By Tom O’Leary

There is no basis for the belief that the incoming Tory government will end austerity. The reality is, from their own perspective and from the interests they serve, the Tories will be obliged to deepen it.

It is extremely important that the labour movement, all those who want decent living standards and public services and the left are not suckered into believing that this Tory government will be any improvement on its predecessors. Instead Johnson will pile up further misery, in addition to the damage that has already been inflicted.

Early pointers

It is easy to list some obvious pointers to the government’s direction on austerity.

First, the government’s legislative programme (the ‘Queen’s Speech’) contains measures to outlaw strikes in the transport sector. There is no need to outlaw strikes unless you are planning a confrontation with unions. If the Tories are successful they will be emboldened to take on other workers. In recent days, this has been supplemented by the frame-up arrest of a union leader at a peaceful picket as well as an attack on the role or even the existence of the FBU from the government’s inspectorate of fire services.

Secondly, in the same programme there is planned legislation for permanent underfunding of the health service (as well as the threatened removal of performance targets on waiting times at A&E services). In real terms, the NHS funding law will provide the lowest cumulative rise in real spending since the inception of the NHS. Labour attempted to amend it so that the real increase is 4% per annum (which, although still modest rises by historical standards takes some account of both rising population and the higher inflation of medical equipment and drugs, plus the costs of technological innovation). The amendment was rejected.

Thirdly, on this government’s own assessment the economy will be severely hit by the Trump/Johnson Brexit. GDP will be 6.7% lower by 2034 than it would if the status quo was maintained and real wages 6.4% lower. This is not George Osborne’s stupidly exaggerated ‘project fear’ of immediate and sharp recession. It is this pro-Brexit government’s own assessment of the consequences of something like a ‘No Deal’ Brexit. Typically, these official estimates tend to underestimate the damage, as SEB has previously shown.

Finally, the economy is contracting. GDP in November shrank by 0.3%, and outright contraction for the whole of the 4th quarter is possible. With just one month’s data remaining it is almost certain too that industrial production will have fallen for the year as a whole 2019 compared to 2018. Business investment is not rising and was lower in the 3rd quarter of 2019 than it was for the same quarter in 2016.

The Tories are clearly faced with a worsening economic crisis and the global economy offers no grounds for optimism. The idea that they will address this crisis in the interests of the working class and the poor is plainly ridiculous. Instead, they have given strong indications they are gearing up for a major fight.

Why is there an austerity policy at all?

Austerity has not been adopted because Tory politicians are nasty. A change (in this case policy) cannot be explained by a constant.

SEB has repeatedly explained that austerity amounts to a transfer of incomes from workers and the poor to big business and the rich. So, in the very first austerity budget, the Treasury documents showed that the projected revenue increase from raising VAT of £13 billion (which mainly hits workers and the poor) was almost exactly the same as the revenue lost by cutting Corporation Tax. The deficit was unaffected by these measures, but income had been transferred upwards, to business and the rich.

Using correct, Marxist terms there were two main elements to austerity. The rate of exploitation was increased by cuts in real pay and pensions. In addition, the social surplus was redirected away from workers and the poor (cuts to welfare payments, rise in VAT) towards capital and the very rich (tax cuts).

The combined effect of these measures was to force workers to work more for less and to incentivise businesses to invest more. But the second part of this policy has failed. Real wages did fall, but businesses did not increase their rate of investment.

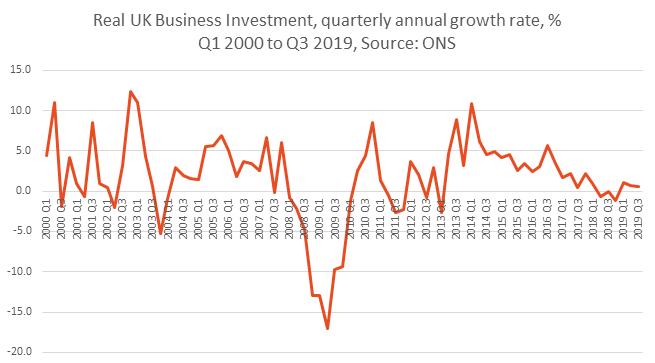

Fig.1 below shows the quarterly real annual rate of growth for business investment from the 1st quarter of 2000. Business investment has been slowing since the beginning of 2014 and is now beginning to contract outright.

Fig 1. UK Business Investment, quarterly real annual rate of growth from the 1st quarter of 2000 to 3rd quarter of 2019

In the last great crisis of British capitalism, Margaret Thatcher was drafted in to do a very similar job to the one attempted by Cameron and Osborne. Helped along by the huge windfall of North Sea oil revenues, which were frittered away, she did produce a recovery in business investment.

This was achieved by increasing the rate of exploitation. Cameron and Osborne followed her example quite slavishly with spending cuts, real cuts to public sector pay, cuts to welfare, cuts to taxes for the highest earners and big business and privatisations. The cloak for these policies, the hue and cry over the deficit, was different to their predecessor, inflation and monetarism, but the project was broadly similar.

But the failure of the later Thatcherites can be shown decisively in terms of business investment, the renewed expansion of capital accumulation based on a series of defeats for the working class which allowed her to increase the rate of exploitation.

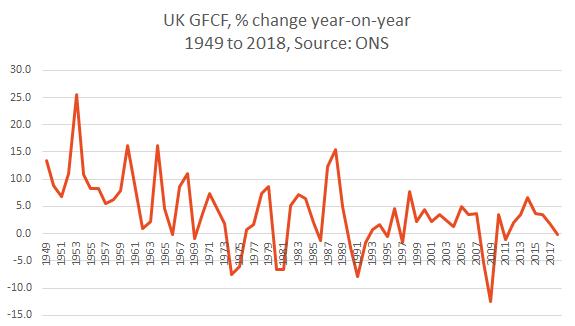

Fig.2 below shows the change in investment, (GFCF, Gross Fixed Capital Formation) from 1949 onwards. Data for UK business investment alone only begins in the 1990s. But, as the UK is a capitalist economy the majority of the investment throughout will have been made by the private sector, and so provides an approximate guide to what the relative impact of Thatcherism was in this area.

Fig 2. UK GFCF, % change year-on-year, 1949 to 2018

In the immediate post-World War II era there were relatively high rates of investment, but it slowed markedly. This reached outright contraction in the early 1970s. Thatcherism was the antidote to this, by cutting real wages and business taxes. Although there was initially a slump, Thatcher’s project was successful and investment recovered throughout the 1980s, until it was brought to a crashing halt by the excesses of the Lawson boom, where the government refused to use the oil revenues for public investment and cut personal taxes instead, fuelling an unsustainable boom in consumption.

As the chart shows, investment growth has only ever been meagre since. Worse, the sharp contraction of the 2007 financial crash and the 2008-09 recession has only ever produced a meagre and short-lived investment recovery. Investment is now slowing to a stop once more. Cameron and Osborne completely failed to emulate Thatcher’s temporary ‘success’.

This is now the situation that confronts Johnson.

Of course there is an alternative to renewed austerity and some seem to believe the renewed breathless PR about the ‘Northern powerhouse’, ‘an infrastructure blitz(!) in the regions (Guardian)’ and ‘pouring cash into the Midlands’ (FT).

This will not happen. The splits in the British ruling class over Brexit were set aside in their united opposition to Jeremy Corbyn precisely because he intended to increase the role of the state in the economy. This diminishes the ability of most parts of the private sector to maintain their profits, or to expand them. It is anathema to them. The Tories will not do it.

Instead, there are protections for workers that currently apply in British law because of adopting EU law. Johnson has signalled repeatedly that he does not want to continue with ‘alignment’ with EU laws and rules. The Trump/Johnson Brexit will include a programme of rolling back workers’ rights.

The objective conditions are also set firmly against Johnson’s economic policy being some version of Corbynomics-lite, as much of the press seem to want to believe. The government’s own negative assessment of economic prospects under Johnson’s Brexit policy will also mean a sharp deterioration in government finances. Under those circumstances a sharp increase in state investment is not impossible, but goes beyond the limit of what the private sector is likely to voluntarily provide in the form of buying increased government debt. Some form of compulsion, including nationalisations and raising taxes on business would be required. The Tories will not do it.

From their perspective, the Tories cannot and will not abandon austerity. Instead, it should be clear they are preparing for a further attack, and that this time it will include major political struggles, over union rights, the right to organise and to protest and other issues.

Recent Comments