This week the British government Education Secretary held up

Denmark as the model the UK would follow in re-opening schools. This is to copy Denmark (if that is what is

actually planned) rather than learn from it.

Norway and Denmark have very similar population levels (5.4

million and 5.8million respectively).

They experienced their first cases of Covid-19 at approximately the same

time and followed a broadly similar trajectory in terms of the spread of the

virus.

In European terms they are among the better performing

countries, with deaths per million of 44.2 per million for Norway and

91.2million for Denmark, compared to Germany 93.5, or now Italy 514.5 and the

UK 495.1.However, on April 15 Denmark decided to begin re-opening the schools,

having been one of the first to close them on March 12.

Since that time the spread of the virus has been more

pronounced in Denmark than Norway.

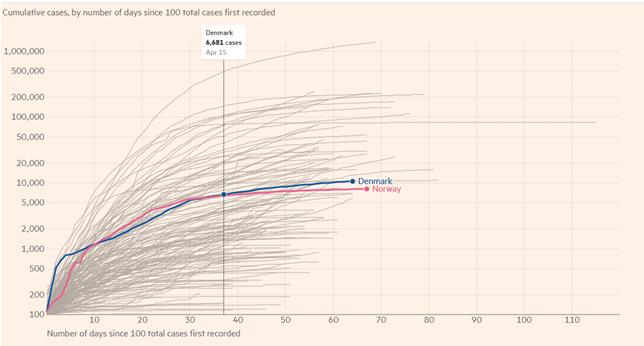

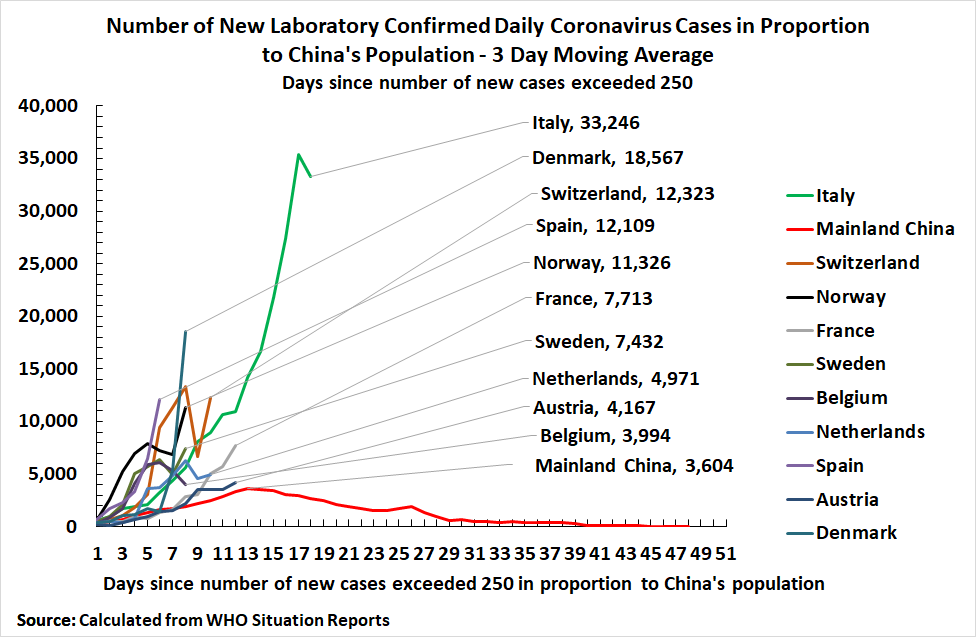

Cumulative cases for Norway and Denmark

The FT chart above shows Norway and Denmark had comparable

trajectories and almost exactly the same total number of cases at April 15,

just under 6,700 cases. Since that time,

Norwegian cases have risen to 8,142 and Danish cases have risen to 10,675.

Following the return to school in Denmark about 1 month ago

cases have risen by just under 60% while Norwegian cases have risen by

21%. Danish cases have risen almost 3

times in proportion. Of course, other factors may be at work. But the timing and correlation are striking.

Gavin Williamson says that the government is following the

Danish approach in re-opening the schools.

Re-opening schools now would be the wrong lesson to draw.

The global coronavirus crisis is a

public health catastrophe with extremely severe social and economic

consequences. But the driver of those consequences is the coronavirus itself. Therefore

all attempts to prioritise the impact on the economy – as most of the Western

governments have done – are bound to lead to a prolonged catastrophe. This will

involve, and is already causing, a far greater and avoidable death toll and a

much more severe economic and social crisis as a result.

The Western governments have effectively

put ‘the economy’, that is the profits of firms first, before the well-being of

the population. We will all be affected by the profound consequences for many

years to come.

Herd immunity as policy

Infamously, the principal adviser to

Boris Johnson told a private gathering that the government’s policy was “herd immunity, protect the economy and

if that means some pensioners die, too bad” (£). Although

this was later denied, a recent article on Reuters

news agency, makes it absolutely clear that this was in fact official

government policy. On March 2nd the government was told that,

without a lockdown and the many other measures pursued in China, there could be

around 500,000 deaths in this country. Yet Boris Johnson did not announce what

was initially described as a ‘severe lockdown’ until three weeks later on March

23rd. Meanwhile both Johnson and the chief scientific adviser had

publicly promoted the idea of herd immunity as government strategy, which

Johnson himself described as ‘taking it on the chin’ (video).

The UK

experience is not unique. The Trump administration pursued the same strategy

and only did a U-turn on its rhetoric at the same time as the British

government in the third week of March. To differing degrees most Western

governments have pursued similar strategies.

It

should be clear that in the US and British cases the policy change is mainly

rhetorical. There is a very partial lockdown in Britain, with many

non-essential workers still obliged to travel to work, no mass testing, limited

PPE for medical workers, social care workers and many others, and no tracking

and tracing (which is impossible without mass testing). In the US, the partial

lockdown is even more lax, although the US has proved adept at international

piracy in forcing PPE to be redirected, even at the expense of ‘allies’.

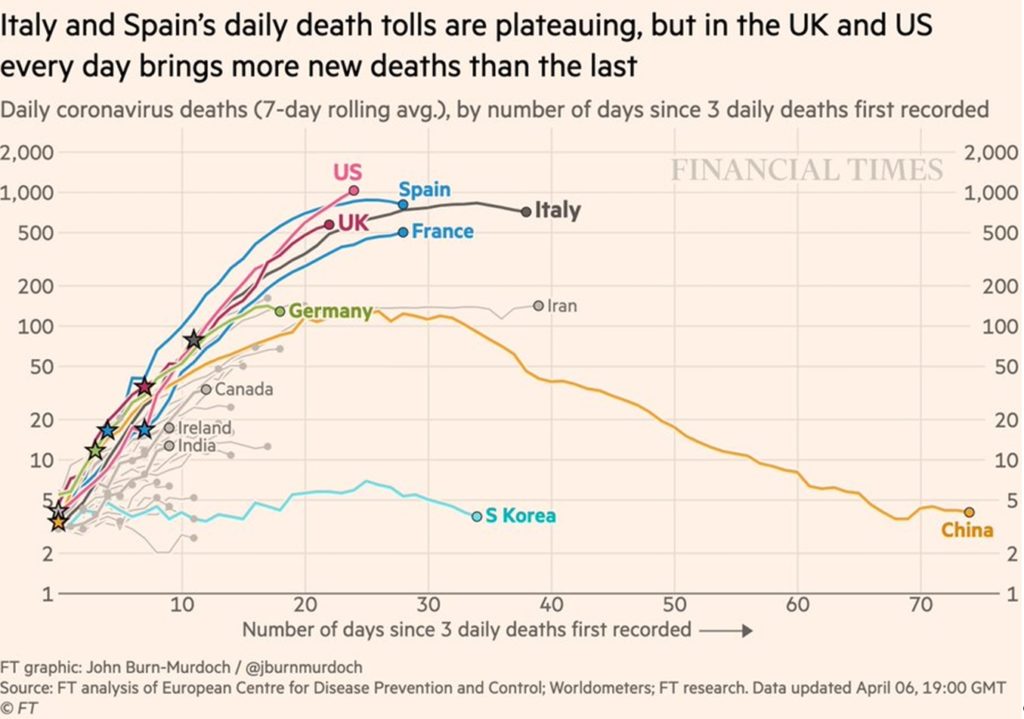

Many

other Western government have pursued a less extreme version of the same

policy, which has led Britain and the US to become world leaders in the growth

of the coronavirus infection rate, as this chart from the Financial Times

shows.

Chart 1. Death rates from coronavirus (log scale)

Sweden has

frequently been held up by right-wing commentators as the model

because it has almost no lockdown at all (except in higher education). But the

performance of Sweden is disastrous. To give one example, Sweden and Norway

(with half the population) recorded their first known cases at approximately

the same time. Norway’s death toll stands at 127 in the latest WHO situation

report (number 86), while Sweden’s death toll is unfortunately

much higher at 1,033.

In general, the Western countries have

pursued a half-way house between ‘herd immunity’ and an effective lockdown. The

verdict is clear. In the 5 largest Western European countries (Spain, Italy

Germany, France and Britain) the most recent daily reported total was just

under 20,000 new cases and just under 3,000 reported new deaths. In the US

alone there were over 24,000 cases and over 1,500 new fatalities.

Other

countries, such as Germany have had some important success because of mass

testing and tracking and tracing. But because all measures are necessary, partial

measures will fail. The WHO described it as a ‘whole of government, whole of

society’ response in China which required a severe lockdown in Hubei province. Germany’s

testing has been excellent compared to Britain, but its lockdown has been lax

compared to China. In the latest WHO report the German case load had risen to 1,537 per

million, and deaths had risen to 39.2 per million. The

comparable data for China is 61 cases per million and 2.4 deaths per million.

Yet another

bank bailout

It is

clear that the Western governments in general attempted to put the economy

first in their response to coronavirus crisis. The unavoidable consequence of

that policy was as Dominic Cummings put it, ‘if some old people die, too bad’. It

should be noted that this is a propaganda line the

BBC is still pursuing, arguing that many people would have died anyway.

The

various ‘bailout’ packages should be seen in this light. They do not stand in

contradiction to the blatant disregard for the well-being of the population but

are an extension of it.

In

Britain, the March Budget contained just £5bn in spending measures to offset

the effects of coronavirus. This is a fraction of the structural underfunding

of the NHS (about 1.6% of GDP compared to Germany, equivalent to £35bn annually).

As explained previously by SEB, the Budget’s big

increase in government spending for next year is Brexit-related, not to tackle

the health catastrophe.

As for

the follow-up package of measures from the Chancellor, the numbers themselves

determine the character of the bailout. Of a total of £350bn in the package,

£330bn is a bank loan guarantee scheme. This prevent banks from incurring losses

if the loans go bad, although does not oblige them to lend, or even limit the

rate of interest they can command. It is a bank rescue package. By contrast,

local authorities which have to deal with additional spending on homelessness, free

school meals, support for the elderly and so on, have been provided with just

£1.6bn, or about £24 for every person in the country.

The

idea that the Tories are ‘implementing half the Labour manifesto’ is completely

muddle-headed. Austerity is the transfer of incomes and assets from workers and

the poor to big business and the rich. It should be clear that the Chancellor’s

measures are more of the same. The cost of the bailout will be borne by

taxpayers, and most tax revenue is either in the form of income tax on the pay

of workers and the poor, or on their consumption, through VAT. This is not

partially implementing Corbynism. Corbyn would have implemented the opposite

policy.

The

claims for the Trump bailout measures (incorrectly labelled a ‘stimulus package’)

are just as frequently false. Of the $2trillion bailout, just $250bn is

earmarked for households. The overwhelming bulk is direct subsidies for

businesses and banks. The widely touted transfer of $1,200 for adults earning

less than $75,000 a year is meant to cover them for 3 months! Many will wait

months more to receive it. Undocumented workers, the unemployed, those without

unemployment insurance and many young workers are not covered at all. The

actual beneficiaries of the Trump bailout are big businesses and the banks.

It’s not the

economy, stupid

It is

impossible to deal with the huge economic and social consequences of the

coronavirus crisis without dealing directly with the coronavirus crisis itself.

Measures to ameliorate hardship and prevent unemployment surging and business closures

are absolutely necessary and the Western governments have generally failed to

provide these in sufficient amounts, or with the appropriate priorities.

But the

economic crisis cannot end until the source of it is ended, which is the public

health crisis.

Ignoring

this fact has led big business, their lobbyists and friendly commentators to

raise the clamour for an early end to the lockdown. But simple logic dictates

that this will end ignominiously, if not catastrophically. The lockdowns are

the product of the correct view that disrupting physical interaction is

necessary to introduce a series of breaks into the pattern of virus spreading. The

more comprehensive the lockdown, the quicker the spread of the virus is halted,

and vice versa. The experience of China is positive confirmation of that, while

the experience of Britain and the US is the negative confirmation.

Therefore,

any premature ending of (even a partial) lockdown will risk a renewed spread of

the virus, especially if there is also no mass testing, tracking and tracing,

and quarantining of the new cases.

As the

bulk of the population that can has acted on government social isolation advice

and has accepted this logic, it is necessary for the big business interests

that want an early end to the lockdown to propose a new argument. This has come

in the form of the claim that ‘the lockdown is worse than the virus’.

Of

course, the lockdown is worse than the virus for the resumption of production

and profits. But the claim that the lockdown is worse for public health, in

terms of mental health, suicide, poverty-related disease is false.

A book

by economics Nobel laureate Angus Deaton,, Deaths and Despair and the Future of Capitalism,’ (webinar link here) is based on studies

of countries such as Greece and Spain during and after the economic crisis that

began in 2008. He concludes that it is not recessions themselves which reduce

longevity, but austerity. Some factors, such as mental health, suicide and the

increase in poverty do increase mortality rates. But other factors, such as

reduced vehicle accidents, lower alcohol and drug-related accidents and lower

accidents at work (especially construction) are significantly greater effects

in the opposite direction.

The

argument that we need to get back to work for public health reasons is dangerously

false.

Economic

outlook

Even

so, the global economic outlook is catastrophic, the negative impact on the

global economy certainly worse than was experienced in 2008-09. Within that it

is clear that:

In the Western

economies black people, ethnic and other minorities are disproportionately hit,

along with poorer people and that they are also bearing the brunt of the death

toll among essential workers

There is a

potential catastrophe on an even greater scale among the developing economies,

whose capacity for lockdowns and social isolation is limited by objective

social conditions and where health care systems are often rudimentary

International

and national bodies are obliged to provide forecasts of the economic outcome of

the current crisis and are now doing so. But these must be purely speculative,

since the economic crisis is caused by the public health crisis and can only be

ended once the outbreak is fully brought under control.

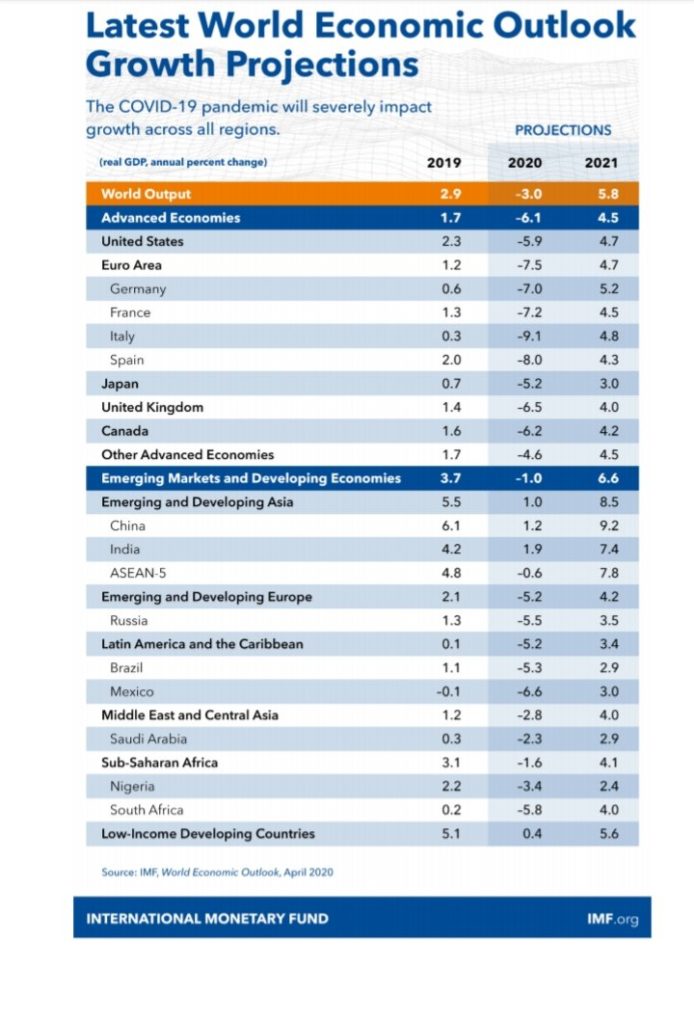

Therefore,

the forecasts from the IMF World Economic Outlook shown in Chart 2 below are

even more uncertain than usual.

Chart 2. IMF Real GDP Growth Projections April 2020

These

are unprecedented levels of contraction for the world economy as a whole. As a

result, even if there is an early end to the public health crisis the

consequences of such an enormous contraction in output would be felt for many

years to come.

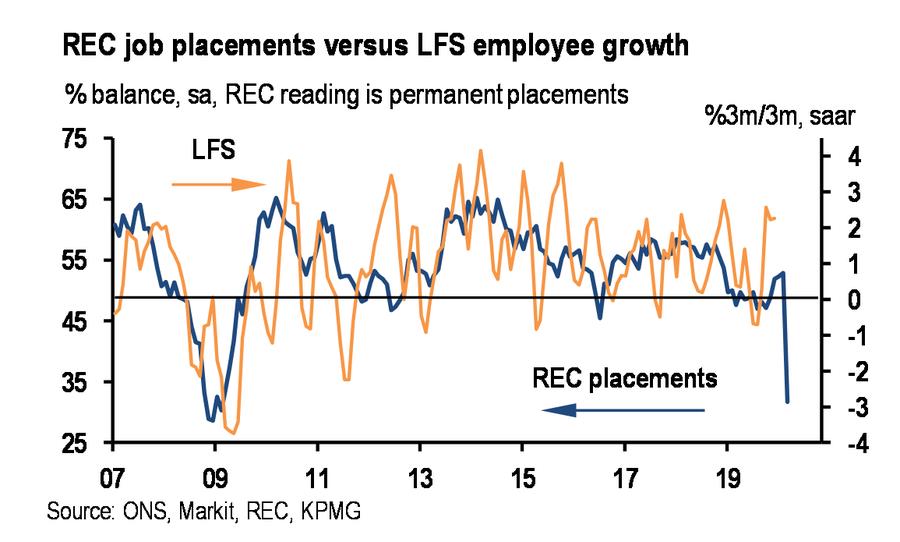

Short-term

indicators tend to be even more severe. In the US, electricity usage is currently

down about 17% down from a year ago and the FT reports

British energy usage contracting by around the same proportion. One of the most

negative indicators is the impact on employment. In the first 4 weeks of the

very partial US lockdown, there were 22 million new

claims for unemployment insurance even though these only include those workers

eligible for unemployment insurance. In Britain, the indicators show that the

impact on jobs is also severe. The REC survey points to an immediate

contraction in jobs of 3% of total employment. This is equivalent to an

immediate loss of 1 million jobs.

Chart 3. REC Jobs Survey versus Labour Force Survey

Employment Growth

The truth is that it is impossible to

provide any reliable forecast because the starting point for that must be

ending the coronavirus itself. Unless and until that is achieved, the economy

will continue to contract and unemployment will continue to rise. It is also

highly doubtful that there will be a sharp ‘V-shaped recovery. But SEB

will return to that point in a later piece.

Three points of confusion

At a time of crisis there is a natural

and inevitable tendency to cling to old truisms. Unfortunately, the truisms can

be wrong and in some cases are a cause of the crisis. Three points of confusion

have arisen in particular that are worth refuting, because they are quite

widespread (even though there are many others).

‘Preserving the economy’. The assertions of

Western governments should not be taken at face value when they say that they

are also trying to protect the economy, while trying to save lives. If they

were trying to save lives they would have followed the Chinese approach and the

result would have been deaths in the hundreds, rather than the tens of

thousands. But it is also mistaken to believe their assertions on the economy. Their

economic aim is to preserve profits. This can be demonstrated through the

experience of austerity, which was not generally imposed until 2010, when there

was generally already a recovery under way after the recession in 2008/09. It

was widely understood (including by those who implemented it) that austerity

would hurt growth simply by reducing government expenditures alone. But its

purpose was to transfer incomes to big business and the rich, not economic

growth. The key variable targeted by Western economic policy, never stated, is

profits not GDP.

‘Austerity is ended’. As shown previously, the

bailout packages launched by the Western government are primarily aimed at

supporting banks and big business (the key extractors of profits). The bailouts

range between inadequate and non-existent for everyone else. The most marginal

workers get next to nothing. This is all from the first pages of the austerity

playbook. After the bank bailout comes the austerity, and the British

Chancellor has already begun to hint at renewed austerity. It is highly likely,

for example that there will be reductions in pensions, renewed pay freezes, a

prolonged much higher level of unemployment. Under these circumstances it would

be no surprise if many businesses will try to make the temporary cut to 80% of

wages permanent.

‘This is our 1945 moment’. Unfortunately,

among the Western left, and especially in Britain there is a widespread myth

that the enormous sacrifices and hardships of World War 2 inevitably lead to a

much better conditions in its aftermath. But this was not true after World War

1 and nor was it true at a more prosaic level in 2008-09. It was the

international defeat of fascism beginning at Stalingrad in 1943 which led to

global upsurge in the fight against reaction. In Western Europe this was

manifest as the ‘1945 moment’ of the introduction of the ‘welfare state’,

decent health care, unemployment insurance and so on. 1945-style gains will not

be handed to any working class coming out of this crisis. On the contrary, it

will require huge international victories, relying on international allies to

achieve those gains.

SEB will return to these aspects of the crisis in

future postings, to develop these points and highlight the dangers of the

current crisis and the working class response.

Immediate action needed

But

there is an immediate crisis, where thousands of people continue to die daily. It

is possible that the failure of the Western governments could lead to an even

more enormous loss of life in some Latin American, Africa and the poorer Asian

economies.

Thankfully,

the number of deaths in developing countries is currently much more limited

than in the Western epicentres. But there are no guarantees that will remain

the case and the consequences could be calamitous.

Therefore,

in terms of the principles it is clear that public health must be the priority,

not private profit. The first demands must be international in scope; we need

to learn from where the actions worked and China holds first place in that. There

must also be full debt forgiveness for every developing economy which begins to

experience a serious outbreak (perhaps defined as more than 1 death per

million) in addition to the foreign aid budget being increased and redirected to

cope with increased health and social requirements.

In

the Western countries themselves, the epicentres of the outbreak, full

lockdowns are required and so all non-essential workers must be ordered to stay

home on no less than their current pay if they are on average incomes or below.

Full PPE must be provided for all essential workers. Persistent, mass testing

must be conducted, along with tracking and tracing in line with WHO guidelines.

There must be no racist scapegoating, no Sinophobia or attacks on faith

communities, as well as acceptance of refugees and an end to all immigration

detention. The elderly and the disabled must not be regarded as second-class or

even expendable.

When

the appropriate time comes, as new fatalities fall into single figures, a

controlled and monitored easing of the lockdown can begin, but only if mass

testing, tracking and tracing capacity is already in place. No worker should be

forced to return to work until the crisis is ended.

These

and other demands can be formulated to try to unify all those who want to put

people first in combatting the crisis. The next piece on SEB will deal

with these demands more concretely.

Through tremendous sacrifices China has brought the coronavirus under control – the number of new daily cases being reduced from the peak of 3,887 on February 5 to 11 on March 13 (7 imported from outside China), a decline of 98.2 percent. In doing so, the Chinese authorities performed an enormous service not only to the Chinese people but also gave a crucial opportunity to the whole rest of the world to prepare.

To precise, through the determined fight against the virus, China bought almost two months warning to the rest of the world before the coronavirus began to significantly spread there. But the terrible truth is that while China benefited greatly from determined action against the virus, the facts show the West entirely wasted this precious time.

Because the huge economic effect of the coronavirus cannot be separated from its medical impact, it is necessary to study the two together. This is due to the fact that the coronavirus is simultaneously a supply and demand side economic shock. The supply side shock is that the health risk means the work force cannot produce normally, causing huge falls in output. The demand side effect is that significant numbers of services and goods, if they are not consumed in the short term, will not be purchased at all – particularly in the service sector. The falls in China’s official manufacturing PMI, to 35.7 in February, and the non-manufacturing PMI to 29.6, reflected this impact within China.

The facts show clearly that the spread of the virus in the West is now already reaching levels far higher than at the worst point of the crisis in China. As will be demonstrated, nothing short of a disaster is now unfolding in Europe. The situation in the U.S., so far, is following Europe with a delay of about 10 days.

This fact that the intensity of the coronavirus crisis in Europe is already worse than at the worst period of the virus in China is concealed by misleading comparisons of the absolute number of cases in Europe compared to China. But, for example, China’s population is 17 times larger than Germany or 23 times larger than Italy. To realistically measure the relative impact of the coronavirus crisis in Europe compared to China, it is necessary to measure the virus’s spread in proportion to population.

The peak day for the number of new virus infections in China was February 5 at 3,887. But according to the World Health Organization’s daily situation reports, at the time of writing the peak day in France (780 on March 13) was equivalent to over 16,000 relative to China’s population, in Spain (1,266 on March 13) over 38,000, and in Italy (2,651 on March 12) over 60,000.

Western governments are openly telling their populations that it is only a matter of time before the number of deaths becomes very high. British Prime Minister Johnson announced: ‘Many more families, are going to lose loved ones before their time.’ Italy’s cumulative death toll (1,400 as of March 14) would be equivalent to around 33,000 in a country with China’s population!

This data makes clear Europe’s situation is already far worse than at the worst period in China. In short, the European governments totally failed to use the time they had to prepare for the virus to arrive.

The virus’s huge economic impact in the West follows from this medical disaster. Data on the impact on production of the virus in the West is not yet available. But the Western economies were already weakening when the coronavirus hit. The peak of the current U.S. and EU business cycles was in the second quarter of 2018. From then until the fourth quarter of 2018, the U.S. GDP growth had fallen from 3.2 percent to 2.3 percent, and the EU’s from 2.5 percent to 1.2 percent. Without an extraordinary stroke of luck the virus hitting already slowing Western economies will push them into recession.

As Western companies had already accumulated very large debts any resulting revenue slowdown, creating difficulty to repay this debt, carries a risk of transmission of crisis into credit and other markets.

This explains the literally unprecedented impact on Western share markets. The fall of U.S. share prices into a bear market, a 20 percent fall, took only 16 days – even more rapid than in 1929.

Why, when China has been getting the virus under control, has there been such a catastrophic failure in the West? The reason is in large part because instead of learning the positive lessons of China’s ability to control the virus, the Western media and the U.S. government engaged in anti-China propaganda. The bitter truth is that the anti-China propaganda campaign has to some extent contributed to the West being negligent to the looming crisis and they are now facing a medical, human and economic disaster.

The coronavirus is literally a life and death issue for

millions of people – this is why it is totally dominating mass attention and

the media. It has also simultaneously produced a gigantic global economic shock.

It is impossible to separate these two issues because the coronavirus’s impact

on the global economy depends on whether it can be brought under control and

how fast.

It is crucial to understand that we are only seeing the

beginning of this crisis – the coronavirus’s impact is only going to deepen in

the West. This is due to the fact that the coronavirus crisis in Europe and the

US is now far worse than at the worst period in China and so far is continuing

to worsen. Indeed, the failure of the capitalist countries to control the virus

has produced a disaster – the only question is whether it will now worsen to

create a catastrophe.

Taking first the least important of the two aspects of

health and the economy, the economic one, the coronavirus is unusual in being

simultaneously a supply side and a demand side shock. The supply side shock is

that the health risk means the work force cannot produce normally, causing huge

falls in output. The demand side effect is that significant numbers of services

and goods, if they are not consumed in the short term, will not be purchased at

all – people will not travel to work twice to make up for when they did not go

to work, they will not have twice as many meals in restaurants etc.

This was reflected in the huge falls in output in China in

January-February, as the country basically shut down its economy to the level

necessary to contain the spread of the virus, and to safeguard China’s people

from it. The decline of China’s industrial production compared to the year

before of 13.5% in January-February, the fall of 20.5% in retail sales, and the

25.5% fall in fixed asset investment showed this impact.

But China’s drastic economic action was entirely justified in

the more important human terms as the coronavirus was decisively brought under

control. In only five weeks and two days from the peak level of daily

infections, that is between 5 February and 13 March, the number of daily new

cases in China was reduced from 3,887 to 8 – that is by 99.8%. This shows that

decisive action, giving a total priority to safeguarding people’s health, can control

the virus.

By 15 March only 0.006% of China’s population had been

infected with coronavirus. This rapid reduction of the spread of the coronavirus,

in a matter of weeks, and with only a very small part of the population

infected, is in total contrast to the British government projecting that the

outbreak may last for very many months to the end of the year, that people over

the age of 70 must prepare for four months of self-isolation, and that 60% of

the population need to become infected to achieve ‘herd immunity.’

The coronavirus situation in the West is far worse than in China

But the economic impact in the West, seen immediately in the

huge stock market falls but which will rapidly spread into the productive

economy, was not due to China’s coronavirus situation but to the coronavirus

situation in the West – which is now far worse than anything seen in the worst

period in China.

That the global economic impact is being driven by the coronavirus

crisis in the West, not in China, is clearly shown by the fact that during

January-February, the worst coronavirus period in China, US stock markets were

still soaring – the Dow Jones Industrial

Average’s all-time peak was on 12 February when the coronavirus was raging in

China with 2,015 new cases that day. The recent most severe Western stock

market fall in contrast, on 9 March, came when the coronavirus was coming under

control in China – the number of new cases in China on that day was only 40.

In terms of the global situation, sharp declines in the

number of new coronavirus cases in China confirm that the coronavirus outbreak

there, while not over, was decisively being brought under control. Therefore,

production and supply chains both in China, and from China to the global

economy, would begin to improve.

But despite the sharp improvement of the situation in China the

huge fall in the Western stock markets was entirely rational because they

reflected a correct understanding that the place the coronavirus is presently out

of control is not China but in the West. Indeed, it is crucial to factually understand

that the speed of spread of the virus in key Western countries is now very much

faster than at the worst period in China. This reality is merely obscured by

making comparisons in terms of the absolute number of cases, because China’s

population is so much larger than any capitalist country except India.

For example, attempts have been made to hold up success in

South Korea in controlling the virus as equivalent to China’s. But this is factually

not nearly the case. Mainland China’s worst day for the number of new

laboratory confirmed coronavirus cases was on 5 February at 3,887. The worst

day in South Korea was on 29 April at 813. But to assess the relative impact of

the coronavirus on a country this comparison in terms of absolute numbers is

highly misleading for the simple reason that Mainland China’s population is more

than 27 times that of South Korea. Therefore 813 cases in South Korea, in

proportion to its population, is equivalent to 21,993 in Mainland China. The

relative size of the peak number of new cases in South Korea was more than five

and a half times as high as in China. Furthermore, by 15 March there were still

76 new cases reported in South Korea which is equivalent to 2,056 in proportion

to the population of China – on that day in China there were only 20 cases.

Therefore, South Korea has made welcome progress compared to European countries,

but its success is far less that in China – the number of new cases in South

Korea on 15 March, relative to its population, was a hundred times higher than

in China.

The situation in Europe is now disastrously worsening when

measured in relative terms – which gauges the real impact of the virus. China’s

population is 17 times Germany’s, 21 times Britain’s and the north of

Ireland’s, and 23 times Italy’s. Recalling

that the highest number of new coronaviruses cases in China on a single day was

3,887, the number of new daily cases reported by the WHO on 15 March in Germany

(733) was over 12,000 relative to China’s population, the number of new cases

in France (829) was equivalent to almost 18,000 relative to China’s population,

the number of new cases in Spain (1,522) was equivalent to almost 46,000

relative to China’s population, and the number of new cases in Italy (3,497)

was equivalent to almost 82,000 relative to China’s population. So, in

proportion to the population, the number of new daily cases in Germany was

three times as high as the peak in China, in France five times as high, in

Spain 12 times as high, and in Italy 21 times as high.

The relative impact of the coronavirus is therefore already very

much worse in Europe than at the most severe period in China. Furthermore, the

number of European cases is rising. While China is bringing the coronavirus

under control, failure of the European capitalist countries to take similar

measures to China has led to the virus spreading extremely rapidly.

Economic and market impact

The global economic impact follows inevitably from this

failure in the West to contain the virus. Europe is the world’s largest

economic area – taken together even bigger than the US. Therefore, the fact

that the relative speed of spread of the coronavirus in Europe is far faster

than at the worst period in China has a very severe impact on the world

economy. This by itself inevitably has a harsh effect on Western stock markets

and economies. This negative economic shock then also explains the plunging oil

price and the oil production war waged by Saudi Arabia, Russia etc. The oil price shock then worsened the stock

market falls through the crash in energy company share prices.

The situation in the US is perhaps two weeks behind Europe –

although this is difficult to judge precisely as the US authorities are taking

a dangerous approach of minimising the virus’s danger. Trump initially tweeted

that the coronavirus is a less serious risk than ordinary influenza. As is

widely understood a similarly reckless policy is being adopted by the British government.

The US appears in key cases to either have a totally

inadequate number of virus test kits or may be taking the criminal decision not

to test – a policy now being adopted by the British government. For example, to

take the worst case, the Washington

State nursing home which suffered the most severe outbreak in the US, with

19 suspected deaths, waited days before receiving kits to test others – which

revealed another 31 cases. A patient must pay over $3,000 for a coronavirus

test in the US so many without medical insurance will not take tests.

There are also extreme disparities between US data and that

which is being supplied to the WHO, greatly understating the coronavirus’s

spread in the US – presumably this data is supplied by the US authorities. For

example on 9 March the official data published by the WHO, doubtless US supplied,

showed only 213 US cases while the very reputable Johns Hopkins University,

which has collated reports, already found 761 US cases – more than three times

as high as the figures supplied by the US to the WHO. This disparity between

data supplied to the WHO by the US and studies by reputable institutions in the

US is continuing.

In Europe, apart from Britain, the authorities appear to be

keeping serious records, but as already noted these reveal that the spread of

the virus in key countries is proportionately more rapid than at the worst

period in China. It is unclear if the US situation represents severe lack of

preparation in light of two months warning of the arrival of the virus,

organisational chaos, or the administration’s severe underestimation of the

seriousness of the virus or deliberate measures to under report cases for

reasons such as aiding the stock market.

The British government’s decision not to test all cases is

clearly a deliberate policy to attempt to try to keep the number of reported

cases down. This is criminal irresponsibility – without testing the spread of

the virus cannot be traced and those who do recover from symptoms have no idea

whether they really had the coronavirus or not. This furthermore means that the

most immune group, those who have had the virus and have recovered, do not know

that they are the best people to help the most vulnerable as they have never

been tested.

In summary, in addition to the direct health impact, the

severe stock market falls came when China was overcoming the virus but was because

an extremely serious situation was revealed in Europe and great lack of clarity

in the US – the stock market crash, logically, was due to the coronavirus

situation not in China but in the West.

The economic perspective depends on the medical policy

It is impossible to precisely estimate the precise depth of

the economic downturn, although it will be sharp, without knowing whether the

coronavirus can be brought under control in the West. While emergency measures in

slashing interest rates and undertaking Quantitative Easing are being taken by

the US Federal Reserve, other central banks, and capitalist governments, many measures

cannot be taken while the health emergency continues. People will not go to shop,

to restaurants, to travel for holidays etc, whatever the economic inducements,

if they think they may die as a result. Many economic recovery measures therefore

can only be taken when the medical situation is ended.

As China is getting the coronavirus under control it can already

begin to prepare economic recovery measures. But until capitalist Europe is

prepared to take the decisive measures to control the coronavirus, similar to

those used in China, the medical situation will continue to deteriorate, and it

cannot launch any effective economic recovery measures. Simultaneously the medical

situation in the US remains entirely unclear due to the entirely wrong approach

taken at the beginning of the outbreak by the Trump administration. The World

Health Organisation has explained

the situation clearly in a virtually unveiled attack on the policy of the

British and US governments: ‘The most effective way to prevent infections and

save lives is breaking the chains of transmission. And to do that, you must

test and isolate. You cannot fight the fire blindfolded. And we cannot stop

this pandemic, if we don’t know who is infected. We have a simple message for

all countries Test, test, test. Test every suspected case.’

The background in the Western economies when the coronavirus

hit was clear. Their economic situation was weakening since the peak of the

current US and EU business cycles in the second quarter of 2018. From then

until the 4th quarter of 2018 US GDP growth had fallen from 3.2% to 2.3%,

and the EU’s from 2.5% to 1.2%. The coronavirus will clearly weaken this

economic growth further – by how much depends, as already analysed, on how

rapidly decisive European and US anti-coronavirus measures are taken. The UK

recorded zero GDP growth in the three months to January, before the coronavirus

impacted this country. Given this weakness before the coronavirus struck it

will therefore be a miracle if a recession in the West is avoided.

The experience of China shows the coronavirus can be brought

under control. But so far, the capitalist Western countries are not taking

these measures. There is therefore already a disaster in the West due to the

failure of response to the coronavirus. The only question is whether the

disaster will worsen further into a catastrophe.

This is an updated version of an article from John Ross,

which first appeared in Chinese in Global Times

The claim from the Tory government and its army of media

supporters that the latest Budget has ended austerity is completely false. It

is very important for the left and the labour movement as a whole that they

grasp the character of the new attacks to come, so that they can resist them.

In effect, this is a Tory government of a new type. Previously,

since austerity was first implemented in 2010, the Tory governments have

transferred incomes from workers and the poor to big business and the rich. This

is in the hope that both increased rates of exploitation and the transfers of

funds themselves will encourage business investment. But the encouragement to

private investment has been a dismal failure. Private investment growth is

officially forecast to be zero this year.

The new Tories want to provide further inducements to

private sector investment by increasing public sector investment. SEB

has argued vociferously for increased public investment over a prolonged

period. This not investment for its own sake, but to increase the productive

capacity of the economy (adding to the means of production) as the most

decisive factor in raising the output of the economy and therefore prosperity.

But these Tories intend the opposite. They want to increase

the rate of exploitation further, provide incentives to private business to

investment, and intend to do this by funding with investment with yet another

reduction of public services and (probably) public sector pay. They will further

shift the burden of the crisis onto the shoulders of workers and the poor.

Government current spending is being cut over

the medium-term.

There is a one-off boost, to cope with the

effects of their own disastrous Brexit

The projected rise in government investment (if

it materialises) will still leave total government expenditure lower than in

recent years

This means that the rise in public investment is

more than being funded by further attacks on public services and public sector

workers

There is a significant projected increase in net

government borrowing. This is despite a fall in debt interest payments, which

themselves are being used to boost spending in the short-term

This is not ‘deficit-financed growth’, as has

been claimed. It is the effect of weaker growth on public finances, pushing both

tax revenues lower and automatic outlays (such as welfare payments) higher

In fact, the current year for which the OBR

provides an estimate and the subsequent 5 years’ forecasts are the weakest on

record for such a prolonged period

Taken together, SEB can find no recorded

10-year period of real GDP growth where every year is below 2%. This is what

the actual recent growth years’ growth rates will amount to, combined with the

OBR forecasts

There is a sharp one-off rise in government

current spending next year. This is not to combat the effects of the

coronavirus crisis, which is current. Instead, it follows the withdrawal from

the EU at the end of this year. It clearly indicates the government expects a

very negative outcome from the Brexit it is planning

There is nothing substantial in the Budget to

address the climate crisis, and the need for large-scale investment in

renewable energy production, or conservation

Austerity resumed

Despite the mass of commentary suggesting that austerity is

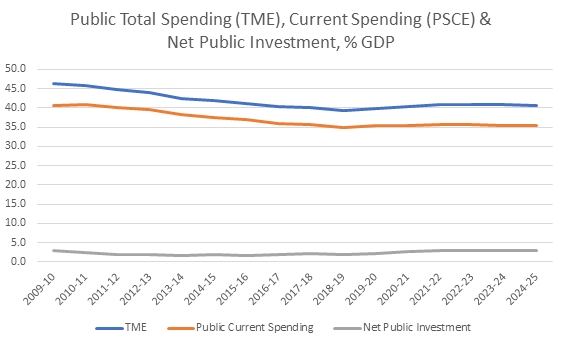

over, it is very simple to demonstrate that is not the case. The chart below is

taken from the OBR databank and shows total for public spending (TME), current

(or day-to-day spending, PCE) and net public spending as a percentage of GDP.

Chart 1. UK Public Spending Totals, Current Spending and New

Public Investment, as a % of GDP

The chart lines show a downward trend of total government

spending. For the 6 years of OBR estimates and forecasts from 2019/20 to

2024/25 average TME (total government spending) is 40.5% of GDP. For the

preceding 6 years it was 40.8%. Total government spending will be lower and austerity

is not ending at all.

The big impact will be felt by public current spending. Over

the same 6-year periods, Public Sector Current Spending (which includes health,

education, welfare and so on) will fall to 35.5% of GDP, from 36.5% of GDP.

By contrast public sector net investment is projected to

rise from 2% of GDP last year to 3% by the end of the 6 years of the OBR’s

forecast period. But it should be clear, it is ordinary people who most rely on

public services who will be paying for this increase. Furthermore, as the OBR

itself points out, there is a persistent and large shortfall between the

projections for public sector investment and what actually takes place.

Planning investment is not the same as delivering it.

A significant one-off

boost to spending

The basis for all the hyperbole and false claims about the

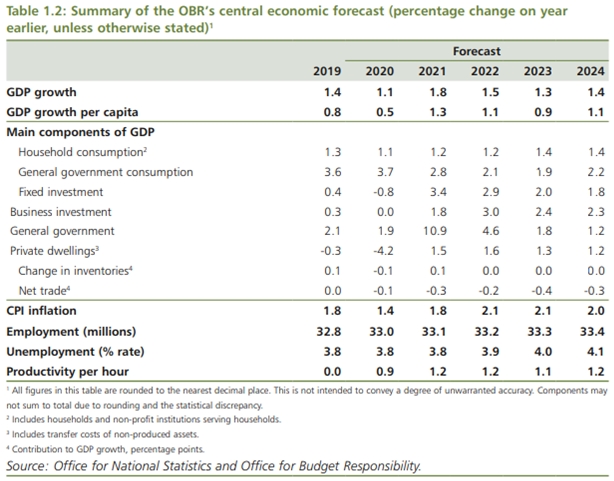

Budget is because of a one-off increase in government spending next year. This

can be shown in one of the key tables from the Treasury’s Red

Book.

As the table shows general government spending receives a

very large boost in 2021, rising by 10.9%. This falls back in the following

year and austerity returns in 2023 and 2024. It is important to note that the

growth rate of this measure of government spending is even slower than in the

most recent years, 1.8% and 1.2% in 2023 and 2024, compared to 2.1% and 1.9% in

2019 and 2020.

This increase in government spending is not

coronavirus-related, which is a current crisis that the government will be

hoping is over before the end of this year. Instead, it is a response to the

Withdrawal Agreement from the EU which does end in December of this year. Clearly,

the government expects a large negative shock from the Brexit it intends to

carry out, and the increased spending is an attempt to offset its worst

effects.

The attempt is only partly successful, using their own data.

Real GDP growth is expected to rise to 1.8% in 2021. However, general

government expenditure accounts for about 40% of GDP, so a one-off increase of

nearly 11% should lead directly to a boost in GDP of well over 4%. But the

projected increase is just a fraction of that, with real GDP rising from just

1.1% in 2020 to a very modest 1.8% in 2021, when the spending is to take place.

Clearly, the implicit assumption is that without the one-off spending splurge,

growth would be sharply negative with the planned Tory Brexit.

Miserably low growth

The official projections for real GDP growth are a terrible

indictment of government economic failures. This includes but is not confined

to their own assessment of the further damage they will inflict with their

preferred Brexit outcome. As the Treasury’s Table 1.2 above shows, there is no

single year in which real GDP growth reaches 2% in the recent data and the

forecast period.

This is unprecedented. It would amount to at least a 9-year

period of real growth below 2%, a lost decade. There is no equivalent in the

modern era of such sluggish growth, in either the Great Depression or the Long

Depression at the end of the 19th century.

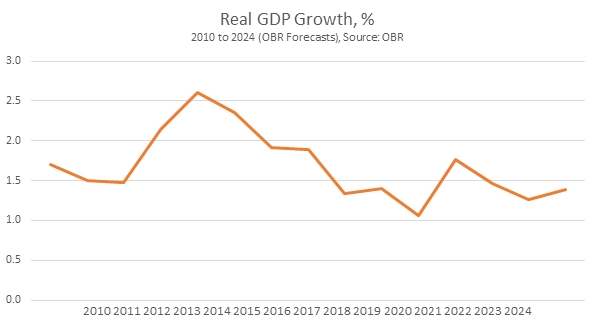

In fact, as Chart 2 below shows, the official outlook for

growth is even worse in coming years than the period immediately behind us, in

the years following the Great Recession in 2008.

Chart. 2 Real GDP Growth, 2010 to 2024 (Forecast)

This unprecedentedly weak growth has a series of

wide-ranging effects, depressing any rise in living standards or improvement in

public services. It also has the consequence of damaging public finances,

lowering the growth in government taxation revenues and automatically pushing

some government spending higher, for example in some welfare payments. This is

the cause of the large deficits in public finances that are forecast.

This is not ‘deficit-financed growth’ as has been claimed;

there is no growth and the economy slows. And, as already noted total

government spending will fall. These deficits are a reflection of economic

weakness, not ‘keynesian pump-priming’.

The multiple crises

There are a series of crises that the government is failing

to address: coronavirus, the weakness of the economy, the damage from its own

intention to crash out of the EU without a deal, the crisis in public services,

the unprecedented weakness in the economy and the existential threat of

catastrophic climate change. Measured against any of these challenges the

government’s response has been woeful.

On the coronavirus crisis, at every turn, it has unpicked

the measures praised by the World Health Organisation and enacted in China and

Viet Nam. Every excuse is made for inaction, that masks are not perfect,

testing is not 100% accurate, there is no point in heat-testing or even hand

gels at the airports, and so on. Instead, it has relied on measures to correct

some of the economic effects of coronavirus spreading. These steps, and many

more will need to be taken. But they are pointless unless and until government

is bearing down on the spread on the virus itself, which is clearly not the

case.

This will put enormous strain on the economy and public

services, especially the NHS (but also care for the elderly and education,

among others). Public services are already buckling under impact of a decade of

austerity. The UK already has below-average ratio of nurses to the population,

7.9 per thousand compared to 9.0 for the OECD as a whole. The only comparably

high-income country with a lower nurse/population is Italy (OECD

data).

It is clear that the increased spending in 2021 is not

coronavirus-related. Instead, it is a response to the effects of its own

determination to pursue a hugely damaging No Deal Brexit, presumably in order

to do a deal with Trump and adopt US business and labour market norms. The

government’s own forecasts show that a huge increase in spending to offset its

Brexit will produce barely a flicker of growth.

The planned increase in public investment is long overdue. But

it is very unlikely to produce either the transformation of ‘levelling-up’

across the country or the necessary corrective to abysmally low productivity

growth. For accuracy, the OBR forecasters do not expect either outcome.

One neglected factor, well established in classical

economics from Smith onwards, is that the effectiveness of all investment is

determined by the scope of the market. Any Brexit that takes this economy

outside the customs union will necessarily reduce the effectiveness of all

investment, because the market will also be severely contracted.

Finally, despite hosting COP26 in Glasgow later this year,

it is clear that the Budget contains no plan to address the climate crisis with

decisive action. Instead, this a government that has tried to press ahead with

plans such as the third runway at Heathrow and a road-building programme

regardless of the law. There was not even a pale imitation of Labour’s Green

New Deal, or anything similar. The Green New Deal is precisely the required,

targeted and ‘shovel-ready’ programme that could be implemented with

large-scale state investment – and is absolutely necessary. Instead, it seems

likely that The Tory recipe will be to search for new business-friendly

projects, such as more roads, and local and haphazard local projects.

When this fails to transform the economy, no doubt there

will be a new ideological offensive against public investment of all types. But

by then, US companies may be in control of large swathes of the public services

in this country.

There is no basis for the belief that the incoming Tory

government will end austerity. The reality is, from their own perspective and

from the interests they serve, the Tories will be obliged to deepen it.

It is extremely important that the labour movement, all

those who want decent living standards and public services and the left are not

suckered into believing that this Tory government will be any improvement on

its predecessors. Instead Johnson will pile up further misery, in addition to

the damage that has already been inflicted.

Early pointers

It is easy to list some obvious pointers to the government’s

direction on austerity.

First, the government’s legislative programme (the ‘Queen’s

Speech’) contains measures to outlaw strikes in the transport sector. There is

no need to outlaw strikes unless you are planning a confrontation with unions. If

the Tories are successful they will be emboldened to take on other workers. In

recent days, this

has been supplemented by the frame-up arrest of a union leader at a

peaceful picket as well as

an attack on the role or even the existence of the FBU from the

government’s inspectorate of fire services.

Secondly, in the same programme there is planned legislation

for permanent underfunding of the health service (as well as the threatened

removal of performance targets on waiting times at A&E services). In

real terms, the NHS funding law will provide the lowest cumulative rise in real

spending since the inception of the NHS. Labour attempted to amend it so

that the real increase is 4% per annum (which, although still modest rises by

historical standards takes some account of both rising population and the

higher inflation of medical equipment and drugs, plus the costs of

technological innovation). The amendment was rejected.

Thirdly, on this government’s own assessment the economy

will be severely hit by the Trump/Johnson Brexit. GDP

will be 6.7% lower by 2034 than it would if the status quo was maintained

and real wages 6.4% lower. This is not George Osborne’s stupidly exaggerated

‘project fear’ of immediate and sharp recession. It is this pro-Brexit

government’s own assessment of the consequences of something like a ‘No Deal’

Brexit. Typically, these official estimates tend to underestimate the damage,

as SEB has previously shown.

Finally, the economy is contracting. GDP in November shrank

by 0.3%, and outright contraction for the whole of the 4th quarter

is possible. With just one month’s data remaining it is almost certain too that

industrial production will have fallen for the year as a whole 2019 compared to

2018. Business investment is not rising and was lower in the 3rd

quarter of 2019 than it was for the same quarter in 2016.

The Tories are clearly faced with a worsening economic

crisis and the global economy offers no grounds for optimism. The idea that

they will address this crisis in the interests of the working class and the

poor is plainly ridiculous. Instead, they have given strong indications they

are gearing up for a major fight.

Why is there an

austerity policy at all?

Austerity has not been adopted because Tory politicians are

nasty. A change (in this case policy) cannot be explained by a constant.

SEB has repeatedly

explained that austerity amounts to a transfer of incomes from workers and the

poor to big business and the rich. So, in the very first austerity budget, the

Treasury documents showed that the projected revenue increase from raising VAT

of £13 billion (which mainly hits workers and the poor) was almost exactly the

same as the revenue lost by cutting Corporation Tax. The deficit was unaffected

by these measures, but income had been transferred upwards, to business and the

rich.

Using correct, Marxist terms there were two main elements to

austerity. The rate of exploitation was increased by cuts in real pay and

pensions. In addition, the social surplus was redirected away from workers and

the poor (cuts to welfare payments, rise in VAT) towards capital and the very

rich (tax cuts).

The combined effect of these measures was to force workers

to work more for less and to incentivise businesses to invest more. But the

second part of this policy has failed. Real wages did fall, but businesses did

not increase their rate of investment.

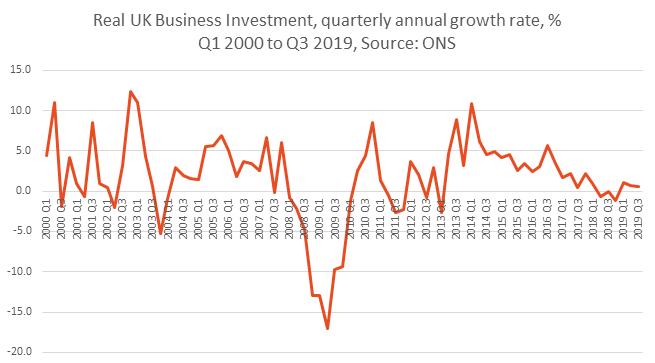

Fig.1 below shows the quarterly real annual rate of growth

for business investment from the 1st quarter of 2000. Business

investment has been slowing since the beginning of 2014 and is now beginning to

contract outright.

Fig 1. UK Business Investment, quarterly real annual rate of

growth from the 1st quarter of 2000 to 3rd quarter of

2019

In the last great crisis of British capitalism, Margaret

Thatcher was drafted in to do a very similar job to the one attempted by

Cameron and Osborne. Helped along by the huge windfall of North Sea oil

revenues, which were frittered away, she did produce a recovery in business

investment.

This was achieved by increasing the rate of exploitation. Cameron

and Osborne followed her example quite slavishly with spending cuts, real cuts

to public sector pay, cuts to welfare, cuts to taxes for the highest earners

and big business and privatisations. The cloak for these policies, the hue and

cry over the deficit, was different to their predecessor, inflation and

monetarism, but the project was broadly similar.

But the failure of the later Thatcherites can be shown

decisively in terms of business investment, the renewed expansion of capital

accumulation based on a series of defeats for the working class which allowed

her to increase the rate of exploitation.

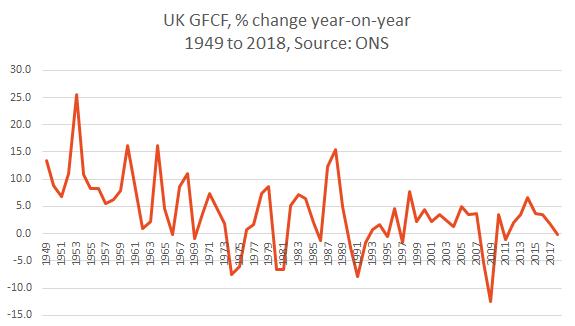

Fig.2 below shows the change in investment, (GFCF, Gross

Fixed Capital Formation) from 1949 onwards. Data for UK business investment

alone only begins in the 1990s. But, as the UK is a capitalist economy the

majority of the investment throughout will have been made by the private

sector, and so provides an approximate guide to what the relative impact of

Thatcherism was in this area.

Fig 2. UK GFCF, % change year-on-year, 1949 to 2018

In the immediate post-World War II era there were relatively

high rates of investment, but it slowed markedly. This reached outright

contraction in the early 1970s. Thatcherism was the antidote to this, by

cutting real wages and business taxes. Although there was initially a slump,

Thatcher’s project was successful and investment recovered throughout the

1980s, until it was brought to a crashing halt by the excesses of the Lawson

boom, where the government refused to use the oil revenues for public

investment and cut personal taxes instead, fuelling an unsustainable boom in

consumption.

As the chart shows, investment growth has only ever been

meagre since. Worse, the sharp contraction of the 2007 financial crash and the

2008-09 recession has only ever produced a meagre and short-lived investment

recovery. Investment is now slowing to a stop once more. Cameron and Osborne

completely failed to emulate Thatcher’s temporary ‘success’.

This will not happen. The splits in the British ruling class

over Brexit were set aside in their united opposition to Jeremy Corbyn

precisely because he intended to increase the role of the state in the economy.

This diminishes the ability of most parts of the private sector to maintain

their profits, or to expand them. It is anathema to them. The Tories will not

do it.

Instead, there are protections for workers that currently

apply in British law because of adopting EU law. Johnson has signalled

repeatedly that he does not want to continue with ‘alignment’ with EU laws and

rules. The Trump/Johnson Brexit will include a programme of rolling back workers’

rights.

The objective conditions are also set firmly against

Johnson’s economic policy being some version of Corbynomics-lite, as much of

the press seem to want to believe. The government’s own negative assessment of

economic prospects under Johnson’s Brexit policy will also mean a sharp

deterioration in government finances. Under those circumstances a sharp

increase in state investment is not impossible, but goes beyond the limit of

what the private sector is likely to voluntarily provide in the form of buying

increased government debt. Some form of compulsion, including nationalisations

and raising taxes on business would be required. The Tories will not do it.

From their perspective, the Tories cannot and will not

abandon austerity. Instead, it should be clear they are preparing for a further

attack, and that this time it will include major political struggles, over

union rights, the right to organise and to protest and other issues.

Climate

change is the most important political issue of our generation. There’s 99

percent scientific consensus that humans are causing global

warming and that, unless we stop putting greenhouse gases in the atmosphere,

life on earth will become increasingly unviable. If we continue at the current

trajectory in terms of greenhouse gas emissions, we’re facing over four degrees

Celsius of warming by the year 2100. David Wallace-Wells writes in his book The Uninhabitable Earth: A Story of the

Future that, “according to some estimates, that would mean that

whole regions of Africa and Australia and the United States, parts of South

America north of Patagonia, and Asia south of Siberia would be rendered

uninhabitable by direct heat, desertification, and flooding.”

According to

the UN’s Intergovernmental Panel on Climate Change (IPCC), humanity needs to

halve its greenhouse gas emissions by 2030 and hit net zero by 2050. If we fail

to hit those deadlines, hundreds of coastal cities (including New York,

Shanghai, Hong Kong, Mumbai and Lagos) will likely be permanently submerged;

the agricultural system faces collapse; wars will be fought over climate

change-induced scarcity of resources; and there will be hundreds

of millions of climate refugees. Floods, droughts,

hurricanes, typhoons and wild fires will become so commonplace as to barely be

newsworthy. The results of climate change are already all too visible: 18 of

the 19 warmest years on record have all occurred

since 2001, and we’re witnessing an unusually high rate of

extreme weather events.

Most

environmentalists agree that the safe upper limit for global warming before the

planet reaches an irreversible tipping point is 1.5 degrees centigrade. Bearing

in mind that the average global temperature today is already

0.9 degrees higher than it was in 1880, we’re only left with

0.6 degrees before we hit the point of no return.

What needs

to happen?

There is one

critical target to focus on for the next decade, as outlined in the IPCC

Special Report on 1.5 degrees, which is to reduce global carbon emissions to 50

percent of current levels.

Labour’s

manifesto sets out an even more ambitious target, aiming to “achieve the

substantial majority of our emissions reductions by 2030 in a way that is

evidence-based, just and that delivers an economy that serves the interests of

the many, not the few.” Labour has made a world-leading pledge to generate 90%

of electricity and 50% of heat from renewables and low carbon sources by 2030.

Globally,

the target will be to get to net zero emissions by 2050. Note that ‘net zero

emissions’ doesn’t necessarily mean not emitting any carbon at all – but

whatever is emitted must be captured and stored.

Practically,

this means that “flying, driving, heating our homes, using our appliances, basically

everything we do, would need to be zero carbon”, writes climate change expert Kevin

Anderson.

This goal is

achievable. We already have the technology to generate all our electricity via

renewable energy. Particularly in technologically advanced countries, it should

be perfectly possible to completely phase out fossil fuel-based power plants

within a few years; it simply requires investment in the surrounding

infrastructure, along with the political will to stand up to fossil fuel

capitalism.

We can also

massively cut down on waste and inefficiency. Energy efficiency – making our

economy less energy-intensive – is “widely considered to be the most important

single option for carbon reduction”, in the words of Neil Hirst, former

Director of the International Energy Agency (The Energy

Conundrum). David Wallace-Wells notes that around half of British

greenhouse gas emissions come from inefficiencies in construction, discarded

and unused food, electronics, and clothing. Retrofitting homes for heating

efficiency, for example, would make a significant contribution to reducing

emissions in relatively cold countries like Britain. According to Mike

Davis, “heating and cooling the urban built environment alone

is responsible for an estimated 35 to 45 percent of current carbon emissions.”

Transport is

another key area for reducing – and ultimately eliminating – carbon dioxide

emissions. There’s tremendous potential for fully-electric public transport

systems, along with electric car pools, electric bicycles, and urban designs

that encourage cycling. Again, this requires major investment, along with

rigorously-enforced laws to stop the climate criminals. In the words of Gus

Speth, former Dean of the Yale School of Forestry and Environmental Studies, “a

reliably green company is one that is required to be green by law.” (Cited in

Naomi Klein’s This Changes Everything:

Capitalism vs. The Climate) Meanwhile, until we find a way to power

aeroplanes without burning fossil fuels (the technology isn’t far off), we’ll

need to reduce air travel significantly.

We also need

to change our diets. We don’t all have to become vegan, but meat consumption

will need to be reduced in wealthy countries. Mike Berners-Lee writes that “the

single most important change will be an amazingly simple dietary shift towards

less meat and dairy consumption, with a particular focus on reducing beef. This

will markedly reduce greenhouse gases, improve the nutritional output of our

land and, by relieving land pressure, ought to be pivotal in stemming

deforestation.” (There Is No

Planet B: A Handbook for the Make or Break Years)

However,

it’s important to note that individual acts of good planetary citizenship are

not going to solve the problems we’re facing. As Wallace-Wells observes, “we

frequently choose to obsess over personal consumption, in part because it is

within our control and in part as a very contemporary form of virtue

signalling. But ultimately those choices are, in almost all cases, trivial

contributors, ones that blind us to the more important forces.” Without

concerted action at a national and international level, without large-scale

decarbonisation, we will not avoid catastrophic climate change. As such, the

problem is a political one.

Responsibilities

of the rich countries

At a global

level, China

leads the way in tackling climate breakdown, in terms of

investing in renewables and electric vehicles, driving the costs of green

energy down via massive state-led investment, carrying out vast afforestation

projects, and rolling out fully-electric buses and trains. However, China is

still a developing country, with over 1.3 billion people, many millions of whom

are likely to increase their energy consumption in the near future, since they

are still at a stage of development where increased energy consumption

correlates directly with improved quality of life outcomes. China can’t save

the planet on its own, nor can it be expected to. In terms of “common

but differentiated responsibilities”, the

technologically-developed wealthy countries of the OECD have the greatest

responsibility when it comes to averting catastrophic climate change.

The rich

countries fuelled their own industrial revolutions with coal and oil, resources

which they came to dominate in no small measure through colonial conquest and

imperialist manoeuvring. The US and Europe – with around 15 percent of the

global population – have contributed to over half the cumulative carbon dioxide

emissions since 1850. And the horrific irony is that these countries are the

least affected by climate change. Catastrophic climate events will hit – are

hitting – the poorer regions of the planet first.

As such,

countries like Britain have a clear moral responsibility to take the lead in

addressing climate change. To this day, it’s the wealthy that are living

wasteful lives, contributing to the ever-worsening situation. According to Ann

Pettifor, “just 10 percent of the global population are responsible for around

50 percent of total emissions. Per capita carbon dioxide emissions in Africa

are less than 10 percent of those in Western Europe and North America. Tackling

the consumption and aviation habits of just 10 percent of the global population

should help drive down 50 percent of total emissions in a very short time.” (The Case for the Green New Deal)

Furthermore,

it’s precisely the rich countries that have the resources to lead the way on

climate action. As has been pointed out before, “we

bailed out the banks, so now we can bail out the planet.” In

countries where large numbers of people don’t have access to modern energy, it

is understandable and correct that people want to provide that access with a

minimum of delay and cost. Sometimes that may even mean new coal capacity in

countries like Pakistan, where coal is by far the cheapest and most accessible

fuel (although the west should be offering the material support necessary to

allow such countries to meet their energy needs in a way that doesn’t damage

the environment). In OECD countries on the other hand, there is absolutely no excuse

for pursuing anything other than a rigorous and thoroughgoing energy

restructuring based on renewable sources.

How are we

doing so far?

The United

Nations Framework Convention on Climate Change was adopted in 1992, committing

the 154 signatory nations to “preventing dangerous anthropogenic interference

with Earth’s climate system”. The sad fact is that, in the intervening 27

years, “the sum of all the world’s climate action has so far made little or

perhaps even zero detectable impact on rising global emissions.” (Mike

Berners-Lee)

We are

nowhere near on track to meet the targets discussed above, for the simple

reason that we’ve left it to the capitalist market to provide solutions to the

planet’s problems. The domination of neoliberal economics over the last few

decades has reduced governments’ ability to set economic policy in the national

interest. Fiscal revenue isn’t sufficient to finance large-scale green

development, and shareholder-driven capitalism is incapable of long-term

strategic planning on the level that’s needed. Meanwhile, the big fossil fuel

companies have an extraordinary level of entrenched power that they’ve used

systematically to slow down the energy transition.

There isn’t

even any meaningful agreement among the western ruling classes as to how to

respond to climate change. Although there is a relatively more forward-thinking

section that understands that they too would be affected by climate breakdown

(in much the same way that sections of the English bourgeoisie became

interested in public health when they realised that they too could fall victim

to cholera), there are also the neoliberal extremists who are happy enough with

the idea of moving to Finland or New Zealand and setting themselves up in gated

communities.

In summary,

neoliberal capitalism has shown itself to be utterly incapable of averting

environmental catastrophe. Even in Britain, where there has been some focus on

wind power, this has been far too slow. Today, wind contributes 17 percent of

electricity generation in Britain (well behind gas, at 40 percent). The

economist Mariana Mazzucato, arguing for concerted state-led investment in

green development, complains that the strategies thus far employed in the US

and Britain “lack a clear direction and fail to offer long-term incentives,

resulting in a start–stop approach to green initiatives that produces dubious

outcomes at best.” (The

Entrepreneurial State)

The Green

New Deal

The Green

New Deal (GND), conceived a decade ago by British economists and

environmentalists but recently popularised by progressive US congresswoman

Alexandria Ocasio-Cortez, provides the first viable, comprehensive and

actionable plan for developed countries to decarbonise their economies whilst

creating jobs, tackling inequality and promoting equality and social justice.

Measures include investment in renewable energy and zero-carbon public

transport; upgrading buildings for energy efficiency; building ‘smart’

distributed power grids to provide affordable clean electricity to all;

reorganising the food system; ending subsidies to the fossil fuel industry; and

prioritising basic needs.

The key to

implementing a programme such as the Green New Deal (or as it’s often referred

to by Labour politicians, the Green Industrial Revolution) is public investment

on a grand scale. As Berners-Lee points out when discussing the future of

renewable energy, “the solutions we need to the problem of intermittency and

storage are all coming along nicely; the critical factor is investment.”

This is

precisely what has been agreed by Labour’s recent conference, and what is being

put

on the table by shadow chancellor John McDonnell: a programme

of government investment “mobilising £250 billion of capital spending on the

projects needed to decarbonise Britain to avert irreversible climate change.”

Supported by

a National Investment Bank and network of regional development banks, the

programme will seek to ensure that “the transition to sustainability is one

that benefits everyone across our society.”

Starting

with the infrastructure for widely deploying clean energy, along with a plan

for retrofitting homes to be energy-efficient, the Green New Deal would create

hundreds of thousands of skilled jobs. The

plan includes nationalising the major UK-based energy

companies, replacing all gas boilers, closing fossil fuel-based power stations,

investing in and subsidising electric cars, vastly expanding off-shore wind

capacity, and decarbonising the public transport system.

On top of

the Green New Deal, it’s worth mentioning that Labour has also committed to making

green technologies available cheap or free to the countries

of the Global South. Plus of course the present Labour leadership is deeply

opposed to war, which has a major

environmental cost on top of its more obvious human cost.

If Labour

wins the General Election on 12 December and a Jeremy Corbyn-led government can

implement its version of the Green New Deal, it will be a huge boost for the

global battle to save the planet. Britain will blaze a trail for the rest of

the OECD to follow, towards a global Green New Deal that is, in Ann Pettifor’s

words, “a global banner behind which millions can assemble with one voice in

order to address the gravest crisis humanity has ever faced.”

If, on the

other hand, Labour loses the General Election and Britain has to endure another

five years of hard-right Tory government, the result for the fight against

climate breakdown would likely be disastrous. Boris Johnson’s ‘hard Brexit’

vision involves leaving the EU customs union and negotiating a free trade deal

with the US. That will mean a wide-ranging political alignment that could well see

Britain leaving the Paris Climate Agreement. With both Britain and the US

outside the Paris Agreement, the prospects for international cooperation to

combat climate change would look increasingly grim.

The planet

needs a left Labour government in Britain.

This is a slightly amended version of an article which originally

appeared in the Morning

Star.

The election plans laid out by the two major parties mean

that it is crystal clear only Labour has policies to address the current crises

(the LibDems can be disregarded in policy terms, as they only have one policy,

which they claim is ‘stop Brexit’ but which is actually ‘stop Corbyn’). There are combined crises of the climate

catastrophe as well as the stagnation of the economy and living standards.

The depth of the British economic crisis is not at all

widely understood. It should be as only

a proper appreciation of the scale of the problem can lead to the appropriate

measures to tackle it, the policies that are necessary and the political

choices that follow.

The scale of the economic crisis is illustrated in the chart

below. Fig.1 shows the growth rate for the capital stock, the total value of