Zoe Plummer from The People’s Assembly in conversation with Economist Michael Burke

Click here to watch the video

Comment and analysis for the movement against austerity.

Zoe Plummer from The People’s Assembly in conversation with Economist Michael Burke

Click here to watch the video

By Michael Burke

The inflationary surge is global. It is causing severe hardship in the advanced capitalist economies and economic disaster, social and political turmoil in large parts of the Global South. Reversing this crisis requires both identifying its source and adopting policies directed at that source.

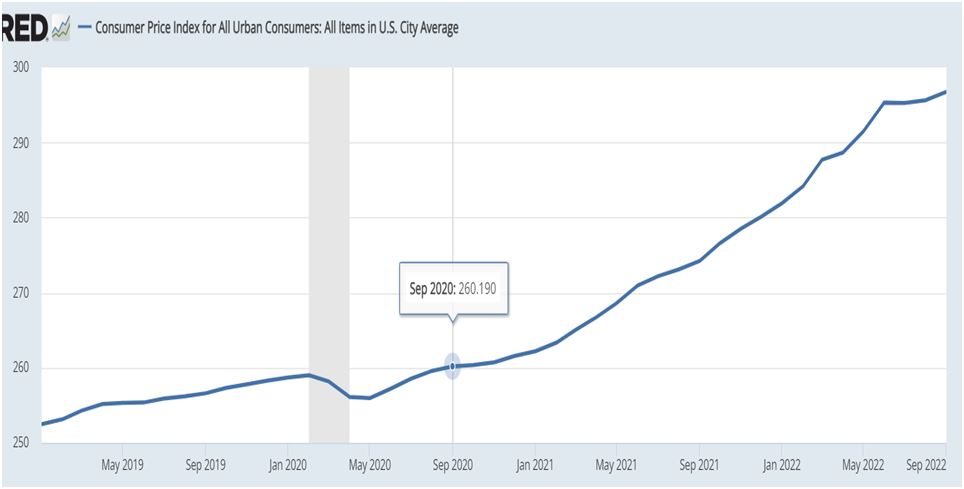

Previously SEB has shown that the widespread claim that the inflation crisis is caused by the war in Ukraine, or, as the Biden administration puts it ‘Putin’s price rises’, is completely false. This is easily shown in the chart below. Far from being a response to the war, US inflation began to rise in May 2020, which is almost two years before the war began (February 24, 2022). No event can cause changes before it even happens.

Chart 1. US CPI inflation index, January 2019 to September 2022

Source; Federal Reserve database (FRED)

Over that period of rising inflation, the cumulative rise in the CPI index has been 16%. Three-quarters of the entire rise in US CPI took place before the war began. Even if we assume that that the entirety of remaining rise was entirely caused by the war (which is not a reasonable assumption), then it is still case that the vast bulk of the rise in prices took place before the war.

SEB has also previously shown that the cause of the inflationary surge was the extraordinary and unprecedented expansion of both US Government Consumption and US money supply. As this followed a prolonged period of weak growth in Investment these policies meant a huge stimulus to the economy when there was no capacity to supply an increase of goods and services. The result was first US, then global inflation.

Money creation

There is one argument that should be addressed, not because it is powerful but because it is both widely shared and completely wrong. This is the claim that ‘poor people don’t have too much money, so the cause of inflation cannot be too much money’. This tends to be put forward by various supporters of the idea that money creation is a panacea, and that production is not central to the economy or the well-being of the population.

It was exactly this type of nonsensical think that drove the Biden administration, among other things, to sending cheques to the population to help out with rent, which had the effect of pushing up rents in the US. Rent controls combined with homebuilding are the appropriate response.

Fundamentally, money creation of this type ignores the existence of social classes and the enormous body of research ever since the GFC and the bank bailout, that relying solely on money creation benefits only the rich and the owners of capital (including landlords). It is perfectly true the poor have no money, but vast money creation makes them poorer still as the owners of capital push up prices.

No surprise of persistently high inflation

In recent months financial markets have repeatedly been thrown off guard by persistently high US inflation. This has led to both a rising US Dollar and rising intertest rates.

Both of these market responses have negative consequences for the rest of the world. A stronger Dollar leads to further upward pressures on inflation as most global commodities remain priced in US Dollars. In addition, global costs of borrowing tend to rise at least as fast as US market interest rates. Here the dominant role of the Dollar is also decisive as the US effectively sets the floor for global interest rates. (Other countries can and frequently can do have lower long-term interest rates, but their currencies play nothing the same weight in global lending).

Financial markets should not have been surprised by inflation remaining high. SEB has previously shown that the causes of inflation are the unprecedented monetary and fiscal stimulus that has been adopted in the US. Those factors have not significantly abated and as a consequence they remain a force pushing prices higher.

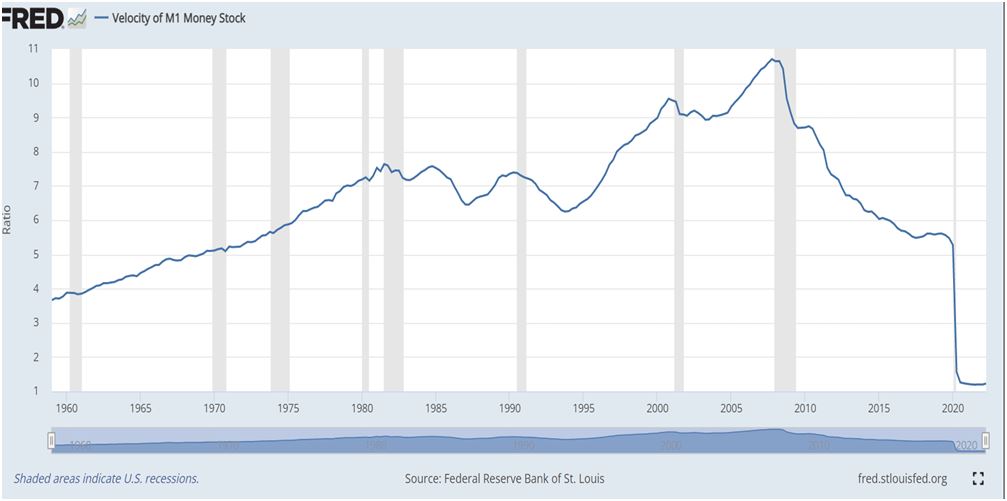

This is shown in the chart below. The velocity of money is a measure used mainly by monetarists, but also others. It is simply the level of money GDP divided by the level of M1 money supply. To return the ratio to its previous lowest ever level would require money supply to be cut by two-thirds from current levels. To return to the previous high-point (and there has been a long-term growth trend in the velocity of money ratio) would require current M1 money supply levels to be cut to less than one-eighth of its current level.

Similarly, while US Government Consumption is not rising as fast as in 2020/21, there is no reduction and may not be, even after the US mid-term elections. Both monetary policy and US Government Consumption remain highly inflationary.

Chart 2. US Velocity of M1 money supply, Q1 1959 to Q2 2022

Source; FRED

Transmission to other countries

As noted above, the global dominance of the US Dollar means that US economic and financial conditions are transmitted to the rest of world. This takes place through a number of related mechanisms; dominance of the US Dollar in global commodities’ prices, setting a floor on global market interest rates and direct currency effects in the exchange rate with the US Dollar.

Even extreme changes in the US are magnified for most countries, but especially for those dependent on overseas capital or who suffer under unequal terms of trade. The countries most badly affected by gyrations in the US economy and financial markets therefore tend to be grouped in the Global South.

International forecasters such as the IMF, World Bank and others have been slashing growth forecasts for world economy including the Global South. In addition, inflation is expected to be rampant in many countries, with double-digit inflation not just last year but forecasts of similar over several years to come. Argentina is one of the worst, with CPI inflation of close to 50% expected for many years to come, close to the hyper-inflation that destroys all fixed incomes and savings.

In the advanced industrialised economies the outlook is not as grim. But Britain is now among those where CPI inflation is above 10%, as is the Euro Area as a whole.

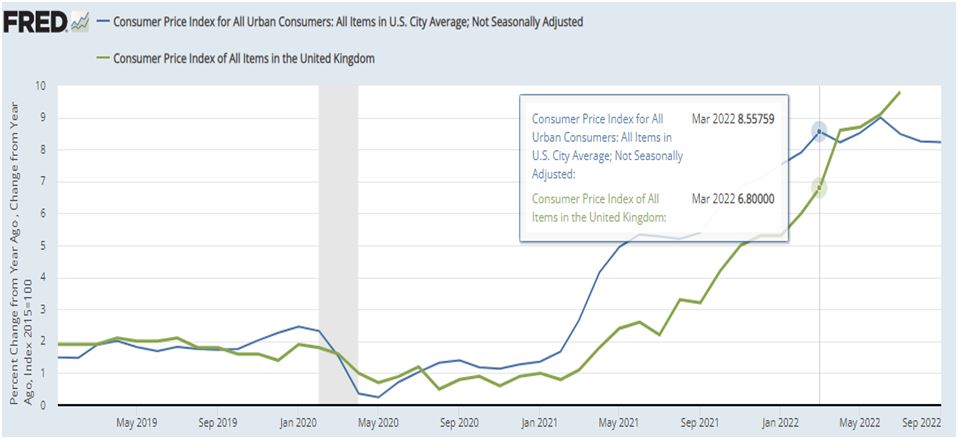

The correlation between US and British inflationary pressures is shown in the chart below. There is a comparable pattern with inflation in the Euro Area. Measured in terms of year-on-year inflation, US CPI began to rise in late 2020. Britain followed a few months later. But British price rises did not exceed those of the US until after the Ukraine war began.

This confirms that the inflationary pressure emerged in the US, especially as the Euro Area price rise is in lock-step with Britain’s. It also completely undermines any idea that inflationary pressures emerged as a result of ‘Chinese supply bottlenecks’ as China itself has experienced no similar rise in prices at all.

Chart 3. US and UK CPI inflation from 2019 onwards

Source: FRED

Almost exactly half the British (and European) rise in prices cannot at all be attributed to the war or its indirect consequences, as they took place before the war began. It is not possible to accurately disentangle the sources of price pressures after that date, but is certainly some combination of US economic policy and the price rises as a result of the war.

But even these are indirect consequences, as it not the case that Russia has cut off Western European countries from energy supplies. Instead, it is those countries that have imposed sanctions on Russia, including a boycott of its energy output.

Reversing the inflation trend

For the world as a whole the two key measures which would see a rapid decline in inflation would be:

Naturally, for policymakers in the US there are other priorities. These may have included a misconceived attempt to kickstart the US economy to vault over its rivals, the political impossibility of withdrawing massive stimulus before the mid-terms and the war.

For European and other governments who cannot determine US policy the biggest single contribution they could make to suppressing inflation would be to abandon the sanctions regime. This would also benefit countries from the Global South who suffer not only energy price rises but also grain and fertiliser shortages as part of the sanctions regime.

In addition, they could take specific measures to curb energy prices by windfall taxes or legislation to curb profiteering. Some European countries have taken these measures, such as France.

There should also be significantly increased investment in renewables as well as market measures to ensure that their actual price advantage over fossil fuels, gas in particular, is allowed to operate. There must be no more tying of renewable energy prices to gas prices, to subsidise the gas producers.

Structurally, the inflation burst is a reflection of the long-run decline in Investment in the advanced capitalist economies. The US authorities gave a huge boost to Consumption, but without Investment there was no capacity to meet it. The policy of the central banks is now a disastrous one of pushing down Consumption growth to the low level of Investment; causing a slump to lower inflation.

The logical and far less damaging course is to increase Investment and raise capacity. Done in a timely way this would lead to lower inflation and avoid or at least curtail a slump. The starting point should be the needed investment in renewables plus energy saving and insulation, as well as switching to extensive networks of environmental public transport and public housing.

The current crisis was made by policy choices, and it can be unmade by better ones.

By Mary Robertson

Coming the week after the Tories pledged to resume fracking, Labour’s plans for a publicly owned energy company have been widely welcomed, with parts of the left triumphant at putting public ownership back on the agenda. But beneath the shift in tone, Labour’s proposal fails to understand the deeper causes of the energy crisis, leaves in place the vast majority of Margaret Thatcher’s energy privatisations and is unlikely to deliver significant savings for the public. It also falls drastically short of what is needed to manage the climate emergency.

Coupled with a commitment to decarbonise the electricity system completely by 2030 and pitched as a response to the energy bill and climate crises, Great British Energy (GBE) would invest in new renewable energy generation alongside the private sector. With rising wholesale gas prices underpinning skyrocketing energy bills, this would reduce reliance on gas by helping to increase the supply of renewable energy.

Leaving aside the long-term nature of this solution to what is a very immediate problem (fuel poverty is likely to remain in excess of the 6.7 million households reached in April this year), it is not clear that increased renewable generation will translate into lower bills.

Many energy supply companies are also involved in energy generation: making enormous profits throughout the energy crisis thanks to higher wholesale prices being passed on to customers. Generation and supply are, however, separated by a series of markets, guaranteeing that the prices we pay are determined by demand and supply at an international level. Simply inserting an additional generation company leaves this dysfunctional system intact.

In contrast with the TUC’s proposal to also establish “public ownership within the customer-oriented parts of the energy system”, GBE will have no way of directly affecting bills, and an operator on its scale is unlikely to have much impact on wholesale prices.

Worse still: in Britain’s wholesale electricity market, the most expensive generator – gas – sets the price, as energy Professor Michael Grubb has explained, with households and businesses paying far more for their electricity than what it costs to generate it from renewable sources. Additional renewable generation, while leaving the privatised supply and wholesale market untouched, will not change this.

While the wholesale price of energy has driven up bills, it still accounts for only 51% of a dual (electricity and gas) household bill. 11% of household bills pays for the profits and running costs of energy supply companies and 18% for companies responsible for transmission and distribution. These aspects are will remain in private hands under Labour, despite record profits made by transmission and distribution companies during the crisis. Distribution networks enjoy the highest profit margins of any sector in Britain and use household bills to pay out billions in dividends and interest on intercompany loans. National Grid reported a 19% increase in pre-tax profits from 2020 to 2021, while earnings per share increased from 36.3p to 46.3p. The flipside of this profiteering is poor investment and infrastructure quality.

Starmer rightly asked why the private sector should be the main beneficiaries from the carbon transition, as they were from North Sea oil. But GBE will have little opportunity to change this given its limited scale, the need to establish itself in a large private-dominated market, and a likely mandate to undertake riskier new investments, effectively de-risking climate transition for the private sector. EdF, the French state operator with which it has been compared, is responsible for the vast majority of generation capacity as a result of its history as a state monopoly founded by nationalisation. GBE will have no such advantage.

What, then, about the climate crisis? Any additional renewable generation is not to be sniffed at but here Labour’s commitments are again woefully unambitious. The £8bn pledged for renewables projects (including but not limited to GBE) is the same amount Labour’s 2019 manifesto committed for additional wind power generation alone. The 2030 target for 100% renewable electricity is only five years earlier than the government’s current plans and ignores heat, which is much more gas dependent than electricity.

Labour published 30 by 2030 in 2019, a report written by a team of climate scientists and engineers that set out thirty recommendations to decarbonise heat and electricity at a pace they judged to be the upper limit of technical feasibility. Labour’s 2019 manifesto committed to deliver these recommendations through a £250bn ‘green transformation fund’ and an integrated and publicly-owned system of energy generation, transmission, distribution and supply, largely removing the ‘need’ for competing electricity suppliers to charge prices dictated in international markets.

Starmer’s announcement represents a huge rowing back from these commitments and a tragic wasted opportunity to take historic steps towards solving the energy and climate crises. As encouraging as it is to hear public ownership back in Labour’s lexicon, GBE falls far short of what the public and the planet need.

The above article was originally published here by Labour List.

By Michael Burke

The ‘mini-Budget’ delivered by Kwarteng and Truss was so devastatingly bad for the British economy and for the key finacial markets that one major international bank ended the day calling for an emergency interest rate rise by the Bank of England!

Of course, this would do nothing to alleviate the economic crisis that underlies this slump, and may be just special pleading by financial speculators. But it is an indicator how far removed this government is from economic reality.

As such they will completely fail to deliver on their stated aim of lifting the long-term growth rate of the economy from abysmally low levels. Instead, they are engaged in fantasy Thatcherism, an effort to Americanise the British economy with a policy of hammering workers and the poor, susbsidising big business and the rich. The are likely do enormous damage before failing.

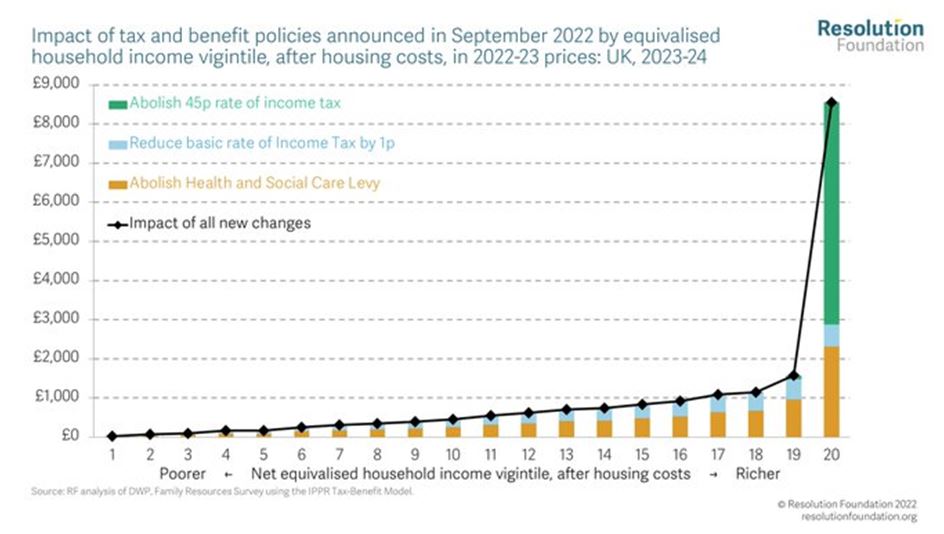

Numerous commentators have pointed how regressive the government’s measures are, in redistributing upwards for high earners and for owners of capital. This is how the Resolution Foundation explained this reactionary redistribution, shown in Chart 1, saying, “Almost half of the gains from tax cuts next year go to the richest 5% of households. The poorest half get an average of £230 vs £3,090 for richest fifth.” Overall, taking into account all changes to tax and National Insurance, “only those earning over £155,000 will be better off.”

This is just 1.4% of all taxpayers. This is economics of and for the 1%.

Chart 1.

Source: Resolution Foundation

At the same time, there is an enormous tax giveaway for businesses, amounting to tax cuts of just under £70bn in taxes on profits over the next 5 years.

All of these measures are being enacted when the mass of the population is struggling with the deepest crisis of living standards in living memory. The message to workers and the poor, ‘Go to hell!’

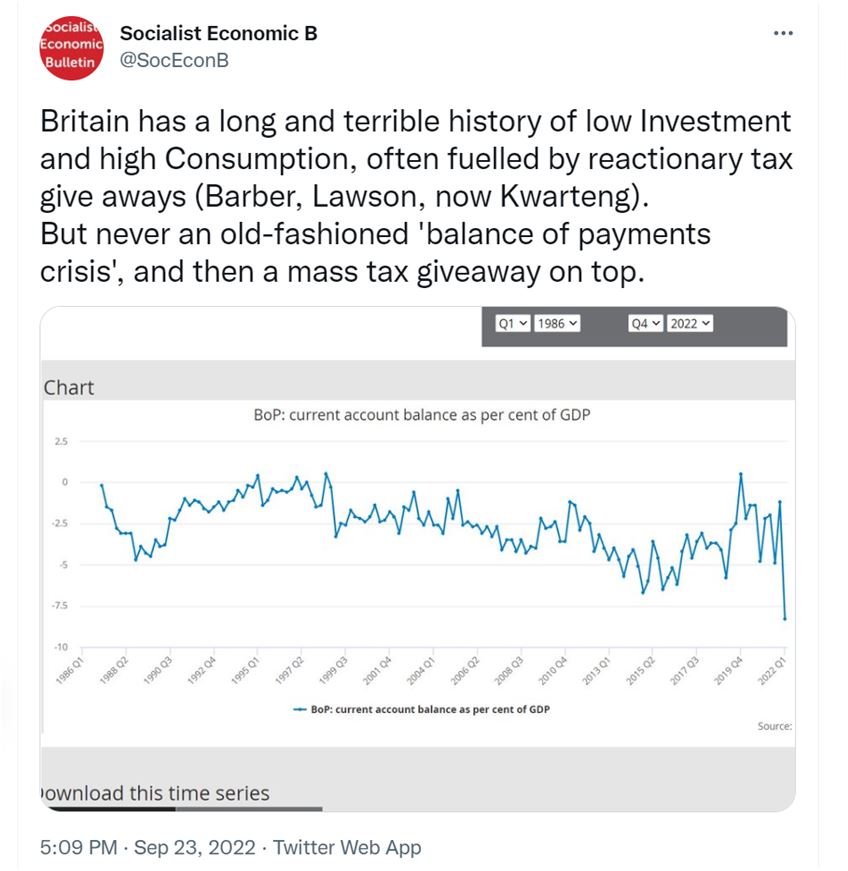

A balance of payments crisis

This wilful disregard of the objective reality is not confined to the issue of the impact on households and the cost of living crisis. The mini-Budget simply failed to take account of the key problems of the British economy, which is why the response of financial markets was panic, rather than horror from the population.

Britain has a long and unhappy history of ‘balance of payments crises’. These reflect the British economy’s chronic lack of Investment, leading to both weak productivity growth and lack of competitiveness.

The catalyst for these long-term trends to turning into an outright crisis of a falling currency and rising interest rates on government (and other debt) has frequently been tax cutting Budgets. These only served to suck in imports further, weaken the pound and make government debt unattractive to overseas investors without offering much higher interest rates. This is what happened in both the Barber and Lawson Booms.

We can now add the name Kwarteng to this rogues’ gallery of Tory Chancellors. However, a key difference with his predecessors is that the current Chancellor implemented the enormous giveaways to business and the rich when there was already an old-fashioned balance of payments crisis under way.

This is how SEB characterised the comparison on Twitter.

The basis for the British economy’s repeated balance of payments crises has the same sources as its weak growth, weak productivity and low wages. This is its chronically weak levels of Investment.

There is too the specific factor of Brexit. But it is not simply a case that Brexit has made it harder to export goods to the EU. It is worse than that, as shown in Table 1.

Table 1. UK Trade Balance in Goods with the EU and non-EU Countries, £bn

| EU | Non-EU | |

| Q1 2022 | -30.2 | -31.0 |

| Q1 2021 | -16.9 | -12.7 |

| Q1 2017 | -24.2 | -11.2 |

Source: ONS

The overall deterioration in the trade performance in goods certainly accounts for more than the overall widening of the current account deficit. The trade deficit has widened significantly. And the UK trade balance with the EU between the 1st quarter of 2017 and the same quarter in 2022 has certainly deteriorated, as shown in Table 1.

However, the widening of the trade gap is more pronounced outside the EU. In addition, UK exports to the EU are slightly higher than they were at the beginning of 2022 than in the same period in 2017, £42 billion versus £39 billion.

But trade is not simply about one country selling a food to another. There are incredibly complex cross-border supply chains that operate particularly in advanced manufacturing. The British economy has been a major importer of these semi-finished goods, as well as a major re-exporter (in European terms) of either finished goods or semi-finished ones, with some value added. There has been a surge in imports of these semi-manufactures from outside the EU without any corresponding rise in exports to the same countries. In effect, it appears as if Brexit has cut out Britain from existing supply chains in Europe, and companies based in this country will have had to replace them with more expensive and/or inferior products.

Naturally, this sharp adjustment in Britain’s place in global supply chains will further depress Business Investment. While virtually all major capitalist economies have experienced a pronounced decline in levels of Investment over decades, the downturn in British Investment has been even greater. This has been a chronic malaise, now made acute ever since the outcome of the referendum in 2016.

Chart 2. Investment (Gross Fixed Capital Formation)as a % of GDP in the EU, US and UK since 1970.

Source: World Bank

Why have they done it?

Clearly this government is not primarily concerned with courting popularity, unlike Johnson, Cameron or even Thatcher who lied about their intentions. Nor have they taken much account of the likely response in financial markets, where a falling pound will add to inflation and rising interest rates will deepen the downturn.

As a result, in deepening the structural failings of the British economy they have created additional problems for themselves politically. So, why do it?

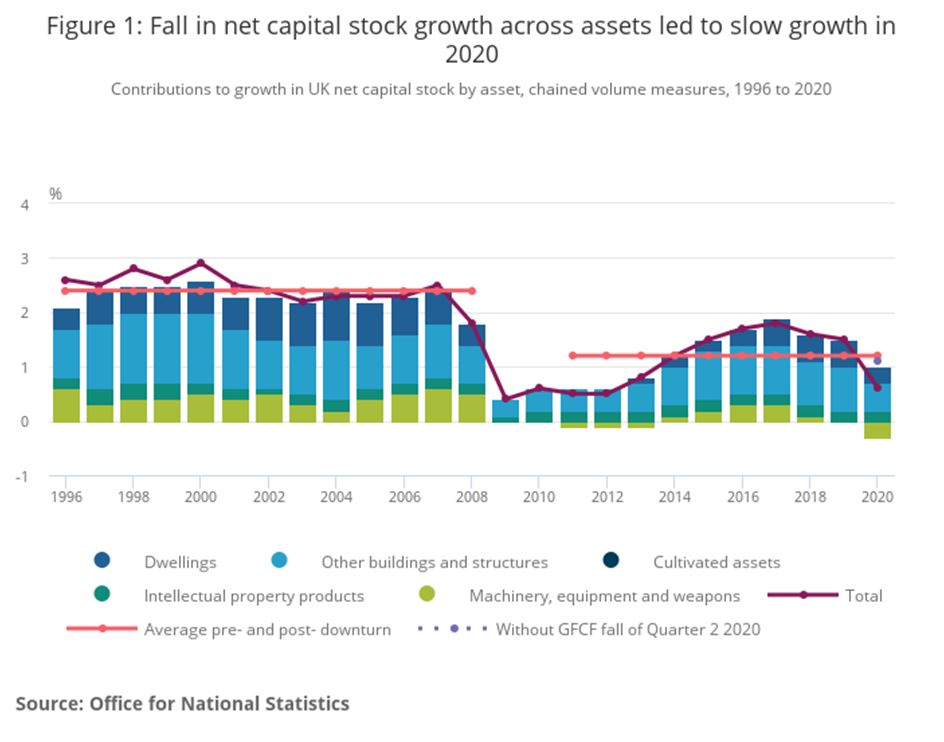

The economic policy is not irrational if the scale and character of the British economic crisis is grasped. A key aspect of this is shown in Chart 3 below.

Chart 3. UK Net Capital Stock and its Components 1996 to 2020.

The net capital stock is the product of Investment in the economy once depreciation and dilapidation are taken into account. It is the means of production. Prior to the Global Financial Crisis in 2007 to 2008 the average annual growth rate for the net capital stock had settled at around 2.4%. In the business cycle since, which is probably ending now, the growth rate of the net capital stock has halved to 1.2%.

It is not coincidental that the net capital stock in both instances is closely related to the real growth rate of the economy over the business cycle, as net investment is the primary determinant of growth.

As we know, Investment has since fallen, led by Business Investment which was 12% lower in 2021 than in 2019. This comes close to an absolute crisis for the British economy and especially for its business sector.

The ‘mini-Budget’ shows that the health of the business sector is clearly the most important priority for this government. The Truss/Kwarteng government differs from its predecessors by stripping way any pretence otherwise. For any government an Investment strike by its business sector would be a matter of grave concern. For this government it is a catastrophe.

Their agenda is to boost the returns to private capital by cutting taxes, cutting wages, deregulation, outsourcing and privatisation. The problem is that this Thatcherite solution does not work. It did not work under Thatcher and will not work by repeating it in much worse conditions.

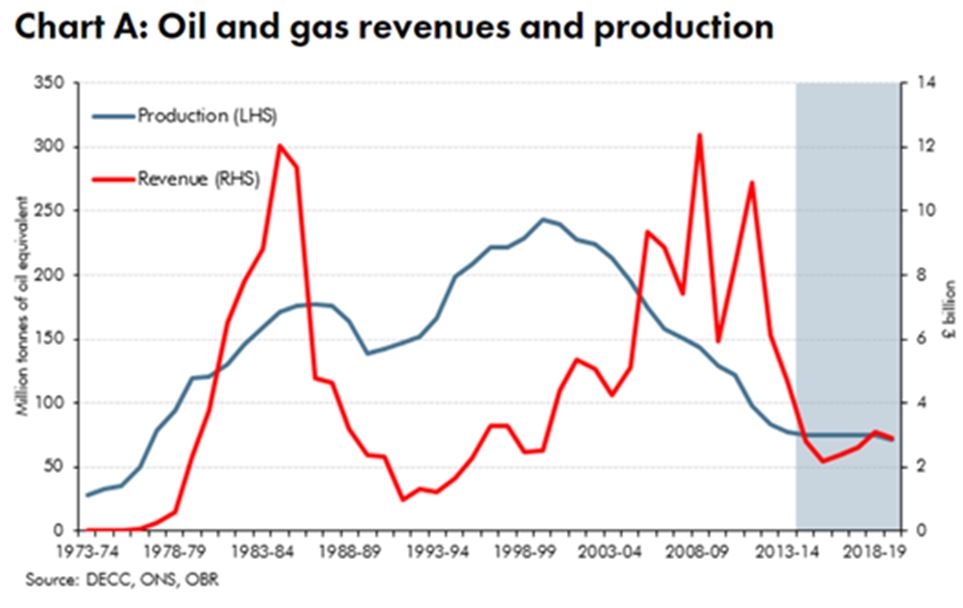

As Chart 4 below shows, Thatcher’s policies benefitted from enormous N Sea oil revenues almost from the moment she entered Number 10 Downing, peaking at 3.4% of GDP in 1984-85.

Chart 4. North Sea Oil Revenues

Source: OBR

This was an enormous windfall. But the policy response was tax cuts and privatisation, even including the main company benefitting directly from the oil bonanza, BP! These tax cuts eventually led to an unsustainable boom (the ‘Lawson boom’) which ended with a crash. But the dominant trends of the Thatcher period were economic slump and mass unemployment. The official unemployment total stayed close to 3 million people for 6 years.

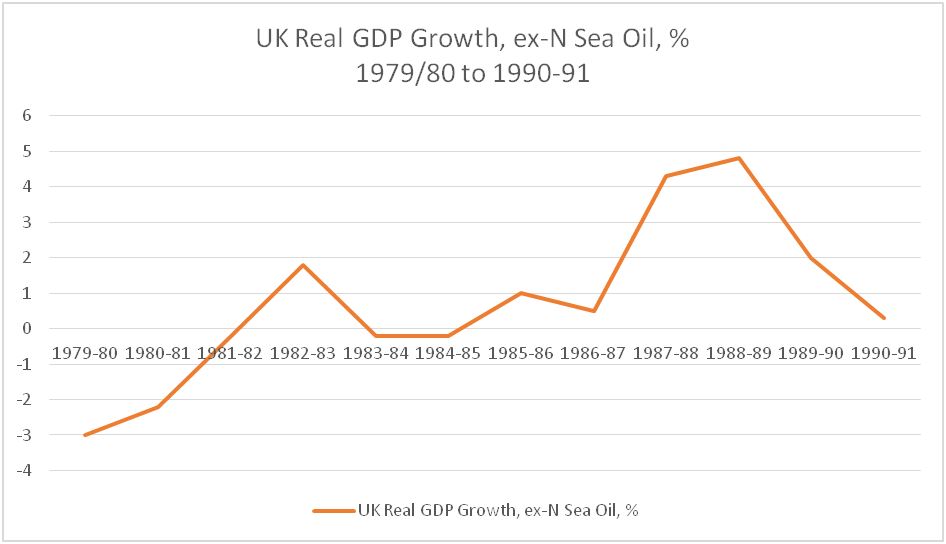

The weakness of the economy is highlighted in the chart below.

Chart 5. UK Real GDP Growth Under Thatcher, excluding North Sea Oil revenues, % change

Source: OBR, ONS data, author’s calculation

Excluding the surge in N Sea oil revenues the economy grew by just 12% over the entire period, making it the weakest period of growth of this length over the entire era since the end of World War II. There was also no net asset creation, as there has been with Norway’s Sovereign Wealth Fund. The revenues were simply frittered away in tax cuts.

These are the policies now being emulated by this government. And it should be stressed that their own, self-made inheritance is far worse on all key economic indicators than Thatcher operated under in 1979.

This government has taken the view that it is impossible to disguise the scale of the attacks that are coming, even with the help of the British media, so they are not going to try.

Instead, they have staked out ground that claims they have the answers to the economic crisis. They will then dare other social forces, most notably the unions, and the opposition, to formulate an alternative. That is the next major challenge.

The article below was originally published here on The Rising Tide blog.

An emergency budget is due on September 23. The new government led by Liz Truss has started as it means to go on. It will borrow £150bn to give to the already engorged energy companies. Meanwhile, the people will pick up the tab.

Under the premiership of Johnson and now Truss, their critics have given far too much weight to issues of competence and style. The issue is not competence or even intelligence but policy.

The class war content of the policies enacted and proposed has been grotesquely downplayed. Or even worse, in the case of Johnson often misrepresented as defying traditional Tory policies of low public spending rather than the reality of unprecedented levels of public expenditure being used to enrich big business and the wealthiest in our society.

Thatcher

The new Chancellor, Kwasi Kwarteng, will be centre stage when he delivers his first budget. His 2015 book, ‘Thatcher’s Trial, Six Months That Defined A Leader’, provides many clues to understanding his politics, and how they will shape his economic policies. The book focuses on the six months from March 1981 budget to Thatcher’s September 14 cabinet reshuffle.

The events Kwarteng selects in the book find an echo today. The new prime minister making her mark; a controversial budget dominated by inflation and a crisis in Ireland. On the other hand, others like the Thatcher purge of the so-called wets in the Tory party has already been done by Johnson, or in the case of the 1981 right-wing SDP split in the Labour Party, has taken the form of a defeat of the left within the party. The other events Kwarteng looks at, like the social rebellions, are probably just around the corner.

The book is more narrative than analysis. But it has a distinct theme: Thatcher as a leader defying the odds and conventional wisdom in a crusade of national renewal. In short, the book is a celebration of right-wing voluntarism.

Kwarteng provides no evidence for national economic success under Thatcher because none exists. But as with Johnson and Truss, the talk of national renewal and unprecedented economic growth is just fodder for the newspapers, the BBC and election-time propaganda.

Monetarism

This week, the Chancellor will echo the PM when he speaks about the importance of growth. Kwarteng and Truss will put forward policies for the few, not the many. They will justify their redistribution of wealth to the rich by claiming that everyone benefits from the bigger national economic cake they say will follow, rather than focus in their view on redistributing more fairly, an increasingly small one.

With no sense of irony, they will decry the economic failure of previous governments, including the Tory ones. They may even imitate Thatcher, who criticised previous Tory leaders like Macmillan and Heath as quasi-socialists for their ‘acceptance’ of the post-war social contract and the welfare state.

They will offer the well past its sell-by-date reheated fare of monetarism as a way to increase economic growth. Unlike Thatcher, who had the Nobel Prize-winning Milton Friedman to add some intellectual gloss to the economics of warfare against the working-class and oppressed, Truss and Kwarteng will be relying on the downmarket versions in the form of the Adam Smith Institute and the TaxPayers’ Alliance who now occupy senior advisory posts to the government.

Chancellor Kwarteng’s mantra will be the same as Thatcher’s. As he puts it, ‘For her, ‘the way to achieve recovery was to ensure that a smaller proportion of the nation’s income went to the government, freeing resources for the private sector where the majority of people worked’.

State investment

But this mantra, as the Socialist Economic Bulletin SEB explained, “is a misreading, as the far higher growth rate in the US and to a lesser extent the UK was in the pre-war and war period itself. The exceptionally strong growth was caused by the state taking control of investment and directing very large increases, in order to wage war. The subsequent ‘Golden Age’ was the gradual deceleration of this war boom.”

Chart 1 SEB

The 1970s

The collapse of the post-war boom in the early seventies brought a combination of a political, economic and social crisis. The question was, as it remains today, in the interests of which class was a solution to be devised.

Edward Heath, [Conservative PM 1970-74], tried and failed to implement his ‘Selsdon Man’ policies of free market competition and attacks on the rights of trade unions. Instead, a united labour movement led by the NUM defeated him.

Heath did try to make the working class pay to resolve the economic crisis with his version of an irreversible shift in power and wealth from labour to capital. But as Heath explained, this was not enough to increase investment and, with it, growth.

In 1973 he complained to the Institute of Directors, ‘The curse of British industry is that it has never anticipated demand. When we came in we were told there weren’t sufficient inducements to invest. So we provided the inducements. Then we were told people were scared of balance of payments difficulties leading to stop-go. So we floated the pound. Then we were told of fears of inflation and now we’re dealing with that. And still you aren’t investing enough’.

Thatcher rose to power in the Tory party on the back of Heath’s two electoral defeats in 1974. Like Heath, she was also committed to growth.

Her strategy – embraced by Truss and Kwarteng – is highlighted by the new Chancellor in a reference he makes to an anonymous journalist writing in the Economist: ‘the government was elected in 1979 above all else to roll back the frontiers of the public sector, to leave resources free for private-sector expansion. The key to this strategy lay in reducing public spending and borrowing, to bring down taxes and interest rates.’ Critical to this was defeating the organised labour movement by set-piece confrontations backed by anti-trade union laws designed to make strikes as ineffectual as possible.

Powellism

In his book ’From Labourism to Thatcherism’, Colin Leys also highlighted another strategy proposed inside the Conservative Party by Enoch Powell. A strategy implemented by Boris Johnson, to be continued by Truss and Kwarteng. “The later sixties saw ‘a more fundamental right-wing movement than Heath’s ‘competition policy’ gaining ground inside the Conservative Party. Enoch Powell, shadow minister for health, shared his enthusiasm for the market for cutting back the state, but went much farther in calling for denationalisation, an end to state intervention in industrial disputes and strict control of the money supply to control inflation. He also combined this with a nationalist campaign against entry into the EEC and a racist campaign against immigrants.”

Powell’s strategy was carried out by Johnson. Truss will take Powell’s strategy many steps further. That will not be about her character or competence but her design and purpose. It will be about the times and the demands of the capitalist class she is the political leader for the moment. Already, there is talk in the papers that the government is reviewing regulations on the 48-hour week and holiday pay. That is just the beginning. On her watch, the vicious racism will accelerate. The Tory press is already crowing that Truss will stop all attempts by those fleeing war to cross the English Channel.

In short, each attempt by the Tories since 1970 to reverse Britain’s economic decline has become more extreme.

Tory austerity

Twelve years of Tory austerity, an unprecedented wage fall, and a surge in the wealth of the 1% have failed to foster growth. The critical element to growth, investment, has not been revived. On the contrary, Britain faces an investment strike by capital as workers have not been squeezed enough to restore the level of profits it demands before investing.

The economics espoused by Truss and Kwarteng is like the bloodletters approach that hastened Charles II’s demise – a decline in the patient’s condition has not led to alternative remedies being pursued. The answer – then and now – is that the bloodletting did not go far enough.

Brexit and Covid

Brexit was both an application of and a facilitator for the new Powellism of Johnson and Truss. Covid has set the template for transferring vast amounts of public money to private corporations. As a result, the NHS continues to be deliberately undermined, and the take-up of private health treatment is surging, often with reluctant patients. Conservative think tanks openly talk about using inflation to reduce the real level of public spending and wipe out some areas of state provision altogether.

Slash and burn

Truss may not have much time as PM, but we should not assume she won’t use it to great effect. Her policy will be one of slash and burn. She will try to Americanise as much as she can of not only the British economy but also British politics. The latter will see a ramping up of racism, bigotry and attacks on women’s rights. She will hope that an incoming Labour government will be reluctant to undo her ‘achievements’, particularly on privatisation and attacks on trade union rights. She will also hope that Keir Starmer will be what Tony Blair was to Thatcher, her ‘greatest achievement’.

The labour movement

Truss and Kwarteng have signalled their desire to achieve 2.5% GDP growth in the British economy in advance of the budget. Anything approaching that growth rate can only be achieved in one of two ways – by a massive increase in public investment as proposed by Jeremy Corbyn and John McDonnell i.e. Corbynomics, or by unleashing an even more vicious attack on the working class share of the economy. The latter would cause much more devastation than the austerity assault suffered since 2010.

It would be of great benefit for our side in the class struggle to emulate Kwarteng, the political historian, in one way – learn from the 1970s. A united labour movement brought down a Tory government in 1974 and replaced it with a Labour one. It can do so again. But a Labour Party that repeats the failures of the Wilson and Callaghan governments will lead to an even bigger disaster for the working class and the oppressed than in 1979.

‘Thatcher’s Trial, Six Months That Defined A Leader” by Kwasi Kwarteng, 2015

By Michael Burke

There are widespread hopes that the surge in prices may be coming to a halt. Yet there is little evidence to support them. There is very little to suggest the main driving forces of global inflation are receding. This can be shown factually in a few graphics.

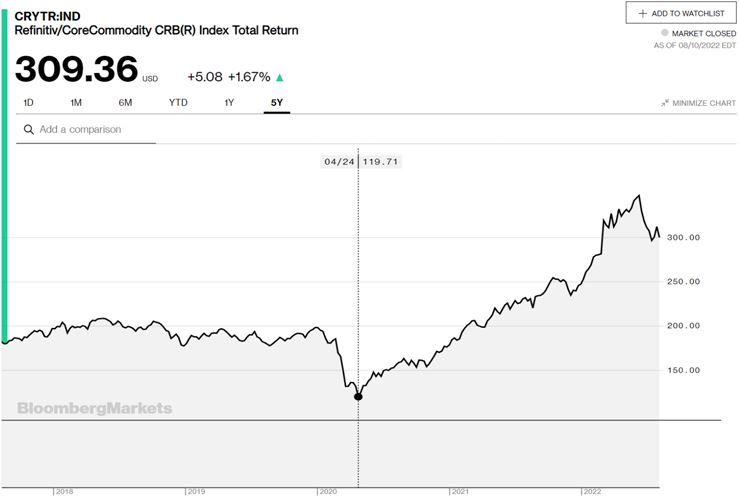

The main causes of inflation have nothing to do with the war in Ukraine. The chart below shows an index of globally traded commodities. It is clear that the surge in prices began in April 2020, while the current military conflict in Ukraine began on February 24 this year.

Chart 1. CRB Commodities’ Index, last 5 year

Source: Bloomberg

SEB has previously argued that the impulse for the inflationary wave was provided by an extraordinarily reckless US economic policy. This combined an unprecedented growth in money supply with an equally unprecedented rise in US government Consumption. This was also timed for the synchronised exit from lockdown that was taking place in early 2020 in the main Western economies. It also came after a prolonged period of low or falling Investment in those same economies.

This was almost a textbook case of causing inflation by printing money and stimulating Consumption without anything remotely like a corresponding rise in Investment. As in the textbooks, this led to inflation.

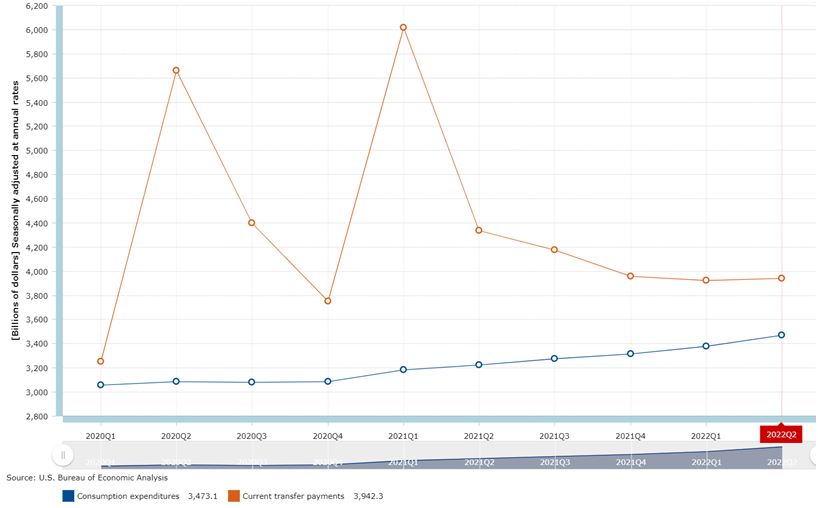

The first of these factors can be seen in Chart 2 below, which shows the main components of US Government Consumption Expenditures from the beginning of 2020 onwards.

Chart 2. US Government Consumption Expenditures, $bn

Source: BEA

Before the policy began, the combined US government outlays on Consumption Expenditures and Current Transfers totalled $6.3 trillion. The largest inflationary impulse came from an increase in this total the 1st quarter of when the combined total of outlays was $9.2 trillion. This level of spending has subsequently receded, but at $7.4 trillion remains way above the starting point at the beginning of 2020.

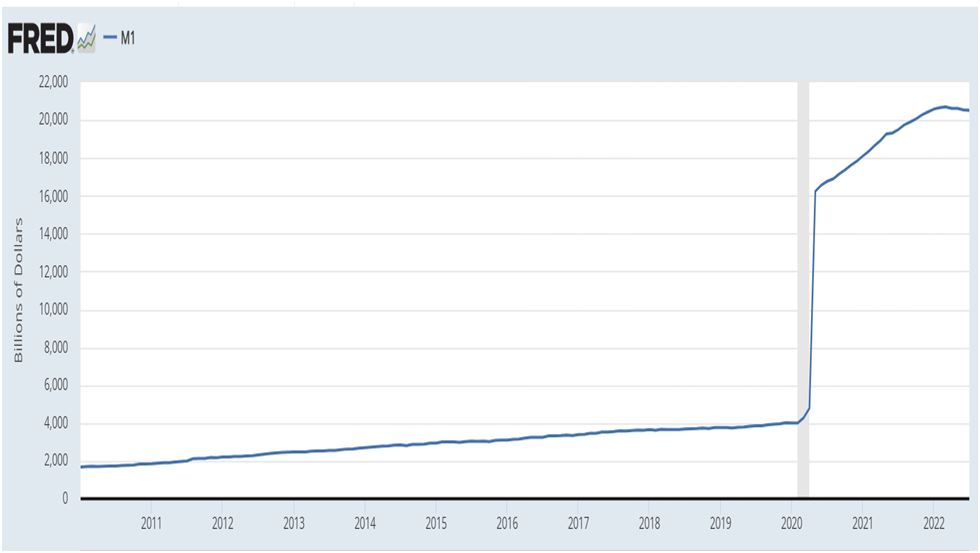

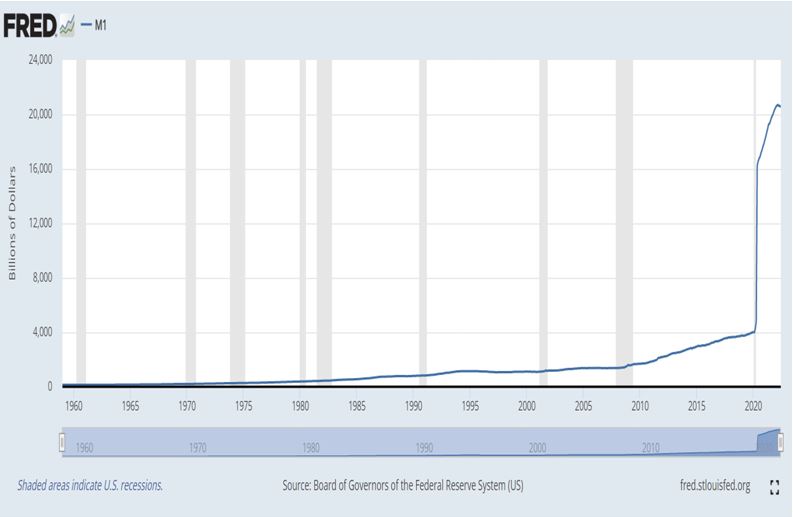

The inflationary trend is reinforced by the exceptional growth in US money supply, as shown in the chart below. The exceptional pace of growth in the supply of money can be illustrated by the point that it took 10 years for US M1 money supply to double from $2 trillion to $4 trillion. But M1 money supply rose from $4 trillion in February 2020 to $20.7 trillion in March 2022, over 5 times larger in little more than 2 years.

Chart 3. US M1 money supply, US$ billions

Source: FRED

The level of money supply has since edged lower, down to $20.5 trillion. It is probably not prudent to withdraw this money at the same reckless pace it was created. But the consequence of such exceptionally high level of money supply circulating in the economy will be to reinforce inflationary pressures for some time to come.

As already noted, the same note of caution applies to US Government Current Expenditures. They have fallen back but remain at a level likely to support inflation rather than suppress it.

Crucially, none of this has huge stimulus to spending has led to increase in Investment. Increasing the means of production through Investment is the only method for raising the level of output up to the inflated levels of government Consumption and money supply growth.

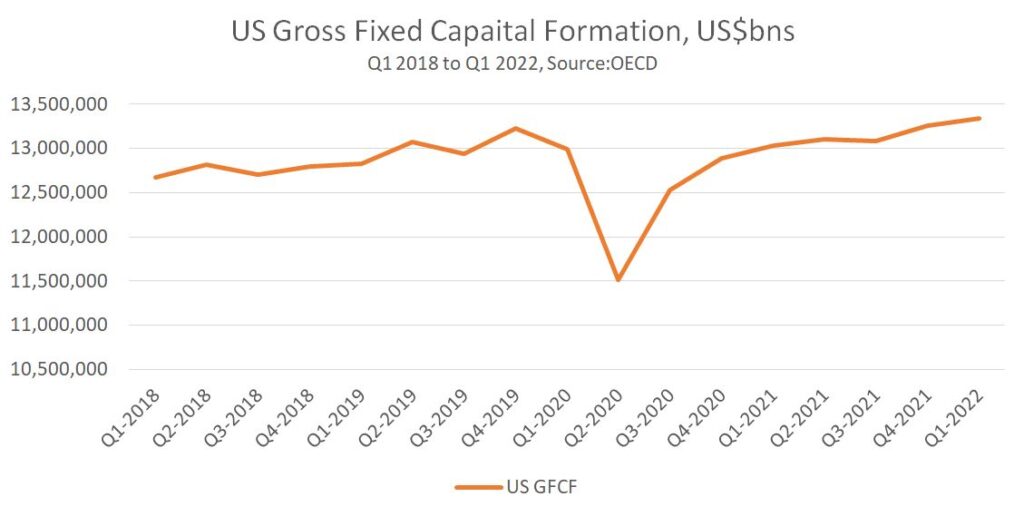

As shown in Chart 4 below, over the 2-year period from the 1st quarter of 2020 to the 1st quarter of 2022, the total level of Investment (Gross Fixed Capital Investment, GFCF) has risen by just 2.6%. There has been almost no increase over that period in the means of production (especially when the rate of depreciation is considered). As the consequences of this completely negligent US economic policy are euphemistically described as ‘bottlenecks’, this highlights there is limited spare capacity slack in the economy to prevent prices rising further.

Chart 4. US Gross Fixed Capital Formation, US$ billions, 1st Quarter 2018 to 1st Quarter 2022

Source: OECD

Finally, it is important to note the impact of central bank monetary policy, as interest rates are generally being increased in the Western economies in a misguided attempt to dampen inflation. Because those price pressures are caused by an economic policy which has created a huge imbalance between supply and demand, interest rate rises are an attempt to correct that imbalance by suppressing Consumption.

The central bankers explicitly state they aim to suppress wage growth below inflation. This will mean adding to the risks of slump and amount to a redistribution of wealth and incomes from workers and the poor to the profitable and to the asset-rich.

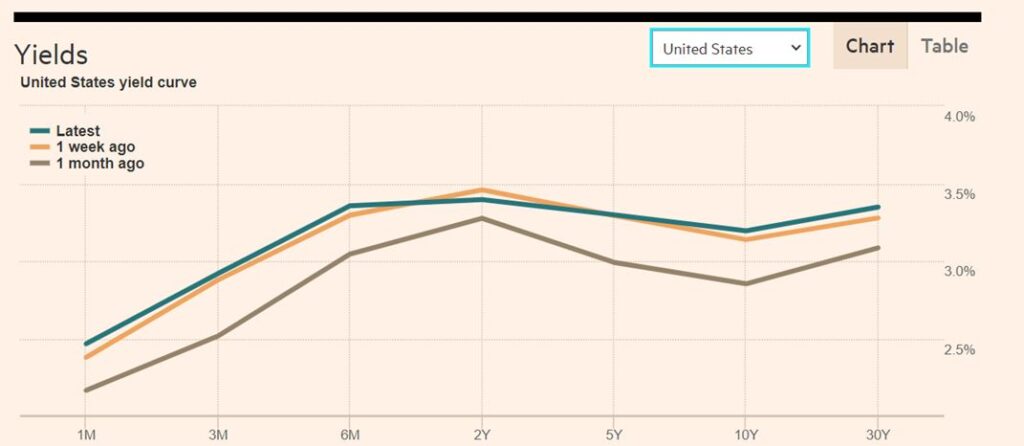

In addition, for those with access to credit, real interest rates remain extraordinarily low. Chart 5 below shows the US government yield curve, which is the interest rate payable on US government bonds from 1 month out to debt that matures in 30 years.

One of the key benefits for the US of the US Dollar dominance in global trade is mirrored in global financial markets, with the US setting the floor on global interest rates for most countries (the main exception being Japan).

Chart 5.

Source: FT

There is no part of the US government yield curve where interest rates are currently more than 3.5%. Yet US CPI inflation is currently 8.5%, meaning that interest rates in real terms are -5%. For anyone who can borrow at interest rates close to these levels in real terms, credit is exceptionally cheap.

However, this is available only to those with the best credit ratings, big businesses and the very rich. In practical terms, while most of the population is suffering a sharp fall in real incomes, the financial markets operate in such a way that only widens class divides and deepens the upwards redistribution of wealth and incomes that is currently taking place.

Yet the best credit ratings of all, and the cheapest borrowing costs still belong to government. The Western governments could slow and then reverse the surge in inflation with a massive level of Investment in the productive economy. The imbalances between Investment and Consumption could be ended by a very large increase in Investment, rather than suppressing Consumption.

But that would significantly increase the role of the State in the productive economy and lessen the dominance of the private sector. This is not at all the current policy programme, and is in fact its opposite.

By Michael Burke

The British economic crisis combines all the elements of the world economic turmoil, but in a uniquely negative way. As a result, Britain is set to have the most severe economic dislocation of all the advanced industrialised economies, which is driven by the string of policy choices made by this and preceding governments. The task for socialists is to analyse the cause of the crisis and to plot the alternative.

To begin with the analysis, it is completely false to claim that the global surge in prices is a response to the Russian invasion of Ukraine. Chart 1 below shows the trend in oil price (Brent Crude) over the last 3 years.

The surge in the oil price began in April 2020. The military conflict began on February 24, 2022. The oil price jumped, from effectively $100/bbl on the day of the invasion to over $130/bbl but is now close to $95/bbl. There is no longer any price premium on oil arising from the war.

Chart 1. Brent Crude oil price, last 3 years

Source: FT

Instead, the current elevated level of the oil price began over two years ago and for entirely different reasons than the war. Although oil is perhaps the single most important commodity in relation to prices in general, this pattern of the surge in prices taking place long before the war is evident for commodities in general, the surge in prices beginning in April 2020, as shown in Chart 2 below.

Chart 2. CRB Commodities Index

Source; Bloomberg

What happened in early 2020 is that the major Western economies were coming out of lockdown, which was always going to be a period of rising Consumption. But as shown elsewhere it was precisely at this point that the Biden Administration chose to launch the biggest increase in Consumption spending in US history, far greater than anything ever seen, even including world wars.

At the very same time, the US Federal Reserve Bank decided to embark on the largest pace of money creation ever seen in US history, as shown in Chart 3. The narrow measure of money supply rose rapidly in February 2020 from $4 trillion to over $20 trillion.

Chart 3. US M1 money supply total

Source: US Federal Reserve Data (FRED)

Whatever the motivation for these unprecedented steps, in early 2020 there was both an extraordinarily sharp increase in the level of money supply in the US economy and a government-sponsored increase in Consumption, without any increase in Investment.

It is not necessary to be a monetarist to accept that the combination of vastly greater amounts of money in the economy, plus increased Consumption demand without any commensurate increase in the supply of goods via Investment was certain to push prices higher.

This is exactly what happened. Furthermore, because of the weight of the US in the global economy and especially because most globally traded commodities are denominated in US Dollars, then this inevitable surge in prices was bound to have a global impact. This is the source of the current global surge in prices, the period we are still in.

It is also this mismatch between Consumption and the availability of money on the one hand, and the supply of goods in the absence of any Investment which has been dubbed the ‘supply-side’ crisis.

The next part of this piece examines the distortion of economic reality in the economic theory of monetarism. Many readers may want to skip this section and go straight to the section dealing with the British crisis. But the grain of truth monetarist theory contains might be of interest to some.

Mendacious monetarism

The theory of monetarism is not really a theory at all. It is simply an accounting identity. The classic monetarist formula is as follows:

MV = PQ

where M is the level of money supply in the economy

V is the velocity (the rate of transactions over a certain time period)

P is the price of goods and services

Q is the quantity of goods and services.

The logic of the equation is not at issue. Yet the supporters of monetarism claim that their insight held the key to the control of inflation. In the dictum of its most famous advocate Milton Friedman, “inflation is always and everywhere a monetary phenomenon”.

Their policy asserted that if M is controlled (and they held endless and inconclusive debates on which measure of M that should be) then P could be controlled. So, for many years the central banks of the advanced industrialised economies spent all their efforts on controlling the supply of money M in order to control the level of prices P.

But the essential dishonesty of monetarism is that the equation contains 4 variables, not two. In addition to M and P there is also V and Q. And the essence of variables is that they vary.

To take an obvious example, suppose Q falls and there are fewer goods and services in the economy, but P is rising. This is the current situation, what is known as ‘stagflation’. But if inflation (P) is rising by 9% and that is offset by falling Q, as output of goods and services is falling way below trend, is the role of monetary policy to boost output or to curb prices? And what about V, which is currently falling?

The claims made for monetarism are clearly false because it treats a multi-variable equation as simple mathematics.

However, it as an accounting identity that rests on a truism. If money in the economy is expanding at a rate without a comparable increase in the quantity of goods available, prices will rise.

The uniquely grim British economy

The British government and its supporters like to claim that that the economic crisis is because of international factors. This is correct. Although they cling to the false assertions about the war in Ukraine rather than the reality of a completely reckless US economic policy as the cause.

But the government has made a global economic crisis much worse through the effects of its own policies. Britain’s stagflation will be far worse than comparable countries.

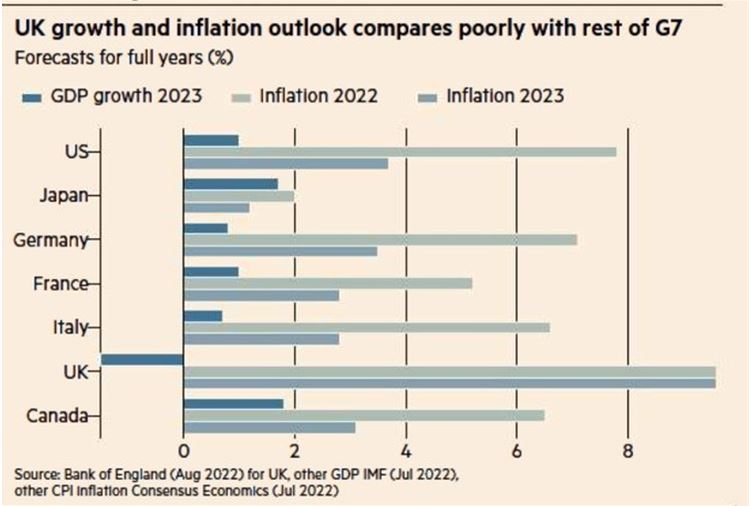

This is shown in Chart 4 below, where the projected levels of growth and inflation for the British economy are far worse than in the rest of the G7.

Chart 4. UK, G7 countries outlook for GDP growth and inflation

Source: FT

SEB has previously shown that exceptionally weak business investment has fallen even further since the Brexit referendum. Exports have also fallen, while the priority of protecting business in the pandemic has left the economy permanently scarred and shrunk the labour force. Now the Bank of England is issuing dire forecasts of 13% inflation, much higher unemployment and a 3-year slump.

None of these policy choices are accidental or arises from missteps. These are a conscious political programme to deal with the structural economic weakness of the British economy, which has become acute. As the Tory leadership debate shows, there is a consensus around main elements of this programme.

All of the impositions of lower pay, the cuts to benefits and pensions, the defunding of public services and the attempts to smash the unions are part of the same project. They are also much easier to implement in real terms when inflation is high, than to achieve the same effect by nominal cuts.

It is popularly known as making workers pay for the crisis, which is increasing the rate of exploitation of labour, to boost the profits of capital. Attacks on government spending (the ‘small state’ of the Tory party debate) are to facilitate tax transfers to big business and the rich, accelerating the programme that has been in place since 2010.

Responding to the crisis

A crisis caused by grossly excessive money creation in the US and stoking Consumption cannot be addressed by further money creation or stimulus to Consumption.

Instead, the main planks of a programme to address the ‘supply-side’ crisis require an increase in the factors of production, both labour and capital (labour shortages, where pay is too low to cover outlays is a also a key feature of the current crisis in all the advanced industrialised economies, made worse in Britain by Brexit). In addition, measures must be taken to lower prices.

The most immediate and pressing need is to lower prices. The energy price cap could do what it claims, by spectacularly fails, which is impose a cap on prices. Instead, the cap is really a cushion for profits, with the regulator ensuring that any supplies conforming to its rules makes very substantial profits.

The cap should be set at a pre-crisis tariff, so that average annual bills return close to £1,000 rather than over £4,000 which is currently projected. Any supplier which goes under should be taken over by the State, with no compensation for shareholders.

In addition, all sorts of prices that are administered by government-appointed regulators, such as water, mail, transport and others should be frozen at pre-crisis levels, with the same policy applied on renationalisation. The reasonable expectation would be that these policies would lead to the State rapidly becoming a major owner of industry once more.

At the same time, strong measures are required to tackle the rise in poverty, including for those in work, on benefits or relying on the State pension. Inflation-matching rises are required for all grades in the public sector earning £52,000 or below (twice the average full-time wage). This will help set a ‘going rate’ in the private sector as well. The minimum wage should be raised to the inflation-adjusted living wage.

There must also be widespread measures to increase labour participation rates, including a programme of retraining and proper apprenticeships. All taxes on learning must be abolished, so student loans must go. A further specific measure is to freeze all rents.

Yet none of this is affordable without a dramatic and large increase investment. There would be a risk of government finances collapsing or a further plunge in the pound, driving up inflation even further.

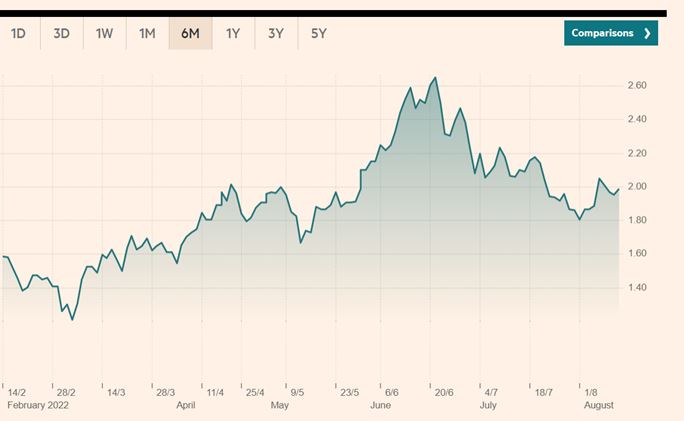

However, the mechanism for achieving this is readily at hand. No sensible Chancellor or Finance Minister, even in the neoliberal period has ever sought to limit government borrowing for investment. Instead, they have simply refused to carry it out. Yet with inflation currently at 9% and poised to go into double digits, the interest rate on government bonds is massively below that level. In effect, investors are willing to pay (in real terms) to hold government debt. The yield on UK government debt (gilts) is still below 2%, as shown in Chart 5 below.

Chart 5. UK Government 10-year bond yields, %

Source: FT

The government purchase of almost any viable asset will enjoy huge returns as a result, including the nationalisation of major companies. But, of course very large-scale investment is required in the real economy, to make the transition to renewables, electrify and expand the public transport network, retrofit homes to save energy and bills, to fix our broken waterways and modernise and upgrade the entire rail network.

Over the medium-term structural issues such as the housing shortage, the lack of R&D and the private chaos of our transport delivery networks can be addressed through the investments of a state-owned National Investment Bank, which have operated successfully in other countries for decades. Taxes on big business, especially on penalising share buybacks and dividends can be used to supplement borrowed funds.

The opposite of increasing the rate of exploitation of labour is to increase the level of productivity through Investment, and to ensure that the working class and society as a whole are the chief beneficiaries of that.

Of course, under the current political configuration none of this seems at all likely. But that does not mean it is impossible. As well as analysing the current crisis and developing alternatives, a key task of socialists is to broaden support for ideas such as these so that when the opportunity comes there is widespread support for clear-sighted policies.

By Tom O’Leary

After 12 years of austerity it is a significant moment when groups of workers have decided to resist further cuts in real wages, as well as worse terms and conditions. All of these impositions are designed to boost profits. Even in the public sector the excuse that ‘there is no money left’ serves to obscure the fact that the government is trying to set an economy-wide ‘going rate’ below inflation, to the benefit of private shareholders, including Tory donors.

Naturally, all socialists support the striking rail workers and any others who enter the fray (including the striking barristers, who are vital to maintaining legal aid). But it is important to note at the same time the difficulty presented by another altogether different strike that has been taking place in the British economy – the investment strike by British companies.

This strike is decisive in determining growth and prosperity. Breaking it must be a central objective of socialist economic policy.

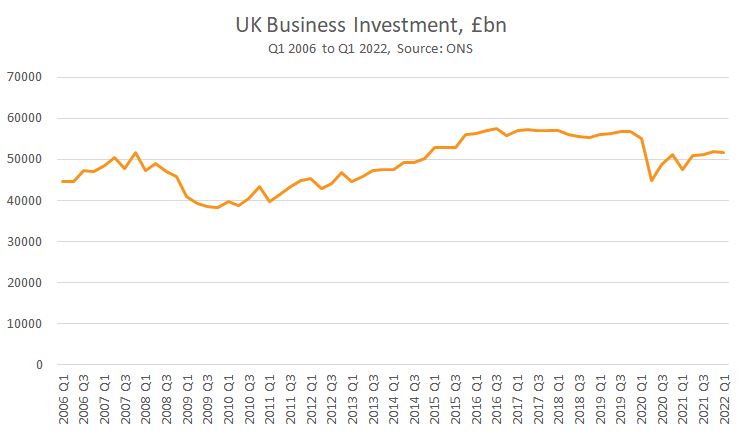

The scale and length of this strike is shown in Chart 1 below. In effect there has been a 15-year long refusal to invest by business since the Global Financial Crisis of 2007-08. The level of business investment peaked at £51.6 billion in the 4th quarter of 2007. In the 1st quarter of 2022 it was still lower by around £50 million.

Chart 1. UK Business Investment 2006 to 1st Quarter 2022

Over the same period Business Investment has fallen as a proportion of GDP. Even though the British economy has crawled along at a snail’s pace of approximately 0.9% on average per annum over the last 15 years, there has still been a sharp decline in the proportion of national income devoted to Business Investment.

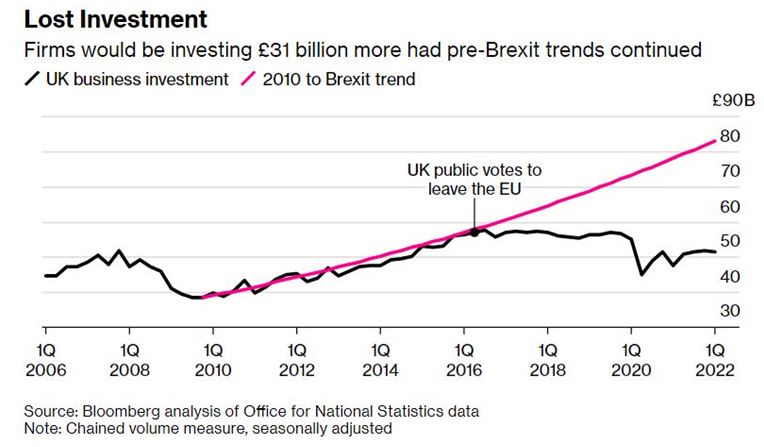

In the 4th quarter of 2007 it amounted to 10.6% of GDP, but is now just 9.1%. As Chart 2 shows, much of the recent trend is attributable to Brexit. As Adam Smith pointed out in The Wealth of Nations, the efficiency of all investment is partly determined by the size of market. Brexit reduced the size of the market that the majority of larger British firms were operating in. Reducing the efficiency or expected return on investment tends to deter it, as shown in the chart. Therefore, this may be a lasting, structural effect.

Chart 2 UK Business Investment pre- and post-Brexit, £bn

Source: Bloomberg

But, as previously shown, this weakness was already in place from 2007 onwards, and has become sharply worse from 2016 onwards.

Why Investment matters

All goods and services can only be consumed if they are first produced. The two most important factors in production are labour and capital. Labour is the most important of these, but cannot by itself increase production and increase prosperity without working harder or longer. But an increase in capital, or an increase in the means of production can lift output. While both may require only one person to operate it, a mechanical digger has greater productive capacity than a shovel.

An increase in the means of production can increase prosperity. Investment either maintains or increases the means of production. Raising the level of Investment can therefore increase the means of production. In a capitalist country like Britain that overwhelmingly means Business Investment, which bears a decisive role in future prosperity, or lack of it.

But this is precisely what has been lacking. The miniscule increase in GDP in this country over the last 15 years has largely been driven by population growth (more workers) and greater exploitation (longer or unpaid hours).

Most of the real GDP growth over the period is accounted for by the increase in the number of workers, up 10.8% since 2007. Investment growth has been absent. It is extremely difficult to raise living standards if there is no growth of Investment.

Instead, some companies are now riding the wave of global inflation to increase prices and profits, while keep a lid on pay. As prices have surged this increase in profit margins by some firms has led to broad misery for the mass of the population, whose incomes from work, or benefits or pensions have fallen way behind the rise in prices.

Worse performance

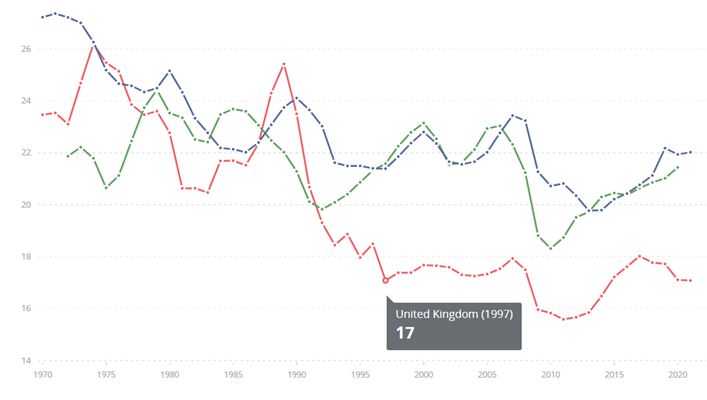

It is also true that most of the leading Western economies have also been experiencing a prolonged downturn in the level of Investment (or GFCF, Gross Fixed Capital Formation). Chart 3 below shows the level of total GFCF (both private and public) as a proportion of GDP.

In the European Union and in the US there has been a significant slowdown, which largely accounts for the marked deceleration in GDP growth itself. These are shown in the blue and green lines respectively and are currently 22% and 21% of GDP.

But total GFCF in the British economy has been considerably below their levels for some time, beginning in 1992. This coincided with the British Pound crashing out of the Exchange Rate Mechanism in September of that year, which its proponents said would lead to greater economic freedom and a surge in investment.

The opposite has been the case. GFCF in Britain has fallen back to 17% of GDP once more, which will largely determine slower growth than both the EU and US in the next period.

Chart 3. GFCF in the EU, US and UK as a % of GDP, 1970 to 2021

Source: World Bank Key: EU blue line, US green line

Economic policy

Currently, this is why the current strike wave is not only fully justified but is crucial in reversing these trends. It is important for far broader layers of the population than just the rail workers and others that they are successful, going way beyond the workers directly in industrial disputes themselves.

Yet this raises too the question of economic policy as a whole. Suppose some disputes are successful, or others less so, or even defeated. Only those workers who win will be cushioned against price rises and possibly only to some extent. And those on benefits or pensions will gain nothing unless a change in government policy can be forced. Broad misery will increase without a change of economic policy.

Over the medium-term, the stagnation of the British economy means it is incapable of sustained improvements in living standards. Without an increase in the productive capacity of the economy, even heroic efforts to wrest the profits from companies will eventually reach a dead-end, and even anything close to that would be fiercely resisted by the state, as those who remember the miners’ strike can testify.

So, in addition to extremely important industrial disputes, the working class must think for itself. Acting in its own interests, it can lead the economy and society out of the current morass. It is the only class that can.

This means adopting policies which re-order economic activity to produce broad and rising prosperity for the overwhelming majority. It means preventing profits being off-shored in tax havens, or paid as ‘special dividends’ to shareholders, or to finance enormous remuneration for executives and their luxury consumption. It means the State increasingly directing investment, through nationalisation, a state investment bank, and changing the entire tax regime to penalise dividends and excess pay, supporting private investment.

The value generated by labour needs to be used to restore living standards for the working class and the poor as a whole, and with the remaining portion increasingly directed towards productive investment, beginning with renewable energy as well as sectors such as public transport, education, green affordable housing and others.

The immediate cost of living crisis is driven by the slump in the purchasing power of labour – prices of goods have soared while pay and other ordinary incomes have stagnated. To lower the price of goods means they need to become more plentiful – increasing the capacity to produce them through investment. The shortages of labour that have been caused by reduced pay can be reversed by increasing pay.

Victory for striking workers, and generalising their disputes against austerity policies are now decisive. At the same, the Business Investment strike must be broken for any realistic possibility of a sustained rise in living standards.

By Paul Atkin

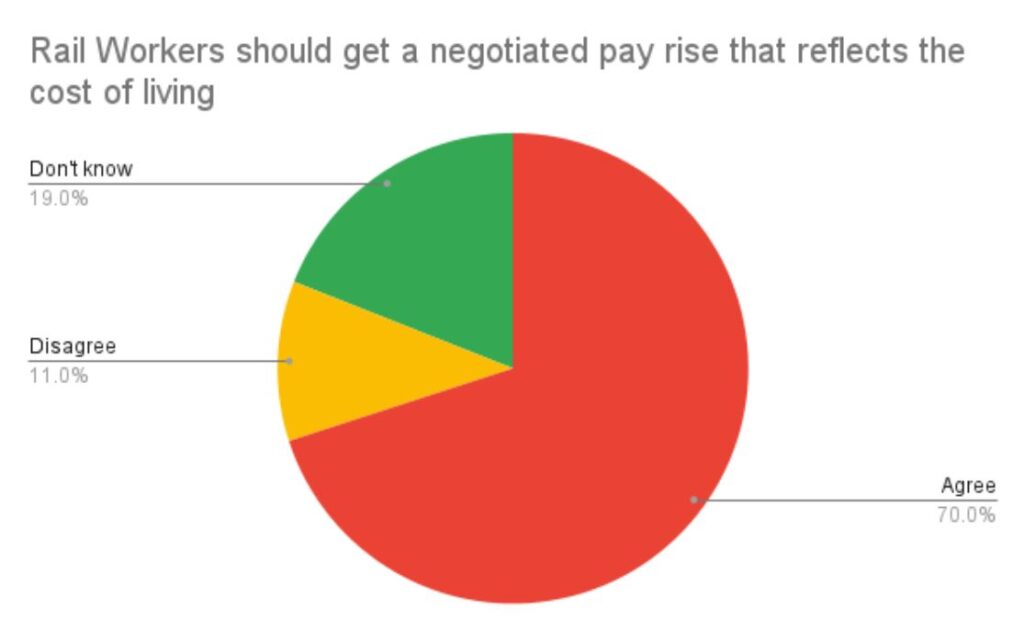

Government attempts to divide the rail workers from others are falling flat. An independent poll by Opinium shows strong public support for the workers’ case.

On pay, there is overwhelming support for rail workers to get a pay rise that reflects the increase in the cost of living. This is an interest we all have in common and its becoming increasingly plain that the government does not agree. They now explicitly state that wage claims should be BELOW the rate of inflation. This is the death knell for any claim that they want to “level up”, or believe in a “high wage economy”.

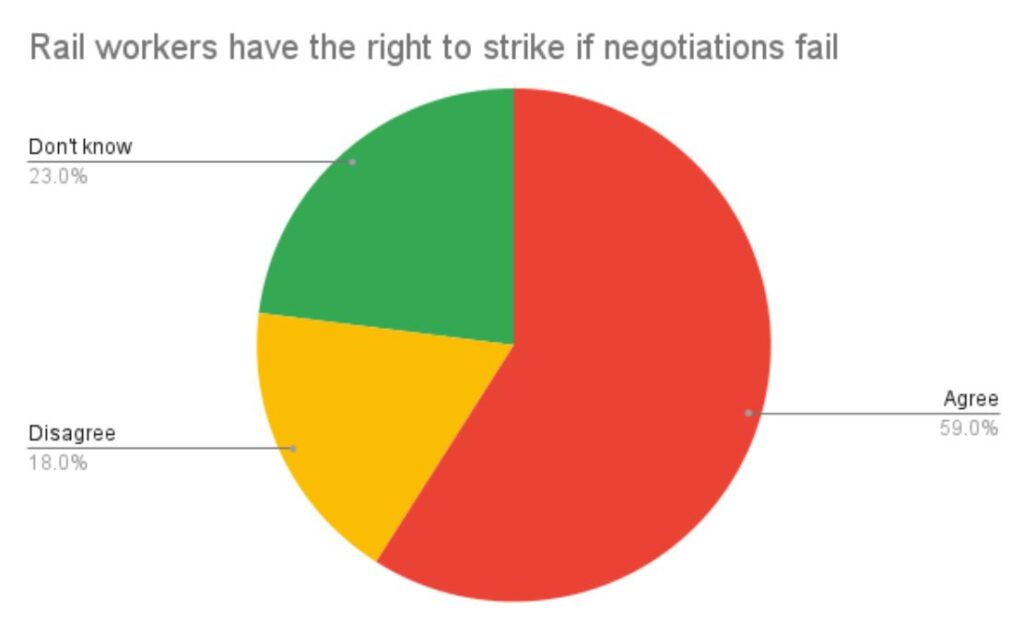

Three out of five support the right to go on strike if negotiations fail. Government sabre rattling about restricting the right to strike is not cutting with the grain.

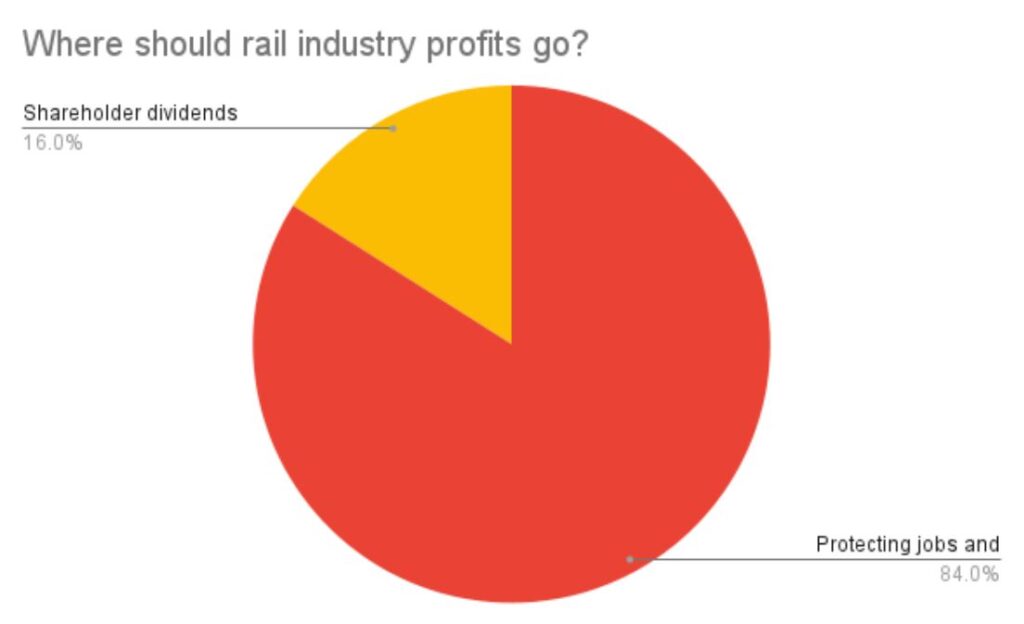

The weakest part of the government’s case is their belief in privatisation and the sacrosanct character of profits and dividends, with overwhelming support for profits from rail services to be reinvested in protecting jobs and improving services. This reflects a growing awareness that the share of the economy being taken by owners of capital is rocketing at a time that the rest of us are being squeezed until our pips squeak.

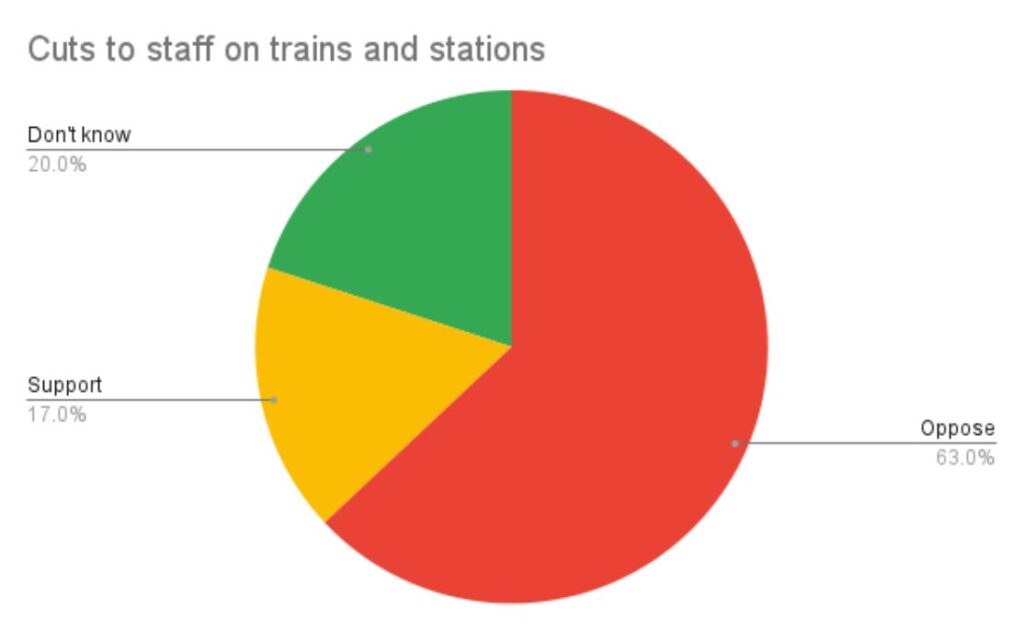

This takes a specific form in large majorities opposing cuts to jobs on trains and stations.

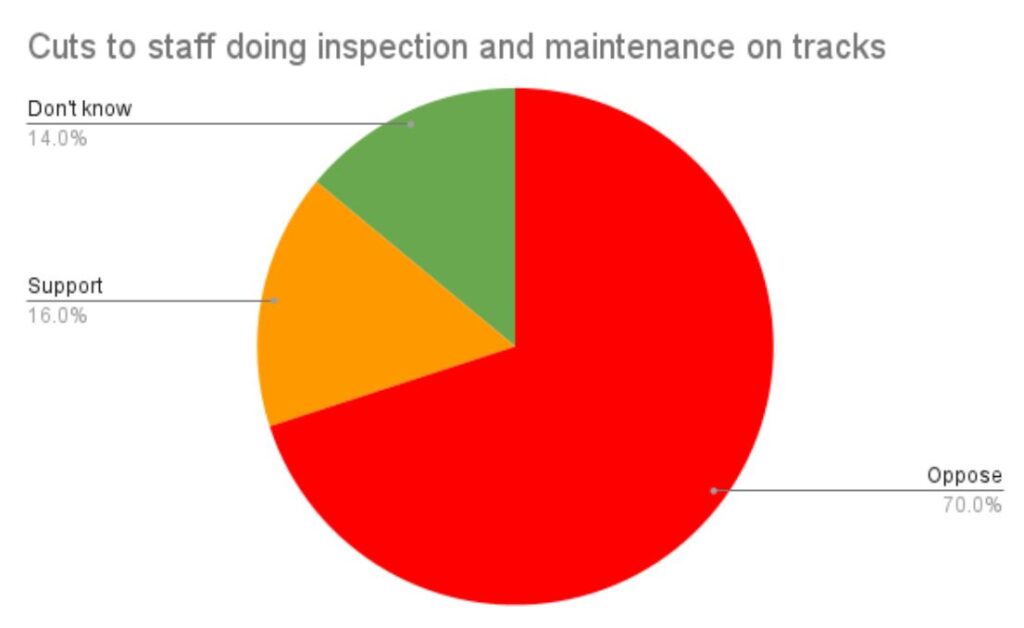

And even more opposing cuts to staff inspecting and maintaining safety on the tracks.

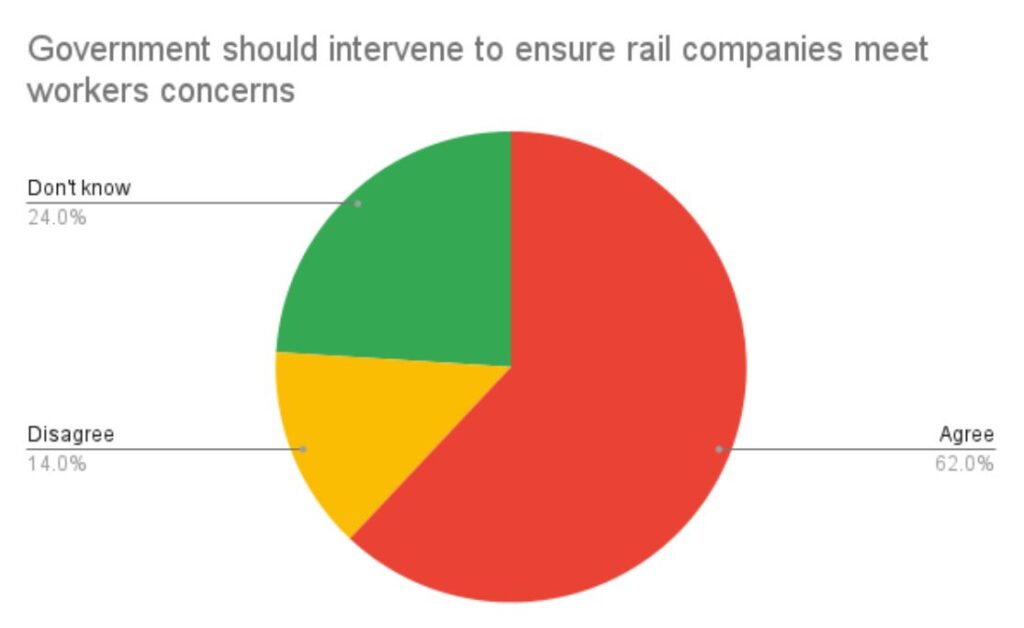

Given that the government is very evidently intervening to make sure that the rail companies do NOT meet the concerns of the workers, they are doing the opposite of what the public wants them to do.

Labour should take note. We are heading into a summer and autumn in which the rising costs of food and energy are propelling workers to turn to their unions to try to stop themselves being forced under. This affects all of us. Most of the public support the workers taking action. If Labour front benchers give “a categorical no” to support for that action, as David Lammy did for airline workers in UNITE and GMB on Sunday, the party will be acting as a human shield for the government (and giving it a lifeline).

See you on a picket line some time soon.

The above article was originally published here on Urban ramblings.

By Paul Atkin

As revealed in this Oxfam Report, the poorest 50% and middle 40% of the global population have a minimal or declining carbon footprint. The top 10%, and even more the top 1%, already have carbon footprints that are unviable and are increasing so fast that they will have bust us through the 1.5C limit on their own by 2030.

The top 10% are people who are on more than £125,000 a year. Most of them live in the Global North, but are a minority even here. The working class in the Global North, is overwhelmingly in the middle 40%.

The strategy of the ruling class in the Global North is primarily to sustain their own wealth and power.

What that means is an immediate future dominated, not by win-win global cooperation to solve our problems and build a sustainable society, but by wars and crises that make doing so ever more difficult. Campaigning against these is an urgent priority for anyone committed to Just Transition.

A strategic challenge for the working class in the Global North is therefore recognising that our own ruling classes are structurally incapable of making the transition; but are divided between those that will openly sabotage it and those that will float half measures.

While we can bloc with the latter against the former, if we want a full transition, we have to lead it. If we don’t want to be thrown under the bus, we have to be driving the bus. That means thinking like the leaders of society, because it’s our job now. And we need to seek alliances with the global majority, including countries that see themselves as Socialist.

The tactical challenge is that we operate in a national polity that presumes a “national interest” that subordinates the working class to the ruling class and this is deeply ingrained in popular perception, political (and union) movements; so consciously thinking internationally – outside the limits of the Brit Box – and framing our campaigning accordingly is essential.

Recent Comments