By Tom O’Leary

The latest surveys from the Purchasing Mangers’ Institute (PMI) show the British economy slowing sharply.

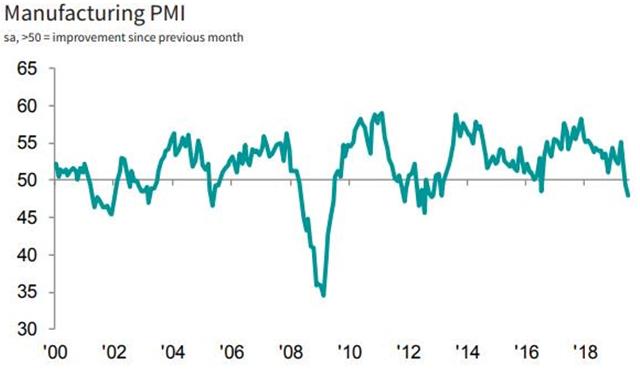

The manufacturing PMI in June fell to 48.0 (from 49.4), the lowest level since February 2013, shown in Chart 1 below. According to the survey providers IHS Markit, this survey reading is consistent with a contraction in output of 4% from a year ago.

Chart 1. UK Manufacturing PMI Survey, April 2019

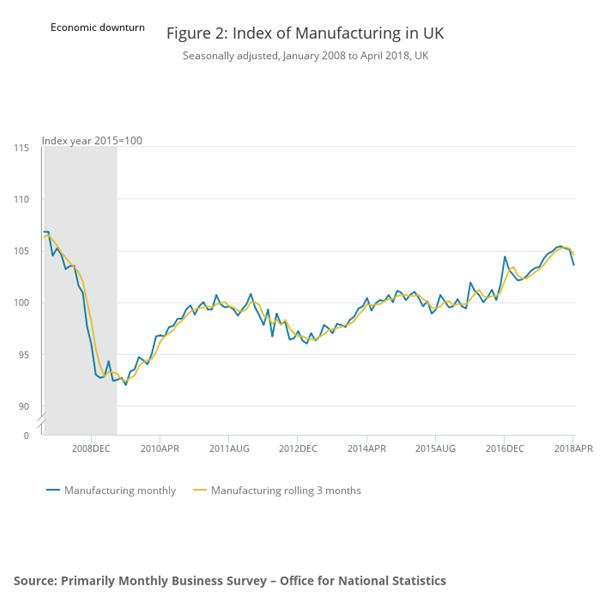

This latest downturn in output represents an acceleration of the long-term decline of both manufacturing and industrial production (which includes energy and water supplies). The current reading for the index level of industrial production was 101.4. This is less than 1% higher than when the Tory/LibDem coalition took office in May 2010 and is now 9% lower than the pre-recession peak in May 2007. At the same time, the manufacturing index is now 102 and has recovered by 5.9% since May 2010, but is still 3.6% below its pre-recession peak while the survey evidence from the PMI shows it is heading lower. These medium-term trends are shown in Chart 2 below.

Chart 2. UK Industrial production and Manufacturing Indices, January 2008 to April 2018.

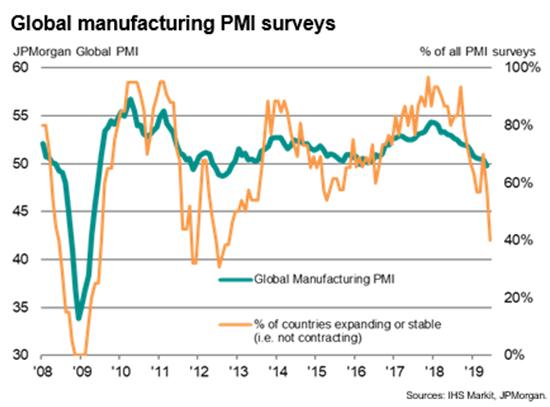

The global context is a negative one. The global manufacturing PMI dived in June to 49.4, the lowest level for 6 years (Chart 3). Key regional hubs for international production and trade such as South Korea have been badly hit, and the worst-affected country in the June survey was Germany, one of the largest economies most connected to global production chains. Slowing world trade and trade tariffs imposed the US are clearly having a widespread negative impact, with export orders the weakest component of all in the survey.

Chart 3. Global manufacturing PMI June 2019

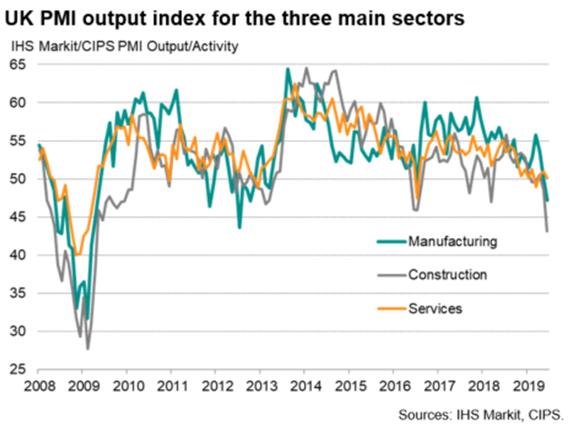

But the entire British economy is struggling, not just manufacturing. The June construction PMI plummeted to 43.1 (from 48.6 in May) and the services sector PMI and the services sector PMI slid to 50.2 (from 51), close to stagnation. All three PMI indices are shown in Chart 4 below.

Chart 4. PMIs for manufacturing, services and construction, June

Construction is the least internationalised of the three sectors, and the least susceptible to changes in international conditions as a result. It is clearly leading the way in the downturn in the British economy. This is a domestic crisis, within a global slowdown.

Clearly, the domestic aspect is Brexit-related. All three sectors within construction fell, house-building, commercial construction (shops, factories and so on) and civil engineering (public and private infrastructure construction), suggesting the unwillingness to invest is broad-based.

The rising risk of a No Deal outcome will only put further downward pressure on the economy. Expectations of the next move in official interest rates have done a U-turn as a result, with markets now priced in line with future rate cuts. The National Institute assumes that GDP will have grown by just 0.2% in the 3 months to June.

Perhaps the most startling financial market indicator of the crisis is the fact that the UK government bonds linked to inflation (‘index-linked gilts’) are all offering interest rates lower than minus 2%. This means that the UK government can borrow at negative real interest rates, once CPI inflation is taken into account, for anything between 3 years and 18 years.

But with the two Tory rivals speaking only about tax cuts for businesses and the rich, only a Labour government would be willing to take advantage of this opportunity to increase borrowing for investment.

Recent Comments