The Tories have no real plan to get out of the current

economic crisis, but they are determined that the working class will foot the

bill. In that way, their hope is that

the end result of this economic slump will be much lower wages across the board

and that profits for the remaining companies will significantly increase as a

result.

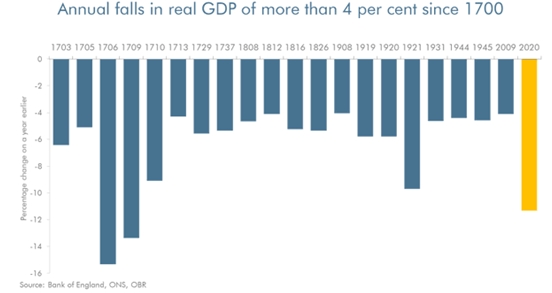

The UK has one of the worst per capita death tolls in the

world. With an OBR forecast of a

contraction in GDP of 11.3% it also has an economic slump of the same

magnitude. The OBR reckons it is the worst for over 300 years.

Chart 1. OBR: The Worst Slump since the Great Frost of 1709

This slump is treated by ministers and commentators alike as

if it is an act of God, rather than a consequence of government failure. However, its alleged effects fall into a

different ‘something must be done’ category.

In particular, the propaganda campaign on the deficit in government

finances has begun, in a farcical re-run of the drive to austerity from 2009

onwards that led to austerity, the BBC’s chief political correspondent Laura

Kuenssberg plays an especially prominent, pernicious role with bulletins filled

with talk of “we

can’t afford” to support jobs and families during and after the pandemic,

that there is “no money left”, that we’ve “maxed out the

nation’s credit card”, that we’re “loading debt onto our

children”. Even mainstream economists such as Jonathan Portes describe

this all as ‘economically illiterate nonsense’.

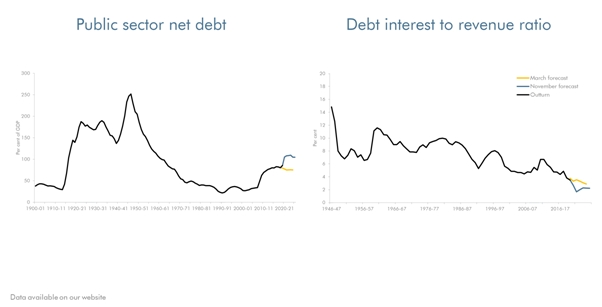

As

Chart 2 shows, public debt is rising but it is far from unprecedentedly

high. Crucially debt interest as a

proportion of GDP is close to its all-time lows because global interest rates

remain so low. The debt is currently

easily affordable, because interest payments are so low.

Chart

2: OBR: Debt and debt interest payments as a proportion of GDP

The scaremongering about the debt and deficit levels serve

another purpose altogether. This is the attempt to justify the freeze in public

sector wages, which is a cut in real terms (after inflation). This is the one big ‘saving’ announced in the

Spending Review, along with further big cuts in spending on public services in

later years.

Yet it is not a big saving at all. Unusually, the Chancellor did not provide a

specific estimate of the ‘saving’ in his review of Policy Costings. But an approximate estimate (current author’s

calculation) is an annual saving of £3billion to £4billion.

This is a pitifully small amount relative to government

finances in aggregate. The total forecast deficit for this year is £394

billion, so the entire cut to public sector wages falls with the scope of

accounting errors. The Chancellor

boasted that £280 billion had already been spent, largely on supporting

businesses. And it should not be

forgotten that the public sector workers’ wages have already been earmarked as

a contribution towards a £26.4 billion increase in military spending.

As SEB has argued previously the purpose of the

public sector pay freeze (a real terms cut) is not to reduce the deficit. With these magnitudes it would take over 100

years, even assuming there were no indirect negative economic consequences

arising from it. The real purpose of the

public sector pay freeze to attempt to set a ceiling on all pay after the

crisis is over, and thereby lower all wages in real terms.

This was its purpose in the austerity offensive from 2010

onwards. This had the desired effect of

lowering real wages for a period, but the electoral timetable combined with

very low unemployment meant that holding down wages could not be

maintained. The current plan is to solve

that problem of wages creeping higher while there is low or zero productivity

growth, and which prevents the growth of profits. This is the return to mass unemployment.

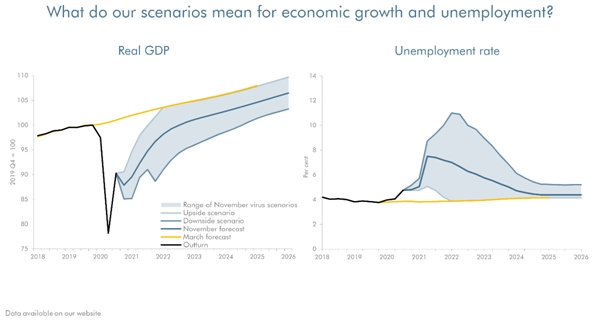

The OBR’s central forecast is that 2.6 million people will

be made unemployed and that the unemployment rate will rise to 7.5%. Its worst-case scenario is that the

unemployment rate rises to 11%, or almost 4 million people. This is getting into Thatcher territory.

Chart 3. OBR: Forecasts for fall in GDP, rise in

unemployment

In this way, this government will hope to combine the

Thatcherite effort to lift profits by deindustrialisation, with the cuts to

real pay under the Tory-led Coalition. Of

course, neither of these strategies worked even in their own terms, as profits

did not rise sufficiently to restore UK competitiveness or spark an investment

boom.

Yet the current Tory strategists will be hoping that by combining

this worst of both worlds, cutting real pay and mass unemployment, they can

achieve something their predecessors could not. They aim to get wages down and keep them

there. We shall see if this toxic mixture has the desired effect. But millions of people will face misery,

increased poverty and unemployment if their plan is put into action.

The experience of this country (both positive and negative)

and many others shows that there should be a compete lockdown to combat the

pandemic. This means all non-essential work stopped, all leisure and other

services halted, schools closed and all possible higher education moved

online. There should also be proper

compensation for workers, who should receive 100% of their pay, not the 80%

currently (or none at all for some freelance and other workers). That

compensation should be for the duration of the furlough itself, at first approximately

8 weeks and until new cases reach levels where they can be suppressed, and then

extended for the necessary period while the gradual back to work process is

completed.

A combined crisis

The public health crisis caused by the Covid-19 pandemic has

led in turn to an economic crisis. There

is no possibility of ‘saving the economy’ while a pandemic is raging. Services account for approximately 70% of the

economy and the demand for many of these is discretionary. You cannot force people to go to pubs,

cinemas or restaurants in a pandemic. On

the experience of this country and many others, the majority of people will

simply refuse to take up their normal leisure and cultural activities. It is not the restrictions that are killing

these businesses and workers’ jobs. It

is the pandemic itself.

Similarly, there is no ‘trade-off’ between combatting the

virus and protecting the economy, as ministers and others frequently

claim. The UK’s own disastrous record on

both demonstrates that. The UK has one

of the worst death tolls per capita of any large country in the world, and the

worst total in Europe despite both waves of the virus hitting this country

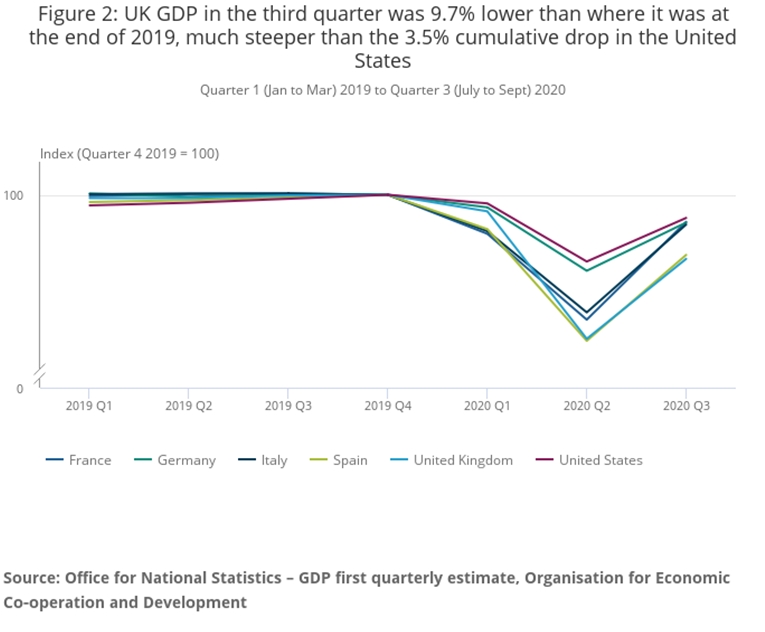

later than continental Europe. It has also the worst economic performance any

major Western economy (see Chart 1 below).

Chart 1. UK GDP, Largest Contraction Among the Major Western

Economies

By contrast, it is clear that all the countries that have

effectively eliminated the virus are also the economies that will grow the

strongest this year, as shown in Table 1 below.

Table 1. IMF Real GDP

Growth Forecasts for 2020

Country/Region

Real GDP Forecast, %

China

+1.9

Viet Nam

+1.6

USA

-4.3

EU

-7.6

UK

-9.8

Source: IMF World Economic Outlook

At the same time there is a public health imperative to

combining full lockdown with full pay for all furloughed workers. Many workers are already in poverty even at

100% of their usual pay. Excluding

pensions, most

benefit claimants are people in work and 56% of those in poverty before the

pandemic were in work. Put simply,

millions of a were already poor when being paid at 100% of their wages. Reducing it to 80% increases the probability

of outright destitution for millions.

The pay cut also compels many to ignore lockdown

restrictions, even when they know they are putting themselves and their loved

ones at risk. 80% of breadline wages is

insupportable. People are then forced to seek additional work, in breach of the

requirement to close all non-essential workplaces. It is morally unjustifiable to cut those wages,

including those on the National Minimum Wage, as this government is doing. It is in the interests of the whole of

society that people are able and do adhere to strict lockdown measures.

‘There is no money

left’

The main objection to 100% pay for all furloughed workers is

cost. But the additional outlay for full

pay is tiny in comparison to other levels of expenditure, including a £300

billion bank loan guarantee scheme and the

initial £110 billion support for businesses (via the Job Retention Scheme,

the bounce back loan scheme, the business rates holiday and other measures).

The estimated cost of the initial furlough scheme which ran

from March

to the beginning of October was £40 billion. Using simple maths, the total cost of a scheme

offering 100% of wages is only marginally more at £50 billion. Of course, the government cap can continue to

apply at £2,500 pay per month.

The National Institute for Economic and Social Research

(NIESR) estimates

that the scheme is self-funding.

This is because over the long-term it helps to preserve jobs and all the

tax revenues that they generate. Furlough payments are like an insurance

policy, helping to ensure the continuation of that future tax revenue stream

dependent on jobs.

But the furlough scheme, and increasing it to 100% of pay,

is also largely self-financing even in the short-term. Over the period of the first half of the

Financial Year (FY), which approximately coincides with the bulk of the initial

furlough scheme from April to the end of September, government revenues

declined by £42.6 billion. As the

biggest contributors to tax revenues are from personal income taxes and

indirect taxes on personal consumption, it is clear that government revenues

are lowered by reduced employment and reduced pay. So, in the first 6 months of this FY, taking

just VAT, income tax and social security together, government revenues fell by

£23 billion compared to the first half of the last FY. The shortfall would be even greater adjusted

for inflation.

The increase to 100% furlough pay is easily affordable.

It would also be an important part of a genuine lockdown,

which could break the back of the virus as has been done elsewhere (and which

was almost done here until lockdown was ended too early in June).

There may be a more valid objection about fairness,

especially for essential workers who would continue at work even during a

properly effective lockdown. But that should

be dealt with in other ways, such as large bonuses and substantial

above-inflation pay rises when the pandemic is finally ended.

The labour movement should argue for 100% of pay in a

complete lockdown. Full lockdown and

full pay now!

Recently the Chancellor Rishi Sunak won widespread plaudits for

altering the terms of his financial support for workers whose jobs are under

threat because of the restrictions introduced in response to the pandemic. The furlough scheme is back, leaving the

workers affected with just 80% of their wages, rather than 67%.

This was simply a tactical retreat. The government has clearly signalled it is

conducting a ferocious attack on living standards but has had to recalibrate

what it can impose right now.

It should be clear that the scale of this attack on the living

standards of the working class and poor, is much more ruthless than the

austerity of 2010 or in some respects even than Thatcher in the 1980s. As a result, it should be equally clear that

success for the government would be a decisive shift in favour of big business

and the rich, at the expense of workers and the poor.

Since class warfare is being waged, anyone who preaches social

peace now is simply making it harder for the working class and its allies to defend

themselves against a major defeat.

Ratcheting

down, not levelling up

The claims that the Boris Johnson government is engaged in ‘levelling

up’ poorer areas of the country belong with the falsehoods that he is

‘implementing Corbyn’s policies’, is ‘spending like a socialist’, has

‘abandoned austerity’. They are all pure

hokum. They are proposed by those wishing to blunt any opposition to the

government, and repeated by those who clearly do not understand what is going

on around them.

All these claims fall apart as soon as the government meets any

resistance, as the excellent campaign for free school meals by Marcus Rashford

and others shows. Donating £12 billion

to SERCO, Deloitte’s and other private sector companies, most of whom are

intimately connected to the Tory Party, while they for long refused £120

million for free school meals is not levelling up, implementing Corbyn’s

policies or socialist spending or any other of the spurious claims.

Austerity is properly understood as a transfer of incomes and

wealth from poor to rich, from labour to capital. So, in the very first

austerity Budget by Osborne and Cameron there were £12 billion in cuts to

social security while business taxes were cut by almost exactly the same

amount. Clearly, even in simple

accounting terms (leaving aside any economic effects) this had nothing to do

with reducing the deficit, as was claimed.

But it did transfer government spending from the poor to the rich.

Austerity has continued in the same vein, with varying intensity ever since. Previously,

Thatcherism used the cloak of monetarism in order to effect exactly the same

type of transfer, largely through an assault on the unions and tax breaks for

the rich.

In the same fashion, the overwhelming bulk of every package

announced in the current crisis is to benefit big business. So, of the initial £330 billion emergency

package that was finally announced after the March Budget, £300 billion was in

the form of loan guarantees to the banks to avoid losses on their business

lending. In contrast, just £1.6 billion is for local

authorities who are under enormous pressure both from reduced revenues and much

higher outlays to meet the mounting effects of the crisis caused by the

pandemic.

The attack

on the working class

The centrepiece of the class warfare being waged by big business

and their government is on wages, hours and employment. Here, the ratchet down effect is the most

wide-ranging in its effects.

This is easy to demonstrate.

Before the crisis began, however low wages were for workers across many sectors,

they did at least receive 100% of those wages.

Under furlough conditions, where work was supposed to be suspended, this

has been reduced to 80%. At the same

time, and completely against the rules, many companies committed fraud by

forcing staff into work for no additional pay. Up to a third of all employees

were asked or forced to come in, according

to one estimate.

In addition, a large number of firms are in the process of making

that reduction permanent. Three high

profile employers, British Gas, British Airways and the BBC have all launched

fire and rehire schemes to reduce wages and conditions. Many others are following suit but are less

well known. As the end of the previous furlough

scheme approached, the government tried to enforce a reduction to 67% of wages

for some topped up by 5% from employers, and no support at all for those caught

in the spurious ‘Tier 2’ restrictions.

The fear over the probable immediate collapse in jobs forced a tactical

retreat.

Now that furlough is back, there has been a return to 80%, at

least for the time being. But even if this is the full extent of the reduction,

it still represents an enormous and dramatic shift from labour to capital. Nothing on this scale was achieved under

austerity.

The intention of the ruling class and the Tory government is as

far as possible to make this reduction permanent.

Mainstream economists have long studied the issue of the

determinants of wages for obvious reasons.

There is a whole literature devoted to what they describe as the problem

of rigidities that lead to ‘sticky’ wages, that is the difficulty in driving

down nominal wages (here is just one example pdf, there

are innumerable others).

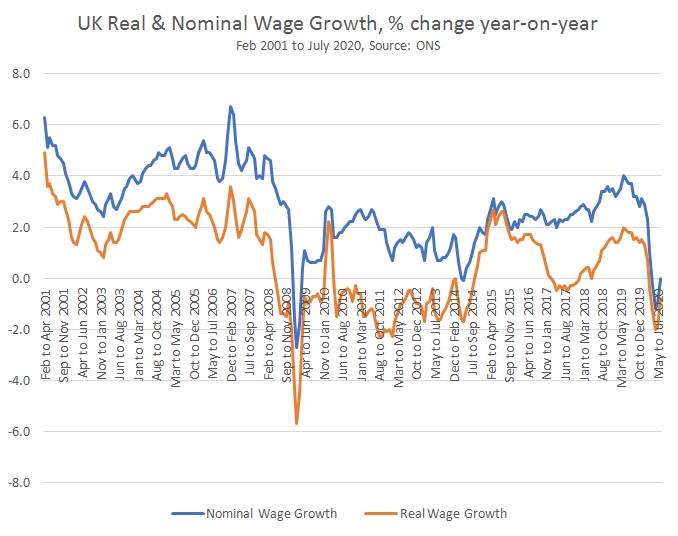

This ‘stickiness’ of wage growth is shown in Chart 1 below. The annual growth in wages in nominal terms

is shown in orange, the growth in wage in real terms (after adjusting for

inflation) is shown in blue. Nominal

wage growth hardly fell at all in the last recession. The brief dip in wages occurred in the first

few months of 2009 and began to recover very slowly in later months. It was only the simultaneous fall in the

value of the pound, which drove up prices in an economic slump, which caused

real wages to fall over a more prolonged period, from mid-2008 to the end of

2009. But even wages in these terms

began to recover in early 2010.

Real wages for public and private sector workers fell after the

June 2010 ‘emergency Budget’ all the way through to October 2014. This was a result of government policy. Only as the Coalition government geared up

for an election the following year by loosening government spending did real

wages start to crawl higher. The

austerity policy was highly successful in cutting real wages, as it was

designed to do.

Chart 1. UK Nominal and Real Wage Growth, % change

If everything else is unaltered, the combination of economic

weakness, rising import prices and rising real wages from 2010 onwards was

bound to damage profits severely. The centrepiece of the austerity policy was

to combat this profits-damaging combination of factors.

The chosen method was a public sector pay freeze. Not only did this have the direct impact of

cutting real wages (as well as cuts to pensions) for approximately 1 in 6 UK

workers (over 5 million of them) in the public sector where union densities are

highest, but it also had a ‘demonstration effect’ (pdf), of

setting a nominal wage freeze or similar in the private sector as well. With

prices still rising because of the effects of the weakness of the currency,

real wages for workers started to fall once more.

However, as appealing as it may be to employers to cut wages if

they can, this does not by itself resolve the issue of profitability especially

if the overall business conditions are characterised by sluggish growth and

rising import prices. The austerity policy of driving down wages was only

successful in raising the level of misery. It was not successful in its overall

aim of raising profits.

Worse, from the perspective of the architects and supporters of

austerity, nominal wage growth continued to rise at a very modest pace after

2014 and continued to rise until the current pandemic began. Real wage growth was more erratic, undercut

by rising inflation once more in 2017.

But even so, no blow had been struck which cut wages sufficiently to

raise profits on an enduring basis.

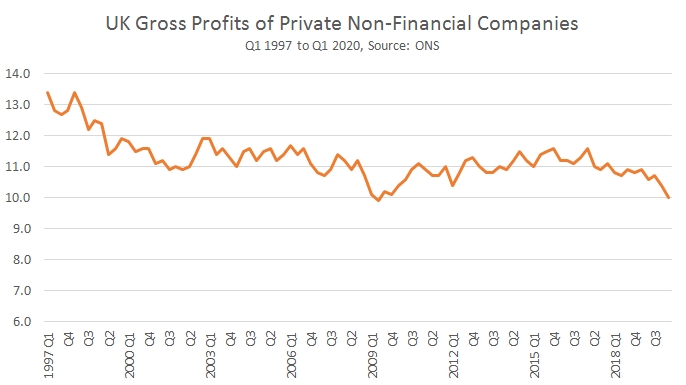

This trend in profits is shown in chart 2 below. Initially, profits fell as they tend to

during a recession. Sales were falling

and as noted above wages remain ‘sticky’.

(The ONS data shown is actually a measure of the rate of return on

capital, not strictly profits, but it is a useful guide to profitability). Subsequently profitability did recover but

only moderately.

Yet profitability continues to remain below 2008 levels. And, as

regular readers of SEB will know, profitability never rose sufficiently

to spark an upturn in private sector investment. From the perspective of the

capitalist class as a whole, there is no incentive to raise investment, which

means adding to the productive capacity of the economy, if the rate of return

on existing investments is depressed below usual levels.

Chart 2.

The

reserve army of labour

In the last recession and under the austerity policy real wages

fell initially by 6% and only recovered over a very prolonged period. Under

Thatcher, real earnings for those in work did not fall at all. Instead, her policy addressed the problem of

low profitability by massive deindustrialisation that created 3 million

unemployed.

The current policy is a combination of these two. Through government policy wages are being

slashed by 20% for very large parts of the workforce, even including those on

the National Minimum Wage. At the same

time there is a sharp rise in the level of unemployment, and some businesses

will fold. The combination of these two factors,

the sharp reduction of wages and the surge in unemployment is government

policy. It is a new development and its

architects will be hoping that one reinforces the other, that much higher

unemployment will be a decisive factor in keeping wages low long after the

public health crisis is over.

This mechanism was first analysed by Marx as the creation of the

‘industrial reserve army’ of labour. Marx says the reserve army of the

unemployed exists in no previous form of society except in capitalism, and is

integral to it.

“The industrial reserve

army, during the periods of stagnation and average prosperity, weighs down the

active labour-army; during the periods of over-production and paroxysm, it

holds its pretensions in check. Relative surplus population is therefore the

pivot upon which the law of demand and supply of labour works. It confines the

field of action of this law within the limits absolutely convenient to the

activity of exploitation and to the domination of capital.” – Karl Marx, Capital, Volume One, Chapter 25

In general, high or sharply rising

unemployment holds the risk that it may produce social unrest and political

discontent. The government of an

advanced industrialised country may choose to engineer a sharp rise in

unemployment in an attempt to restore profitability, or it may choose to try to

cut wages. But both stratagems entail

high risk. Combining the two is

exceptionally high risk. Only in a

period of desperation and generalised crisis would they be attempted or could

they be potentially successful.

Under the cloak of the public health

crisis which their own policies have helped to create, the current government

is attempting such a strategy. Naturally it is in the interests of all workers,

all the oppressed and vast majority of society that they are not successful.

In the West the population is at present sheltering to

protect itself from Covid, entering the greatest economic downturn since the

Great Depression, and facing the threat of unemployment and reduced living

standards. On the other side of the world in China, something going in exactly

the opposite direction is occurring. China unveiled its new Five-Year Plan.

This will take a country which in 1949 was almost the poorest in the world, and

its almost 1.4 billion population, into the ranks of high-income economies by

international classification – with all the steps forward in life expectancy, living

standards, health, education and social conditions this brings with it.

There has never been such a large scale economic and social ‘miracle’

in the entire history of humanity – the population of China is larger than the combined

population of all other high-income economies in the world.

This transformation therefore poses the most profound possible

questions for socialists, socialist theory, and the international left. If, as

some on the left claim, China is a capitalist country then the only conclusion

that can be drawn from these facts is that capitalism remains a progressive

system. If capitalism can raise almost one fifth of humanity from nearly the world’s

most grinding poverty to high income status in 70 years, that is within a

single lifetime, it is nonsense to claim that capitalism has exhausted its

possibilities. If capitalism had delivered 850 million people from

internationally defined poverty, as China has, then capitalism would have

delivered gigantic progress for humanity. Capitalism would have delivered an

immense improvement, a qualitative step forward in life, for a higher

proportion of humanity than the European Union and the US combined.

Furthermore this capitalist system would also have been demonstrated

to be able to deliver similar results not only to China but to be a path that

could be followed by other major countries – for example Vietnam, a country of

almost 100 million people, is delivering economic growth and reduction of

poverty at a rate, if at an earlier stage of development, essentially the same

as China’s. If capitalism can deliver such benefits it is utopian not to

support capitalism.

But in that case, there is an impossible mystery. Why has

such unparalleled economic development and improvement in living conditions not

been delivered by the other countries following the capitalist system?

In summary, the ‘leftist’ claim China is a capitalist

country paradoxically, and doubtless against the subjective intentions of those

on the left who put it forward, leads to the conclusion that capitalism can

deliver historically unparalleled improvements in living standards!

There is in fact no such mystery because China, and Vietnam,

are not capitalist but socialist countries. That is why such progress has been

made. And this is why the left has a real model for economic development across

the world – something it is vital for the left to understand, most immediately

in developing countries. Socialism is not a utopia, it is not a dream, it is

not something which was achieved in 1917 in Russia and has never been achieved

since. It is something real, totally practical, and which delivers immediate

benefits to truly gigantic numbers of people.

The following article by John Ross, which appeared in

China.org.cn, on China’s new Five Year Plan analyses the historical facts which

have to explained by any analysis of China, the nature of its new plan, and the

step forward that this represents as the country enters the stage of

development of a high income economy.

* * *

The press conference which followed the Plenary Session of

the CPC’s Central Committee put forward guidelines not only for China’s next

Five-Year Plan, for 2021-2025, but also for more medium-term development of

China up to 2035. The two are interrelated because the next Five-Year Plan will

inaugurate a qualitatively new period in China’s economic development which is of

global significance. This goes beyond the fact that China’s short-term economic

prospects are better than for any other major country – the IMF estimates in

2020-2021 it will account for 60% of global growth. The new Five-Year Plan inaugurates

a fundamental transition.

China in 2020 became a ‘moderately prosperous’ economy by

its own national classification – also achieving its goal of the elimination of

absolute poverty. But most countries use World Bank classification in making international

comparisons – dividing economies into low, medium and high-income groups. By

this criterion in approximately 2022-23, the middle of the next Five-Year Plan,

China will enter the ranks of global ‘high income economies.’

Achieving this new level of development determines the

Five-Year Plan’s nature. Previously China planned for escaping underdevelopment,

whereas this plan centres on the different tasks of building a high-income

economy. Furthermore, due to US actions, it will do so in a different

international context and where serious challenges face humanity – particularly

the threat of climate change and of economic recovery from a pandemic which Western

failure to control has created the deepest global economic downturn since the

Great Depression.

To understand this Five-Year Plan’s place in China’s national

development, the almost incredible character of what has been achieved must be understood.

In 1949 China was almost the world’s poorest country – only 10 counties had

lower per capita GDPs. Only 73 years later, the span of a single lifetime,

China will count among the world’s high-income economies.

When the Communist Party of China took power in 1949 in

essence it put forward a promise to China’s people: ‘if China adopts our

methods the Chinese people will be taken from a century of humiliation, regain

control of their own destiny and rejuvenate their country.’ The achievement by

China of high-income international status during the next Five-Year plan is a key

symbol on the economic field that this promise was delivered – following

similar achievements in national unification, elimination of foreign military forces,

gigantic improvements in health, life expectancy, education, culture and

numerous other fields.

Internationally the scale of what is represented by the new

Five-Year Plan is clearly understood by historical comparison. Today, by World

Bank classification, only 16% of the world’s population lives in high income

economies. But China is 18% of the world’s population. China becoming a high-income

economy will therefore more than double the proportion of the world’s

population living in such states. It is a fact that no such comparable single improvement

in the position of such a large proportion of humanity has ever taken place in the

whole of history.

This staggering achievement brings new challenges. Some are

internal – a high income economy is far more complex than a low or medium one.

But some are external. The US has embarked on an attempt to block China’s development. This

path was launched by Trump with tariffs and technology bans. But there is no

indication that US policy will fundamentally change no matter who wins the US

presidential election.

This is what makes the much-discussed concept of a ‘dual

circulation’ economy so crucial in the new plan. Many US analysts consider

Trump made tactical errors in his attack on China. That the tariffs were a

mistake as they were paid by the US population and attacked China on terrain

where it was strong, and the US could not compete – good quality medium

technology manufacturing. Instead, it was argued, the US attack should be concentrated

on its strong point – high technology. The US should concentrate on weakening China’s

most high technology companies as with Huawei and Tiktok. Trump and Biden are therefore

urged to create a ‘technology blockade’ of China.

There are certainly doubts whether the US can achieve this goal

– it is against the interests of other countries and its own high technology

companies which previously had strong markets in China. But it would be a naïve,

unrealistic, strategy for China to base its policy on an assumption that US

policy will collapse due to its own contradictions. Therefore, to progress as a

high-income economy, China will have to increasingly rely on its own

technology. Every part of the production chain must be potential achievable in

China – best described as ‘domestic circulation’. This is different to the 1978-2016

period in which China could rely to a great extent on importing technology.

China remains committed to globalisation, which would be the

best path of development for the world, and uses every opportunity for

internationalisation, but in the new situation its domestic economy will

dominate.

Obviously, this requires great national effort – money has

to be poured into R&D and scientific research. Large investments are required

to embody and produce new technology. Fortunately, China has the financial

resources for this.

This issue overlaps with international problems which are

not just due to US policy but also to common problems of humanity and particularly

climate change. Regarding this it is China’s prowess in the field of renewable

energy manufacturing technology that makes possible the meeting, and potential

exceeding, of the goals of the Paris Climate Change accords.

China had outlined its goal of ‘ecological civilization’ conceptually

previously but global attention was paid to Xi Jinping’s statement at the UN on

22 September that: ‘We aim to have [carbon dioxide] emissions peak before 2030

and achieve carbon neutrality before 2060.’ For example, Adam Tooze, one of the

West’s most eminent economic analysts and historians, noted in the US Foreign

Policy magazine: ‘with those two short sentences China’s leader may have

redefined the future prospects for humanity.’

To achieve these goals, they will have to begin to be

embodied in the new Five-Year Plan and globally these will be among the most

eagerly noted of its targets.

All economies will be adversely affected by the coronavirus

crisis. But within the group of advanced

industrialised countries, the UK economy is set to be one of the most badly hit

by the crisis. This relatively worse

performance is entirely due to entirely policy choices.

One indicator of how much worse the British economy will perform is shown in the International Monetary Fund’s (IMF) latest World Economic Outlook. The key table on real GDP growth projections is shown below.

Table 1. IMF WEO Real

GDP Projections, October 2020

Source: IMF

As the table shows, the UK economy is projected to contract

by 9.8% in 2020. This is far worse than

the performance of either the world economy as a whole, where output is

expected to decline by 4.4%, or for the advanced economies which are projected

to decline by 5.8%.

According to the IMF, none of the advanced economies is

projected in 2021 to fully recover the output lost in 2020. If the entire 3-year period of 2019 to 2021

is taken together, the world economy is expected to grow by just 3.4% over that

time period and the advanced economies are expected to lose just under 0.5% of

GDP. But the UK economy is expected to

have contracted by 3%.

The IMF’s projection are unlikely to be pinpoint accurate in

all cases. But the general trend is

similar to that of other major international forecasters, such as the

OECD. The UK economy is expected to be

much weaker over the medium-term than even the very weak advanced economies.

Reasons for economic

weakness

The primary reason for the relative weakness of the UK

economy is the scale of the pandemic itself.

This is shown in Chart 1 below.

Chart 1. Advanced

Economies Covid-19 Death Toll per Million

Source: FT

The UK’s death toll is currently 642 per million, the worst

among this group of advanced economies. There is no ‘trade-off’ between

economic activity and suppressing the virus.

A failure to drive down the number of cases and deaths inevitably means

that the economy cannot recover as all types of consumer industries are

hit. The weakness of these sectors also

depresses the production and distribution industries connected to them,

everything from food processing to transportation.

But other factors are also at work. The UK has a uniquely poor government support

scheme for jobs, which has already been kicked away. And the economy was also slowing at the turn

of the year, prior to the pandemic and in anticipation of Brexit.

All of these, the failure to suppress the virus, the removal of the furlough scheme and the threat of Brexit, are the product of government decisions. It is the government that is causing this extreme economic weakness.

The cumulative consequences are disastrous. In addition to a huge and mounting death

toll, the government’s efforts to ‘protect the economy’ have proved to be

completely counter-productive. This is

shown in the chart below.

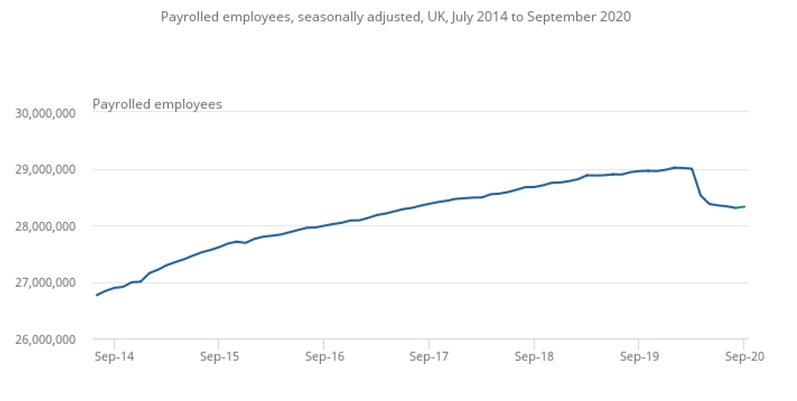

Chart 2 shows the number of UK payroll jobs as reported to

HMRC. As such they are a very valuable

and timely indicator of what is happening to regular paid employment.

Chart 2. UK Payroll

employees

Source: HMRC – PAYE Real Time

The data shows that a net 690,000 jobs have been lost

between January and September this year.

Crucially, there was barely any pick-up in jobs in September despite the

fact that lockdown was ended well before then.

As the full furlough scheme, with 80% of wages paid ends in October,

another slump in payroll jobs seems likely.

This too is the responsibility of the government, who are

well aware ending the furlough scheme will crush jobs. But the government clearly does not see its

role as preserving lives or jobs. The

focus is on preserving profits, and this will be dealt with in a follow-up

post.

The decision of Jay Powell the chair of the US Federal

Reserve Bank (central bank) to adopt a policy of higher inflation is another

hammer blow to workers and the poor.

Already reeling from job losses and pay cuts under the cloak of dealing

with the economic fallout from the pandemic, workers and those on fixed incomes

such as benefits will see their living standards fall even further, if the

central bankers are successful.

The central bank which most closely follows the Federal

Reserve policy changes is the Bank of England. But others may also feel they

are obliged to follow suit, especially as the US Dollar is falling sharply,

which places upward pressure on other currencies and damages their competitiveness.

The new policy

The Fed chair justified his new policy on the grounds that

at some point in the future interest rates would have to be cut again to

support the economy, but as they are already near-zero inflation would be

necessary to allow interest rates to rise first.

This is hokum, which only highlights the complete failure of

official policy in the Western economies over a prolonged period. The G7 has

never properly recovered from the 2008 recession and its economies are now

facing the worst crisis since the 1930s.

The time for decisive action is now, not at some unspecified point in

the future.

The central bankers and many other policymakers share the

widespread misconception that the growth in Consumption is key to economic

revival, because it is the larger component of the Western economies. In reality, as only Investment can add to the

means of production, it is Investment which creates the basis for the

sustainable growth in prosperity.

The false view on the role of Consumption (unfortunately

widely shared on the left and among progressive economists) has led to a series

of absurdities. Money is provided for an

‘eat out to help out scheme’ but money is refused to advanced manufacturing

companies that are going bust. Taxes are

cut for the rich, the central bank inflates money supply, buys bonds, gets

interest rates (both short-term interest rates and bond yields) to record lows

in an effort to boost ‘demand’ – and none of it works.

This is because the crisis which began before 2008 is a

crisis of profits, which is then expressed as a slump in private sector Investment.

The is shown in Chart 1 below.

Investment (Gross Fixed Capital Formation, GFCF) in the G7

slumped in the 2008 recession. It had

already begun to slow sharply from 2006 onwards, long before the recession

itself reflecting the slowdown in profits’ growth. Investment was also the component of growth

which registered the largest fall in percentage terms and for a prolonged

period accounted for the entire fall in GDP in the G7. In short, the recession

was driven by the slump in Investment.

Chart1. GFCF Growth

in the G7

As the chart shows, Investment in the G7 remained weak after

recession. There was never a sharp rise in Investment equivalent to the depth

of the fall in 2008 and 2009. Even

worse, Investment was contracting in the leading capitalist economies at the

turn of 2020, that is before the pandemic had any impact.

The G7 economies entered this economic crisis after a

prolonged period of Investment weakness and with renewed declines. And

Investment contracted sharply in the 2nd quarter of this year as the

pandemic spread rapidly. In the US GFCF

fell 7.5% from a year ago and in Germany the decline was 8.3%. Elsewhere it was even worse, with a fall of 24.5%

in France and the UK the worst of all with a decline of 29.8% from a year ago.

The effect of the

policy

It is not possible to address a crisis of investment by

adjusting the policy on inflation. But

that does not mean that the Fed’s new policy will have no effect at all.

The real impact of the policy is that it aims to lift

prices. It has already been widely noted

that jobs are being cut and wages falling across a number of countries,

including all of the G7 in response to the economic impact of the pandemic. By raising the sales prices of producers and

retailers, while wages are being cut across the private sector, the hope is to

raise profits.

Since the decline in profits is itself the cause of the

private sector refusal to Invest, it may even be possible for big business to

lay the basis for a profit-led recovery in Investment. In strictly scientific, that is Marxist

terminology the capitalists will have increased the rate of exploitation either

by getting the retained workforce to work harder without an increase in pay and/or

forcing workers to do the same hours for less pay.

This is certainly what stock market speculators are

expecting. The US stock market is

reaching new all-time highs even during a global pandemic and deep economic

crisis. This is because speculators expect

the actions of firms in cutting payroll and pay to boost profits. The actions of the Fed, and any other central

banks that follow suit, will have the effect of adding to those pressures, for

higher prices and profits, and lower pay and living standards.

Chart 2. S&P

500 Index Above Pre-Covid19 Peak, New All-Time Highs

Source: FT

There is currently an

all-sided attack taking place on the living standards of workers and the

poor. The aim of the new central bank

policy is to reinforce that attack.

The enormous loss of jobs in recent weeks will not be halted

by the miserable ‘summer statement’ announced by the government. In fact, the flow of job losses is a direct

result of government policy itself, in particular how it is ending the furlough

scheme. Despite intense public (and

presumably private lobbying) from both employer organisations and trade unions,

the Chancellor Rishi Sunak made no changes to the furlough scheme, which is

widely described as a ‘cliff edge’ for jobs.

The cliff edge

The jobs furlough scheme is being phased out with employers

having to meet 20% of pay for retained workers from August. The scheme will end entirely in October. The government claims that the scheme is

uniquely comprehensive and generous.

These claims are false.

Fig. 1 from the OECD shows the number of employees covered

by the job retention scheme in the UK is less than a third of the total. This is very far from the best in the OECD

and does not include at all the large numbers of self-employed, many of who

have been forced into fake self-employment over several years. It should be

noted too that actual job retention for employees in the US is virtually

non-existent.

Fig1. Job Retention Schemes in the OECD

But soon even these supports will be kicked away. From August 1st, employers will need to pay

20% of wages of retained workers and from October 1st they will have

to pay 100%. The businesses that are

currently generating little or no income will lay off workers rather than have

to pay even 20% of wages. Come October,

the vast majority of businesses who are failing to generate profits will lay

off workers or severely cut pay both, or both.

The reason for the wave off announced job losses now is

because of statutory requirements to consult with the workforce about job

losses. The consultation period varies

according to the size of job losses – 30 days for

layoffs for up to 100 workers, 45 days for 100 or more.

Critics are right to call it a cliff edge. It is because of this sudden and brutal

withdrawal of even the inadequate support for furlough that companies are

announcing the job losses now. And the

wave of announced job losses is enormous, and with a far greater proportion

likely to be done without any fanfare.

The job

losses announced in July alone include Jaguar Land Rover, Poundstretcher,

Bella Italia, Harrods, Arcadia, John Lewis, Accenture, Upper Crust, Café

Ritazza, Harveys, TM Lewin and Royal Mail.

Other companies have threatened job losses to achieve pay cuts, Ryanair,

Mirror Group Newspapers and BA among them.

Against this backdrop, both the scale and composition of the

government’s ‘Plan for Jobs’ (pdf

) is wholly inadequate. A combined package of £30 billion is equivalent to just

1.4% of GDP, the type of small stimulus that would be appropriate coming out of

a mild recession.

Worse, the package is best characterised as a series of

small subsidies to businesses. Yet many

of these consumer businesses will continue to fail because the government has

failed to get the virus under control.

School attendance, footfall in shops and even pub going remain massively

below where they would normally be because the majority of the population is

right to remain extremely wary of a return to normal. Paradoxically, in putting profits first at

every stage rather than public health, the government has deepened and

prolonged the economic crisis.

The private sector in general will only retain workers or

maintain investment levels if there is a prospect of profits. These small-scale subsidies are largely

irrelevant to profitability. At best

they are one-off windfalls to businesses who will not change their plans as a

result. The ‘Plan for Jobs’ will fail.

Remembering 2008 to

2010

There is a remarkable propensity to forget what happened in

the crisis of 2008 onwards. This is

especially dangerous in the current period, because lessons from that period

are vital in understanding the current threat to jobs, pay and living

standards.

The fall in profits in the UK began in 2007, leading to

full-blown recession in 2008. The initial

policy response was to bail out banks and big businesses in 2008 to 2009. Only as the economy stopped contracting was a

vicious austerity programme introduced in 2010.

When the Chancellor announced £330 billion in bail-out

measures in March this year he was simply repeating that sequence. The austerity is in the pipeline.

But history will not simply repeat itself, for two reasons.

It was extremely difficult for businesses to impose big real terms cuts in pay

from 2008 onwards because unemployment did not rise sharply and inflation

remained low. Achieving cuts in nominal

pay (before inflation) under those circumstances is extremely difficult for

businesses. Instead, they relied on the

government cutting real wages in the public sector from 2010 onwards in order

to lower them across the economy, but with only limited success.

Now, the downturn is much more severe and the government is

attempting to ensure that businesses can take full advantage of the

crisis. The depth of this crisis is

shown in the chart below, in latest data from the Office for National

Statistics (ONS) on average hours worked, which compares US and UK average

hours worked versus the same periods in the previous 12 months.

Chart 1. UK and US Average Weekly Hours Worked to May

2020, per Employee

In the UK, average hours worked in April were 25.4. This compares to 32.2 hours in April 2019, a

fall of almost 27% per cent. As labour

is the most important factor in production, it is impossible for a fall of this

size not to produce an extremely large fall in output.

This is in sharp contrast to the crisis of 2008 onwards,

shown in Chart 2 below. Average weekly

hours also peaked at 32.2 hours in February 2008. The low-point was 31.3 hours in April-May

2011, a much more modest decline of 2.9%.

Chart 2. UK Average Weekly Hours Worked in 2008 to 2012

On this measure, of average weekly hours lost per employee,

the current crisis is qualitatively worse than in the recession of 2008

onwards.

The alternative

The ‘Plan for Jobs’ approach will fail because, as in 2008

to 2010 the policy relies on subsidies to the private sector to revive the

economy even though it is unwilling or unable to rehire and invest. On both occasions, pro-business governments

refused to do what was necessary to revive the economy because this would

interfere with the workings of the private sector.

So, (necessary) schools rebuilding programmes are permissible because they do not involve state ownership of the means of production. The state taking control of failing railways, or investing in new renewable energy production are both ruled out. This is because the state then would then become a bigger economic agent, preventing the direct accumulation of profits in some sectors. This would be to overturn the entire policy of the last 40 years, which has been to allow the private sector ever greater ownership of the means of production through privatisation and outsourcing.

One obvious response to the jobs crisis is to share the work

available and demand a 4-day week. This

has already been raised by MPs,

led by the Labour left, and could be taken up by trade unions. But it is imperative that this demand is

raised in conjunction with the simultaneous demand for no loss of pay. Otherwise, there is simply the danger of

facilitating the threats from BA and Ryanair, who have imposed huge pay cuts

under the guise of job-sharing.

But it should be clear that huge attacks on the working

class are coming. In fact they have already begun. The labour movement needs to resist these

otherwise it will suffer very heavy blows.

The depth of the economic crisis that has already begun to

grip the British economy will inevitably lead to a full-scale assault on the

working class. This is because capital

requires the restoration of profits, which will have fallen sharply in the

crisis.

The struggle to increase the rate of exploitation in order

to restore the profitability of UK firms will necessarily be a ferocious one. It

is completely mistaken to suggest that austerity is over as it is imperative

that profits are restored. If there is to be any successful resistance it is

necessary to face facts and not engage in wishful thinking.

The next crisis,

before the last one is over

By widespread consensus, the current crisis will be sharper

than the recession of 2008 to 2009. The

UK recession in 2008/09 lasted 5 quarters from the 2nd quarter of

2008 to the 2nd quarter of 2009 inclusive. From the pre-recession peak in the economy

the total decline in output was 6%, the largest fall in the UK in the

post-World War II era. Because of very

weak growth, the economy did not recover to its pre-recession peak until the 2nd

quarter of 2013, four years after the crisis began.

In one important sense, there never has been a full recovery

from that recession in terms of returning to previous trends. There were also clear signs that the economy

was slowing from a very weak pace, even before the impact of the coronavirus

was felt. This can be seen in Chart 1

below, although naturally the most striking feature is the unprecedented pace

of the contraction in March and April this year.

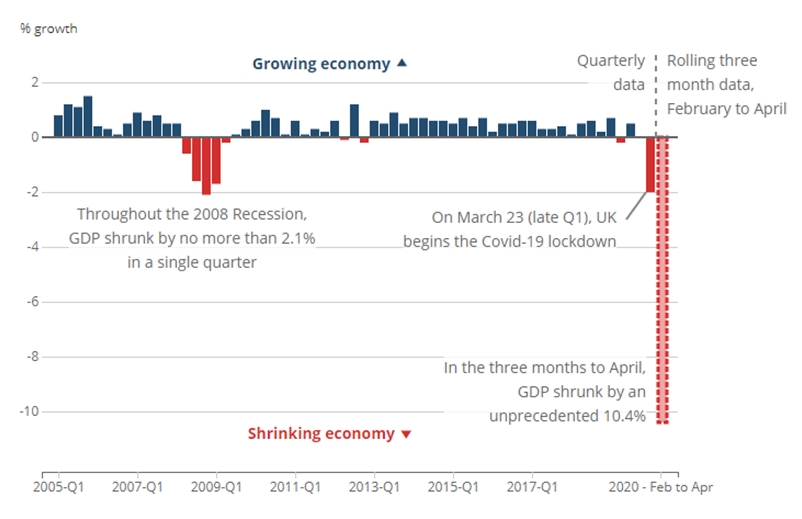

Chart 1. UK Real GDP, Quarterly Q1 2005 to Q1 2020

Source: ONS

The Office for National Statistics (ONS) has highlighted all

periods of economic contraction in red.

Helpfully it has also provided an estimate of GDP in the 3 months to

April. In that period the economy shrank

by 10.4% (and fell by 20.4% in April alone). As the chart shows the pace of the

contraction is already much more rapid than in 2008-09.

It is also likely to be a more severe recession than a

decade earlier. This is based on the

evidence to date. In addition, the most

recent noted forecasts for UK GDP in 2020 range from a 7.2% contraction from

the National Institute for Economic and Social Research, to the ITEM Club’s 8%

fall, to the European Commission’s decline of 8.3%.

But the forecasts are deteriorating as the extent of the

coronavirus becomes clear, along with the UK government’s catastrophically bad

response to it. The OECD is the only

major institution to have published a UK GDP forecast in June and it now expects

a decline of 11.5% in 2020, the worst outcome of any advanced

industrialised economy. This would be

almost double the total contraction in output of 2008-09.

Profits first, last

and always

The motor of the capitalist economy is profits. Firms do not exist under capitalism to make

specific goods, or to employ a given number of people or to provide a basis for

philanthropy. Firms can and frequently

close entire sectors of their business and switch to others, or fire large

parts of their workforce, or spend large resources in avoiding paying

taxes. The purpose of the capitalist is

to realise profits.

In a recession, profits get crushed. Very frequently, profits fall first, firms

stop investing and that itself causes recession. This is precisely what happened in the US

from 2006 onwards, concentrated in the housing sector. In this country there was a very sharp fall

in the rate of return on capital employed by UK firms directly linked the

recession, as shown in Chart 2 below.

Chart 2. Rate of

Return on Capital of UK Firms, 2003 to 2019

British firms suffered a fall in the rate of return of from

11.6% in 2006 to 9.4% in 2009. The

response was ‘austerity’ in 2010, which Alistair Darling’s 2010 Budget

threatened (widely said to

have been written by Peter Mandelson) and which Cameron and

Osborne implemented.

Austerity is aimed at restoring profits. The rhetoric about government debt being out

of control is merely a device to cloak the real content of economic policy, as

was monetarism before it. And one of the

reasons SEB has repeatedly warned that austerity would not be ended now

is because British capital had not resolved its crisis of profitability. In fact, Chart 2 also shows that

profitability was declining once more even before the coronavirus hit.

There are a number of different ways that profitability can

be restored. But, in the unlikely event

that British firms will conquer new markets (at the same time as erecting

barriers to their biggest market in the EU), then the various forms of

increasing the rate of exploitation of workers are required.

These are to demand that workers produce more for the same

pay (either fewer workers and/or shorter hours) or pay is cut outright while

the work is unchanged. In this regard,

the growth of large numbers of unemployed or marginalised workers with few

rights is extremely important. This had

already begun with the growing casualisation of the workforce, the ‘gig

economy’, zero hours and fake ‘self-employment’.

This will be increased through the Covid-19 crisis. In

addition, the government’s new immigration policies will not make good on their

reactionary promise to reduce migration (non-EU migration had already risen

under the Tories to replace the decline in EU migration because of Brexit).

Instead, the real purpose of the policy is to create a large cohort of workers

without either citizens’ or workers’ rights, who can be used to lower pay and

conditions more generally. A general assault on workers’ rights, and the

environmental protections and product standards that are an impediment to

profitability will be facilitated by Brexit.

As the furlough scheme comes to an end, the government has

consciously created a pressure for firms either to cut pay, or to cut

jobs. This gives firms the opportunity

to co-ordinate their efforts, so that the widest possible number can benefit

from increasing the rate of exploitation this way.

Therefore, it is completely muddle-headed to suggest that

Boris Johnson will not return to austerity.

As SEB explained

about the March Budget, he already has. Denying free school meals in the summer to

poorer children while guaranteeing banks’ lending for £300 billion also shows

that transferring resources for poor to rich and from workers to banks ad big

business is back with a vengeance.

A child’s lullaby that everything will be fine, that there

will be an outbreak of fairness from Johnson and Keir Starmer was really a

Cobynista all along is not merely foolish but downright dangerous in the

current circumstances. The British

ruling class is gearing up for an enormous offensive, compelled by the logic of

capitalism itself. The working class and

its allies need to be prepared for the coming onslaught.

In all the catastrophic information generated by the

coronavirus crisis it is easy to overlook an crucial piece of good news. The virus can be defeated and has been

defeated in many countries.

Unfortunately, in many western countries one of the self-serving and

reactionary myths peddled is that the coronavirus cannot be defeated and that

we have to go back to work and ‘live with it’.

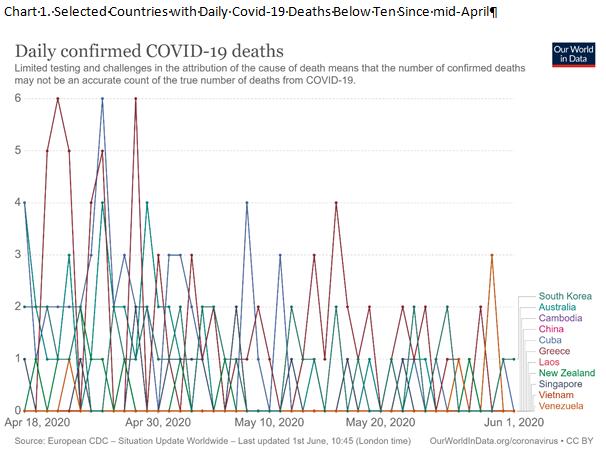

It is easy to demonstrate that many countries have defeated

the virus, or decisively contained its lethal spread. Chart 1 below shows the daily death toll in a

series of selected countries. From April

18 onwards, there is a group of eleven countries whose maximum daily death toll

is now below ten. In many of these

countries, there have been no new deaths at all over a prolonged period.

Chart 1. Selected Countries with Daily Covid-19 Deaths Below

Ten Since mid-April

There are four criteria for selection. Each country has had a significant outbreak

of the disease – meaning they are already below their peak. They have

experienced no sustained new rise in the death toll They are also countries

with a population of approximately 5 million people. Finally, their death toll

has not been in double figures on a daily basis in that period. As the chart shows this group includes

Australia, Cambodia, China, Cuba, Greece, Laos, New Zealand, Singapore, South

Korea, Venezuela and Viet Nam.

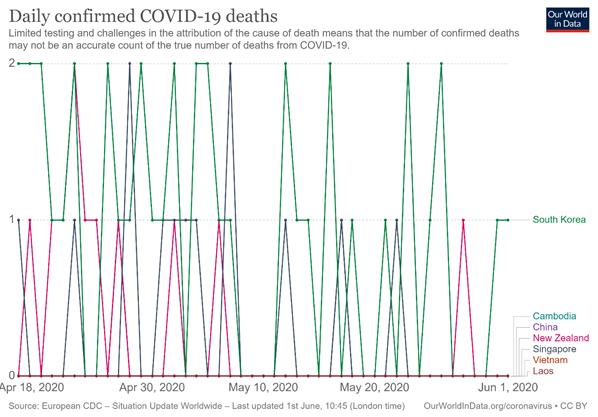

Chart 2. Selected Countries with Daily Covid-19 Deaths at

Two or Below Since mid-April

There is a further select group of 7 countries where the

daily death toll has not exceeded two since April 18, shown in Chart 2 below.

This group includes Cambodia, China, New Zealand, Singapore, Laos and Viet

Nam. These countries have effectively

eliminated the deadly spread of the virus. In per capita terms, China has the

lowest death toll of all, which has had no deaths at all.

Taking either group of countries, they are far from

homogeneous in terms of geography, population or political system. What they all did, to one extent or another

is learn from the Chinese experience when it locked down the province of

Hubei. Above all, they put public health

first, not a vain attempt to avoid disruption to the economy.

Taking the second group of countries, their combined death

toll has been minimal over a period of 6 weeks, a total of under 300 over that

period. This is in a combined population

of over 1.5 billion people. They did not

live with the virus. They defeated it.

By contrast, other countries mishandling of the crisis has

been catastrophic, including the US, UK and Brazil. When their leaders demand the population

lives with the virus, of course they mean that many of them will die with

it. This is a political choice, not an

inevitability.

While

most countries in East Asia and the Pacific (China, South Korea, Thailand,

Australia, New Zealand etc) have reduced the number of daily coronavirus and

deaths to essentially close to zero a number of countries, particularly the US

and in Western Europe, have begun to ease lockdown measures even though the

spread of the coronavirus has not been decisively halted. Both logic and

experience are clear that this latter path is the wrong way around to defeat

the spread of the virus. In addition, the World Health Organisation has already warned of a second peak in

cases.

Instead

lockdowns should continue until some time after it is clear that the virus is

at a manageable level – defined as at most less than a few dozen cases and that

full tracking, tracing, testing and isolation regimes are in place.

Of

course, the trajectory of the virus’ spread matters to each individual country.

It matters for every other country too, given the global spread of the

pandemic. It is also important to learn lessons from each other, to avoid the

worst effects of the pandemic and to mitigate them as far as possible.

Unfortunately,

European countries in general have been extremely reluctant to learn from the

countries of the Asian Pacific who have successfully combated the virus. So,

Germany is held up as an exemplar of how to respond to the crisis, when in a

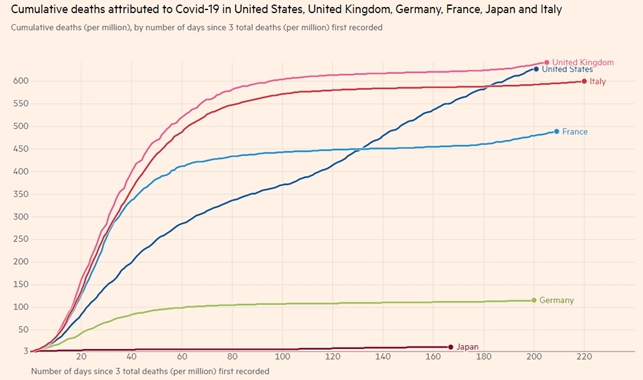

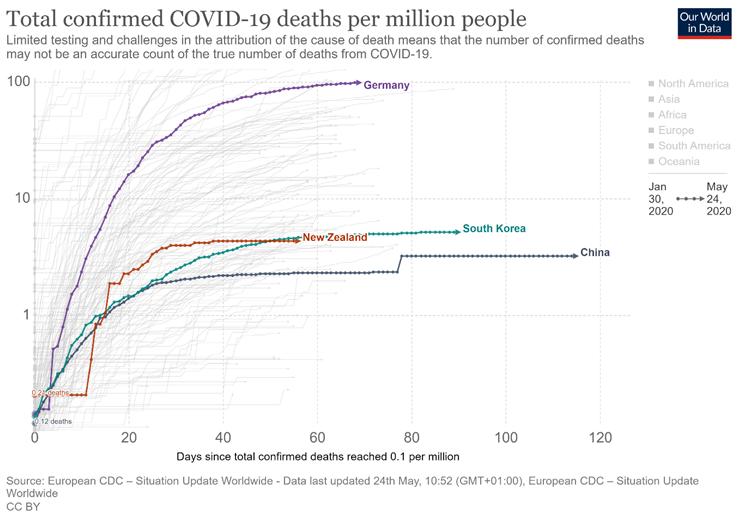

global perspective it is nothing of the kind. This is illustrated in Chart 1

below, which shows the per capita death toll in Germany versus key Asian

Pacific countries. It clearly shows the death toll is catastrophically worse in

Germany (all data throughout from Our

World In Data throughout, unless specified).

Chart

1. Deaths Per Million in China, Germany, New Zealand and South Korea

The

data makes this disparity even more stark. Table 1 below shows the death total

of each of the 4 selected countries in Chart 1.

Table

1. Cumulative Total Covid-19 Deaths for Selected Countries, per million

Total

China

3.3

New Zealand

4.3

S Korea

5.2

Germany

99.5

Source: Our World in Data, based on FT analysis of data from

the European Centre for Disease Prevention and Control and the Covid Tracking

Project.

The

unwillingness to learn from other countries with far greater success in

combating the virus is combined with highly distorted coverage of those

countries in Western media. So, the reports of flare-ups of the virus in both

China and South Korea were treated with a mixture of derision and

misinformation. The implication has been that the Asian Pacific governments

have been extreme in their response and unsuccessful. As the comparative date

above shows, both of these points are untrue. The Asian Pacific countries have

put public health first, unlike the Western governments, and despite a few

missteps they have been remarkably successful.

By

contrast, in their back-to-work propaganda campaign, Western governments

increasingly rely on the completely false assertion that ‘it is impossible to

defeat the virus and we have to live with it.’ Yet many of the Pacific Asian

countries have demonstrated the opposite, including those cited above. Many

have recorded no new deaths for weeks.

Learning from Europe

However,

it is also possible to learn from the missteps of others. In this respect it is

unfortunately the case that Europe provides plentiful examples, especially now

on the premature easing or ending the lockdowns. This is true even in countries

which are relatively successful in combating the spread of the virus, at least

on a European scale.

Countries where new cases are rising

This

is illustrated in Chart 2 below. This shows two European countries where it is

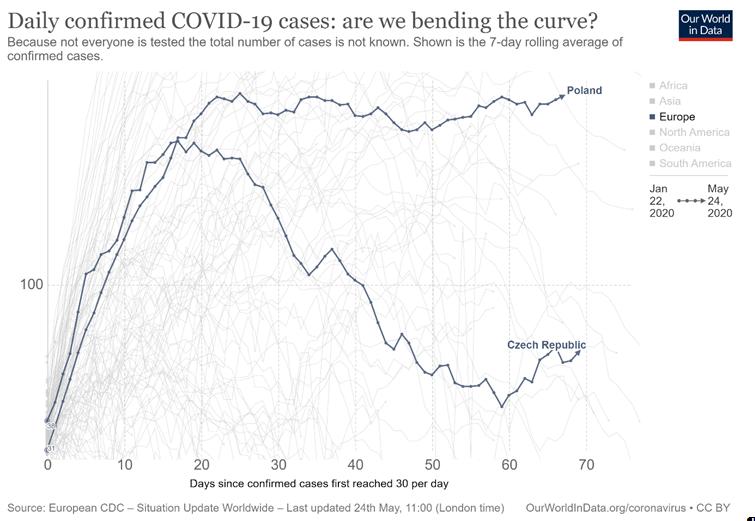

clear that the death toll has started to rise once more, Poland and the Czech

Republic.

Chart

2. Daily New Coronavirus Cases in Poland and the Czech Republic, 7-day moving

average

The

Czech Republic hit a low-point in new cases of 42 on April 27 and these have

since risen to 62. Poland reached a low of 296 new cases on a 7-day moving

average basis on May 5 and they have since risen to 382.

At

this point, the analytical tools provided by Our World in Data are very

valuable. Among many other categories, there is also data on policy changes in relation to the lockdown.

In relation to Poland, the data shows that stay-at-home restrictions on were

introduced on March 31st, but eased again on April 9th.

At the same time Poland has no systematic regime for contact tracing at all. In

the Czech Republic the lockdown on schools was eased on May 11 and the lockdown

for all but essential workers was eased on April 20. Stay-at-home restrictions

were eased one day later, while internal restrictions on movement had been

eased on April 2nd.

Countries where new cases are no longer

declining

There

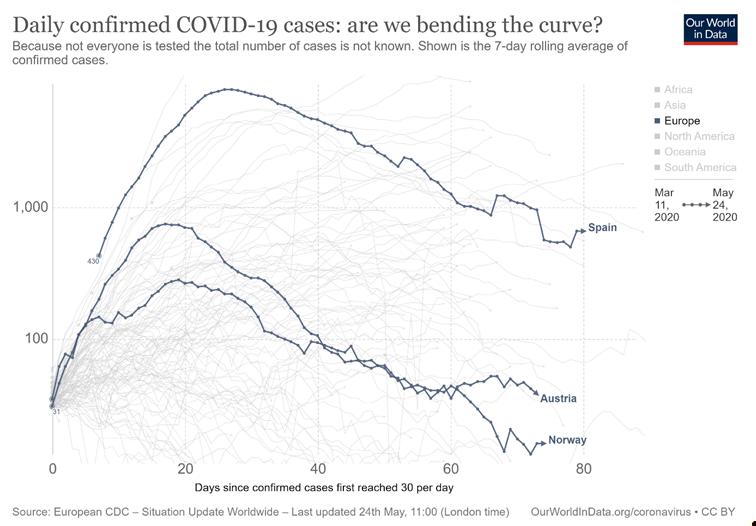

are also a number of European countries where the fall in new cases has halted.

Hopefully this is temporary, but the previous downward trends in new cases has

come to a stop for now. Chart 3 below shows the 7-day moving average for new

cases in Spain, Austria and Norway. Hungary could also have been included, but

has been omitted for clarity in the chart.

Chart

3. Daily New Coronavirus Cases in Spain, Austria and Norway, 7-day moving

average

From

the chart above it is clear that new cases in all 3 countries are no longer

falling. The latest level of Spanish new cases is higher than they were six

days ago. The downtrend in Norwegian cases has stalled. There has effectively

been no decline in Austrian cases since May 7.

Austria

and Norway removed restrictions on all but essential work on April 18 and April

20 respectively. The following day Norway also eased restrictions on public

gatherings, but partly reversed course on May 11, while Austria eased these

type of restrictions on May 2. Norway partially lifted restrictions on schools

on April 20 and again on May 11. Austria reopened schools on May 18, having

lifted the stay-at-home order on May 1st.

It

should be noted that, despite much publicity, Spain is not categorised as

having lifted any restrictions within these data. This is because, having been

very late into lockdown after the virus had spread, the eventual easing of

restrictions by the Spanish authorities was extremely limited. Allowing

children out very briefly, plus limited opportunities to exercise and the

partial reopening of bars and restaurants for takeaway and delivery services

which took place at the end of April and beginning of May had always been

allowed in Britain’s rather lax lockdown, for example.

Countries where the downtrend in cases has

slowed

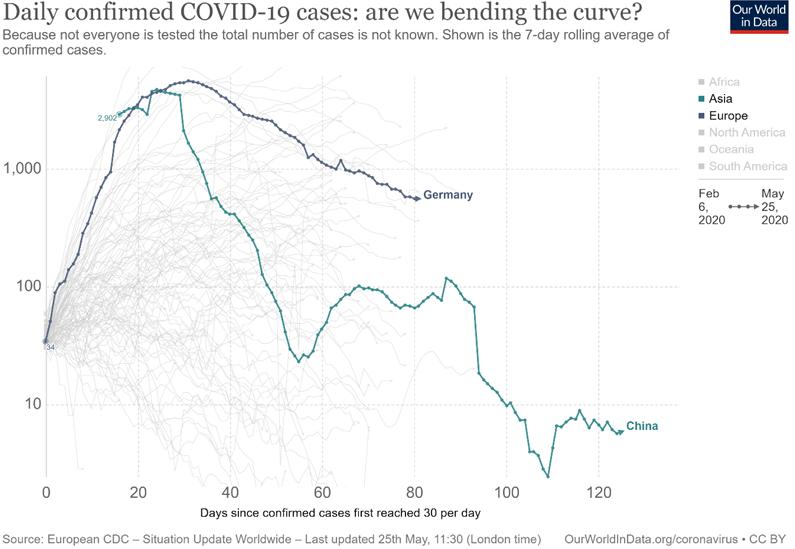

Germany

is not an exemplary country in fighting the virus, as previously noted. Even

so, Germany still has one of the better trajectories in combatting Covid-19 among

the large European countries.

Yet

Germany risks falling into a category of countries where lockdown measures have

been eased but the fall in cases has slowed. This is illustrated in Chart 4

below.

Chart

4. Germany and China New Coronavirus Cases, 7-day moving average

On

May 23rd Germany was in its 83rd day of coronavirus cases, with a

total of 561 new cases per day. At the same period in the spread of the virus

in China cases had fallen to 102 cases. As the chart clearly shows, Germany is

not crushing the spread of the virus in the way that China and other

Asian-Pacific countries have.

But

it has also eased lockdown measures, unlike China and other countries. The

effect has not been to produce a rise in new cases, or even a halt to that

decline. However, the rate of decline has slowed quite soon after the lockdown

was eased. Germany eased the lockdown on schools on May 4, but otherwise most

measures have stayed in place.

Following

this measure, the fall in German cases has slowed. On May 6 German new cases

had slowed to 1,000 per day. They have since fallen by 44% to 561 per day. However,

in the preceding 17-day period they had fallen by 62.5%. This slowdown may only

appear incremental, but the effect is to create hundreds of additional cases

per day. Worse, the real negative effect of easing should only become apparent

up to 14 days later given the incubation period and lags in testing and

results. Using a 7-day moving average to smooth daily volatility will add a

further delay before substantial changes become apparent.

So,

the concern is that a definite slowdown in the new case rate in Germany after

easing the schools’ lockdown may only be registered in the data from now

onwards, in the last week of May. Many other countries where lockdown has been

eased are in a similar position. In both France and Finland it is reported that some schools

were closed once more because of new outbreaks.

The case of Britain

It

is widely understood that in the UK new cases are falling. But it has already

been shown that a simple fall in new cases is insufficient to prevent a

reversal once lockdown is eased.

Two

conditions need to apply. The first is that the number of new cases has fallen

to such a level that each new case can be identified, and the second is that

the contacts of each new case can be rapidly tracked, traced, tested, and where

necessary placed in isolation. Neither of those conditions currently applies in

this country.

Table

2 below shows the number of cases in each of the European countries cited in

this piece at the time lockdown was eased. It also shows, using the Our World

In Data categories, what the type of testing and tracing regimes were in place

at the time of that easing. UK is also shown for comparison.

Table

2. Selected European Countries, Cases Per million and Testing & Tracking

Regimes When the Lockdown Eased

Cases per

million

Testing

Tracking

Poland

9.9

Targeted

None

Czech Republic

11.5

All persons

with symptoms

Comprehensive

Austria

13.8

All persons

with symptoms

Comprehensive

Norway

16.8

Targeted

Limited

Spain*

24.4

Targeted

Limited

Germany

13.0

Targeted

Limited

UK

37.6

Targeted

None

Source:

Our World In Data

*Spain’s

actual ease of lockdown begins on May 26 with a partial school reopening

It

should be clear that the UK is in no position to begin easing lockdown at all. This

comparative group comprises countries where the fall in in cases has either

slowed, or stalled altogether, or where cases are rising once more. Yet in all

cases, the UK number of new cases per million is still far in excess of any of

these when they eased their respective lockdowns.

In

addition, the required system of tracking, tracing, testing (and where

necessary isolation) is simply absent. It is already the case that the UK

system of testing is wholly inadequate, and not just because the government

repeatedly misses its own target of 100,000 people tested each day.

The

UK mortality rate (deaths per case) is currently 14.3%. This compares to a

European average of 8.7% and a global average of 6.5%. There is no suggestion

that the UK is faced with a particularly virulent strain of virus. Instead, the

clear implication is that the testing regime is extremely poor, capturing only

half of the proportion of cases that are recorded elsewhere.

Currently

the UK is still recording an additional 3,000 or so cases per day. It has been

shown elsewhere that each new case presents between 50 and 60 contacts

that need to be tracked and tested. This implies a further 150,000 to 180,000

additional test per day, when even the current requirement cannot be met.

Finally,

there is no contact tracing mechanism in place at all. Instead, we have the

Isle of Wight app, which has disappeared into the same rabbit-hole as the Dyson

ventilators.

The

UK has an extraordinarily high new case rate, despite a limited level of

testing which artificially depresses those numbers. For example, the Office for

National Statistics estimates that the new case rate is 9,000 per day. Any

easing of lockdown would require a massive increase in the current rate of

testing in order to cope with just the currently identified cases. And there is

no system in place at all for tracing those contacts of new cases. None.

The

government says it will make a decision on easing lockdown on May 28 and the Prime

Minister now insists once more that schools will re-open on

June 1. Now is the time to apply maximum pressure to resist this

reckless decision with predictably dire consequences.

Recent Comments