Government attempts to divide the rail workers from others are falling flat. An independent poll by Opinium shows strong public support for the workers’ case.

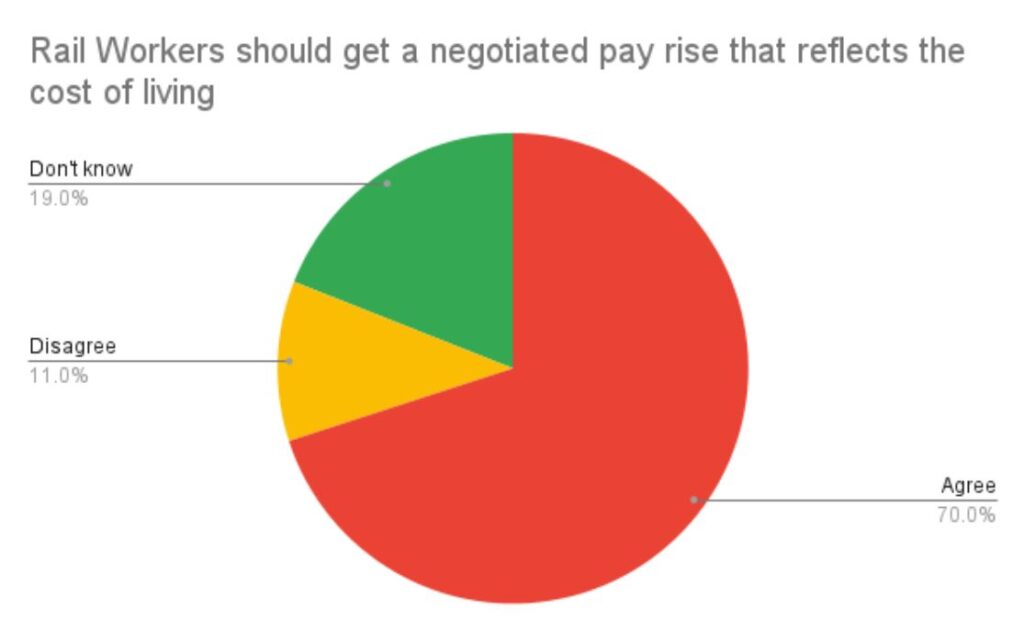

On pay, there is overwhelming support for rail workers to get a pay rise that reflects the increase in the cost of living. This is an interest we all have in common and its becoming increasingly plain that the government does not agree. They now explicitly state that wage claims should be BELOW the rate of inflation. This is the death knell for any claim that they want to “level up”, or believe in a “high wage economy”.

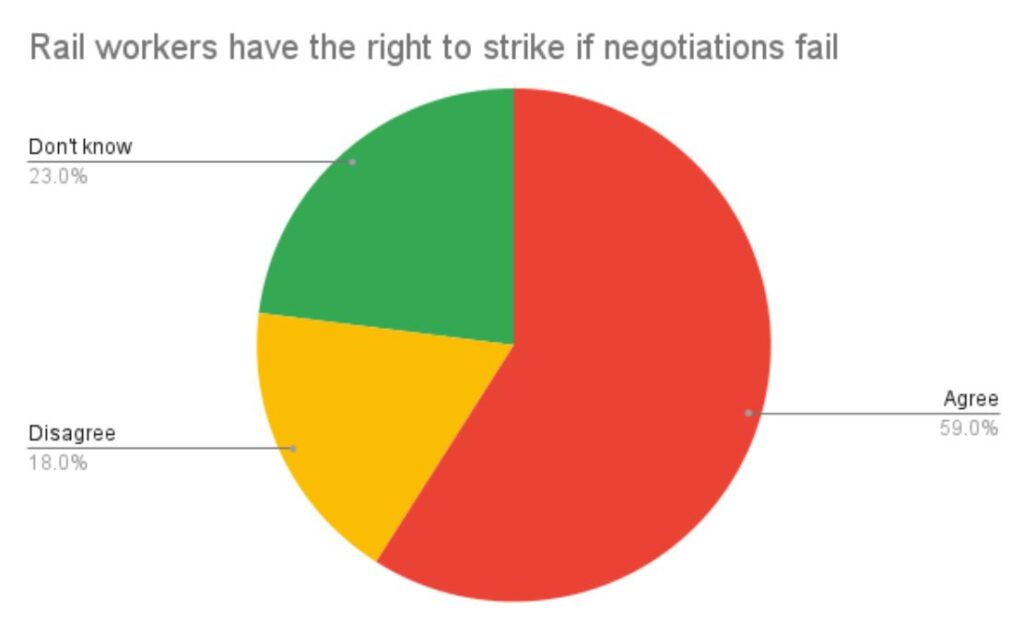

Three out of five support the right to go on strike if negotiations fail. Government sabre rattling about restricting the right to strike is not cutting with the grain.

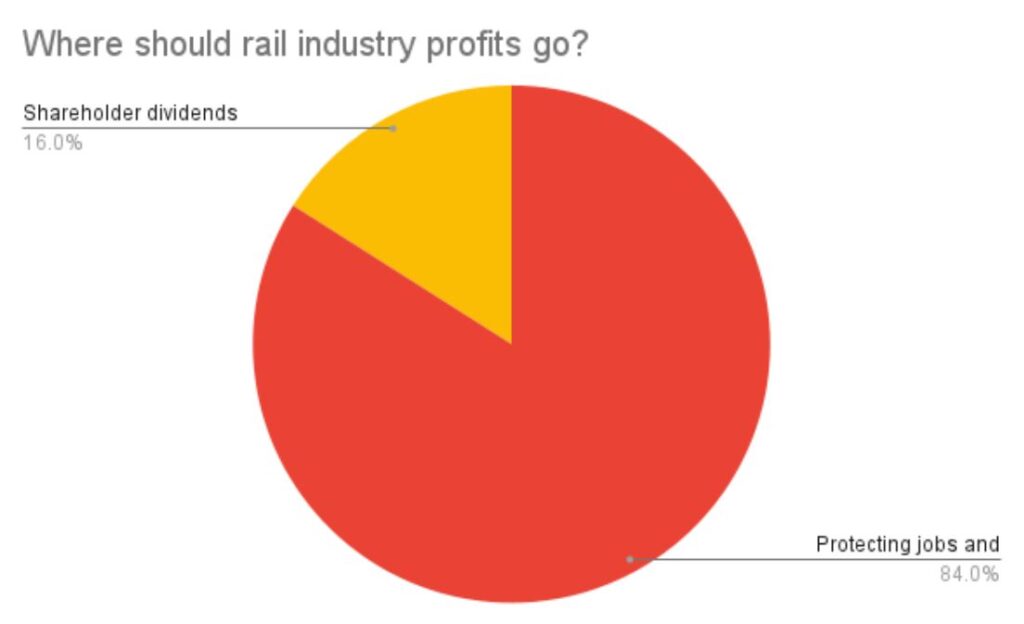

The weakest part of the government’s case is their belief in privatisation and the sacrosanct character of profits and dividends, with overwhelming support for profits from rail services to be reinvested in protecting jobs and improving services. This reflects a growing awareness that the share of the economy being taken by owners of capital is rocketing at a time that the rest of us are being squeezed until our pips squeak.

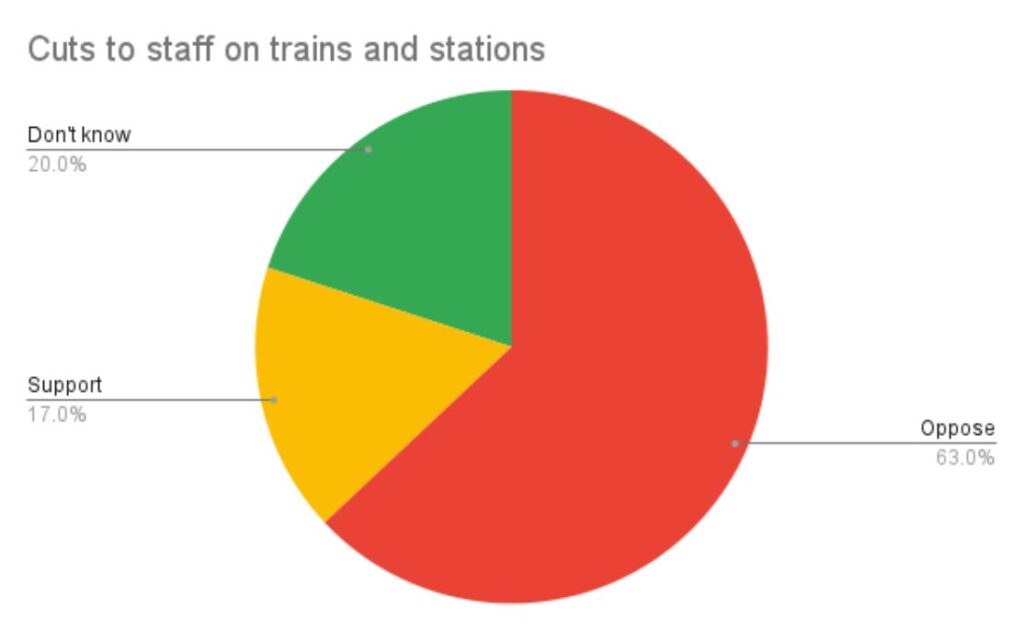

This takes a specific form in large majorities opposing cuts to jobs on trains and stations.

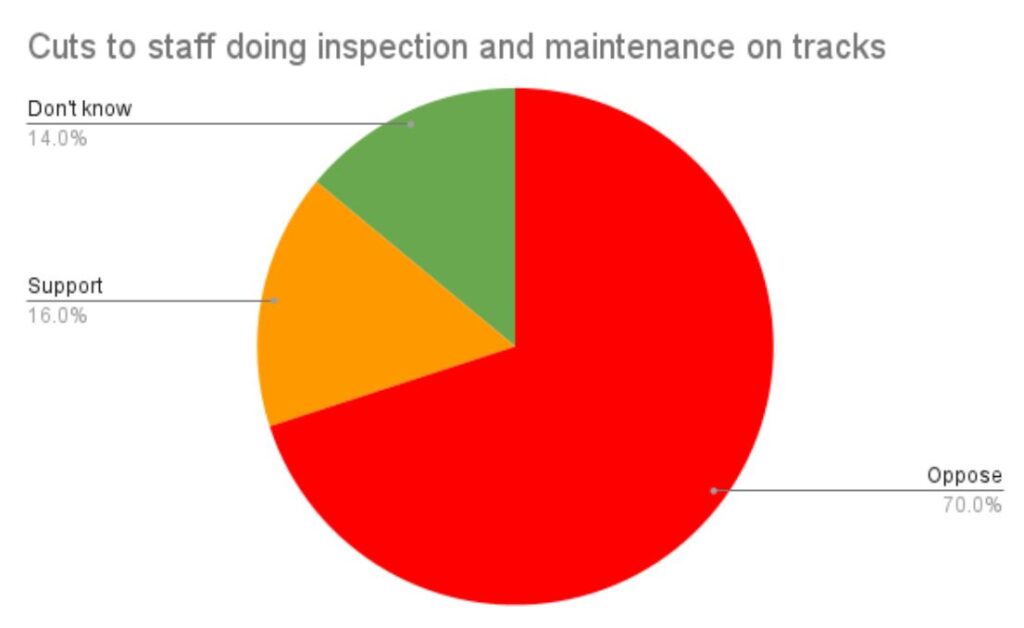

And even more opposing cuts to staff inspecting and maintaining safety on the tracks.

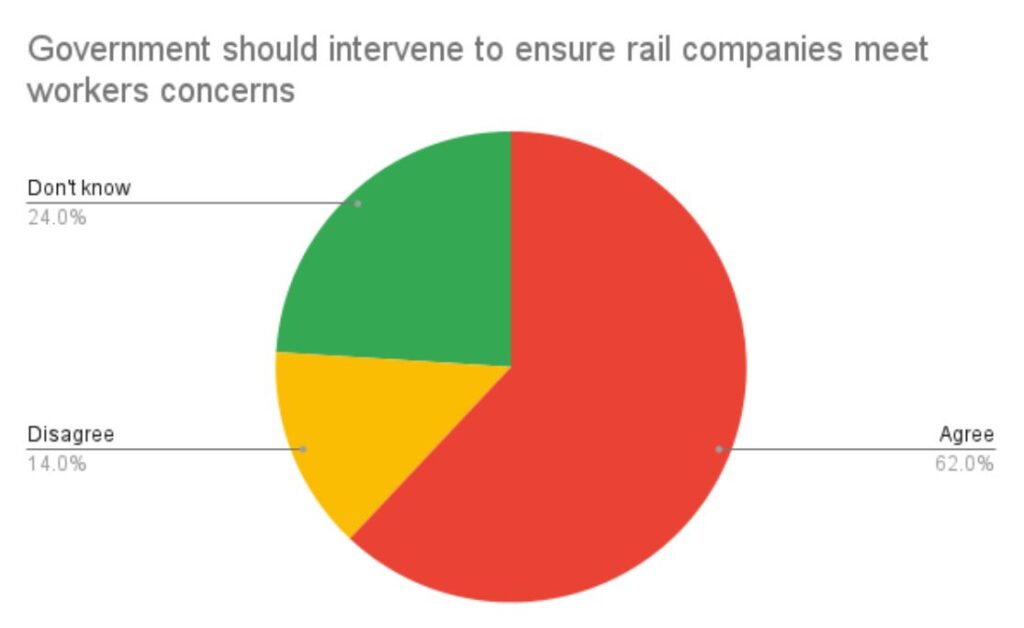

Given that the government is very evidently intervening to make sure that the rail companies do NOT meet the concerns of the workers, they are doing the opposite of what the public wants them to do.

Labour should take note. We are heading into a summer and autumn in which the rising costs of food and energy are propelling workers to turn to their unions to try to stop themselves being forced under. This affects all of us. Most of the public support the workers taking action. If Labour front benchers give “a categorical no” to support for that action, as David Lammy did for airline workers in UNITE and GMB on Sunday, the party will be acting as a human shield for the government (and giving it a lifeline).

See you on a picket line some time soon.

The above article was originally published here on Urban ramblings.

As revealed in this Oxfam Report, the poorest 50% and middle 40% of the global population have a minimal or declining carbon footprint. The top 10%, and even more the top 1%, already have carbon footprints that are unviable and are increasing so fast that they will have bust us through the 1.5C limit on their own by 2030.

The top 10% are people who are on more than £125,000 a year. Most of them live in the Global North, but are a minority even here. The working class in the Global North, is overwhelmingly in the middle 40%.

The strategy of the ruling class in the Global North is primarily to sustain their own wealth and power.

Even those that recognise reality can only envisage a green transition which prioritises their own consumption standards by keeping the bottom 50% impoverished. Carbon offsetting by keeping the global majority in their place.

Hence the failure to transfer investment to the Global South and the prospect that the 350 carbon bombs identified by the Guardian will be dropped; because it is profitable to do so.

This underlines the paradox of the debate about “stranded assets”, as assets are only stranded if there is a viable transition. If there isn’t, they stay profitable until everything collapses around us; which will always be the stronger motivation for companies operating on quarterly profit returns. The notion that Fossil Fuel capital will be more motivated by social responsibility than profits runs counter not only to the record of its counterparts in the tobacco and asbestos industries, but also its own record in covering up its own research on the climate impacts of its operations from the 1950s onwards. They knew. They covered it up. Now that we know, they greenwash instead.

As they recognise that climate breakdown will create social and political crises on an unimaginable scale, from waves of climate refugees to possible war in the Arctic, they are prioritising military spending over solving the problem. The US government is spending 14 times as much on its armed forces as it planned to do on domestic climate measures – and then didn’t agree to. They have committed $40 billion to stoke the war in Ukraine rather than seek a peace deal; while climate transition funding for the Global South is reluctantly dispensed through an eye dropper.

What that means is an immediate future dominated, not by win-win global cooperation to solve our problems and build a sustainable society, but by wars and crises that make doing so ever more difficult. Campaigning against these is an urgent priority for anyone committed to Just Transition.

A strategic challenge for the working class in the Global North is therefore recognising that our own ruling classes are structurally incapable of making the transition; but are divided between those that will openly sabotage it and those that will float half measures.

While we can bloc with the latter against the former, if we want a full transition, we have to lead it. If we don’t want to be thrown under the bus, we have to be driving the bus. That means thinking like the leaders of society, because it’s our job now. And we need to seek alliances with the global majority, including countries that see themselves as Socialist.

The tactical challenge is that we operate in a national polity that presumes a “national interest” that subordinates the working class to the ruling class and this is deeply ingrained in popular perception, political (and union) movements; so consciously thinking internationally – outside the limits of the Brit Box – and framing our campaigning accordingly is essential.

UNITE the union’s new general secretary Sharon Graham has launched a ‘profiteering commission’ to discover and expose the role of profiteers in the current cost of living crisis. This is a good initiative as the exposures themselves can play a role in increasing the level of understanding about who is responsible for the crisis. This may also contribute to raising the level of class consciousness, which has not increased in proportion to the fall in real incomes since 2010.

There is no doubt that profiteering is a major factor in pushing prices higher. As the chief executive of BP said, “we have more cash than we know what to do with,” after annual profits rose to almost £10bn. This statement alone explodes the myth perpetuated by ministers that any windfall tax on energy companies would interfere with investment plans.

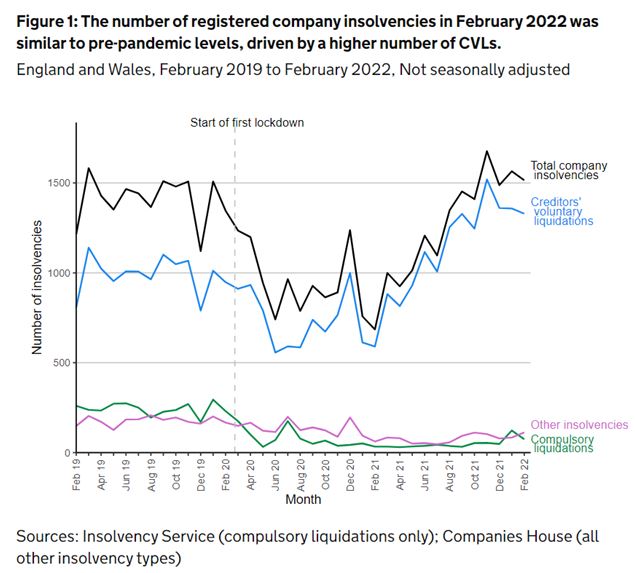

But the statement itself is highly revealing in another way. Profits are crucial to capitalism, and some are experiencing a bonanza. Yet it is widely understood that some firms continue to struggle. As shown in Chart 1 it is clear that the level of company insolvencies is now above the pre-pandemic level.

Chart 1. Company insolvencies England & Wales February 2019 to February 2022

This is hardly surprising as growth was already weak prior to the beginning of the pandemic. The level of output has only recently recovered to end-2019 levels, before the economic effects of the pandemic were first felt. In addition, some producers of finished or semi-finished goods, as well as service providers will have been hard hit by the rise in commodities’ prices. All of this also flatly contradicts all the government’s boosterism about a surging economy.

As a result of this economic weakness, the situation is very uneven on profits. Clearly, some are experiencing a price-gouging bonanza, while others are experiencing declining profitability. Therefore, it is necessary to examine some of the key economic trends as a whole, in addition to analysing the role of specific sectors or firms.

Table 1. below shows some key variable for the British economy over two different periods. The first is the period from the 4th quarter of 1999 to the 4th quarter of 2021 (the most recent data). The second period is shorter, beginning before the pandemic in the 4th quarter of 2019 and also ending in the 4th quarter of 2021.

Table1. Wages, Compensation, Profits and Business Investment, £bn

Q4 1999 to Q4 2021, £bn

% change

Q4 2019 to Q4 2021, £bn

% change

Wages

111 to 254

+129

226 to 254

+12.4

Total Compensation (incl. employers’ social contributions)

128 to 309

+141

278 to 309

+11.2

Total Profits (Gross Operating Surplus)

55 to 139

+153

124.5 to 139

+11.6

Business Investment

31.3 to 53.2

+70

56.8 to 53.2

-6.3

Source: ONS, author’s calculations

Wages, Profits and Investment

Taking just wages and profits first, over the longer period the growth in profits has been the strongest of all, rising 153% (all data are based on nominal, not real £, for the purposes of comparison). However, this growth rate in profits is not hugely or qualitatively greater than the growth of compensation or wages, although it is clear that business owners have been winning in the struggle over each class’s share of national income.

The most significant laggard is in the growth of business investment which has risen at half the pace of the growth in the level of profits over the 22-year period.

Turning to the much shorter period starting with the quarter immediately before the pandemic, these patterns have largely continued but in a somewhat more dramatic form. There is no qualitative difference in the growth rates of wages, compensation or profits over the 2-year period. (Again, it should be stressed these are nominal data, before adjusting for inflation). But there has been no growth at all in business investment, which actually declined over the period.

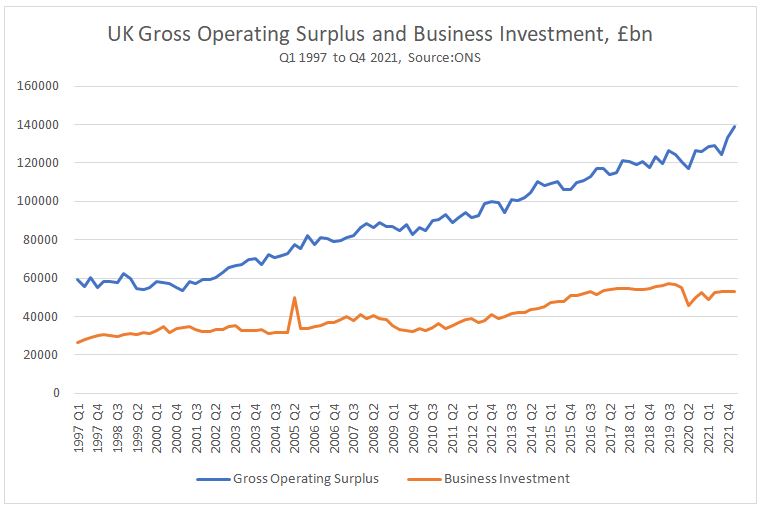

Chart 2. UK Gross Operating Surplus and Business Investment, £bn

As Chart 2 clearly shows the level of business investment has completely failed to keep pace with the increase in the total mass of profits for businesses. At the end of 1999 business investment amounted 57% of profits on this measure. At the end of 2021 it was equivalent to just 38%.

This is equivalent to approximately a decline of £100 bn in business investment in 2021 compared to 1999, based on the rise in profits and an unchanged investment ratio.

Why investment matters to prices

This reduction in investment directly lowers the growth rate of GDP, as it is equivalent to approximately £100 billion, around 4% of GDP. But crucially, Investment has the effect of producing an increase in the means of production.

It is widely recognised that the current surge in prices globally is a product of a ‘supply-side’ shock, where the supply of goods is insufficient to meet demand. In the first instance this was caused by US monetary policy, which has been extraordinarily expansionary without any commensurate increase in Investment. Sanctions against Russia and the war in Ukraine have exacerbated these trends.

In contrast, all productive Investment either replaces or augments the existing capacity to supply goods to the economy (increases the means of production). Without it, demand can outstrip supply and cause prices to rise. A sustained increase in Investment would both create high quality jobs as well a generally lowering the upward pressures on prices.

Of course, specific mechanisms would be needed to ensure that this happened. Companies based in Britain have shown a distinct reluctance to increase their Investment over the long run. Changes to the tax code would be necessary to oblige them to increase Investment at the expense of both shareholder dividends and executive pay. The tax rate could be increased on profits, so that the State could use the revenues to directly increase its own Investment (as well as increasing borrowing to Invest).

Naturally, none of this should cut across the work of the profiteering commission. The numerous scandals that can be revealed in that process can both rouse the indignation of the population as well as identifying funds to increase pay and lower prices for hard-pressed households.

Recent Comments