By Tom O’Leary

The decision of Jay Powell the chair of the US Federal Reserve Bank (central bank) to adopt a policy of higher inflation is another hammer blow to workers and the poor. Already reeling from job losses and pay cuts under the cloak of dealing with the economic fallout from the pandemic, workers and those on fixed incomes such as benefits will see their living standards fall even further, if the central bankers are successful.

The central bank which most closely follows the Federal Reserve policy changes is the Bank of England. But others may also feel they are obliged to follow suit, especially as the US Dollar is falling sharply, which places upward pressure on other currencies and damages their competitiveness.

The new policy

The Fed chair justified his new policy on the grounds that at some point in the future interest rates would have to be cut again to support the economy, but as they are already near-zero inflation would be necessary to allow interest rates to rise first.

This is hokum, which only highlights the complete failure of official policy in the Western economies over a prolonged period. The G7 has never properly recovered from the 2008 recession and its economies are now facing the worst crisis since the 1930s. The time for decisive action is now, not at some unspecified point in the future.

The central bankers and many other policymakers share the widespread misconception that the growth in Consumption is key to economic revival, because it is the larger component of the Western economies. In reality, as only Investment can add to the means of production, it is Investment which creates the basis for the sustainable growth in prosperity.

The false view on the role of Consumption (unfortunately widely shared on the left and among progressive economists) has led to a series of absurdities. Money is provided for an ‘eat out to help out scheme’ but money is refused to advanced manufacturing companies that are going bust. Taxes are cut for the rich, the central bank inflates money supply, buys bonds, gets interest rates (both short-term interest rates and bond yields) to record lows in an effort to boost ‘demand’ – and none of it works.

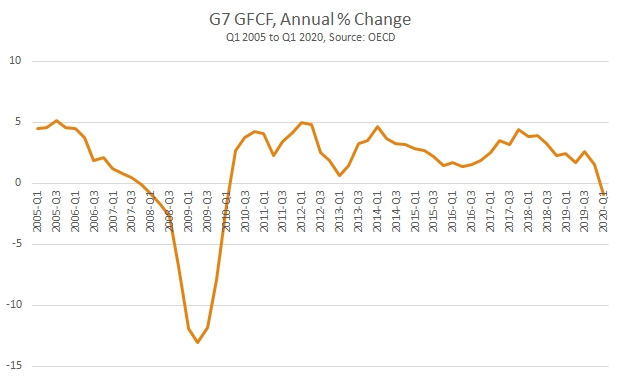

This is because the crisis which began before 2008 is a crisis of profits, which is then expressed as a slump in private sector Investment. The is shown in Chart 1 below.

Investment (Gross Fixed Capital Formation, GFCF) in the G7 slumped in the 2008 recession. It had already begun to slow sharply from 2006 onwards, long before the recession itself reflecting the slowdown in profits’ growth. Investment was also the component of growth which registered the largest fall in percentage terms and for a prolonged period accounted for the entire fall in GDP in the G7. In short, the recession was driven by the slump in Investment.

Chart1. GFCF Growth in the G7

As the chart shows, Investment in the G7 remained weak after recession. There was never a sharp rise in Investment equivalent to the depth of the fall in 2008 and 2009. Even worse, Investment was contracting in the leading capitalist economies at the turn of 2020, that is before the pandemic had any impact.

The G7 economies entered this economic crisis after a prolonged period of Investment weakness and with renewed declines. And Investment contracted sharply in the 2nd quarter of this year as the pandemic spread rapidly. In the US GFCF fell 7.5% from a year ago and in Germany the decline was 8.3%. Elsewhere it was even worse, with a fall of 24.5% in France and the UK the worst of all with a decline of 29.8% from a year ago.

The effect of the policy

It is not possible to address a crisis of investment by adjusting the policy on inflation. But that does not mean that the Fed’s new policy will have no effect at all.

The real impact of the policy is that it aims to lift prices. It has already been widely noted that jobs are being cut and wages falling across a number of countries, including all of the G7 in response to the economic impact of the pandemic. By raising the sales prices of producers and retailers, while wages are being cut across the private sector, the hope is to raise profits.

Since the decline in profits is itself the cause of the private sector refusal to Invest, it may even be possible for big business to lay the basis for a profit-led recovery in Investment. In strictly scientific, that is Marxist terminology the capitalists will have increased the rate of exploitation either by getting the retained workforce to work harder without an increase in pay and/or forcing workers to do the same hours for less pay.

This is certainly what stock market speculators are expecting. The US stock market is reaching new all-time highs even during a global pandemic and deep economic crisis. This is because speculators expect the actions of firms in cutting payroll and pay to boost profits. The actions of the Fed, and any other central banks that follow suit, will have the effect of adding to those pressures, for higher prices and profits, and lower pay and living standards.

Chart 2. S&P 500 Index Above Pre-Covid19 Peak, New All-Time Highs

Source: FT

There is currently an all-sided attack taking place on the living standards of workers and the poor. The aim of the new central bank policy is to reinforce that attack.

Recent Comments