The ‘Golden Age’ and the Public Sector Deficit

John McDonnell’s fiscal policy framework continues to come under fire from both left and right. The framework broadly states that the Government should borrow for investment (the capital account) and that over the business cycle Government day-to-day spending (the Government’s current account) should be in balance.

The attacks from the right are largely disingenuous. They argue that the McDonnell framework is little different from that of Ed Balls, a cloak for austerity-lite. The Balls approach also included a commitment to match Tory spending plans in the first two years. These would have been the deepest cuts to public spending in history and were so draconian that the Tories themselves abandoned them in office after May 2015. Balls supplemented this with a ‘zero-based spending review’, that is a commitment to have no commitments, not even to pensions, to social welfare for disabled people, or to the NHS.

The contrast with John McDonnell is a sharp one. He has consistently opposed austerity. Crucially, McDonnell he has committed to the establishment of a National Investment Bank to address the acute investment shortage of the UK economy. He has also committed to borrowing £500 billion for investment to tackle the crisis. The McDonnell framework is not different to Balls because it can be suspended. Its content and its effects would be entirely different.

‘Keynesian’ misunderstanding

Unfortunately, because of a deep misunderstanding of economics, economic history and public finances, many progressive or ‘keynesian’ economists echo these same rightist criticisms. As this is primarily misunderstanding not malevolence, it is worth addressing once again.

From a theoretical perspective the misunderstanding arises because of the widespread view that Consumption can lead growth. Therefore, it is argued, the Government should increase its own Consumption in order to foster recovery. The premise is false.

Consumption cannot lead growth because it is not an input to it. Consumption is a consequence of production, and growing Consumption is a consequence of growing production. If production has not risen increased Consumption requires borrowing, which is a financial claim on future production. Furthermore, if an increasing proportion of output is devoted to Consumption rather than Investment the growth rate of the entire economy will slow, and so too will Consumption.

Yet ‘keynesians’ and other progressives who wish to end austerity persist in arguing for Government to increase Consumption by borrowing on its own account- hence the attacks on McDonnell. This is also flies in the face of economic history.

History

It is widely recognised the economic growth rate of the UK and of many of the Western economies was greater in the post-World War II period, from 1945 to the early 1970s than in the subsequent period. This recognition includes ‘keynesians’ and many others, some describing it as the ‘Golden Age’.

This itself is a misreading as the far higher growth rate in the US and to a lesser extent the UK was in the pre-war and war period itself. The exceptionally strong growth was caused by the state taking control of investment and directing very large increases, in order to wage war. The subsequent ‘Golden Age’ was the gradual deceleration of this war boom.

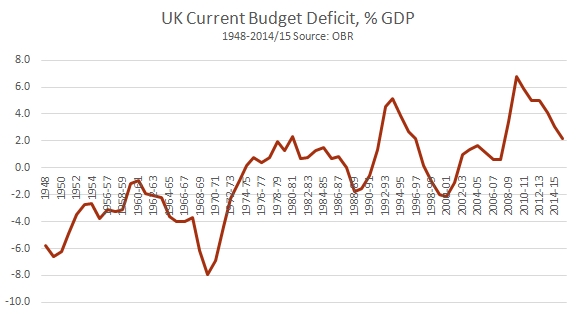

Even so, the recognition that growth in the post-War period was markedly stronger than the period beginning in the early 1970s is shared. It is factually correct. Yet this ‘Golden Age’ does not at all conform to the ‘keynesian’ prescription for permanent public sector deficits on the current Budget. In fact it shows the opposite.

In Fig.1 below the UK Current Budget Deficit is shown as a proportion of GDP. A level above zero shows a deficit. Below zero shows a surplus. For the entire period of the ‘Golden Age’ the UK Current Budget was not just balanced, it was in surplus.

This post-WWII period of large current Budget surpluses coincided with the establishment of the NHS, the creation of the ‘welfare state’, a massive public sector house building programme, large scale nationalisations and other measures.

How is this possible? How can there both be (sometimes huge) surpluses on the current Budget while Government current spending was initiating a whole series of new or improved public goods?

The answer is investment, public investment. Fig.2 below shows the level of Public Sector Net Investment as a proportion of GDP over the same period.

This explains why both rightist and leftist criticisms are misplaced. The McDonnell framework will not lead to austerity if investment is increased. More importantly, it offers a way out of the crisis. If investment is sufficiently strong the economic recovery will provide sufficient tax revenues and lower social security outlays to become self-sustaining. This improvement in government finances can be used for more investment and for increased current spending.

On the other hand, if it should be the case that recovery remains weak and therefore the current budget remains in deficit, then the answer would not be to cut current spending, but to increase public sector investment.

The period of the greatest advances in public sector current spending took place when there were surpluses on this current account, only made possible by relatively high levels of public investment, in British terms at least. Current spending has been in crisis ever since 1974, with Denis Healey’s fake IMF crisis, then Thatcher and her successors, who slashed public investment.

Mainstream economics largely tries to bury economic history. Those genuinely seeking an alternative to austerity should not make the same mistake.

Recent Comments