widespread panic. In the drive to rearm, old and discredited ideas are being revived to justify the diversion of public funds—a blatant case of policy-based evidence-making. These include growing claims about the supposed positive effects of military spending on technology, R&D, and job creation. [5] As we have seen, economic theory, empirical data, and historical experience all show that these claims are not valid.

Practical Considerations, and Opposition in Practice

There are also a number of objective difficulties in implementing the policy of increasing military spending. As the character in the gangster movie says, “Blood is a big expense.” The cost—even before accounting for the toll in human lives—is twofold. First, the shift to a war economy requires significant outlays that cut across society and its existing spending priorities. Second, other forms of production must be halted or redirected toward the war effort.

NATO countries (with the exception of the United States, which has been continuously engaged in military operations since its inception) are attempting to shift to a war economy without undertaking the full, wrenching expenditure and economic redirection that such a shift entails. Either they will have to make that significant wrench, or they will fail in their aim. This tension is reflected in the discrepancy between the 5% target for total aggregate military spending and the 3.5% allocated strictly to military hardware. Additionally, it is questionable whether an increase of 1.5% annual spending on military-related infrastructure will be sufficient to accommodate an effective doubling of Britain’s military capacity remains to be seen. In any case, it will require a sustained annual commitment.

Yet there is a broader challenge beyond infrastructure investment. The required increase is nearly equivalent to Britain’s annual net public investment over the life of this parliament, as outlined in the October 2024 Budget. This challenge is magnified by the fragile state of government finances, even before meeting Trump’s demand for military spending to reach 5% of GDP. Britain has already seen three austerity-driven fiscal events under the current government: the October 2024 Budget, the Spring Statement, and the Spending Review in early 2025.

As with previous austerity packages, these measures have left both the economy and public finances in a worse state, prompting calls from austerity advocates for further tax increases and spending cuts. The traditional mantra—“there is no money left”—is not applied to military spending. But without economic growth and the resulting improvement in public finances, the government will be forced to slash other areas of spending to fund increased military outlays.

Ministers have already indicated a return to cuts in welfare spending, which previously triggered parliamentary rebellions within the Labour Party and imposed a heavy political cost on the current leadership. The Office for Budget Responsibility (OBR) estimates that total government spending will amount to 45% of GDP in the current financial year. The planned increase in military spending demanded by Trump will amount to 2.7% of GDP—an enormous rise.[6]

Clearly, this cannot be funded by cutting military spending or avoiding debt interest payments. Together, these already account for 6.2% of GDP (OBR data). For political reasons, the government has ruled out touching the state retirement pension. Altogether, these commitments total 13.9% of GDP. The increase in military spending must therefore come from the remainder—namely, spending on health, education, public services, and welfare. A series of ministerial statements suggest that welfare payments are the primary target. But given the depth of the fiscal crisis, little else has been ruled out. In effect, disabled people, the poor (including the low-paid), and pensioners will bear the cost of the war drive. In his latest statement, Starmer added that those suffering from mental health conditions would also be affected.

However, there is notable resistance. This was most evident in the parliamentary rebellion over cuts to disability payments, where the government was forced into a series of concessions that angered austerity advocates but still led 47 Labour MPs to vote against their own government.

There is a media furore every time it is hinted that the government may be forced to retreat on planned welfare cuts. The demand to cut welfare is the demand to cut the social wages and thereby lower wages in general. The demand to increase military spending fits with the new political priorities of the US-sponsored drive to war.

Perhaps the most significant resistance came from the recent Trade Union Confederation (TUC) conference. This was significant not only because of the social forces involved, but also because of the direct link made between military spending and welfare cuts. Reversing its previous support for immediate increases in military spending (based on job creation claims), the TUC voted to prioritise campaigning for public investment in services and to “reaffirm our movement’s priority is welfare and wages, not weapons and war.” The vote was close: 2,871,000 in favour, 2,291,000 against.

No one expects the TUC to campaign vigorously on this issue, but the vote leaves the door open for individual unions to work with the wider movement to advocate for the policy. It is highly unusual—but not unprecedented—for the organised labour movement to oppose the key war aims of both the British and US governments, especially under a Labour government. In opposing the Suez War, the National Council of Labour (the TUC and Labour combined) aligned with the US. The first real cracks in union support for Britain’s central war aims came during the Iraq War. The latest TUC vote builds on that legacy.

In Britain and many other NATO countries, there is much talk of public investment. But the reality is different. The announcement from Chancellor Rachel Reeves, following the Treasury’s Spending Review, stated that there would be £725 billion in public investment over the next 10 years. But this is less per year than the £77.6 billion invested in 2024. Public investment is being cut. Once the (smaller) envelope for public investment is set, that then determines the level of funding available for consumption.

Just as in the domestic economy, investment + consumption must equal 100% of output, so public investment + public consumption must account for 100% of public spending.

The inescapable logic is that the government must choose between types of consumption within the reduced funds allocated to it. The Starmer government has made its choice: it cut international aid and welfare to increase military spending. Cutting welfare once more and even reducing painfully low state retirement pensions are now openly discussed.

Essentially, under the current allocation for public consumption, the government chose between welfare funding and military funding. Economically, politically, and morally, it made the wrong choice. Other Western governments have made similar decisions.

Living standards are declining in Britain and across Europe. Commentators note the growing divergence in real incomes between rich and poor in the United States, with European countries now at risk of following that example. Therefore, the material basis for opposition to reckless, wasteful military spending may continue to grow.

The above article was originally published in Polish here by Nasze Argumenty.

[1] Paul Krugman, “Weaponized Keynesianism,” The New York Times (blog), June 24, 2009, archived at https://archive.nytimes.com/krugman.blogs.nytimes.com/2009/06/24/weaponized-keynesianism/

[2] “Public Spending Statistics: February 2024,” GOV.UK, published 28 February 2024, https://www.gov.uk/government/statistics/public-spending-statistics-release-february-2024/public-spending-statistics-february-2024

[4] Jonathan Beale and Jessica Rawnsley, “UK Secures £10bn Deal to Supply Norway with Warships,” BBC News, August 31, 2025, https://www.bbc.co.uk/news/articles/cr5rgdpvn63o

[5] “Higher Defence Spending Could Create Up to 200,000 Jobs in Germany, Says Report,” The Brussels Times, February 17, 2025, https://www.brusselstimes.com/eu-affairs/1447802/higher-defence-spending-could-create-up-to-200000-jobs-in-germany-says-report

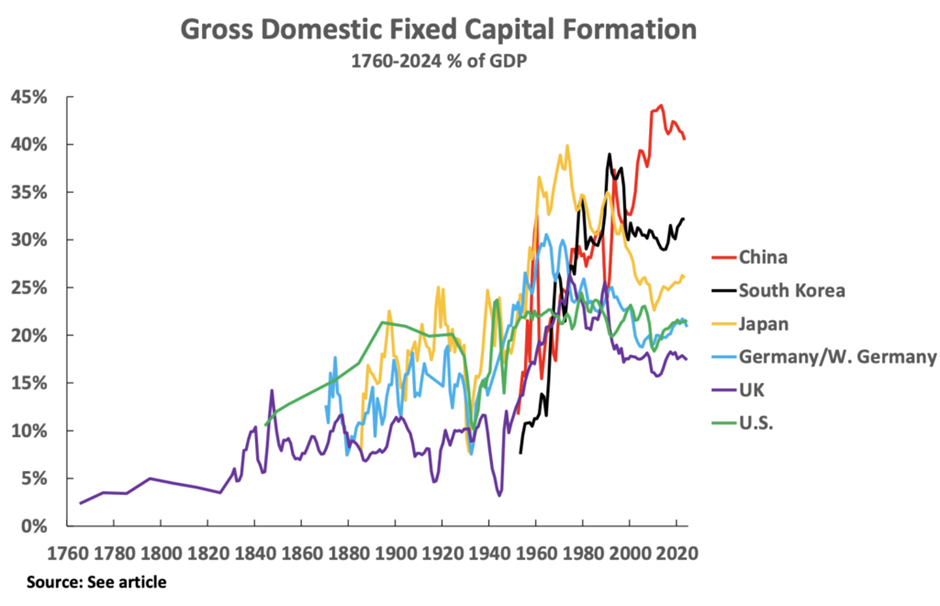

The following article, which shows the sharply rising proportion of fixed investment in the economy in the 250 years since the Industrial Revolution, was written in the context of a specific discussion of China’s economy. This is the claim that China invests too high a proportion of its economy. As the article shows, on the contrary, China’s approximately 40 percent of gross fixed investment/gross fixed capital formation in GDP is merely the latest stage of a process that has been going on for over two centuries. Such a deep process has, of course, profound implications for economic policy—as the article analyzes.

However, the data in this article relates to more general theoretical issues as well as the specific discussion of China. The rising proportion of the economy used for investment is one of the most central predictions of Marx’s Capital—or, as he terms it, the “rising organic composition of capital.” Such a rising proportion of investment in the economy was, less systematically, also predicted by Adam Smith, and by, for somewhat different reasons, by John Maynard Keynes. The attempt by Milton Friedman to refute this was found to be erroneous, even by neoliberals, thanks to modern econometric studies, as discussed below.

In light of this, it is therefore rather astonishing that attempts have been made to refute Marx on the rising organic composition of capital by some of those who claim to be presenting Marx. These critics argue that there is no reason why the proportion of investment in the economy should rise, and that subsequent theoretical work has shown that there is a pattern of technological change between the two sectors (wage goods and means of production) that can keep the ratio of consumption and investment steady in perpetuity.

Such claims mean that, from a theoretical viewpoint, such authors do not understand Marx’s economics. That, however, can be dealt with in a separate article. For present purposes, the issue is one of facts: the rising proportion of investment in the economy is a factual question that can be measured.

In Marx’s analysis, constant capital consists of two parts—circulating capital, which, in modern Western economics, would be termed “intermediate products,” and fixed investment. Factual studies confirmed that the most rapidly growing component of the economy is intermediate products/circulating capital. Thus, for example, in the United States, Jorgenson, Gollop and Fraumeni found: “the contribution of intermediate input is by far the most significant source of growth in output. The contribution of intermediate input alone exceeds the rate of productivity growth for thirty-six of the forty-five industries.”[1]

The same result is found for other economies, including China. For South Korea, Hak K. Pyo, Keun-Hee Rhee, and Bongchan Ha found that regarding intermediate inputs, “the relative magnitude of contribution to output growth is in the order of: material, capital, labor, TFP then energy.”[2] For Taiwan Province of China, analyzing twenty-six sectors in 1981–99, Chi-Yuan Liang found regarding intermediate material inputs were “the biggest contributor to output growth in all sectors during 1981–99, except…seven.”[3] For mainland China, Ren and Sun found that, from 1981 to 2000, subdivided into 1984–88, 1988–94, and 1994–2000, “intermediate input growth [was] the primary source of output growth in most industries.”[4]

However, although the evidence is that circulating capital/intermediate products rises more rapidly than both GDP growth and fixed investment, nevertheless, the facts are clear that there is historically a massive increase in the proportion of fixed investment in the economy—from around 3 percent of GDP in Britain at the time of the Industrial Revolution to 40 percent of GDP in China today. That is, there is also a massive increase in the proportion of the production of means of production in the economy. The facts show a massive increase in the organic composition of capital with economic development. Therefore, not only is it theoretically erroneous that some claiming to represent Marx align themselves with Friedman against Marx, Smith, and Keynes; more importantly, their claims are also entirely against the economic facts.

The data in the article below, which was originally published in Chinese by Guancha, therefore extends beyond the specific issue of China’s current development, to fundamental economic theories of development. Marx’s analysis of the rising proportion of the economy used for investment—that is, the rise of the proportion of the economy used for production of means of production—is one of his greatest achievements and entirely confirmed by 250 years of economic development, including by the 150 years since Marx accurately predicted it.

–John Ross

China’s very high level of investment reflects the historically advanced character of its economy

Accurate analysis of the role of investment in economic development is decisive for China, as it is for every country. The facts that follow confirm this. This applies not only to short-term economic policy but still more clearly to economic strategy—therefore, in particular, to China’s achievement of its goals for 2035 and 2049.

A false claim, a myth, however, is put forward in some sections of the Western media which attempt to obscure such an accurate assessment. This is the claim that China invests too high a proportion of its economy because its level of investment in GDP is much higher than that of Western countries. But in reality, as will be seen, the entire historical period of development since the Industrial Revolution—that is, since the creation of modern economies—has seen progressively higher ratios of investment in GDP. Each successive period has, in turn, been associated with higher economic growth rates. The facts show that China’s high level of investment is simply the latest stage of an international process of economic development that has been underway for over two centuries.

Once this fundamental historical trend is understood, it becomes clear that China’s higher investment rate relative to Western economies is not a problem for China’s economy. On the contrary, it reflects its historically advanced economic structure. China’s gross fixed investment accounts for approximately 40 percent of its economy, whereas the United States’ is only slightly over 20 percent. In the even more important measure of net fixed investment, which takes into account depreciation, China invests 16 percent of its GDP, whereas the United States invests only 5 percent.

As the historical trend below demonstrates, the reason for the difference between China and Western economies is that the level of investment in Western economies is too low for the present global historical stage of economic development. This results in slow growth and consequent social and political instability. In contrast, China’s higher level of investment reflects that it is today the leading part of a process that has been going on since the Industrial Revolution.

The conclusion of this article will consider the implications of this historical trend of the rising proportion of investment in the economy, the faster growth rates that it gives rise to, analysis of the reasons for this trend, and the latter’s policy implications. It will be seen that this trend of the rising percentage of investment in GDP is entirely as predicted by Marx’s analysis of the increasing organic composition of capital—that is, the increasing capital intensity of production.

First, however, before analyzing the implications and following the method of “seeking truth from facts,” the data regarding the historical trend of the rising proportion of the economy used for investment will be clearly established.

Both historical and short-term analyses of the role of investment are consistent

Earlier articles by the present author on these issues used relatively sophisticated econometric methods to analyze the extremely close relation between investment and economic growth over relatively short time frames.[5] This was necessary because, during short time frames, economic growth may be affected not only by the most powerful long-term structural trends that determine an economy’s strategic development, but also by many purely short-term conjunctural fluctuations—business cycles, the impact of non-economic events, and so on. To use an analogy: in examining a short timeframe, it is difficult to distinguish the “signal” from the “noise,” necessitating the use of precise statistical methods to identify the underlying trend amid short-term fluctuations.

In this article a different, simpler method is used to show the clear trend of the rising proportion of investment in the economy. Over long timeframes, short-term, non-fundamental, peripheral, and secondary fluctuations have little effect, and only the most powerful processes dominate, allowing them to be clearly seen without the need for sophisticated econometric techniques. It is therefore hoped that this article, which requires no advanced statistical methods, will make clear to non-specialist readers the fundamental facts regarding the historically rising share of the economy allocated to investment.

It should be made clear, however, that these immediately visible trends neither replace nor contradict the statistical methods used in short-term studies. On the contrary, the two arrive at precisely the same conclusion. The longer-term historical studies provide the context within which the shorter-term processes operate.

The fundamental historical trend

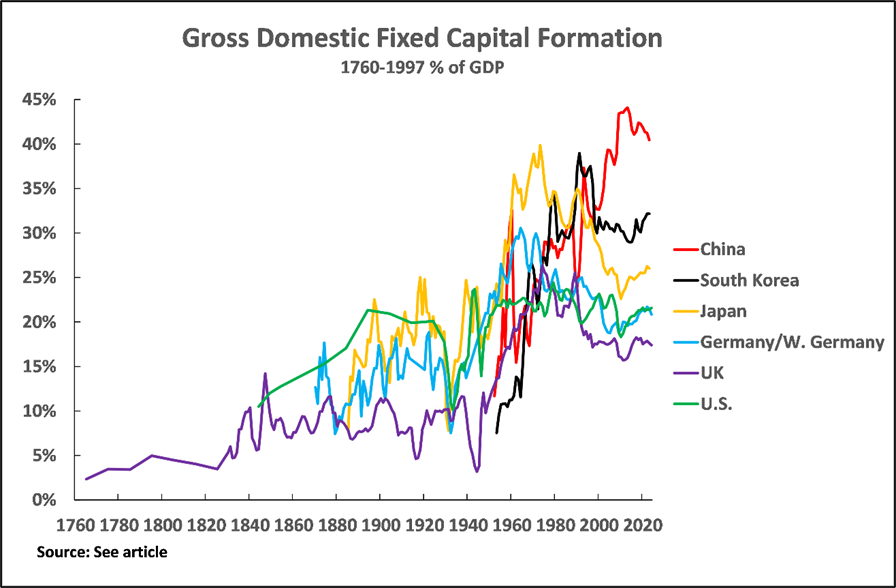

To outline the most fundamental trend first, before considering individual countries in detail, Figure 1 shows the percentage of fixed investment—gross fixed capital formation, to be precise—in GDP in the lead economies in each period of economic development in the approximately 250 years since the Industrial Revolution. The “lead economy” is the major economy which had the fastest rate of economic growth during successive historical periods of economic development—that is, the economy which represented the growth frontier of these successive historic periods.

Figure 1

Figure 1 immediately makes clear that in each successive period, the lead economy had a higher proportion of fixed investment in the economy than the previous one—it will also be shown that each lead economy had a higher sustained growth rate than the previous one.

These lead growth economies, in successive chronological order of their development, were Britain; the United States; West Germany; Japan and South Korea; and China.

As Figure 1 shows, each of these successive lead economies had a higher level of investment in the economy than the one before. This began with Britain, with investment of about 3 percent of GDP at the time of the Industrial Revolution, then rising to 10 percent by the 1830s, followed by gross fixed capital formation of slightly over 20 percent in the United States after the Civil War, then 30 percent in postwar West Germany, over 35 percent in Japan and South Korea, and rising to slightly over 40 percent in China today.[6] It is therefore clear that China’s high level of investment is simply the continuation of a process which has been taking place for 250 years since the Industrial Revolution.

The increasing rate of economic growth

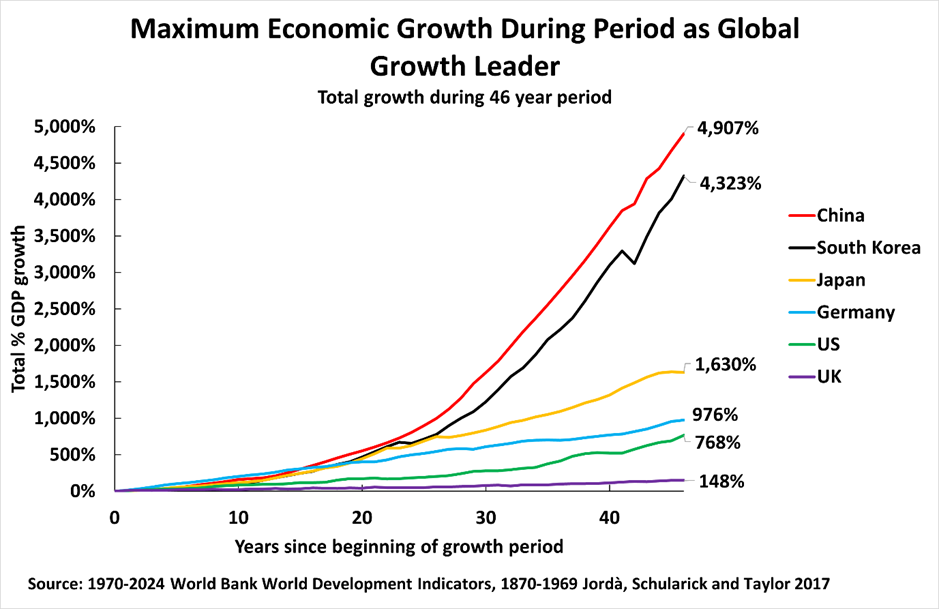

Turning to the growth rates accompanying these increasingly high percentages of fixed investment, the successively faster economic growth rates in each of these periods are shown in Figure 2.

As what is important for fundamental economic development is sustained growth rates, not unsustainable and purely short-term spurts, long-term growth rates are considered here. To be able to make an exact comparison with China since the beginning of Reform and Opening Up, what is considered in each case is the maximum total economic growth achieved over a forty-six-year period during a country’s period of global economic growth leadership (i.e., a period equivalent to China’s growth in 1978–2024). In descending order of growth rate, which is also reverse chronological order, China’s is the fastest, then South Korea, then Japan, then West Germany, then the United States, then the United Kingdom.

Figure 2

Table 1 summarizes these growth rates, showing both the total growth over a forty-six-year period of each of these lead economies and its annual average growth rate during that period. Thus, during its period of global growth leadership, the United Kingdom, the first country to experience the Industrial Revolution and create a modern economy, achieved 2 percent average annual growth, the United States achieved 4.8 percent, West Germany 5.3 percent, Japan 6.4 percent, South Korea 8.4 percent, and China 8.9 percent.[7]

The relation between this percentage of fixed investment in GDP shown earlier and the rate of growth is, of course, one to one. That is, the higher the percentage of fixed investment in GDP the faster the rate of economic growth. In terms of historical development, each historical period saw both a higher level of fixed investment in GDP and a higher rate of GDP growth than the one before.

This data therefore makes very clear that what has been taking place is a 250-year process since the Industrial Revolution of an historically increasing percentage of fixed investment in GDP and an increasingly fast rate of economic growth with progressive economic development. China’s level of investment in GDP (the highest of any major lead economy) and its fast growth rate (the most rapid of any major economy in human history) are therefore not an aberration, but simply the latest stage of this 250-year-long process.

Having shown the overall historic process, each of these lead economies will now be considered in detail—culminating with China.

Table 1 46-year GDP Growth Period China data is 1978–2024. Other states are maximum 46-year growth period after they became the leading growth economy

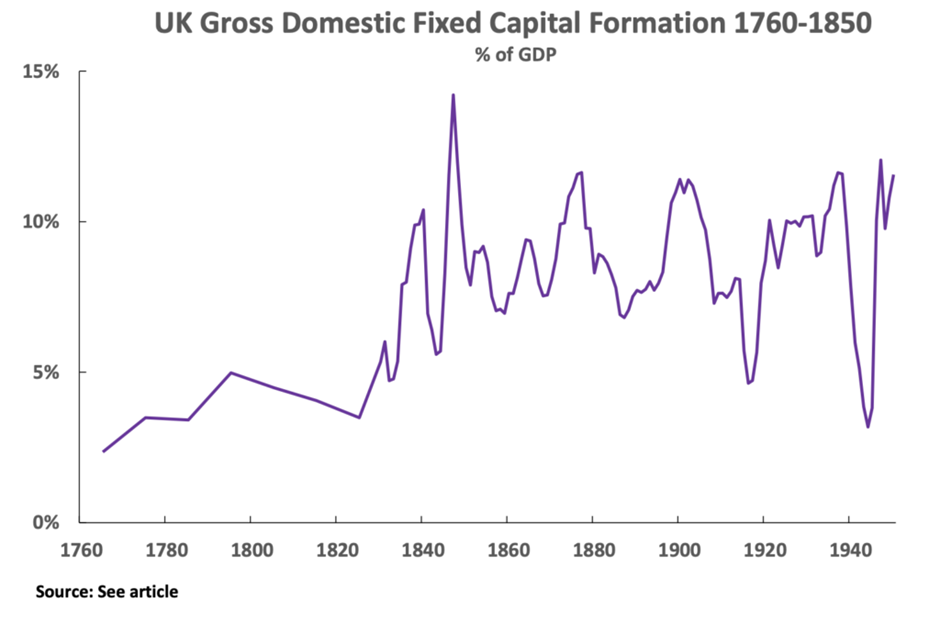

Britain: The first industrial economy

Britain, the first economy to achieve industrialization, raised its level of investment from around 3 percent of GDP on the eve of the Industrial Revolution to 10 percent by the 1830s (see Figure 3), achieving an economic growth rate of 2.3 percent by the end of this period.[8]

Figure 3

During the 18th century and the beginning of the 19th century, Britain experienced economic acceleration, accompanied by introduction of radical new technologies and an increase in the percentage of fixed investment in GDP. [9] By the beginning of the 1820s, Britain had become the largest Western economy (i.e., excluding China and India), but with a per capita GDP almost four times that of China or India.[10] By this process Britain became the first modern industrial state and the world’s most advanced economy.[11]

The percentage of investment in England’s GDP was rising, initially extremely slowly, from the earliest periods for which data exists.[12] The most detailed recent study concludes: “the fixed investment ratio fluctuated at a low level of one to two per cent during the medieval period, increasing to between 2 and 4 per cent during the early modern period. However, the major change was the sharp increase from the mid 18th century, reaching 10 per cent by the early nineteenth century.”[13]

Britain’s economic growth was rapid by Western European standards even before the Industrial Revolution.[14] But the Industrial Revolution saw a qualitative acceleration. Taking ten-year periods to eliminate the effect of purely short-term fluctuations: by the 1780s, British annual GDP growth had reached 1.6 percent, and by the 1830s, 2.3 percent.[15] This secured the United Kingdom’s lead position in the world economy, already analyzed.

This rising trend in the share of gross fixed capital formation in the UK from the Industrial Revolution to 1950 is shown in Figure 3. The increase in the percentage of investment in GDP—a tripling or quadrupling, depending on the calculation made about the initial starting point—was of course enormous for this historical period, but only achieved a low level compared to later historical development.

In summary, from the 1760s to the 1830s, essentially covering the period of the Industrial Revolution, taking ten-year annual averages, Britain increased its percentage of investment in GDP from 3.3 percent to 10.5 percent and increased its annual average economic growth rate from 0.6 percent in 1700–60 to 2.3 percent. This established Britain as the leading economic state of the world.

The fact that Britain’s domestic investment did not progress beyond approximately 10 percent of GDP for a century from the 1830s then played a decisive role in Britain’s being overtaken by the United States as the world’s leading economy, as will be seen in the next section.

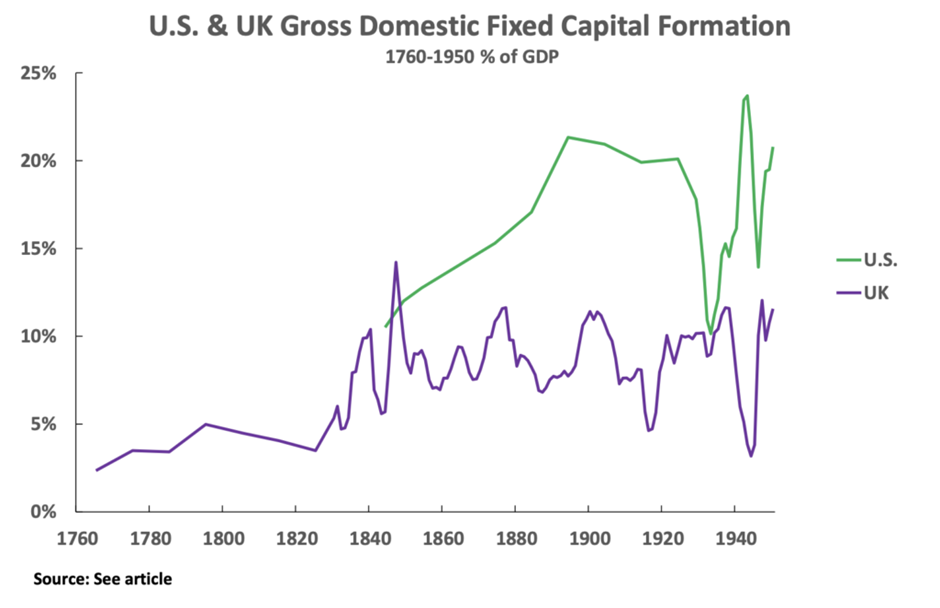

The United States overtakes the United Kingdom

The United States of course overtook Britain during the 19th century to become the leading international economy. The United States showed the next step upward in both the percentage of investment in GDP and the economic growth rate.

At the time of Britain’s Industrial Revolution, the United States was not among the world’s largest economies.[16] In 1775, Britain’s economy was almost 6 times larger than that of the United States.[17] Economic historians differ on the immediate development of the U.S. economy after independence, but by 1820, the most recent estimate is that the U.S. economy was still only 38 percent the size of the United Kingdom’s.[18] However, by 1840, the U.S. economy was already more than half the size of the United Kingdom’s, and by 1850, it was 73 percent, with a higher growth rate as well as a higher level of investment in GDP.[19] By the 1840s, therefore, the United States was already the most rapidly growing major economy; further U.S. economic acceleration after the Civil War was a continuation of this process. For that reason, the date of the United States’ becoming the major lead economy globally in terms of growth is taken here as dating from the 1840s—although it will be shown that taking a later date, for example, after the Civil War, makes no difference to the essential pattern. In terms of total GDP, the United States overtook Britain in the 1860s or 1870s, and by 1900, its total GDP was almost double that of the United Kingdom.[20]

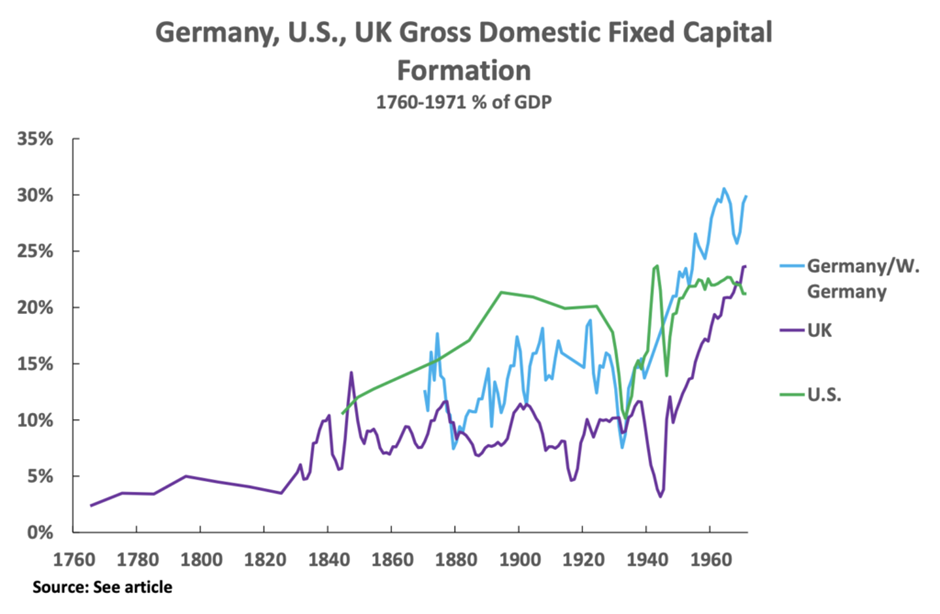

Estimates for gross investment as a percentage of the U.S. economy are, unfortunately, not available for the period of the onset of Britain’s Industrial Revolution—they only become available in current prices from the period 1839–1848. By then, the U.S. level of investment already exceeded the UK: the share of gross national capital formation in U.S. GDP was 14 percent. During the course of the 19th century, the percentage of fixed investment in U.S. GDP rose sharply, eventually far surpassing that of Britain. U.S. gross capital formation oscillated between 14 percent and 16 percent of GNP until 1858, the eve of the Civil War. After the Civil War, this level then rose rapidly to far exceed the UK level. By 1869–78 the U.S. level was 19 percent of GDP; by 1879–1888, 21 percent; and by 1888-98, 23 percent (see Figure 4, which compares the United States and the United Kingdom).[21] This historically unprecedented U.S. investment boom, which had no equal in world history until that time, particularly following the Civil War, transformed the American economy.[22]

Figure 4

In summary, the United States surged to global leadership based on a level of investment in GDP that at that time had no precedent in world history. The advantage of the United States over other economies in fixed investment continued for a prolonged period. As Maddison notes: “The rate of U.S. domestic investment was nearly twice the UK level for the sixty-year period 1890–1950. Its level of capital stock per person employed was twice as high as that of the United Kingdom in 1890, and its overwhelming advantage in this respect over all other countries continued until the early 1980s.”[23]

As a result, from 1840 to 1950, the United States grew at an average annual rate of 3.9 percent—over 50 percent higher than the rate of British GDP after the latter had accelerated following the Industrial Revolution. [24]

The approximate level of fixed investment reached after the U.S. Civil War, slightly over 20 percent of GDP, with only a short-term catastrophic collapse during the Great Depression, was sustained, and still existed in the United States 140 years later, in the 2020s. The fact that, after far surpassing its British rival by the late 19th century, the United States did not increase its investment-to-GDP ratio for nearly a century and a half is crucial for explaining numerous trends in the modern world, as will be analyzed below.

For approximately a century, in particular from the end of the Civil War to the immediate aftermath of the Second World War, the U.S. level of investment of slightly over 20 percent of GDP was the highest of any major economy and the United States was the world’s most rapidly growing major economy. From 1850 to 1950, the average annual GDP growth rate of the United States was 3.8 percent, Germany and Japan 1.7 percent, and the United Kingdom 1.6 percent.

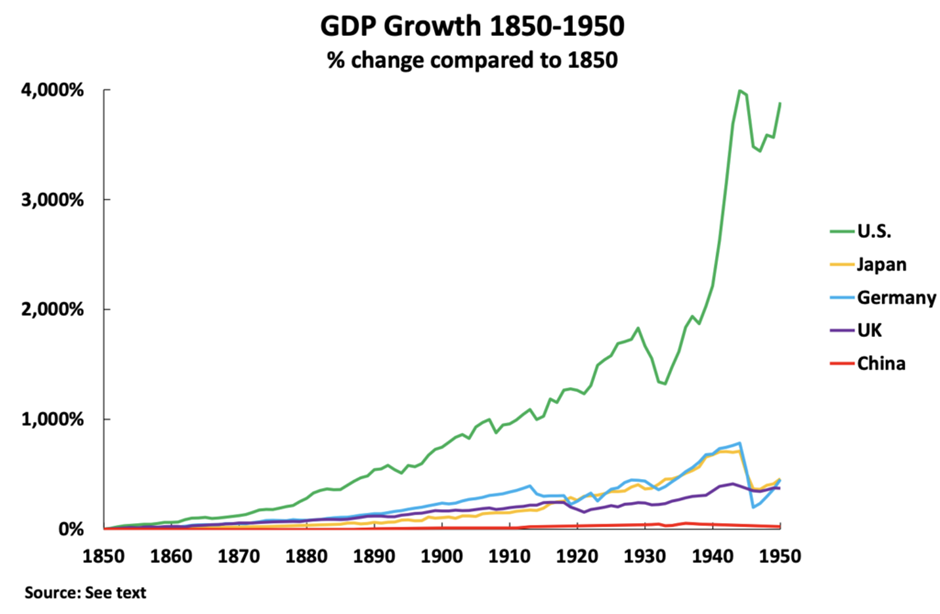

The cumulative effect of such growth rates sustained for almost a century was overwhelming in establishing U.S. dominance. From 1850 to 1950, the U.S. economy increased in size by 3,880 percent, Japan’s by 460 percent, Germany’s by 450 percent, and the United Kingdom’s by 370 percent (see Figure 5).

Figure 5

With total growth over eight times as great as any major competitor, laying the base for defeating both Germany and Japan in the world wars, the economic dominance of the United States in the period up to 1950 was crushing.

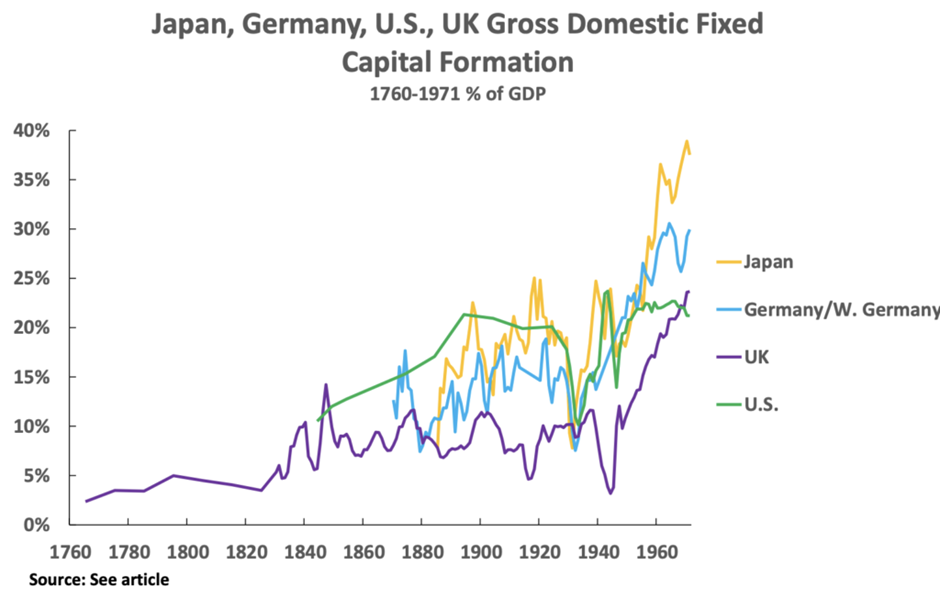

West Germany becomes the first major advanced economy to overtake the U.S. growth rate

Given this U.S. growth dominance for over a century, it was therefore a crucial historic development after the Second World War that, for the first time, a series of major economies began to see levels of investment of significantly over 20 percent of GDP, i.e., above the U.S. level, and achieved more rapid economic growth than the U.S.

The first of these economies was West Germany. By 1955 West Germany had achieved a level of gross fixed capital formation of 26.5 percent of GDP, above the U.S. level, and by 1964 this rose to 30.5 percent (see Figure 6). The United States then launched a major counteroffensive against Germany in the 1960s and 1970s, particularly with U.S. abandonment of the convertibility of the dollar to gold and the end of the Bretton Woods currency system in 1971.[25]

Figure 6

From 1950 to 1971, West Germany achieved an average annual GDP growth rate of 5.9 percent—the first time in history a major economy had grown faster than that of the United States over a sustained period. Despite the sharp fall in the percentage of investment in West German GDP after 1971 and a deep fall in its growth rate, West Germany/Germany still outgrew the United States with a 5.3 percent annual average growth rate during this period, due to West Germany’s very high level of fixed investment, in the forty-six-year period from 1946 to 1992.

The fast-growing East Asian capitalist economies

The second major economy after West Germany to achieve a higher level of fixed investment in GDP and a far higher growth rate than those of the United States was Japan. Japan achieved an even higher percentage of fixed investment in GDP, and a faster growth rate, than West Germany. By 1960 Japan’s gross fixed capital formation was 33.2 percent of GDP and by 1971 it was 37.5 percent (see Figure 7). As with West Germany, Japan was also struck by the U.S. counteroffensive in 1971 as U.S. abandonment of dollar-to-gold convertibility led to a sharp decline in Japan’s percentage of investment in GDP and a sharp economic deceleration. Japan, however, became the first economy to achieve a level of investment of over 35 percent of GDP and over a 46-year period, its annual average GDP growth rate was 6.4 percent.

Figure 7

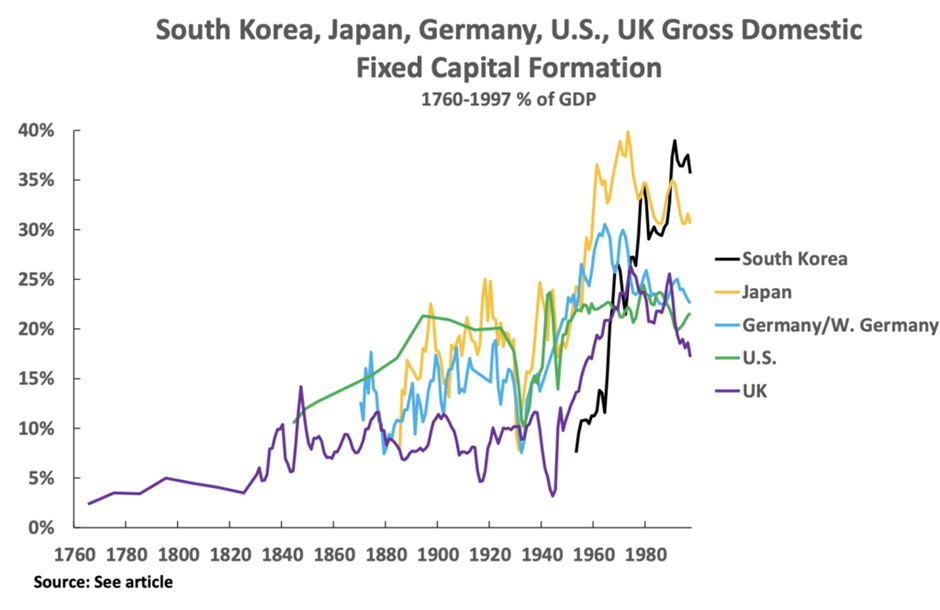

From the late 1970s onward, Japan’s level of fixed investment was matched by the so-called Asian Tigers: South Korea, Singapore, Hong Kong, and Taiwan Province of China. As South Korea is the largest of this group, it will be analyzed in detail.

Starting from an extremely low level of fixed investment in GDP in the early 1950s, by 1979 South Korea’s level of gross fixed capital formation in GDP had reached 35 percent (see Figure 8). This similar pattern of Japan and the Asian Tigers formed what might be termed the “East Asian rapid capitalist growth model.” In 1997 South Korea was struck by another U.S. counteroffensive in the form of the East Asian debt crisis, in the same way that West Germany and Japan had been struck in 1971.This led to a fall in the percentage of fixed investment in South Korea’s economy and a sharp decline in its growth rate.[26] Nevertheless, South Korea’s annual average GDP growth, during its most rapid forty-six-year period of growth, was 8.4 percent.

Figure 8

Socialist China

From 1978, with Reform and Opening Up and the construction of a socialist market economy, China attained the fastest rate of growth of any major economy in history. China’s level of gross fixed capital formation in GDP reached over 40 percent of GDP (see Figure 9), and its annual average growth rate from 1978 to 2024 was 8.9 percent.

Figure 9

This extremely high level of fixed investment in GDP and very fast growth rate differentiate China’s economy from Western economies today. However, it is entirely clear from the preceding data that China’s level of investment and growth rate is neither an “aberration” nor a “miracle” but simply the latest and most advanced stage of a process of the rising share of investment in the economy—that is, of the rising organic composition of capital—that has been taking place for over 250 years since the Industrial Revolution.

Conclusions

As stated at the beginning, the aim of this article is to make clear the historical process of the rising proportion of investment in the economy. It does so by taking the entire period of economic development since the Industrial Revolution, without the need to use sophisticated statistical techniques to separate powerful long-term processes from purely short-term shifts. Doing so has made clear that China’s high level of investment in GDP is merely the latest stage in an historical process which has been taking place for more than two centuries.

Because this is such a deep-rooted economic process, one confirmed by short-term studies and entirely consistent with the predictions of economic theory, it is clear that this historical trend will not stop with China’s current development. In the future, economies will develop that will invest more than 40 percent of GDP. The only issue is whether China will continue to lead this historical process or if another economy will do so. That, in turn, will be determined by China’s own policy choices.

Numerous consequences follow from this historically rising proportion of investment in the economy. For reasons of space, only a few of the most important can be summarized here; others will be dealt with, or have already been dealt with, in separate articles.

Clearly, there is no ambiguity as to the trend of the rising proportion of investment in the economy with historical development. This trend was predicted by Adam Smith, particularly analyzed by Marx (as the rising organic composition of capital), and again predicted by Keynes. While this article, for reasons already stated, has examined an extremely long historical period, this factual conclusion of the rising proportion of fixed investment in the economy is confirmed even by those opposed to both Marx and Keynes and who consider different timeframes.

For example, Barro (who, together with Lucas and Sargent, is one of the founders of New Classical Macroeconomics and of the theory of rational expectations) surveyed trends since 1870. He arrives at exactly the same conclusions: “For the United States, the striking observation…is the stability over time of the ratios for domestic investment and national saving…. The United States is, however, an outlier with respect to the stability of its investment and saving ratios; the data for the other…countries show a clear increase in these ratios over time. In particular, the ratios for 1950–89 are, in all cases, substantially greater than those from before World War II. The long-term data therefore suggest that the ratios to GDP of gross domestic investment and gross national saving tend to rise as an economy develops.”[27]

In short, despite Barro’s overt opposition to Keynes and his attempt to totally ignore Marx, he is forced to arrive at the same economic conclusions as outlined above.

This more than 250-year historical pattern confirms the clear positive correlation between the percentage of investment in GDP and the rate of economic growth—that is, an increasing proportion of investment in the economy is accompanied by rising economic growth rates. The historical trend shown above is consistent with the strong positive correlation in large economies between the percentage of fixed investment in GDP and the economic growth rate during the most recent periods.[28]

The fact that systematic measures of net fixed capital formation, as opposed to only gross fixed capital formation, are available for more recent economic periods simply means that modern studies establish this extremely strong positive correlation between the percentage of fixed investment in GDP and the economic growth rate still more clearly than the long-term historical studies used here. For large economies, the recent correlation between the percentage of net fixed capital formation in GDP and the economic growth rate is over 0.9, i.e., as close to a perfect correlation as will be found in any real economic process.[29]

This strong positive historic correlation between the percentage of fixed investment and economic growth is entirely that which would be predicted by economic theory. This is because capital is an input into the production function in both Western and Marxist economic theory.[30] Therefore, increasing the proportion of the economy used for investment, by increasing inputs of fixed capital, would be predicted to increase the economic growth rate—precisely as confirmed by both historical and short-term studies.

The obverse of this positive correlation between the percentage of fixed investment in GDP and the economic growth rate is that the lower the percentage of fixed investment in GDP, the slower will be the economic growth rate. This is entirely confirmed by the facts.[31]

The consequences of raising the level of consumption in GDP are therefore clear. As investment plus consumption constitutes 100 percent of the domestic economy, increasing the percentage of consumption in GDP, because it necessarily means reducing the proportion of investment, will slow economic growth. Arguments in favor of increasing the proportion of consumption in China’s GDP are therefore, in fact, arguments in favor of slowing China’s rate of economic growth.

Furthermore, because there is an extremely strong positive correlation between the rate of growth of GDP and the rate of growth of consumption, an argument for increasing the percentage of consumption in GDP, by reducing the economic growth rate is, in fact, an argument in favor of slowing the rate of growth of consumption/living standards. This is why there exists a factual negative correlation between the percentage of consumption in GDP and the growth rate of consumption—that is, the higher the percentage of consumption in GDP, the lower will be the growth rate of consumption.[32]

This fact—that increasing the percentage of consumption in GDP leads to slower GDP growth—is in line with economic theory. Consumption, by definition, is not an input into production. Therefore, raising the percentage of consumption in GDP, which necessarily lowers the percentage of investment in GDP, means replacing something which is an input into production (investment) with something which is not an input into production (consumption). Lowering inputs into production necessarily lowers the economic growth rate. As the growth rate of consumption is strongly positively correlated with the GDP growth rate, lowering the rate of economic growth necessarily lowers the consumption growth rate.

From the viewpoint of verifying or falsifying economic theories, the historical data clearly and entirely confirms Smith’s, Marx’s, and Keynes’s conclusion that the percentage of fixed investment in GDP rises with economic development. Referring to investment as part of constant capital, Marx noted that “this law of the progressive increase in constant capital, in proportion to the variable, is confirmed at every step.”[33] Marx’s analysis, developed in the 1860s at a time when, compared to the present day, the level of fixed investment was very low, and which therefore predicted almost over 150 years of economic development, is clearly a work of historical genius. It is also a strong confirmation of Xi Jinping’s analysis that “our study of political economy must be based on Marxist political economy and not any other economic theory.”[34]

These economic facts clearly affect the type of stimulus programs which are required in China. The trends outlined above are fundamental and strategic—i.e., medium to long-term ones. They do not contradict the fact that, to deal with shorter-term economic fluctuations, consumer stimulus may be required. But strategically the rate of China’s economic growth depends on its high level of investment. Short-term stimulus must fit with this economic strategy.[35]

Increasing capital intensity of production is a key foundation of Justin Yifu Lin’s New Structural Economics (NSE). It is clear from the historical data given above, from shorter-term studies considered elsewhere, and from the factual studies carried out even by anti-Marxist and anti-Keynes economists, that this foundation stone of NSE is correct. That is, the historical development of production, and the advance to more developed stages of economic production, is one of increasing capital intensity of production. This confirms that NSE is entirely consistent in this respect with the economic facts and the conclusions on this reached by Smith, Marx and Keynes. Any theory which, unlike NSE, does not arrive at a conclusion of the rising capital intensity of production with economic development is not in line with the facts.

Finally, why are obviously correct things rejected?

But all these facts raise an obvious question. That investment rises as a proportion of the economy with economic development is unequivocally confirmed by historical data, by short-term studies (even by anti-Marxist and anti-Keynes analysts), and by economic theory. Why, therefore, are attempts made to deny this entirely clear fact? And why are attempts made to deny their practical consequences for China?

The first is conscious and unconscious Western arrogance. Factual comparison of economies immediately reveals that the structure of China’s economy, in terms of the level of investment, is different to that of a Western economy. But China’s annual average economic growth is around 5 percent and that of the United States is slightly above 2 percent. Any objective judgement, therefore, would logically conclude that China’s structure was superior to the West’s in producing economic growth.

But seeing that China’s economic structure differs from the West’s, Western commentators are immediately led to the entirely illogical conclusion that it must be China’s economic structure, not the West’s, which is the problem! Instead, the fact that China’s level of investment is much higher than that of Western economies should logically lead to the conclusion: Yes, of course, China is different. Of course China does not correspond to the average. Because China’s is a much more rapidly growing economy than the West. If China had the same economic structure as the West, then it would slow down to the same low speed as the West! The problem is therefore not China’s high level of investment, with its fast growth rate. China is just the latest stage in a process which has been going on for 250 years, since the Industrial Revolution, of a rising proportion of the economy which is used for investment.

China’s economy generates more rapid economic growth and more rapid growth of consumption. The problem is with the Western economies, which have fallen behind the historical trend of the rising percentage of investment in GDP and are therefore trapped in slower growth.

But Western arrogance means it is impossible for them to understand or admit that it is China’s investment level which is superior, and the continuation of a fundamental trend of economic development, and it is the Western economies which are falling behind.

An example: The illogicality of Goldman Sachs

To take a precise example: Goldman Sachs projects that China’s GDP growth will fall sharply to an average 3.4 percent in 2023–32. The reason for this alleged slowdown is because the annual increase in GDP growth created by capital investment is projected to fall by 2.4 percent. And, in turn, the reason for this predicted sharp slowdown is that, Goldman Sachs argues, China’s level of investment in its economy will fall sharply: “Investment as a share of GDP is forecast to decline from 42 percent in 2022 to 35 percent by 2032.”

The reason this will happen is allegedly because China’s level of investment is higher than other economies at a similar level of development. China is at present an upper middle-income economy, although approaching the level of a high-income economy, by World Bank standards, and “investment as a share of GDP in upper-middle-income countries is 34 percent.” Thus, it is argued that China should reduce its level of investment and slow down to the growth rate of other economies.

Why on earth should China do this? China is producing a more rapid increase in average living standards than these Western economies, it is creating more rapid economic growth, it has produced a more rapid reduction in poverty than they have, and so on. The economy with the most rapid economic development is, of course, different from countries with slower economic development. But China is different precisely because it is in line with a trend in economic development, which has been occurring for over two centuries,

A comparison will make the ridiculousness of the argument, and the unconscious Western arrogance, clear. Suppose a company wanted to enter a new industry and asked Goldman Sachs for advice, and Goldman Sachs reported: “In this industry one company is clearly growing much more rapidly than the others. Therefore, you should not learn from this more rapidly growing company, you should copy the more slowly growing companies.” Everyone would laugh at such a proposal—just before they cancelled the contract with Goldman Sachs. But in terms of country-level comparisons, that is exactly what is being proposed.

The only reason the absurdity of these arguments is not immediately clear is the conscious and unconscious arrogance of Western analysts, which makes them think that if there is a difference between China and the West, it must be the West which is correct, even if the objective evidence is to the contrary. That this is Western arrogance is transparently obvious, because the purely economic arguments are so fallacious and contrary to the facts of historical development.

Conclusion

China’s high level of investment is not an aberration. It is the latest stage of an economic process which has been taking place for 250 years since the Industrial Revolution. It is a sign of the historically advanced character of China’s economy, and its development, in a specific national situation, is in line with historical trends.

Notes

[1] Jorgenson, Gollop, and Fraumeni 1987, 200. More precisely, Jorgenson, Gollop, and Fraumeni found: “The contribution of intermediate input is by far the most significant source of growth in output. The contribution of intermediate input alone exceeds the rate of productivity growth for thirty-six of the forty-five industries for which we have a measure of intermediate input…. If we focus attention on capital and labour inputs, excluding intermediate input from consideration, we find that the sum of contributions of capital and labour inputs exceeds the rate of productivity growth for twenty-nine of the forty-five industries for which we have a measure of productivity growth…the predominant contributions to output growth are those of intermediate, capital and labour inputs. By far the most important contribution is that of intermediate input.”

[2] Pyo, Rhee, and Ha, 2007.

[3] Liang 2007.

[4] Ren & Sun, 2007.

[5] See for example 从210个经济体大数据中,我们发现了中国和世界经济增长的密码 https://www.guancha.cn/LuoSiYi/2024_10_05_750743.shtml.

[6] If shorter time periods were used, the Soviet Union would be included because of its rapid growth in the 1930s—its 6 percent annual average growth from 1929 to 1939 was the fastest of any major economy (calculated from Maddison, 2010). This was accompanied by an internationally unprecedented increase in the share of investment in GDP: “the share of gross investment in the national product (measured at 1937 ruble factor cost) went up from roughly 12 per cent in 1928 to nearly 26 per cent in 1937” (Erlich, 1967). However, Soviet longer-term economic growth was greatly reduced by the catastrophic losses during the Second World War. In the immediate postwar period, Soviet economic growth was again fast, but not as fast as Japan—so the Soviet Union can only be considered the global growth leader in the 1930s.

[7] If the starting data of 1968 is taken then, due to the fall in GDP during the Cultural Revolution of the late 1960s, China’s growth rate would be even higher. However, to avoid any suggestion of artificially increasing rates, here only China’s growth from 1978 onwards is considered.

[8] As Britain was the first modern industrial economy, the processes leading to its early development have been intensively studied. There is debate among historians as to the exact dating of the onset of the Industrial Revolution, of detailed estimates of its economic growth rates, and the percentage of fixed investment in GDP during it—also whether it should be best described as a “revolution” or rather as a more gradual cumulative process. But for present comparative historical purposes, these differences are inconsequential, since all estimates are so low by the standards of a modern economy that they clearly indicate the subsequent historical trend.

[9] In terms of technology, individual examples of what constituted advanced machinery for that period began to be introduced from the early 18th century—machinery being fixed investment. The Newcomen steam engine, the first steam-powered pump, was introduced in 1712, the flying shuttle was introduced in 1733, and the first spinning machine was introduced in 1764. The beginning of the development of steam-powered railways, which required a significantly higher level of capital expenditures, began from 1804. Systematic introduction of machinery into textile production, considered the technological commencement of the Industrial Revolution, began in the last third of the 18th century. Railway construction, entailing a further significant increase in fixed investment, began soon after the start of the 19th century.

[10] Calculating from the data in Bolt and Zanden 2020, measured in 2011 PPPs, the United Kingdom’s GDP in 1820 was 70 billion, compared to 57 billion for France, 51 billion for what became Italy, 50 billion for what became Germany, and 27 billion for the United States. Per capita GDP for the United Kingdom in 1820 was 3,306 compared to 882 for China, a ratio of 3.7:1.

[11] Detailed figures for Britain from the most recent comprehensive studies are used here, but alternative estimates would not alter the qualitative trend relative to subsequent developments.

[12] This process began to occur even before the capitalist revolution of 1642–49, and the sharp increase that occurred during the Industrial Revolution. The percentage of fixed investment in GDP is estimated to have risen from about 1.8–1.9 percent of GDP around 1300 to approximately 2.5 percent of GDP by 1760 as the Industrial Revolution commenced (Broadberry and Pleijt 2021, Figure 5). Strikingly, and equally in line with Marx’s analysis, the proportion of fixed capital relative to working capital also rose during this period.

[13] Broadberry and Pleijt 2021, 23. In detail, the earliest data analysed to obtain a realistic account of the structure of the British economy date from 1688, shortly before the systematic introduction of advanced machinery. The first systematic estimates of investment as a percentage of British GDP during the early phase of this process of industrialization ranged from 2.5 percent to 5 percent, but more recent studies have tended to lower that figure still further (Broadberry and Pleijt 2021). The percentage of domestic investment in British GDP (“Domestic investment = fixed investment + stockbuilding” (Broadberry and Pleijt 2021, 36) then began to rise much more rapidly, from 3.3 percent in the 1760s to 7 percent in the 1790s, then fell slightly during the period surrounding the Revolutionary and Napoleonic Wars with France, before rising again to 7.5 percent in the 1830s, and reaching 10.5 percent by the 1840s (see Figure 4). It then failed to rise significantly above this level for almost one hundred years. The data for the period of the Industrial Revolution is from Broadberry and Pleijt 2021.

[14] Britain had an average annual economic growth rate of 0.6 percent between 1600 and 1700, compared with a Western European average of 0.2 percent – calculated from (Maddison, 2010). Broadberry, Campbell, Klein, Overton, and van Leeuwen 2015 gives a slightly higher estimate of British economic growth in 1600–1700 (0.7 percent), but does not provide a comparable estimate for Western Europe for the same period.

[15] Broadberry, Campbell, Klein, Overton, and van Leeuwen 2015, 199, Table 5.03.

[16]Leaving aside China and India, the largest economies globally after Britain in this period were those of France and what would later become Germany and Italy.

[17] For the U.S. interpolating the data of (U.S. Census Bureau., 1975.) for 1770 and 1780 gives a population of 2.5 million, while (Maddison Project, 2023) gives a GDP per capita in 2011 PPPs of 2,419—giving a total GDP of 6.0 billion. For the UK (Bank of England, 2024) gives the population of Great Britain as 8.21 million while calculating from the data of (Gráda, 1979) gives a population of 4.0 million, while (Maddison Project, 2023) give a per capita GDP of 2,895— a total GDP of 35.4 billion.

[18] Lindert and Williamson 2012, Table 4 shows a decline in 1840 constant dollar prices of per capita real incomes, from $85.26 in 1774 to $68.22 in 1800—i.e., a drop of 20 percent, implying a sharp economic contraction. However, Maddison Project 2023, based on calculation from McCusker and from Sutch 2006 gives, in 2011 PPPs, U.S. per capita GDP of $2,419 in 1775 of and $2,545 in 1800, which implies an extremely slow 0.2 percent annual increase averaged over the period. “38 percent the size of the United Kingdom’s”: calculated from Maddison Project 2023.

[19] Calculated from Maddison Project, 2023.

[20] Calculated from Maddison Project 2023, it was 96 percent higher.

[21] Gallman and Rhode 2020, Table 1.3

[22] From 1868 to 1892, 115,960 miles of railways were constructed—four times the total investment in railway construction and equipment compared to the period from 1840 to 1870. Capital per manufacturing establishment more than doubled from $8,400 in 1870 to $18,400 in 1890 (U.S. Census Bureau 1975.)

[23] Maddison 1991, p. 40.

[24] Calculated from Johnston and Williamson 2025.

[25] For a detailed analysis of this process, see 它曾成功“谋杀”了德国、日本、四小龙,现在想要劝中国“经济自杀.”

[26] See 它曾成功“谋杀”了德国、日本、四小龙,现在想要劝中国“经济自杀.”

[27] Barro and Sala-i-Martin 2004, 40.

[28] See, for example, 从210个经济体大数据中,我们发现了中国和世界经济增长的密码.

[29] See 从210个经济体大数据中,我们发现了中国和世界经济增长的密码.

[30] For a more detailed analysis of this see 误读提振消费策略,对中国应对美国竞争非常不利. In a Marxist production function, it is part of constant capital, which, with living labor, is one of the two inputs into production, and in “Western” economics, it is, with living labour and total factor productivity (TFP), one of the determinants of production.

[31] For detailed statistics on this, see 从210个经济体大数据中,我们发现了中国和世界经济增长的密码 and 误读提振消费策略,对中国应对美国竞争非常不利.

[32] For the detailed data on this, see 罗一和吉塞拉·塞尔纳达斯:从210个经济体大数据中,我们发现了误解促消费对经济的危害 and 误读提振消费策略,对中国应对美国竞争非常不利.