Panic on world markets

By Michael Burke

International business news and other TV channels are offering a Babel-like interpretation of the current slump in world financial markets. European (including British) stations are reporting the Wall Street-led declines as a response to the continued debt crisis in Europe. But this makes no sense. An EU crisis would have been felt first in EU markets and perhaps not at all in the US – US stocks had been rising over a prolonged period while Europe has been in turmoil. (And, despite what we may think, Greece or Ireland might fall into the sea while causing barely a ripple in the Hang Seng and the other plummeting Asian stock indices).

US channels have no explanation at all for the crisis- and analysis is limited to individual stocks, the scale of losses for investors and a generalised antipathy to Washington.

The Asian networks come closest to identifying the source of the current crisis- which isn’t in Europe at all. Their consensus is that markets are plunging because of the slowdown in the US economy.

But, why now? We are repeatedly told that financial markets react instantaneously to new information. The US GDP data for the 2nd quarter of 2011 were truly awful, up just 0.7%. As the BEA annualises quarterly data (multiplies by 4) this means that the US economy grew by under 0.2% from the 1st quarter.

On closer inspection the data were even worse. Large downward revisions to both the prior quarter and further back mean that economy fell by 5% in the recession, and has not recovered that prior peak in activity yet, as had been previously thought. This is the weakest US recovery from recession in the post-WWII period. Yet these data were published last Friday. If they were the immediate cause of the panic, it is a slow motion reaction.

No, the new news is the compromise agreement in Congress on Tuesday to raise the Federal debt ceiling in return for large scale cuts in Federal spending. This can only have one consequence- slower growth. Since the anticipated profits derived from growth drive stock prices, it is natural for stocks to fall when growth prospects are lowered. As Wall Streeters say, the US has just suffered a derating.

The crisis is driven by ‘austerity’- US austerity.

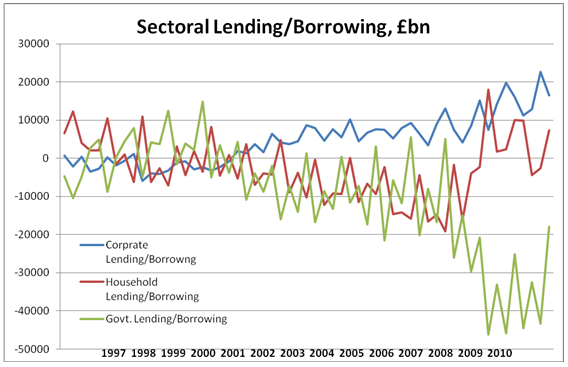

EU financial markets are caught in the backwash of this, as slower US growth certainly harms global growth prospects. This is felt most keenly in their weakest link, the sovereign debt markets, since these have assumed all the stresses of the EU economies and financial systems. But we should not expect stock and other markets in Europe to remain unscathed, especially bank stocks.

In particular, as reaction to the latest bailout of Greece’s creditors shows, bond markets do not reflect any confidence in these repeated prescriptions. Instead a first bailout of the economy is required, in Greece, Ireland and elsewhere.

There was a fondness before for asserting that Ireland was closer to Boston than Berlin. With the German economy recovering far more robustly than the US, we will hear less of that in the years ahead.

It might be wise instead to focus on the German and other answers to the crisis. This was not just short-term economic stimulus, but long-term productive investment.

For too long this economy has been a weigh-station for US companies counting their profits. Instead of listening to their self-serving advice on economic policy (while following German strictures on fiscal policy) policymakers in Ireland should emulate what works, in Germany, Sweden and most of Asia, investment-led growth initiated and guided by the State.

Recent Comments