.430ZMigrants don’t drive down wages (once more)By Tom O’Leary

A false argument can become an established truth by a process of constant repetition. But it is still false. This is now the main method used in the ongoing debate about the effects of immigration to the UK. One of the key false assertions widely made is that immigrants have driven down wages.

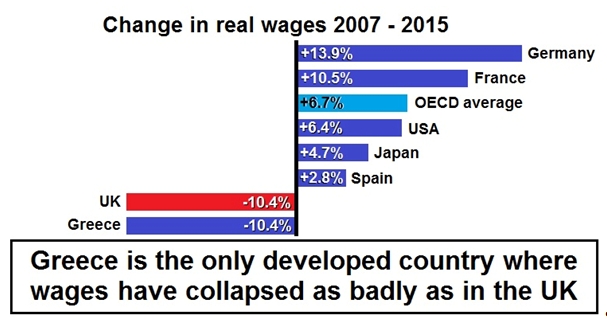

Chart 1 below is based on a TUC analysis on the effect of the recession on real wages in selected countries. Contrary to Government propaganda, the UK economy is not booming. On some measures it is among the worst-performing countries coming out of the crisis. By contrast, while there are many other advanced industrialised countries that have been badly hit by the crisis, only Greek real wages have fallen as far as those of British wages over the period 2007 to 2015.

Source: TUC

This collapse in UK wages has coincided with the continued growth in net migration to the UK. But coincidence is not even correlation, let alone causality.

In reality, no-one outside the far right ever dreamt of linking wages to immigration levels until the Tory Government introduced a net migration target in 2011. This was a blatant attempt to distract from its own unpopularity because of its austerity policy. Labour had started to pull ahead of the Tories in the opinion polls for the first time in 4 years (data here). Blaming migrants for low wages, poor public services, the housing crisis and other issues is classic scapegoating.

The assertion that migrants drive down wages rests on general truisms; that migrants are willing to work for lower pay, they undercut wages and so on. If any of this were true, it would be generally true. There cannot be a unique mechanism which only applies to the UK which does not apply to other advanced industrialised countries. Yet this is one of the more obvious ways in which this argument falls down.

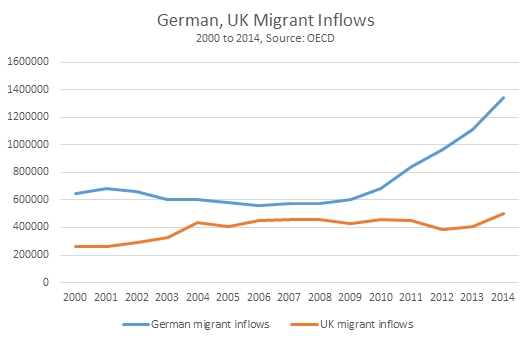

In Chart 2 below the total level of migration to the UK and to Germany from 2000 to 2014. It should be noted that over the period 2007 to 2015 German real wages rose by 13.9% while UK real wages fell by 10.4%, as noted in Chart 1 above.

Yet this is almost exactly the period in which migrant inflows to Germany and to the UK diverge dramatically. In effect, just as German real wages were advancing migrant inflows were soaring towards 1.4 million per annum. At the same time, while UK real wages were declining the level of migrant inflows was more or less steady at approximately 500,000 per annum. As a proportion of the total population German migration was also much higher than that of the UK.

If the general proposition were true that migrants drive down wages in advanced industrialised economies, it would be true across those economies. It is patently untrue. German wages rose in real terms while its immigration rate and totals were far higher than that of the UK.

In reality, the German economy is a much more highly productive economy than the UK, about 30% higher. This is based on much greater openness to the world economy and much higher levels of investment over a prolonged period. This allows both higher wages and higher wage growth than the UK. It is the exceptionally low level of UK investment combined with the economy’s long-term structural weaknesses which have caused the depth of the crisis here and the fall in real wages. Migrants have not cut British wages. British bosses have.

Recent Comments