By Tom O’Leary

There are widespread claims that British Chancellor Sunak is implementing Corbyn and McDonnell’s economic policies even though this has been explicitly denied by both of them. Simultaneously, there is the claim that Biden is resurrecting Keynes with his $1.9 trillion stimulus packages.

These claims are important to examine, and not simply because they are at risk of sowing widespread confusion. It is also important to set out what the recent changes in economic policy represent on both sides of the Atlantic, especially as they are likely to be influential in the Western countries as a whole as the latest iteration of neoliberal economic policy.

Source of confusion

In Western Europe (and to a lesser extent in the US) the dominant economic policy from 1950 to 1980 was ‘demand management’. This was characterised by a loosening of fiscal and monetary policy when there was an economic downturn and the reverse when there was a perceived risk of ‘overheating’ and inflation. This policy fell apart in the economic crisis of the early 1970s and was replaced by Reaganism and Thatcherism from 1980 onwards with what have become known as neoliberal policies.

This failed policy of demand management was incorrectly understood as ‘keynesianism’. It is not in the scope of this article to explain why this is not a product of Keynes’ thought, and this has been done rather well elsewhere on SEB.

The point emphasised here is that this policy of demand management is not effective, as its failure in the early 1970s shows. This is because simply increasing demand does not automatically lead to increased production, and still less it does not automatically lead to increased investment, that is the growth in the means of production.

However, after the horrors of World War II and the following 20-plus years of economic rebuilding, growth and prosperity in Western Europe and the US, the associated ideas of demand management maintain a powerful attraction. This includes in the European labour movements and their Lefts. Yet it remains important to dispel this confusion, as it disarms all of these forces in their response to the latest economic turn in the major Western economies.

The turn in economic policies

Just as they did in the 1980s, the US is leading the Western economies towards a new economic policy, with Britain as its most faithful follower. To understand that economic policy it is necessary to take account of the key developments in the US, which is both the stimulus packages under Biden and Trump taken together, the two British Budgets in March 2020 and 2021 and the various stimulus packages all across in the advanced industrialised countries.

These policies can be summed up as providing a safety net for business (including tax breaks, loans and guarantees as well as direct subsidies). For payroll workers there is an element of wage support, although this also includes wage cuts in most instances. There is little or no support for more marginal workers, the unemployed, those forced into ‘self-employment’ and others.

The latest Biden package totalling $1.9 trillion includes an innovation, a $1 trillion stimulus to household spending. Trump called his own earlier package ‘stimulus measures’ but they were nothing more than temporary and partial subsidies, very little of which went to households (mainly a $600 cheque to households, meant to cover 3 months’ expenditure).

Biden’s is a genuinely large but temporary boost to household incomes, equivalent to approximately 5% of GDP. Taken with the Trump package that was mainly directed towards business the total additional government spending in response to the pandemic is $4.1 trillion, or just under 20% of US GDP. Little wonder that the economy is expected to grow at a rapid pace this year.

In Britain, the Office for Budget Responsibility (OBR) estimates that the total support offered by the British government (which is overwhelmingly to business) at £356 billion, equivalent to approximately 12.5% of GDP. In the other advanced industrialised countries the support measures are sizeable, adjusted downwards in line with the shallower contractions in GDP generally seen elsewhere.

Rising government debt

All of this increased expenditure combined with falling GDP have led to sharp increases in government borrowing.

Government debt issuance in the OECD (Organisation for Economic Co-operation and Development) is expected to be a new record, equivalent to US$19 trillion in 2021 after $18 trillion in 2020 and compared to US$11.2 trillion in 2019. The level of debt issuance was previously on a declining trend in response to the moderate growth of the OECD economies. So, it can be stated that the entire increase in new debt is a product of the economic crisis caused by the failed response to the pandemic.

These totals far exceed the levels of government borrowing seen even in 2008 to 2010. But this is because the depth of the current economic crisis far exceeds the impact of the Long Depression. There is also a distinct possibility there is a China effect. Simply leaving the US economy to its own devices threatened to open such a huge growth gap between the US and China that it would soon become irrecoverable. The huge stimulus is designed to close that growth gap.

Sharply rising government debt and a large temporary boost to spending that may have confused commentators in their wildly inappropriate comparisons. But it should be noted that the initial response to the 2008 crisis was also to increase government spending, and only when the recovery was secured this was followed by vicious austerity in 2010.

In this crisis, it is already clear that increased subsidies and one-off boost to incomes are being combined with structural, that is long-lasting austerity measures. This is shown in the way that Biden reneged on his campaign pledge for a $15/hour Federal minimum wage and cut unemployment benefits. Sunak is cutting government current spending, increasing taxes on workers and maintaining a pay freeze on public sector pay, as has been shown previously on SEB.

Macron in France is still battling for his Thatcherite labour market ‘reforms’, while Germany is eyeing privatisations. All of these are different aspects of a shared drive towards austerity, modified by national conditions.

Will it work this time?

The main factor in determining the level of production is the amount of labour available and its quality (skills, training, education). But increasing the level of production per worker without simply increasing their hours requires an increase in the means of production, through investment.

The reason ‘demand management’ failed was because in a capitalist economy investment is driven not by ‘demand’ but by profits. Firms may either find that additional output is not profitable for a variety of reasons (additional costs or low availability in acquiring raw materials, intermediate goods or necessary labour). Alternatively, they may prefer to try pushing prices higher in response to increased demand, especially if they expect that increase to be temporary. Others may find they have the additional capacity to meet the rise in demand without creating additional productive capacity.

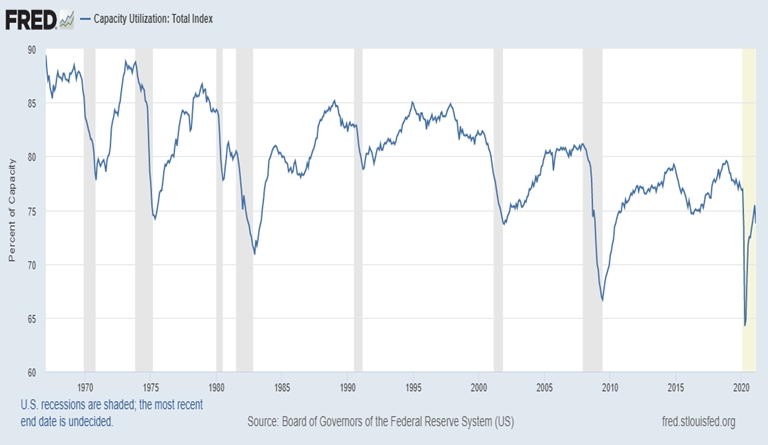

This certainly seems to have been a factor in the US, the leading capitalist economy over a prolong period (and the G7 economies generally). The level of capacity utilisation in the US economy is shown in the chart below.

Chart1. US Capacity Utilisation

Source: FRED

There are two important factors to note from the chart. The first is that the rate of capacity utilisation in the US economy is lower than 75%. There would have to be an enormous, sustained increase in the level of consumption to oblige US capitalists to increase their investment on the confident assumption of future profitability.

Secondly, which reinforces the first point, is that it is also clear that the rate of capacity utilisation in the US economy has been on a long, unbroken downtrend over several decades, only interrupted by cyclical swings. Reversing that downtrend would require a qualitative change in the overall conditions of the US economy to boost profitability, not simply a one-off boost to household incomes however large.

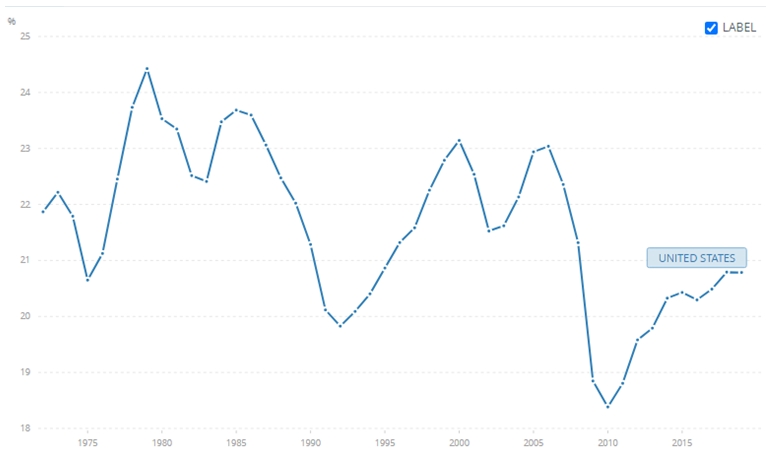

It should be noted too, not entirely as an aside, that this decline in capacity utilisation is mirrored by the same long-term decline in investment as a proportion of GDP in the US economy, as shown in Chart 2 below.

Chart 2. US Gross Fixed Capital Formation as % of GDP

Boosting demand will not be enough to sustain growth over the medium-term, because it is unlikely by itself to create the scope for profitable investment when there is already such a high level of idle capacity. Instead, by themselves the stimulus measures will do only that, stimulate economic activity for a year or two against a backdrop of otherwise very weak growth.

However, as previously noted the governments of the advanced capitalist countries are not simply boosting ‘demand’. They are also imposing austerity measures right now, the most important of which is the surge in unemployment and cuts to pay.

Just as ‘demand’ or consumption does not determine profitability, so it is possible to increase profitability even if consumption remains unaltered (or receives only a temporary boost). Profitability can be increased if the rate of exploitation is increased, specifically if wages for the same work are cut or if work is increased for the same wages.

Both of these are being imposed now, the former largely on manual and other workers who are forced to attend work even under furloughs, and latter largely on stay-at-home, mainly ‘white collar’ workers. Pay per hour worked is cut in either way, initiated by furlough schemes, underpinned by rising unemployment (the mechanism of the ‘reserve army of labour’) and supplemented by measures such as no increase in the Federal minimum wage, or cuts to unemployment benefit, or public sector pay freezes, cuts to Universal Credit payments, and so on.

These austerity measures are integral to the whole economic plan, which is why it is extremely foolish and misleading to compare them to the policies of Corbyn, McDonnell or Keynes. They amount to an all-round attack on wages and the social wage even while there is a temporary boost to demand. In fact, the enormous sugar rush effect of the trillion dollar boost to household incomes may help to mask the effect of these impositions.

This is not so different to the stimulus in 2008 and 2009 followed by austerity from 2010 onwards. The first is meant to revive capitalism and the second designed to boost its profitability by placing the burden of the crisis on the shoulders of workers and the poor. The scale of the crisis caused by allowing the virus to circulate means the scope of policy measures is far greater and the two episodes, of stimulus and austerity, have been concertinaed.

Their purpose is to alter the relationship between labour and capital in the advanced industrialised economies in favour of the latter, to increase the rate of exploitation and then to lay the basis for a rise in profitability leading to a self-sustaining rise in business investment.

This did not work after 2010. It remains to be seen whether it will work this time around. It would be guaranteed to fail if there were large-scale resistance to these impositions. But that has yet to materialise.

Recent Comments