Through tremendous sacrifices China has brought the coronavirus under control – the number of new daily cases being reduced from the peak of 3,887 on February 5 to 11 on March 13 (7 imported from outside China), a decline of 98.2 percent. In doing so, the Chinese authorities performed an enormous service not only to the Chinese people but also gave a crucial opportunity to the whole rest of the world to prepare.

To precise, through the determined fight against the virus, China bought almost two months warning to the rest of the world before the coronavirus began to significantly spread there. But the terrible truth is that while China benefited greatly from determined action against the virus, the facts show the West entirely wasted this precious time.

Because the huge economic effect of the coronavirus cannot be separated from its medical impact, it is necessary to study the two together. This is due to the fact that the coronavirus is simultaneously a supply and demand side economic shock. The supply side shock is that the health risk means the work force cannot produce normally, causing huge falls in output. The demand side effect is that significant numbers of services and goods, if they are not consumed in the short term, will not be purchased at all – particularly in the service sector. The falls in China’s official manufacturing PMI, to 35.7 in February, and the non-manufacturing PMI to 29.6, reflected this impact within China.

The facts show clearly that the spread of the virus in the West is now already reaching levels far higher than at the worst point of the crisis in China. As will be demonstrated, nothing short of a disaster is now unfolding in Europe. The situation in the U.S., so far, is following Europe with a delay of about 10 days.

This fact that the intensity of the coronavirus crisis in Europe is already worse than at the worst period of the virus in China is concealed by misleading comparisons of the absolute number of cases in Europe compared to China. But, for example, China’s population is 17 times larger than Germany or 23 times larger than Italy. To realistically measure the relative impact of the coronavirus crisis in Europe compared to China, it is necessary to measure the virus’s spread in proportion to population.

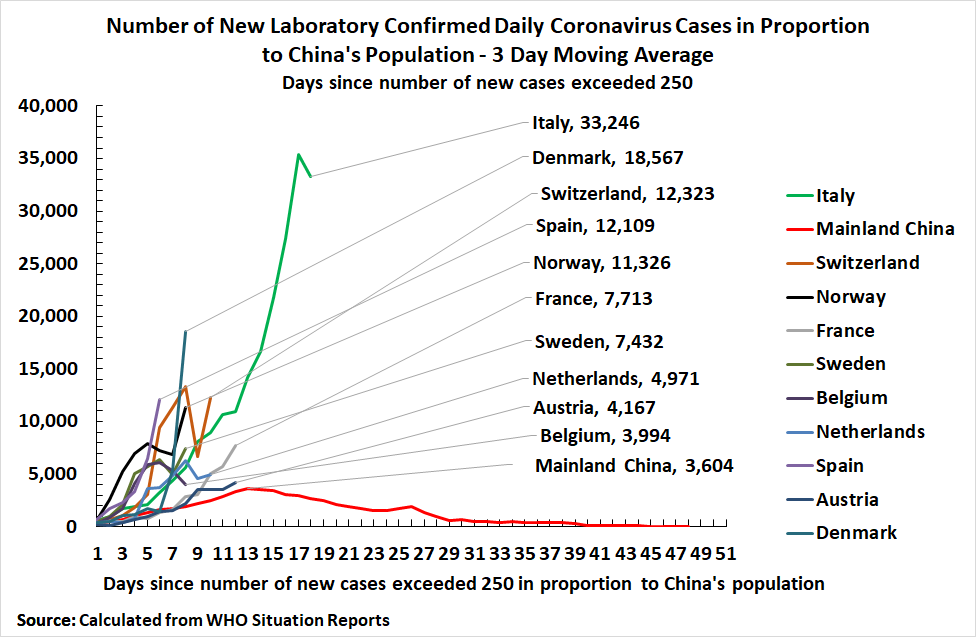

The peak day for the number of new virus infections in China was February 5 at 3,887. But according to the World Health Organization’s daily situation reports, at the time of writing the peak day in France (780 on March 13) was equivalent to over 16,000 relative to China’s population, in Spain (1,266 on March 13) over 38,000, and in Italy (2,651 on March 12) over 60,000.

Western governments are openly telling their populations that it is only a matter of time before the number of deaths becomes very high. British Prime Minister Johnson announced: ‘Many more families, are going to lose loved ones before their time.’ Italy’s cumulative death toll (1,400 as of March 14) would be equivalent to around 33,000 in a country with China’s population!

This data makes clear Europe’s situation is already far worse than at the worst period in China. In short, the European governments totally failed to use the time they had to prepare for the virus to arrive.

The virus’s huge economic impact in the West follows from this medical disaster. Data on the impact on production of the virus in the West is not yet available. But the Western economies were already weakening when the coronavirus hit. The peak of the current U.S. and EU business cycles was in the second quarter of 2018. From then until the fourth quarter of 2018, the U.S. GDP growth had fallen from 3.2 percent to 2.3 percent, and the EU’s from 2.5 percent to 1.2 percent. Without an extraordinary stroke of luck the virus hitting already slowing Western economies will push them into recession.

As Western companies had already accumulated very large debts any resulting revenue slowdown, creating difficulty to repay this debt, carries a risk of transmission of crisis into credit and other markets.

This explains the literally unprecedented impact on Western share markets. The fall of U.S. share prices into a bear market, a 20 percent fall, took only 16 days – even more rapid than in 1929.

Why, when China has been getting the virus under control, has there been such a catastrophic failure in the West? The reason is in large part because instead of learning the positive lessons of China’s ability to control the virus, the Western media and the U.S. government engaged in anti-China propaganda. The bitter truth is that the anti-China propaganda campaign has to some extent contributed to the West being negligent to the looming crisis and they are now facing a medical, human and economic disaster.

The coronavirus is literally a life and death issue for

millions of people – this is why it is totally dominating mass attention and

the media. It has also simultaneously produced a gigantic global economic shock.

It is impossible to separate these two issues because the coronavirus’s impact

on the global economy depends on whether it can be brought under control and

how fast.

It is crucial to understand that we are only seeing the

beginning of this crisis – the coronavirus’s impact is only going to deepen in

the West. This is due to the fact that the coronavirus crisis in Europe and the

US is now far worse than at the worst period in China and so far is continuing

to worsen. Indeed, the failure of the capitalist countries to control the virus

has produced a disaster – the only question is whether it will now worsen to

create a catastrophe.

Taking first the least important of the two aspects of

health and the economy, the economic one, the coronavirus is unusual in being

simultaneously a supply side and a demand side shock. The supply side shock is

that the health risk means the work force cannot produce normally, causing huge

falls in output. The demand side effect is that significant numbers of services

and goods, if they are not consumed in the short term, will not be purchased at

all – people will not travel to work twice to make up for when they did not go

to work, they will not have twice as many meals in restaurants etc.

This was reflected in the huge falls in output in China in

January-February, as the country basically shut down its economy to the level

necessary to contain the spread of the virus, and to safeguard China’s people

from it. The decline of China’s industrial production compared to the year

before of 13.5% in January-February, the fall of 20.5% in retail sales, and the

25.5% fall in fixed asset investment showed this impact.

But China’s drastic economic action was entirely justified in

the more important human terms as the coronavirus was decisively brought under

control. In only five weeks and two days from the peak level of daily

infections, that is between 5 February and 13 March, the number of daily new

cases in China was reduced from 3,887 to 8 – that is by 99.8%. This shows that

decisive action, giving a total priority to safeguarding people’s health, can control

the virus.

By 15 March only 0.006% of China’s population had been

infected with coronavirus. This rapid reduction of the spread of the coronavirus,

in a matter of weeks, and with only a very small part of the population

infected, is in total contrast to the British government projecting that the

outbreak may last for very many months to the end of the year, that people over

the age of 70 must prepare for four months of self-isolation, and that 60% of

the population need to become infected to achieve ‘herd immunity.’

The coronavirus situation in the West is far worse than in China

But the economic impact in the West, seen immediately in the

huge stock market falls but which will rapidly spread into the productive

economy, was not due to China’s coronavirus situation but to the coronavirus

situation in the West – which is now far worse than anything seen in the worst

period in China.

That the global economic impact is being driven by the coronavirus

crisis in the West, not in China, is clearly shown by the fact that during

January-February, the worst coronavirus period in China, US stock markets were

still soaring – the Dow Jones Industrial

Average’s all-time peak was on 12 February when the coronavirus was raging in

China with 2,015 new cases that day. The recent most severe Western stock

market fall in contrast, on 9 March, came when the coronavirus was coming under

control in China – the number of new cases in China on that day was only 40.

In terms of the global situation, sharp declines in the

number of new coronavirus cases in China confirm that the coronavirus outbreak

there, while not over, was decisively being brought under control. Therefore,

production and supply chains both in China, and from China to the global

economy, would begin to improve.

But despite the sharp improvement of the situation in China the

huge fall in the Western stock markets was entirely rational because they

reflected a correct understanding that the place the coronavirus is presently out

of control is not China but in the West. Indeed, it is crucial to factually understand

that the speed of spread of the virus in key Western countries is now very much

faster than at the worst period in China. This reality is merely obscured by

making comparisons in terms of the absolute number of cases, because China’s

population is so much larger than any capitalist country except India.

For example, attempts have been made to hold up success in

South Korea in controlling the virus as equivalent to China’s. But this is factually

not nearly the case. Mainland China’s worst day for the number of new

laboratory confirmed coronavirus cases was on 5 February at 3,887. The worst

day in South Korea was on 29 April at 813. But to assess the relative impact of

the coronavirus on a country this comparison in terms of absolute numbers is

highly misleading for the simple reason that Mainland China’s population is more

than 27 times that of South Korea. Therefore 813 cases in South Korea, in

proportion to its population, is equivalent to 21,993 in Mainland China. The

relative size of the peak number of new cases in South Korea was more than five

and a half times as high as in China. Furthermore, by 15 March there were still

76 new cases reported in South Korea which is equivalent to 2,056 in proportion

to the population of China – on that day in China there were only 20 cases.

Therefore, South Korea has made welcome progress compared to European countries,

but its success is far less that in China – the number of new cases in South

Korea on 15 March, relative to its population, was a hundred times higher than

in China.

The situation in Europe is now disastrously worsening when

measured in relative terms – which gauges the real impact of the virus. China’s

population is 17 times Germany’s, 21 times Britain’s and the north of

Ireland’s, and 23 times Italy’s. Recalling

that the highest number of new coronaviruses cases in China on a single day was

3,887, the number of new daily cases reported by the WHO on 15 March in Germany

(733) was over 12,000 relative to China’s population, the number of new cases

in France (829) was equivalent to almost 18,000 relative to China’s population,

the number of new cases in Spain (1,522) was equivalent to almost 46,000

relative to China’s population, and the number of new cases in Italy (3,497)

was equivalent to almost 82,000 relative to China’s population. So, in

proportion to the population, the number of new daily cases in Germany was

three times as high as the peak in China, in France five times as high, in

Spain 12 times as high, and in Italy 21 times as high.

The relative impact of the coronavirus is therefore already very

much worse in Europe than at the most severe period in China. Furthermore, the

number of European cases is rising. While China is bringing the coronavirus

under control, failure of the European capitalist countries to take similar

measures to China has led to the virus spreading extremely rapidly.

Economic and market impact

The global economic impact follows inevitably from this

failure in the West to contain the virus. Europe is the world’s largest

economic area – taken together even bigger than the US. Therefore, the fact

that the relative speed of spread of the coronavirus in Europe is far faster

than at the worst period in China has a very severe impact on the world

economy. This by itself inevitably has a harsh effect on Western stock markets

and economies. This negative economic shock then also explains the plunging oil

price and the oil production war waged by Saudi Arabia, Russia etc. The oil price shock then worsened the stock

market falls through the crash in energy company share prices.

The situation in the US is perhaps two weeks behind Europe –

although this is difficult to judge precisely as the US authorities are taking

a dangerous approach of minimising the virus’s danger. Trump initially tweeted

that the coronavirus is a less serious risk than ordinary influenza. As is

widely understood a similarly reckless policy is being adopted by the British government.

The US appears in key cases to either have a totally

inadequate number of virus test kits or may be taking the criminal decision not

to test – a policy now being adopted by the British government. For example, to

take the worst case, the Washington

State nursing home which suffered the most severe outbreak in the US, with

19 suspected deaths, waited days before receiving kits to test others – which

revealed another 31 cases. A patient must pay over $3,000 for a coronavirus

test in the US so many without medical insurance will not take tests.

There are also extreme disparities between US data and that

which is being supplied to the WHO, greatly understating the coronavirus’s

spread in the US – presumably this data is supplied by the US authorities. For

example on 9 March the official data published by the WHO, doubtless US supplied,

showed only 213 US cases while the very reputable Johns Hopkins University,

which has collated reports, already found 761 US cases – more than three times

as high as the figures supplied by the US to the WHO. This disparity between

data supplied to the WHO by the US and studies by reputable institutions in the

US is continuing.

In Europe, apart from Britain, the authorities appear to be

keeping serious records, but as already noted these reveal that the spread of

the virus in key countries is proportionately more rapid than at the worst

period in China. It is unclear if the US situation represents severe lack of

preparation in light of two months warning of the arrival of the virus,

organisational chaos, or the administration’s severe underestimation of the

seriousness of the virus or deliberate measures to under report cases for

reasons such as aiding the stock market.

The British government’s decision not to test all cases is

clearly a deliberate policy to attempt to try to keep the number of reported

cases down. This is criminal irresponsibility – without testing the spread of

the virus cannot be traced and those who do recover from symptoms have no idea

whether they really had the coronavirus or not. This furthermore means that the

most immune group, those who have had the virus and have recovered, do not know

that they are the best people to help the most vulnerable as they have never

been tested.

In summary, in addition to the direct health impact, the

severe stock market falls came when China was overcoming the virus but was because

an extremely serious situation was revealed in Europe and great lack of clarity

in the US – the stock market crash, logically, was due to the coronavirus

situation not in China but in the West.

The economic perspective depends on the medical policy

It is impossible to precisely estimate the precise depth of

the economic downturn, although it will be sharp, without knowing whether the

coronavirus can be brought under control in the West. While emergency measures in

slashing interest rates and undertaking Quantitative Easing are being taken by

the US Federal Reserve, other central banks, and capitalist governments, many measures

cannot be taken while the health emergency continues. People will not go to shop,

to restaurants, to travel for holidays etc, whatever the economic inducements,

if they think they may die as a result. Many economic recovery measures therefore

can only be taken when the medical situation is ended.

As China is getting the coronavirus under control it can already

begin to prepare economic recovery measures. But until capitalist Europe is

prepared to take the decisive measures to control the coronavirus, similar to

those used in China, the medical situation will continue to deteriorate, and it

cannot launch any effective economic recovery measures. Simultaneously the medical

situation in the US remains entirely unclear due to the entirely wrong approach

taken at the beginning of the outbreak by the Trump administration. The World

Health Organisation has explained

the situation clearly in a virtually unveiled attack on the policy of the

British and US governments: ‘The most effective way to prevent infections and

save lives is breaking the chains of transmission. And to do that, you must

test and isolate. You cannot fight the fire blindfolded. And we cannot stop

this pandemic, if we don’t know who is infected. We have a simple message for

all countries Test, test, test. Test every suspected case.’

The background in the Western economies when the coronavirus

hit was clear. Their economic situation was weakening since the peak of the

current US and EU business cycles in the second quarter of 2018. From then

until the 4th quarter of 2018 US GDP growth had fallen from 3.2% to 2.3%,

and the EU’s from 2.5% to 1.2%. The coronavirus will clearly weaken this

economic growth further – by how much depends, as already analysed, on how

rapidly decisive European and US anti-coronavirus measures are taken. The UK

recorded zero GDP growth in the three months to January, before the coronavirus

impacted this country. Given this weakness before the coronavirus struck it

will therefore be a miracle if a recession in the West is avoided.

The experience of China shows the coronavirus can be brought

under control. But so far, the capitalist Western countries are not taking

these measures. There is therefore already a disaster in the West due to the

failure of response to the coronavirus. The only question is whether the

disaster will worsen further into a catastrophe.

This is an updated version of an article from John Ross,

which first appeared in Chinese in Global Times

The claim from the Tory government and its army of media

supporters that the latest Budget has ended austerity is completely false. It

is very important for the left and the labour movement as a whole that they

grasp the character of the new attacks to come, so that they can resist them.

In effect, this is a Tory government of a new type. Previously,

since austerity was first implemented in 2010, the Tory governments have

transferred incomes from workers and the poor to big business and the rich. This

is in the hope that both increased rates of exploitation and the transfers of

funds themselves will encourage business investment. But the encouragement to

private investment has been a dismal failure. Private investment growth is

officially forecast to be zero this year.

The new Tories want to provide further inducements to

private sector investment by increasing public sector investment. SEB

has argued vociferously for increased public investment over a prolonged

period. This not investment for its own sake, but to increase the productive

capacity of the economy (adding to the means of production) as the most

decisive factor in raising the output of the economy and therefore prosperity.

But these Tories intend the opposite. They want to increase

the rate of exploitation further, provide incentives to private business to

investment, and intend to do this by funding with investment with yet another

reduction of public services and (probably) public sector pay. They will further

shift the burden of the crisis onto the shoulders of workers and the poor.

Government current spending is being cut over

the medium-term.

There is a one-off boost, to cope with the

effects of their own disastrous Brexit

The projected rise in government investment (if

it materialises) will still leave total government expenditure lower than in

recent years

This means that the rise in public investment is

more than being funded by further attacks on public services and public sector

workers

There is a significant projected increase in net

government borrowing. This is despite a fall in debt interest payments, which

themselves are being used to boost spending in the short-term

This is not ‘deficit-financed growth’, as has

been claimed. It is the effect of weaker growth on public finances, pushing both

tax revenues lower and automatic outlays (such as welfare payments) higher

In fact, the current year for which the OBR

provides an estimate and the subsequent 5 years’ forecasts are the weakest on

record for such a prolonged period

Taken together, SEB can find no recorded

10-year period of real GDP growth where every year is below 2%. This is what

the actual recent growth years’ growth rates will amount to, combined with the

OBR forecasts

There is a sharp one-off rise in government

current spending next year. This is not to combat the effects of the

coronavirus crisis, which is current. Instead, it follows the withdrawal from

the EU at the end of this year. It clearly indicates the government expects a

very negative outcome from the Brexit it is planning

There is nothing substantial in the Budget to

address the climate crisis, and the need for large-scale investment in

renewable energy production, or conservation

Austerity resumed

Despite the mass of commentary suggesting that austerity is

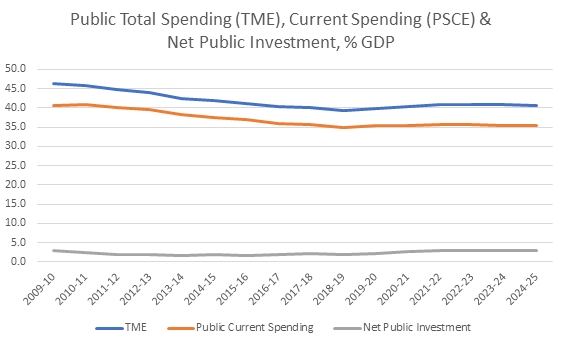

over, it is very simple to demonstrate that is not the case. The chart below is

taken from the OBR databank and shows total for public spending (TME), current

(or day-to-day spending, PCE) and net public spending as a percentage of GDP.

Chart 1. UK Public Spending Totals, Current Spending and New

Public Investment, as a % of GDP

The chart lines show a downward trend of total government

spending. For the 6 years of OBR estimates and forecasts from 2019/20 to

2024/25 average TME (total government spending) is 40.5% of GDP. For the

preceding 6 years it was 40.8%. Total government spending will be lower and austerity

is not ending at all.

The big impact will be felt by public current spending. Over

the same 6-year periods, Public Sector Current Spending (which includes health,

education, welfare and so on) will fall to 35.5% of GDP, from 36.5% of GDP.

By contrast public sector net investment is projected to

rise from 2% of GDP last year to 3% by the end of the 6 years of the OBR’s

forecast period. But it should be clear, it is ordinary people who most rely on

public services who will be paying for this increase. Furthermore, as the OBR

itself points out, there is a persistent and large shortfall between the

projections for public sector investment and what actually takes place.

Planning investment is not the same as delivering it.

A significant one-off

boost to spending

The basis for all the hyperbole and false claims about the

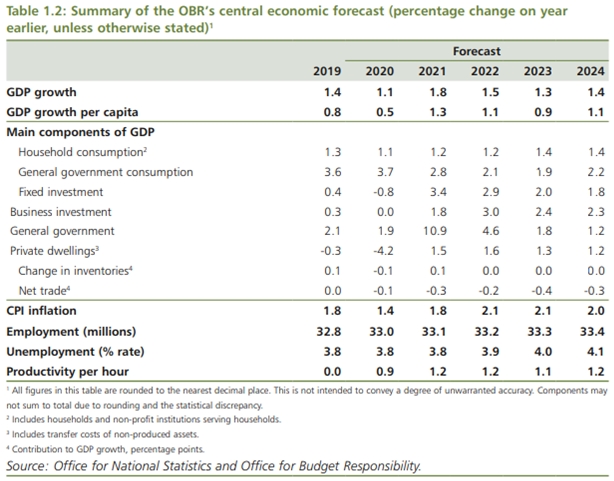

Budget is because of a one-off increase in government spending next year. This

can be shown in one of the key tables from the Treasury’s Red

Book.

As the table shows general government spending receives a

very large boost in 2021, rising by 10.9%. This falls back in the following

year and austerity returns in 2023 and 2024. It is important to note that the

growth rate of this measure of government spending is even slower than in the

most recent years, 1.8% and 1.2% in 2023 and 2024, compared to 2.1% and 1.9% in

2019 and 2020.

This increase in government spending is not

coronavirus-related, which is a current crisis that the government will be

hoping is over before the end of this year. Instead, it is a response to the

Withdrawal Agreement from the EU which does end in December of this year. Clearly,

the government expects a large negative shock from the Brexit it intends to

carry out, and the increased spending is an attempt to offset its worst

effects.

The attempt is only partly successful, using their own data.

Real GDP growth is expected to rise to 1.8% in 2021. However, general

government expenditure accounts for about 40% of GDP, so a one-off increase of

nearly 11% should lead directly to a boost in GDP of well over 4%. But the

projected increase is just a fraction of that, with real GDP rising from just

1.1% in 2020 to a very modest 1.8% in 2021, when the spending is to take place.

Clearly, the implicit assumption is that without the one-off spending splurge,

growth would be sharply negative with the planned Tory Brexit.

Miserably low growth

The official projections for real GDP growth are a terrible

indictment of government economic failures. This includes but is not confined

to their own assessment of the further damage they will inflict with their

preferred Brexit outcome. As the Treasury’s Table 1.2 above shows, there is no

single year in which real GDP growth reaches 2% in the recent data and the

forecast period.

This is unprecedented. It would amount to at least a 9-year

period of real growth below 2%, a lost decade. There is no equivalent in the

modern era of such sluggish growth, in either the Great Depression or the Long

Depression at the end of the 19th century.

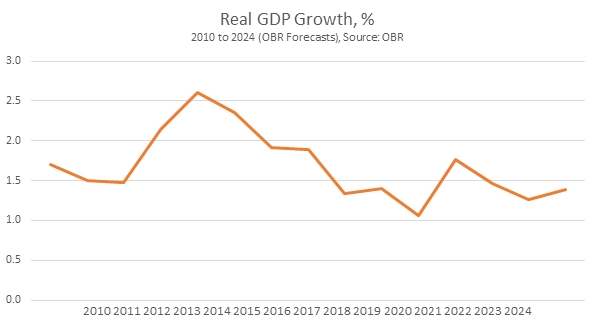

In fact, as Chart 2 below shows, the official outlook for

growth is even worse in coming years than the period immediately behind us, in

the years following the Great Recession in 2008.

Chart. 2 Real GDP Growth, 2010 to 2024 (Forecast)

This unprecedentedly weak growth has a series of

wide-ranging effects, depressing any rise in living standards or improvement in

public services. It also has the consequence of damaging public finances,

lowering the growth in government taxation revenues and automatically pushing

some government spending higher, for example in some welfare payments. This is

the cause of the large deficits in public finances that are forecast.

This is not ‘deficit-financed growth’ as has been claimed;

there is no growth and the economy slows. And, as already noted total

government spending will fall. These deficits are a reflection of economic

weakness, not ‘keynesian pump-priming’.

The multiple crises

There are a series of crises that the government is failing

to address: coronavirus, the weakness of the economy, the damage from its own

intention to crash out of the EU without a deal, the crisis in public services,

the unprecedented weakness in the economy and the existential threat of

catastrophic climate change. Measured against any of these challenges the

government’s response has been woeful.

On the coronavirus crisis, at every turn, it has unpicked

the measures praised by the World Health Organisation and enacted in China and

Viet Nam. Every excuse is made for inaction, that masks are not perfect,

testing is not 100% accurate, there is no point in heat-testing or even hand

gels at the airports, and so on. Instead, it has relied on measures to correct

some of the economic effects of coronavirus spreading. These steps, and many

more will need to be taken. But they are pointless unless and until government

is bearing down on the spread on the virus itself, which is clearly not the

case.

This will put enormous strain on the economy and public

services, especially the NHS (but also care for the elderly and education,

among others). Public services are already buckling under impact of a decade of

austerity. The UK already has below-average ratio of nurses to the population,

7.9 per thousand compared to 9.0 for the OECD as a whole. The only comparably

high-income country with a lower nurse/population is Italy (OECD

data).

It is clear that the increased spending in 2021 is not

coronavirus-related. Instead, it is a response to the effects of its own

determination to pursue a hugely damaging No Deal Brexit, presumably in order

to do a deal with Trump and adopt US business and labour market norms. The

government’s own forecasts show that a huge increase in spending to offset its

Brexit will produce barely a flicker of growth.

The planned increase in public investment is long overdue. But

it is very unlikely to produce either the transformation of ‘levelling-up’

across the country or the necessary corrective to abysmally low productivity

growth. For accuracy, the OBR forecasters do not expect either outcome.

One neglected factor, well established in classical

economics from Smith onwards, is that the effectiveness of all investment is

determined by the scope of the market. Any Brexit that takes this economy

outside the customs union will necessarily reduce the effectiveness of all

investment, because the market will also be severely contracted.

Finally, despite hosting COP26 in Glasgow later this year,

it is clear that the Budget contains no plan to address the climate crisis with

decisive action. Instead, this a government that has tried to press ahead with

plans such as the third runway at Heathrow and a road-building programme

regardless of the law. There was not even a pale imitation of Labour’s Green

New Deal, or anything similar. The Green New Deal is precisely the required,

targeted and ‘shovel-ready’ programme that could be implemented with

large-scale state investment – and is absolutely necessary. Instead, it seems

likely that The Tory recipe will be to search for new business-friendly

projects, such as more roads, and local and haphazard local projects.

When this fails to transform the economy, no doubt there

will be a new ideological offensive against public investment of all types. But

by then, US companies may be in control of large swathes of the public services

in this country.

Recent Comments