The claim from the Tory government and its army of media

supporters that the latest Budget has ended austerity is completely false. It

is very important for the left and the labour movement as a whole that they

grasp the character of the new attacks to come, so that they can resist them.

In effect, this is a Tory government of a new type. Previously,

since austerity was first implemented in 2010, the Tory governments have

transferred incomes from workers and the poor to big business and the rich. This

is in the hope that both increased rates of exploitation and the transfers of

funds themselves will encourage business investment. But the encouragement to

private investment has been a dismal failure. Private investment growth is

officially forecast to be zero this year.

The new Tories want to provide further inducements to

private sector investment by increasing public sector investment. SEB

has argued vociferously for increased public investment over a prolonged

period. This not investment for its own sake, but to increase the productive

capacity of the economy (adding to the means of production) as the most

decisive factor in raising the output of the economy and therefore prosperity.

But these Tories intend the opposite. They want to increase

the rate of exploitation further, provide incentives to private business to

investment, and intend to do this by funding with investment with yet another

reduction of public services and (probably) public sector pay. They will further

shift the burden of the crisis onto the shoulders of workers and the poor.

Government current spending is being cut over

the medium-term.

There is a one-off boost, to cope with the

effects of their own disastrous Brexit

The projected rise in government investment (if

it materialises) will still leave total government expenditure lower than in

recent years

This means that the rise in public investment is

more than being funded by further attacks on public services and public sector

workers

There is a significant projected increase in net

government borrowing. This is despite a fall in debt interest payments, which

themselves are being used to boost spending in the short-term

This is not ‘deficit-financed growth’, as has

been claimed. It is the effect of weaker growth on public finances, pushing both

tax revenues lower and automatic outlays (such as welfare payments) higher

In fact, the current year for which the OBR

provides an estimate and the subsequent 5 years’ forecasts are the weakest on

record for such a prolonged period

Taken together, SEB can find no recorded

10-year period of real GDP growth where every year is below 2%. This is what

the actual recent growth years’ growth rates will amount to, combined with the

OBR forecasts

There is a sharp one-off rise in government

current spending next year. This is not to combat the effects of the

coronavirus crisis, which is current. Instead, it follows the withdrawal from

the EU at the end of this year. It clearly indicates the government expects a

very negative outcome from the Brexit it is planning

There is nothing substantial in the Budget to

address the climate crisis, and the need for large-scale investment in

renewable energy production, or conservation

Austerity resumed

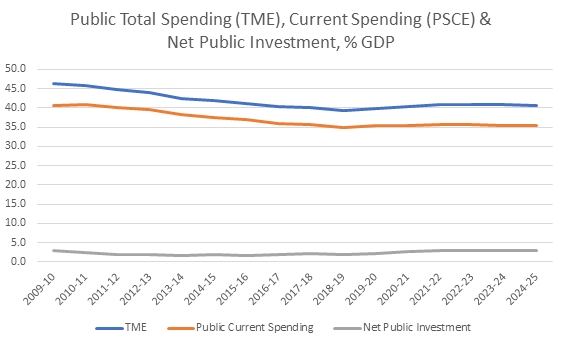

Despite the mass of commentary suggesting that austerity is

over, it is very simple to demonstrate that is not the case. The chart below is

taken from the OBR databank and shows total for public spending (TME), current

(or day-to-day spending, PCE) and net public spending as a percentage of GDP.

Chart 1. UK Public Spending Totals, Current Spending and New

Public Investment, as a % of GDP

The chart lines show a downward trend of total government

spending. For the 6 years of OBR estimates and forecasts from 2019/20 to

2024/25 average TME (total government spending) is 40.5% of GDP. For the

preceding 6 years it was 40.8%. Total government spending will be lower and austerity

is not ending at all.

The big impact will be felt by public current spending. Over

the same 6-year periods, Public Sector Current Spending (which includes health,

education, welfare and so on) will fall to 35.5% of GDP, from 36.5% of GDP.

By contrast public sector net investment is projected to

rise from 2% of GDP last year to 3% by the end of the 6 years of the OBR’s

forecast period. But it should be clear, it is ordinary people who most rely on

public services who will be paying for this increase. Furthermore, as the OBR

itself points out, there is a persistent and large shortfall between the

projections for public sector investment and what actually takes place.

Planning investment is not the same as delivering it.

A significant one-off

boost to spending

The basis for all the hyperbole and false claims about the

Budget is because of a one-off increase in government spending next year. This

can be shown in one of the key tables from the Treasury’s Red

Book.

As the table shows general government spending receives a

very large boost in 2021, rising by 10.9%. This falls back in the following

year and austerity returns in 2023 and 2024. It is important to note that the

growth rate of this measure of government spending is even slower than in the

most recent years, 1.8% and 1.2% in 2023 and 2024, compared to 2.1% and 1.9% in

2019 and 2020.

This increase in government spending is not

coronavirus-related, which is a current crisis that the government will be

hoping is over before the end of this year. Instead, it is a response to the

Withdrawal Agreement from the EU which does end in December of this year. Clearly,

the government expects a large negative shock from the Brexit it intends to

carry out, and the increased spending is an attempt to offset its worst

effects.

The attempt is only partly successful, using their own data.

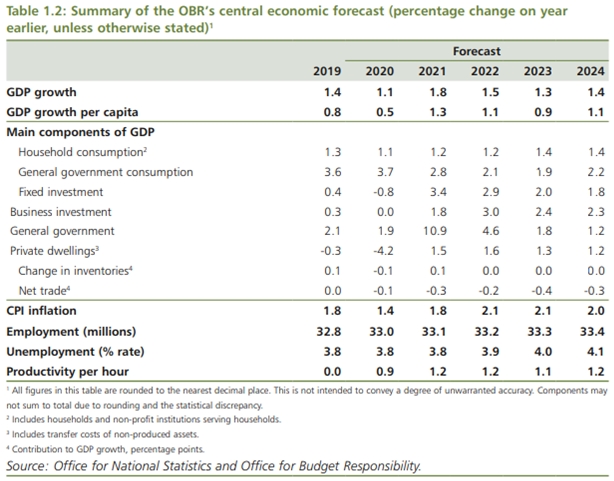

Real GDP growth is expected to rise to 1.8% in 2021. However, general

government expenditure accounts for about 40% of GDP, so a one-off increase of

nearly 11% should lead directly to a boost in GDP of well over 4%. But the

projected increase is just a fraction of that, with real GDP rising from just

1.1% in 2020 to a very modest 1.8% in 2021, when the spending is to take place.

Clearly, the implicit assumption is that without the one-off spending splurge,

growth would be sharply negative with the planned Tory Brexit.

Miserably low growth

The official projections for real GDP growth are a terrible

indictment of government economic failures. This includes but is not confined

to their own assessment of the further damage they will inflict with their

preferred Brexit outcome. As the Treasury’s Table 1.2 above shows, there is no

single year in which real GDP growth reaches 2% in the recent data and the

forecast period.

This is unprecedented. It would amount to at least a 9-year

period of real growth below 2%, a lost decade. There is no equivalent in the

modern era of such sluggish growth, in either the Great Depression or the Long

Depression at the end of the 19th century.

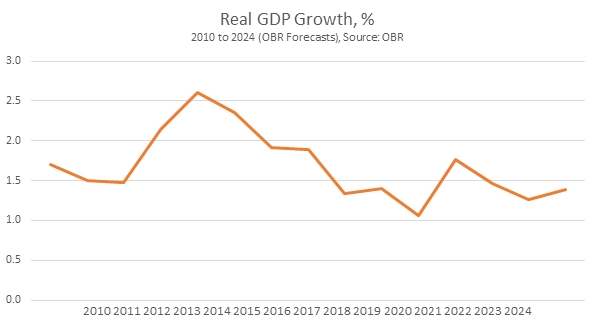

In fact, as Chart 2 below shows, the official outlook for

growth is even worse in coming years than the period immediately behind us, in

the years following the Great Recession in 2008.

Chart. 2 Real GDP Growth, 2010 to 2024 (Forecast)

This unprecedentedly weak growth has a series of

wide-ranging effects, depressing any rise in living standards or improvement in

public services. It also has the consequence of damaging public finances,

lowering the growth in government taxation revenues and automatically pushing

some government spending higher, for example in some welfare payments. This is

the cause of the large deficits in public finances that are forecast.

This is not ‘deficit-financed growth’ as has been claimed;

there is no growth and the economy slows. And, as already noted total

government spending will fall. These deficits are a reflection of economic

weakness, not ‘keynesian pump-priming’.

The multiple crises

There are a series of crises that the government is failing

to address: coronavirus, the weakness of the economy, the damage from its own

intention to crash out of the EU without a deal, the crisis in public services,

the unprecedented weakness in the economy and the existential threat of

catastrophic climate change. Measured against any of these challenges the

government’s response has been woeful.

On the coronavirus crisis, at every turn, it has unpicked

the measures praised by the World Health Organisation and enacted in China and

Viet Nam. Every excuse is made for inaction, that masks are not perfect,

testing is not 100% accurate, there is no point in heat-testing or even hand

gels at the airports, and so on. Instead, it has relied on measures to correct

some of the economic effects of coronavirus spreading. These steps, and many

more will need to be taken. But they are pointless unless and until government

is bearing down on the spread on the virus itself, which is clearly not the

case.

This will put enormous strain on the economy and public

services, especially the NHS (but also care for the elderly and education,

among others). Public services are already buckling under impact of a decade of

austerity. The UK already has below-average ratio of nurses to the population,

7.9 per thousand compared to 9.0 for the OECD as a whole. The only comparably

high-income country with a lower nurse/population is Italy (OECD

data).

It is clear that the increased spending in 2021 is not

coronavirus-related. Instead, it is a response to the effects of its own

determination to pursue a hugely damaging No Deal Brexit, presumably in order

to do a deal with Trump and adopt US business and labour market norms. The

government’s own forecasts show that a huge increase in spending to offset its

Brexit will produce barely a flicker of growth.

The planned increase in public investment is long overdue. But

it is very unlikely to produce either the transformation of ‘levelling-up’

across the country or the necessary corrective to abysmally low productivity

growth. For accuracy, the OBR forecasters do not expect either outcome.

One neglected factor, well established in classical

economics from Smith onwards, is that the effectiveness of all investment is

determined by the scope of the market. Any Brexit that takes this economy

outside the customs union will necessarily reduce the effectiveness of all

investment, because the market will also be severely contracted.

Finally, despite hosting COP26 in Glasgow later this year,

it is clear that the Budget contains no plan to address the climate crisis with

decisive action. Instead, this a government that has tried to press ahead with

plans such as the third runway at Heathrow and a road-building programme

regardless of the law. There was not even a pale imitation of Labour’s Green

New Deal, or anything similar. The Green New Deal is precisely the required,

targeted and ‘shovel-ready’ programme that could be implemented with

large-scale state investment – and is absolutely necessary. Instead, it seems

likely that The Tory recipe will be to search for new business-friendly

projects, such as more roads, and local and haphazard local projects.

When this fails to transform the economy, no doubt there

will be a new ideological offensive against public investment of all types. But

by then, US companies may be in control of large swathes of the public services

in this country.

There is no basis for the belief that the incoming Tory

government will end austerity. The reality is, from their own perspective and

from the interests they serve, the Tories will be obliged to deepen it.

It is extremely important that the labour movement, all

those who want decent living standards and public services and the left are not

suckered into believing that this Tory government will be any improvement on

its predecessors. Instead Johnson will pile up further misery, in addition to

the damage that has already been inflicted.

Early pointers

It is easy to list some obvious pointers to the government’s

direction on austerity.

First, the government’s legislative programme (the ‘Queen’s

Speech’) contains measures to outlaw strikes in the transport sector. There is

no need to outlaw strikes unless you are planning a confrontation with unions. If

the Tories are successful they will be emboldened to take on other workers. In

recent days, this

has been supplemented by the frame-up arrest of a union leader at a

peaceful picket as well as

an attack on the role or even the existence of the FBU from the

government’s inspectorate of fire services.

Secondly, in the same programme there is planned legislation

for permanent underfunding of the health service (as well as the threatened

removal of performance targets on waiting times at A&E services). In

real terms, the NHS funding law will provide the lowest cumulative rise in real

spending since the inception of the NHS. Labour attempted to amend it so

that the real increase is 4% per annum (which, although still modest rises by

historical standards takes some account of both rising population and the

higher inflation of medical equipment and drugs, plus the costs of

technological innovation). The amendment was rejected.

Thirdly, on this government’s own assessment the economy

will be severely hit by the Trump/Johnson Brexit. GDP

will be 6.7% lower by 2034 than it would if the status quo was maintained

and real wages 6.4% lower. This is not George Osborne’s stupidly exaggerated

‘project fear’ of immediate and sharp recession. It is this pro-Brexit

government’s own assessment of the consequences of something like a ‘No Deal’

Brexit. Typically, these official estimates tend to underestimate the damage,

as SEB has previously shown.

Finally, the economy is contracting. GDP in November shrank

by 0.3%, and outright contraction for the whole of the 4th quarter

is possible. With just one month’s data remaining it is almost certain too that

industrial production will have fallen for the year as a whole 2019 compared to

2018. Business investment is not rising and was lower in the 3rd

quarter of 2019 than it was for the same quarter in 2016.

The Tories are clearly faced with a worsening economic

crisis and the global economy offers no grounds for optimism. The idea that

they will address this crisis in the interests of the working class and the

poor is plainly ridiculous. Instead, they have given strong indications they

are gearing up for a major fight.

Why is there an

austerity policy at all?

Austerity has not been adopted because Tory politicians are

nasty. A change (in this case policy) cannot be explained by a constant.

SEB has repeatedly

explained that austerity amounts to a transfer of incomes from workers and the

poor to big business and the rich. So, in the very first austerity budget, the

Treasury documents showed that the projected revenue increase from raising VAT

of £13 billion (which mainly hits workers and the poor) was almost exactly the

same as the revenue lost by cutting Corporation Tax. The deficit was unaffected

by these measures, but income had been transferred upwards, to business and the

rich.

Using correct, Marxist terms there were two main elements to

austerity. The rate of exploitation was increased by cuts in real pay and

pensions. In addition, the social surplus was redirected away from workers and

the poor (cuts to welfare payments, rise in VAT) towards capital and the very

rich (tax cuts).

The combined effect of these measures was to force workers

to work more for less and to incentivise businesses to invest more. But the

second part of this policy has failed. Real wages did fall, but businesses did

not increase their rate of investment.

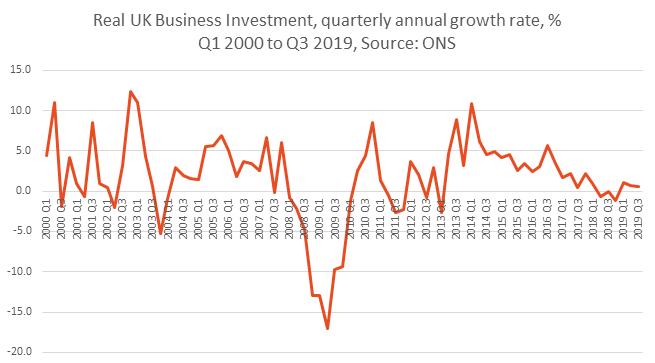

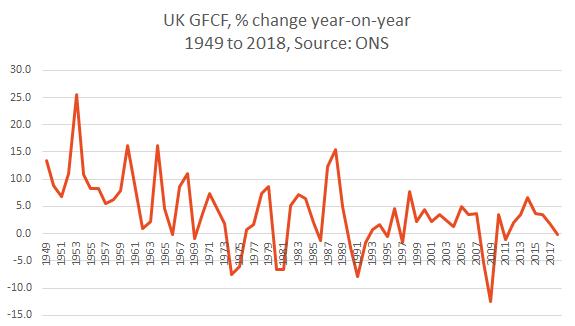

Fig.1 below shows the quarterly real annual rate of growth

for business investment from the 1st quarter of 2000. Business

investment has been slowing since the beginning of 2014 and is now beginning to

contract outright.

Fig 1. UK Business Investment, quarterly real annual rate of

growth from the 1st quarter of 2000 to 3rd quarter of

2019

In the last great crisis of British capitalism, Margaret

Thatcher was drafted in to do a very similar job to the one attempted by

Cameron and Osborne. Helped along by the huge windfall of North Sea oil

revenues, which were frittered away, she did produce a recovery in business

investment.

This was achieved by increasing the rate of exploitation. Cameron

and Osborne followed her example quite slavishly with spending cuts, real cuts

to public sector pay, cuts to welfare, cuts to taxes for the highest earners

and big business and privatisations. The cloak for these policies, the hue and

cry over the deficit, was different to their predecessor, inflation and

monetarism, but the project was broadly similar.

But the failure of the later Thatcherites can be shown

decisively in terms of business investment, the renewed expansion of capital

accumulation based on a series of defeats for the working class which allowed

her to increase the rate of exploitation.

Fig.2 below shows the change in investment, (GFCF, Gross

Fixed Capital Formation) from 1949 onwards. Data for UK business investment

alone only begins in the 1990s. But, as the UK is a capitalist economy the

majority of the investment throughout will have been made by the private

sector, and so provides an approximate guide to what the relative impact of

Thatcherism was in this area.

Fig 2. UK GFCF, % change year-on-year, 1949 to 2018

In the immediate post-World War II era there were relatively

high rates of investment, but it slowed markedly. This reached outright

contraction in the early 1970s. Thatcherism was the antidote to this, by

cutting real wages and business taxes. Although there was initially a slump,

Thatcher’s project was successful and investment recovered throughout the

1980s, until it was brought to a crashing halt by the excesses of the Lawson

boom, where the government refused to use the oil revenues for public

investment and cut personal taxes instead, fuelling an unsustainable boom in

consumption.

As the chart shows, investment growth has only ever been

meagre since. Worse, the sharp contraction of the 2007 financial crash and the

2008-09 recession has only ever produced a meagre and short-lived investment

recovery. Investment is now slowing to a stop once more. Cameron and Osborne

completely failed to emulate Thatcher’s temporary ‘success’.

This will not happen. The splits in the British ruling class

over Brexit were set aside in their united opposition to Jeremy Corbyn

precisely because he intended to increase the role of the state in the economy.

This diminishes the ability of most parts of the private sector to maintain

their profits, or to expand them. It is anathema to them. The Tories will not

do it.

Instead, there are protections for workers that currently

apply in British law because of adopting EU law. Johnson has signalled

repeatedly that he does not want to continue with ‘alignment’ with EU laws and

rules. The Trump/Johnson Brexit will include a programme of rolling back workers’

rights.

The objective conditions are also set firmly against

Johnson’s economic policy being some version of Corbynomics-lite, as much of

the press seem to want to believe. The government’s own negative assessment of

economic prospects under Johnson’s Brexit policy will also mean a sharp

deterioration in government finances. Under those circumstances a sharp

increase in state investment is not impossible, but goes beyond the limit of

what the private sector is likely to voluntarily provide in the form of buying

increased government debt. Some form of compulsion, including nationalisations

and raising taxes on business would be required. The Tories will not do it.

From their perspective, the Tories cannot and will not

abandon austerity. Instead, it should be clear they are preparing for a further

attack, and that this time it will include major political struggles, over

union rights, the right to organise and to protest and other issues.

Climate

change is the most important political issue of our generation. There’s 99

percent scientific consensus that humans are causing global

warming and that, unless we stop putting greenhouse gases in the atmosphere,

life on earth will become increasingly unviable. If we continue at the current

trajectory in terms of greenhouse gas emissions, we’re facing over four degrees

Celsius of warming by the year 2100. David Wallace-Wells writes in his book The Uninhabitable Earth: A Story of the

Future that, “according to some estimates, that would mean that

whole regions of Africa and Australia and the United States, parts of South

America north of Patagonia, and Asia south of Siberia would be rendered

uninhabitable by direct heat, desertification, and flooding.”

According to

the UN’s Intergovernmental Panel on Climate Change (IPCC), humanity needs to

halve its greenhouse gas emissions by 2030 and hit net zero by 2050. If we fail

to hit those deadlines, hundreds of coastal cities (including New York,

Shanghai, Hong Kong, Mumbai and Lagos) will likely be permanently submerged;

the agricultural system faces collapse; wars will be fought over climate

change-induced scarcity of resources; and there will be hundreds

of millions of climate refugees. Floods, droughts,

hurricanes, typhoons and wild fires will become so commonplace as to barely be

newsworthy. The results of climate change are already all too visible: 18 of

the 19 warmest years on record have all occurred

since 2001, and we’re witnessing an unusually high rate of

extreme weather events.

Most

environmentalists agree that the safe upper limit for global warming before the

planet reaches an irreversible tipping point is 1.5 degrees centigrade. Bearing

in mind that the average global temperature today is already

0.9 degrees higher than it was in 1880, we’re only left with

0.6 degrees before we hit the point of no return.

What needs

to happen?

There is one

critical target to focus on for the next decade, as outlined in the IPCC

Special Report on 1.5 degrees, which is to reduce global carbon emissions to 50

percent of current levels.

Labour’s

manifesto sets out an even more ambitious target, aiming to “achieve the

substantial majority of our emissions reductions by 2030 in a way that is

evidence-based, just and that delivers an economy that serves the interests of

the many, not the few.” Labour has made a world-leading pledge to generate 90%

of electricity and 50% of heat from renewables and low carbon sources by 2030.

Globally,

the target will be to get to net zero emissions by 2050. Note that ‘net zero

emissions’ doesn’t necessarily mean not emitting any carbon at all – but

whatever is emitted must be captured and stored.

Practically,

this means that “flying, driving, heating our homes, using our appliances, basically

everything we do, would need to be zero carbon”, writes climate change expert Kevin

Anderson.

This goal is

achievable. We already have the technology to generate all our electricity via

renewable energy. Particularly in technologically advanced countries, it should

be perfectly possible to completely phase out fossil fuel-based power plants

within a few years; it simply requires investment in the surrounding

infrastructure, along with the political will to stand up to fossil fuel

capitalism.

We can also

massively cut down on waste and inefficiency. Energy efficiency – making our

economy less energy-intensive – is “widely considered to be the most important

single option for carbon reduction”, in the words of Neil Hirst, former

Director of the International Energy Agency (The Energy

Conundrum). David Wallace-Wells notes that around half of British

greenhouse gas emissions come from inefficiencies in construction, discarded

and unused food, electronics, and clothing. Retrofitting homes for heating

efficiency, for example, would make a significant contribution to reducing

emissions in relatively cold countries like Britain. According to Mike

Davis, “heating and cooling the urban built environment alone

is responsible for an estimated 35 to 45 percent of current carbon emissions.”

Transport is

another key area for reducing – and ultimately eliminating – carbon dioxide

emissions. There’s tremendous potential for fully-electric public transport

systems, along with electric car pools, electric bicycles, and urban designs

that encourage cycling. Again, this requires major investment, along with

rigorously-enforced laws to stop the climate criminals. In the words of Gus

Speth, former Dean of the Yale School of Forestry and Environmental Studies, “a

reliably green company is one that is required to be green by law.” (Cited in

Naomi Klein’s This Changes Everything:

Capitalism vs. The Climate) Meanwhile, until we find a way to power

aeroplanes without burning fossil fuels (the technology isn’t far off), we’ll

need to reduce air travel significantly.

We also need

to change our diets. We don’t all have to become vegan, but meat consumption

will need to be reduced in wealthy countries. Mike Berners-Lee writes that “the

single most important change will be an amazingly simple dietary shift towards

less meat and dairy consumption, with a particular focus on reducing beef. This

will markedly reduce greenhouse gases, improve the nutritional output of our

land and, by relieving land pressure, ought to be pivotal in stemming

deforestation.” (There Is No

Planet B: A Handbook for the Make or Break Years)

However,

it’s important to note that individual acts of good planetary citizenship are

not going to solve the problems we’re facing. As Wallace-Wells observes, “we

frequently choose to obsess over personal consumption, in part because it is

within our control and in part as a very contemporary form of virtue

signalling. But ultimately those choices are, in almost all cases, trivial

contributors, ones that blind us to the more important forces.” Without

concerted action at a national and international level, without large-scale

decarbonisation, we will not avoid catastrophic climate change. As such, the

problem is a political one.

Responsibilities

of the rich countries

At a global

level, China

leads the way in tackling climate breakdown, in terms of

investing in renewables and electric vehicles, driving the costs of green

energy down via massive state-led investment, carrying out vast afforestation

projects, and rolling out fully-electric buses and trains. However, China is

still a developing country, with over 1.3 billion people, many millions of whom

are likely to increase their energy consumption in the near future, since they

are still at a stage of development where increased energy consumption

correlates directly with improved quality of life outcomes. China can’t save

the planet on its own, nor can it be expected to. In terms of “common

but differentiated responsibilities”, the

technologically-developed wealthy countries of the OECD have the greatest

responsibility when it comes to averting catastrophic climate change.

The rich

countries fuelled their own industrial revolutions with coal and oil, resources

which they came to dominate in no small measure through colonial conquest and

imperialist manoeuvring. The US and Europe – with around 15 percent of the

global population – have contributed to over half the cumulative carbon dioxide

emissions since 1850. And the horrific irony is that these countries are the

least affected by climate change. Catastrophic climate events will hit – are

hitting – the poorer regions of the planet first.

As such,

countries like Britain have a clear moral responsibility to take the lead in

addressing climate change. To this day, it’s the wealthy that are living

wasteful lives, contributing to the ever-worsening situation. According to Ann

Pettifor, “just 10 percent of the global population are responsible for around

50 percent of total emissions. Per capita carbon dioxide emissions in Africa

are less than 10 percent of those in Western Europe and North America. Tackling

the consumption and aviation habits of just 10 percent of the global population

should help drive down 50 percent of total emissions in a very short time.” (The Case for the Green New Deal)

Furthermore,

it’s precisely the rich countries that have the resources to lead the way on

climate action. As has been pointed out before, “we

bailed out the banks, so now we can bail out the planet.” In

countries where large numbers of people don’t have access to modern energy, it

is understandable and correct that people want to provide that access with a

minimum of delay and cost. Sometimes that may even mean new coal capacity in

countries like Pakistan, where coal is by far the cheapest and most accessible

fuel (although the west should be offering the material support necessary to

allow such countries to meet their energy needs in a way that doesn’t damage

the environment). In OECD countries on the other hand, there is absolutely no excuse

for pursuing anything other than a rigorous and thoroughgoing energy

restructuring based on renewable sources.

How are we

doing so far?

The United

Nations Framework Convention on Climate Change was adopted in 1992, committing

the 154 signatory nations to “preventing dangerous anthropogenic interference

with Earth’s climate system”. The sad fact is that, in the intervening 27

years, “the sum of all the world’s climate action has so far made little or

perhaps even zero detectable impact on rising global emissions.” (Mike

Berners-Lee)

We are

nowhere near on track to meet the targets discussed above, for the simple

reason that we’ve left it to the capitalist market to provide solutions to the

planet’s problems. The domination of neoliberal economics over the last few

decades has reduced governments’ ability to set economic policy in the national

interest. Fiscal revenue isn’t sufficient to finance large-scale green

development, and shareholder-driven capitalism is incapable of long-term

strategic planning on the level that’s needed. Meanwhile, the big fossil fuel

companies have an extraordinary level of entrenched power that they’ve used

systematically to slow down the energy transition.

There isn’t

even any meaningful agreement among the western ruling classes as to how to

respond to climate change. Although there is a relatively more forward-thinking

section that understands that they too would be affected by climate breakdown

(in much the same way that sections of the English bourgeoisie became

interested in public health when they realised that they too could fall victim

to cholera), there are also the neoliberal extremists who are happy enough with

the idea of moving to Finland or New Zealand and setting themselves up in gated

communities.

In summary,

neoliberal capitalism has shown itself to be utterly incapable of averting

environmental catastrophe. Even in Britain, where there has been some focus on

wind power, this has been far too slow. Today, wind contributes 17 percent of

electricity generation in Britain (well behind gas, at 40 percent). The

economist Mariana Mazzucato, arguing for concerted state-led investment in

green development, complains that the strategies thus far employed in the US

and Britain “lack a clear direction and fail to offer long-term incentives,

resulting in a start–stop approach to green initiatives that produces dubious

outcomes at best.” (The

Entrepreneurial State)

The Green

New Deal

The Green

New Deal (GND), conceived a decade ago by British economists and

environmentalists but recently popularised by progressive US congresswoman

Alexandria Ocasio-Cortez, provides the first viable, comprehensive and

actionable plan for developed countries to decarbonise their economies whilst

creating jobs, tackling inequality and promoting equality and social justice.

Measures include investment in renewable energy and zero-carbon public

transport; upgrading buildings for energy efficiency; building ‘smart’

distributed power grids to provide affordable clean electricity to all;

reorganising the food system; ending subsidies to the fossil fuel industry; and

prioritising basic needs.

The key to

implementing a programme such as the Green New Deal (or as it’s often referred

to by Labour politicians, the Green Industrial Revolution) is public investment

on a grand scale. As Berners-Lee points out when discussing the future of

renewable energy, “the solutions we need to the problem of intermittency and

storage are all coming along nicely; the critical factor is investment.”

This is

precisely what has been agreed by Labour’s recent conference, and what is being

put

on the table by shadow chancellor John McDonnell: a programme

of government investment “mobilising £250 billion of capital spending on the

projects needed to decarbonise Britain to avert irreversible climate change.”

Supported by

a National Investment Bank and network of regional development banks, the

programme will seek to ensure that “the transition to sustainability is one

that benefits everyone across our society.”

Starting

with the infrastructure for widely deploying clean energy, along with a plan

for retrofitting homes to be energy-efficient, the Green New Deal would create

hundreds of thousands of skilled jobs. The

plan includes nationalising the major UK-based energy

companies, replacing all gas boilers, closing fossil fuel-based power stations,

investing in and subsidising electric cars, vastly expanding off-shore wind

capacity, and decarbonising the public transport system.

On top of

the Green New Deal, it’s worth mentioning that Labour has also committed to making

green technologies available cheap or free to the countries

of the Global South. Plus of course the present Labour leadership is deeply

opposed to war, which has a major

environmental cost on top of its more obvious human cost.

If Labour

wins the General Election on 12 December and a Jeremy Corbyn-led government can

implement its version of the Green New Deal, it will be a huge boost for the

global battle to save the planet. Britain will blaze a trail for the rest of

the OECD to follow, towards a global Green New Deal that is, in Ann Pettifor’s

words, “a global banner behind which millions can assemble with one voice in

order to address the gravest crisis humanity has ever faced.”

If, on the

other hand, Labour loses the General Election and Britain has to endure another

five years of hard-right Tory government, the result for the fight against

climate breakdown would likely be disastrous. Boris Johnson’s ‘hard Brexit’

vision involves leaving the EU customs union and negotiating a free trade deal

with the US. That will mean a wide-ranging political alignment that could well see

Britain leaving the Paris Climate Agreement. With both Britain and the US

outside the Paris Agreement, the prospects for international cooperation to

combat climate change would look increasingly grim.

The planet

needs a left Labour government in Britain.

This is a slightly amended version of an article which originally

appeared in the Morning

Star.

The election plans laid out by the two major parties mean

that it is crystal clear only Labour has policies to address the current crises

(the LibDems can be disregarded in policy terms, as they only have one policy,

which they claim is ‘stop Brexit’ but which is actually ‘stop Corbyn’). There are combined crises of the climate

catastrophe as well as the stagnation of the economy and living standards.

The depth of the British economic crisis is not at all

widely understood. It should be as only

a proper appreciation of the scale of the problem can lead to the appropriate

measures to tackle it, the policies that are necessary and the political

choices that follow.

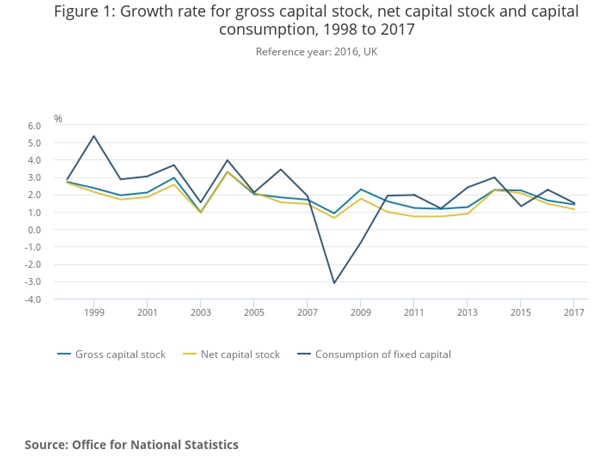

The scale of the economic crisis is illustrated in the chart

below. Fig.1 shows the growth rate for the capital stock, the total value of

machinery, factories, software, computers and so on used in the production of

goods and services across the economy.

Also shown are the growth rate in the consumption of capital, all the

machinery used up in the production process, the equipment the becomes obsolete

and the factories that become dilapidated. From this, the growth rate of the net

capital stock can be derived, which is the growth rate of the capital once the

capital consumption has been taken into account.

Fig.1 Growth in UK Net Capital Stock, 1998 to 2017

From 1998 to 2017 the annual growth rate in the net capital stock has fallen from 2.7% to just 1.1%. This exceptionally low level is a return to the earliest periods of capitalist development in Britain. In the 1760s as George III became the monarch, the growth rate in the net capital stock was about 1% annually. The only period which was significantly slower was in the exceptional period 1933-34, which saw an outright fall in the net capital stock, as part of the Great Depression.

This all matters because the net capital stock is

effectively a measure of the fixed means of production for the whole economy.

It is extremely difficult for the economy or living standards to grow

sustainably beyond the growth rate of the net capital stock. The other main route is to increase the hours

of labour, either by getting more people to work or getting the existing

workforce to work longer hours. But

without a rising level of the capital stock, the productivity of labour cannot

rise.

At the same time, an increase in one specific area of the

net capital stock is needed to tackle the climate crises. This is the required

level of investment in the production of renewable energy as fossil fuels are

eliminated. In addition, investment is

also needed in energy conservation and in the reduction of energy consumption.

The Labour party policy precisely addresses this key

component of the crisis by sharply increasing the level of public sector

investment. Labour plans to invest £250

billion over ten years in a Green Transformation Fund to achieve all these

aims.

Labour will also add a further £150 billion in a social

transformation over 5 years to invest in infrastructure, transport, housing and

capital investment in public goods such as health and education. The dilapidation of the schools and hospital

will be tackled.

The contrast with the Tory plans is not mainly the inadequately

small pledge of £20 billion per annum, or even the sharp U-turn in Tory government

ideology about borrowing to invest (no more ‘magic money tree’ nonsense).

The main issue is

that the Tory plans are completely fake. They are undeliverable under either

Boris Johnson’s deal or No Deal, which is still an option and which is the

clear preference of Trump. Under the government’s

own forecasts, the British economy will be 9.3% lower than it would

otherwise be in 15 years’ time with No Deal. Even if this forecast is accurate

(and mainstream economics tends to underestimate the negative impact on

investment), then the damage to government finances is likely to be very large.

To illustrate this point, the British economy did not

recover to its pre-recession peak until the 1st quarter of 2013,

fully 5 years later. This implies that the economy would have been about 12%

larger if the recession had not occurred. Over that time and in later years,

public sector debt trebled from under 30% of GDP to over 80%, including fierce

austerity measures.

This gives some indication of the likely damage to

government finances following a major negative development, either Johnson’s

deal (which is just No Deal for just Britain) or No Deal for the UK. There will

be no money at all for additional Tory public sector investment.

In fact, the long-standing ideology of the Tory party in

favour of small state economics combined with the absence of any resources

under their Brexit plans means that the entire government ‘programme’ of

investment is a complete fraud.

The Cabinet ideologues, almost all of whom have voted for

and written in favour of privatisation and outsourcing, have no intention of

allowing a sustained increase in public investment. And Trump has no intention

of allowing it either. His imposed deal will be the opposite, privatisation and

outsourcing with US corporations at the head of the queue.

By contrast, Labour gets it.

The scale of the ambition is in line with the objective environmental

and economic crises within the constraints of the current level of public

ownership of the economy. Looking ahead,

one of the key benefits of a large-scale nationalisation programme is that the

state would be able to have an even greater impact on the total level of

investment in the economy. These are the

real economic and environmental choices at stake in the election.

Bolivians vote in a general election on October 20th. Evo Morales has been the President since

2006, winning three successive terms as President.

A victory for him would continue the development of the

economy and the rise in living standards since he took office. It would be a considerable boost to the left

across Latin America, which otherwise faces the impositions of Bolsonaro, Macri

and Moreno, backed by the US and in some cases the IMF. Socialists internationally have every reason

to support a Morales victory.

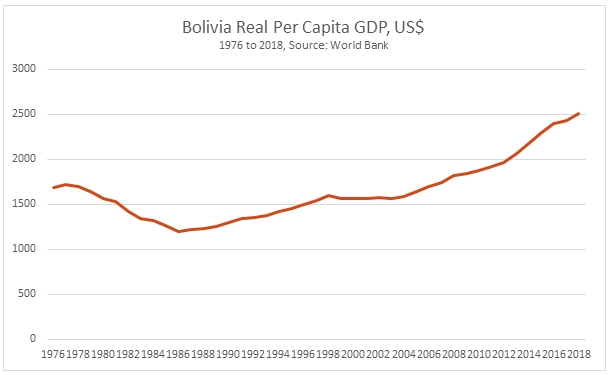

The success of the project begun by Morales and the MAS

(Movement for Socialism) can be shown in 2 charts. The first below shows the level of Bolivian real

per capita GDP since 1976. In the 30 years before Morales came to power, real

GDP per person effectively stagnated. In

1976 it was US$1,687 and was only $1,692 in 2006, barely altered. Since then it has risen to US$2,506,

according to World Bank data. This

represents a rise in average living standards of 48%.

Fig. 1 Bolivia Real GDP

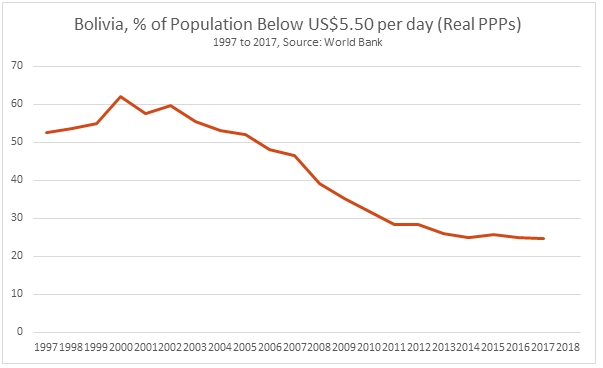

However, it is possible that average living standards rise

but that the bulk of this increase is claimed by the rich and the upper

classes. But this is not the case in

Bolivia. Chart 2 below shows the

proportion of the population below the poverty headcount rate of US$5.50 per

day, adjusted for inflation and PPPs (purchasing power parities).

Fig.2 Bolivia, % of Population on Incomes Below US$5.50

Once again, this measure of poverty shows there was little

progress before Morales. In 1997 52.6%

of the population were subsisting on incomes equivalent to below US$5.50 a day

in real terms. By 2006 that rate had edged down to 48.1%. But the fall since then has been dramatic,

with the poverty rate at 24.7% in 2017 (the latest available data). As the

population of the country is now over 11 million, this means that literally

millions of people, about one-quarter of the population, have been lifted out

of poverty.

The success of

Morales

There are a number of factors which have contributed to

Morales’ success. Initially, like many

countries in Latin America and beyond, Bolivia benefited from the rise in

global commodities’ prices, which were spurred on in particular by the rapid

pace of China’s industrialisation. There

was too a major shift in the population from the countryside to the towns and

cities, which rapidly expanded the workforce available for more advanced

production, including manufacturing.

But these factors were common to many countries, especially

in Latin America, but unlike Morales they failed to maintain their gains, or

even to hold onto office. That

commodities’ price boom has since faded as the Chinese economic model has

adjusted, and the pace of the migration into the urban centres has slowed in

many countries. The world economy is also slowing, so none of the previously

favourable conditions is likely to return in the foreseeable future.

To explain Morales’ success, one key area where the Bolivian

economic project stands apart, certainly in Latin America, is that the gains of

rising prices and output were not simply used to boost consumption, but also to

increase investment. Chart 3 below shows

the proportion of GDP directed towards investment, or GFCF (Gross Fixed Capital

Formation).

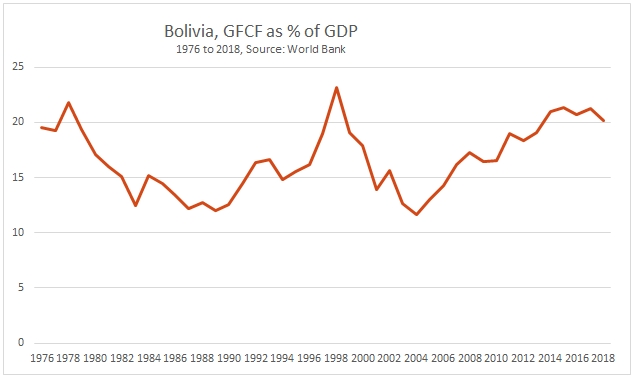

Fig. 3 Bolivia, GFCF as % of GDP

In 2006 GFCF as a proportion of GDP had fallen to a 14.3%

and had been even lower in the preceding period. It has since risen to 21.4% in 2015,

although it has softened a little in following years. The urban population is now 70% of the total,

so there is diminishing scope to increase the workforce available for more

advanced manufacturing or industrial production. Further gains will require the return to

previous high levels of investment, and even their extension.

Prospects

The validity of opinion polls is hotly disputed, although many show Morales well ahead but

short of an outright majority for the first round of voting.

The stakes are very high.

The insurrection in Ecuador against enormous price hikes, imposed by the

Moreno government acting on the instructions of the US and IMF, shows what the

likely alternative to Morales will be.

This includes both huge attacks on living standards, and severe state

repression to carry it out.

Morales’ political background is as organiser and then

general secretary of the peasant farmers, which experienced fierce repression

from the large landowners and the state forces, and forced the farmers into

guerrilla warfare, Morales included.

This is a political formation which creates an understanding of the role

of the state, which classes it defends and the brutality of it attacks, all

supported by the Unites States. It also

teaches the need for collective discussion, unity of action and strong

discipline among the resistance fighters.

It is clear too that, through this experience and his own ethnic

identity, Morales enacts a highly advanced policy towards the indigenous

populations.

Despite or because of all this, here in the West there is a

campaign of slander against Morales, led by the ‘liberal’ press. So, the Guardian repeatedly runs entirely

distorted arguments and outright lies, including describing Morales as ‘the

murderer of Nature’ in the Amazon.’ The

reality is that it is the far right poster boy Bolsonaro in Brazil, an ally of

Trump’s who is destroying the Amazon, and Morales is using every mechanism to combat it.

The stakes are also high for the planet as a whole. The Bolivian elections will not decide that

fate, but they are an important battle in the struggle.

Despite the claims of the Tory party and other supporters of

a No Deal Brexit that a new golden age of trade awaits with the US, the Trump

administration has just imposed new trade tariffs on British producers.

This is important for two reasons. It reveals the falsehoods

underlying the entire No Deal project. It also sheds light on the global

perspective of Trump, and how he aims to address the US economic crisis at the

expense of the rest of the world.

New tariffs

The US Treasury has issued a series of new 25% tariffs on UK

producers and others in the EU (pdf). This list is 8 pages long and includes a wide

range of goods, from aircraft, to whiskies, to woollens to pipe cutters and

many more goods besides. The tariffs are

due to come into effect on October 18.

The tariffs are allowed under the WTO rules (which are

themselves skewed towards the US) because it has found that the EU’s Airbus

production receives state subsidies.

However, experts suggest that a similar finding will be made against

Airbus’s big rival Boeing in a matter of weeks.

Both entities receive state support. In fact, it is

inconceivable that any private corporation would undertake the vast investment

required for large-scale aircraft production without state financing and

subsidies. Inadvertently, the free

market ideologues of both the US and the EU make the case for socialised

investment. In the case of the aircraft

makers, the investment would simply not take place without state intervention.

Airbus is also partly owned by European governments.

Boeing and Airbus are the two main global rivals for the

demand of airlines’ new carriers. They are at each other’s throats for decades,

and the cases against each other at the WTO have rumbled on almost as

long. This has taken a new twist with

Trump’s aggressive imposition of tariffs on a number of countries (including

‘allies’ in Europe,

as well as Canada

and Mexico). There is too the issue of the disastrous roll-out

of the Boeing Max 737, which has led to crashes, huge numbers of fatalities,

lawsuits and a threat to the company.

The imposition of the tariffs has received very little

coverage in the mainly Brexit-supporting press. Tariffs on existing production

destroy jobs and raise prices. If they are sustained these sanctions will raise

prices for US consumers (and EU tariffs will do the same in the EU) and destroy

jobs in the sectors concerned.

The sanctions have a strategic aim and reveal Trump’s

approach to the problems of the US economy.

Trump’s strategy

The US

economy is slowing – and the Presidential election is now little more than

12 months away. GDP growth in the 3rd quarter slipped to 2.1%, from

3.1% in the 2nd quarter. But the US is also experiencing a long-term

slowdown. As John Ross has shown

elsewhere, the medium-term trend in the US economy, removing the effect of

business cycles, is towards slower growth.

Therefore Trump has two problems. The immediate issue is to

raise the growth rate to a level that gives him a better chance of re-election.

The most

recent poll shows his approval rating at -16, which is normally far too low

for an incumbent to be re-elected. But he also has a strategic task in his role

as the representative of the general interests of US big business as a

whole. This is to ensure that the US

growth rate can recover over the medium-term, or at the very least that other

countries do not continue to gain ground on the US.

China is clearly the main target of Trump’s trade policy but

is certainly not the only target. Taken together, and making no judgement on

its likely success, from Trump’s perspective this amounts to an entirely new

trade policy for the US in the post-World War II era. Historically the superior

productivity of US industry and agriculture meant that it was an advocate for

free trade. While there were general benefits, the US would always be the

biggest winner.

Trump has turned that outlook on its head. The US slowdown

will be addressed by a re-ordering of the global trade system in US interests.

Specifically, other countries will be subordinated to the US, providing it with

unfair advantages and crimping the growth of non-US industries where they are

in direct competition with major US companies.

In this light, the attack on Huawei (which

leads on 5G telecoms technology) should be seen as driven by the same

policy as the attack on the makers of Airbus (Boeing’s sole global rival).

Airbus attack

Airbus had sales of €31 billion the first half of 2019. It

employs 136,000 people worldwide, 14,000 of them in the UK, where production of

the high value-added wings and part of the engines takes place.

Because of the integration of production across Europe, Airbus

has already publicly stated that any Brexit outcome which includes leaving

either the Single Market or a customs union would pose the company with

enormous challenges, which could require relocation in the EU.

The Trump/Johnson No Deal project does mean leaving both the

Single Market and the customs union.

This is also true of the latest Johnson proposal, which means that

Britain would leave both. The major

Airbus plant is based in North Wales.

There is clearly an advantage to the US from severely

disrupting the production of Boeing’s only global rival. But it should be

equally clear that there is no advantage to producers in the UK to accepting

such a deal. Unions

and business groups here have been right to highlight this.

This country will have to operate under WTO rules if it

crashes out without a deal. Under those rules, the trade tariffs are allowed

once an unfavourable ruling is made. In fact, there are few other mechanisms

available under WTO. But, until recent

years, the US was the by far the largest economy in the world. So, any system allowing

bilateral trade tariffs massively favoured the US. That will still be the case between the UK

and the US, with Trump holding all the cards in any negotiations or in any

subsequent trade dispute.

At the same time, it is futile to protest that Trump should

have targeted other countries instead, if he wants to get a US-UK trade deal. This is the approach of some business groups

in this dispute.

Trump’s aim is firstly to attack Airbus so that it does not gain an insurmountable advantage over Boeing. But he also rejects any soft-pedalling in his aggressive trade policy, even for ‘allies’. Outside of the EU’s Single Market and customs union, Britain will have to accept whatever Trump offers. And what he offers, or at least intends, is a complete restructuring of the global trade system in US interests.

Socialism’s aim is to improve the well-being of humanity. And

nothing in history has remotely improved the condition of such a large part of

humanity in such a small period of time as the development of the People’s

Republic of China since 1949 – the 70th anniversary of the founding

of which occurs on 1 October 2019.

China’s was one of the two greatest socialist revolutions of

the 20th century – the other was the October 1917 Russian

revolution. The international impact of the Russian revolution, overthrowing

the weakest link in the imperialist system, among its other enormous

achievements, played a decisive role in smashing to pieces the colonial empires

which had oppressed the great majority of humanity for centuries. China’s was

the greatest revolution within the developing countries, those oppressed by

imperialism, within which the great majority of humanity still live.

In 1949 China, oppressed by a century of foreign invasion in

which around 100 million Chinese people were killed, was almost the world’s poorest

country – the details are in the article below. Angus Maddison, former head of

statistics of the OECD, and the world’s most renowned analyst of long term

growth, calculates that at the time of the creation of the People’s Republic of

China (PRC) its per capita GDP was not only lower than 130 years previously but

far lower than Western Europe or England in 1500 – that is lower than in the late

European Middle Ages and far lower than at the time of Shakespeare. Reflecting

this fact average life expectancy in China was only 35. But by 2019 China’s

people, almost 1.4 billion or nearly a fifth of humanity, had been lifted from

poverty to a living standard to the verge of becoming a high-income economy by

international standards. Nothing approaching such a rapid improvement of the

life of such a large proportion of humanity has ever taken place anywhere else

in human history. That is the measure of the literally incredible achievement

of the PRC since 1949.

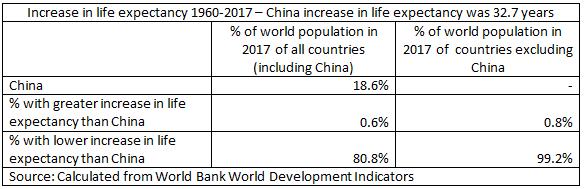

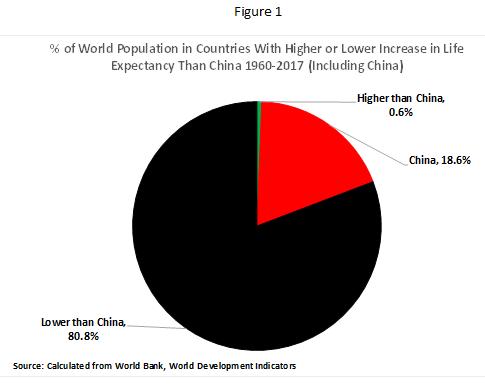

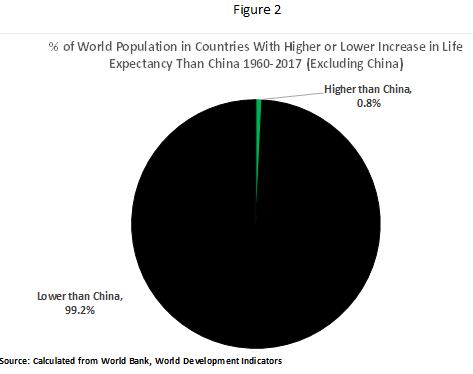

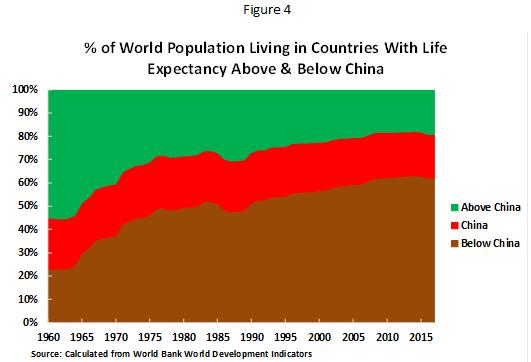

The article below examines that improvement in the life of

China’s people via the most direct of all measures – life expectancy, which is

well known to be the most sensitive measure of overall social well-being. The

figures are staggering. Leaving aside China itself, China’s life expectancy has

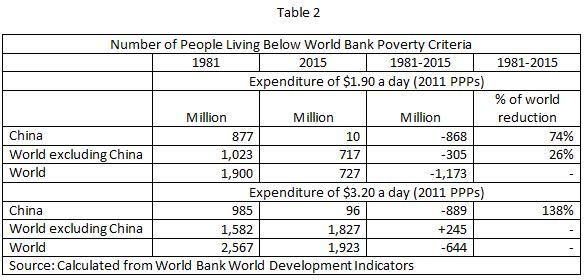

increased by more than that of 99.2% of humanity! This is in addition to China

being responsible for lifting over 850 million people out of internationally

defined poverty – three quarters of the reduction of world poverty. China has

lifted out of poverty far more people than the entire population of the

European Union or the entire continent of Latin America.

Capitalism naturally lies regarding China

To anyone who can think seriously about the well-being of

humanity what is reflected in these ‘dry statistics’ about China is such a gigantic

improvement in the lives of people that for anyone understanding it they must

almost be moved to tears. Therefore, naturally capitalism does everything it

can to make sure such realities are known to as few people as possible in the

world. Nothing else is to be expected from capitalism, because if such

realities were widely known it would be a gigantic blow to the standing and

hegemony of capitalism. As China becomes still more successful, and the life of

the 1.4 billion Chinese people improves further, all that will happen from

capitalists and the media they control is that the amount of distortion and

lying will increase – because it is vital for capitalism to prevent the rest of

the world knowing how much the life of the Chinese people has improved in the

70 years since China’s socialist revolution. Because if that truth is known

more people, particularly at present in developing countries, would want to

follow that route.

Any serious progressive individual or media, let alone

socialists, would, of course, hail the gigantic step forward for humanity which

has taken place in China – while doubtless making whatever were their liberal qualifications

or critiques of it. But capitalism and liberals long ago ceased to be

progressive. If you read newspapers such as the Guardian or the New York Times around

the 70th anniversary of the PRC you will see not analysis of what a

huge step forward for humanity this is but suppression of the real facts

regarding China’s development – liberals long ago ceased not only to be

progressive but to pay any attention to the truth.

In addition to the overall lies against China there are of

course specific ones which any examination of the facts disproves. One is

related to the gigantic support for Mao Zedong in China. Supposedly this is

inexplicable given that it is claimed by capitalism Mao Zedong was a vile

oppressor. In reality in China during

the period of Mao Zedong, despite the huge mistakes of the Great Leap Forward

and Cultural Revolution, China experienced the most rapid improvement in social

conditions, reflected in increase in life expectancy, in human history – a

reflection of China’s emphasis on health care and education. As the article

notes: ‘In the 27 years between the establishment of the People’s Republic of

China in 1949, and the death of Mao Zedong in 1976, life expectancy in China

increased by 31 years – or over a year per chronological year…. Far from being

negative, China’s record in this period was one of history’s most extraordinary

social achievements.

‘Instead of engaging in factual falsification and myth

making, foreigners can more accurately understand the support for Mao Zedong in

China, even leaving aside other issues, such as the achievement of real

national independence, merely by the lived experience of this fact. If someone

leads you to live an extra 31 years it is unsurprising you hold them in esteem!

‘

The fact that capitalism systematically lies about China of

course makes it incapable of understanding the real dynamic in that country.

Confusion in parts of the left

But if rejection of reality is to be expected from

capitalism and its apologists what is ridiculous is that sections of the left

refuse to face such a gigantic reality as China’s social achievements – these

‘left’ criticisms in fact only repeat capitalist propaganda. At the most absurd

they spread capitalist lies such as that Chinese workers life in ‘slave like’

conditions – something which is refuted in 1 second by looking at the figures

on China’s life expectancy dealt with in this article. The idea that a

‘sweatshop’ produces a more than 40 year increase in life expectancy, more than

every major country in the world, is an absurd joke, or more precisely ‘leftist’

repetition of capitalist propaganda.

Illustrating even more lack of seriousness about socialist

and Marxist theory is left repetition of the claim that China is capitalist. This

is refuted by any Marxist analysis of China’s economic structure – see ‘Why China is a socialist country – China’s theory is

in line with Marx (but not Stalin)’. For those who claim China is

capitalist it is then necessary to explain why these gigantic and measurable steps

forward for humanity took place in a country which declares itself socialist

and no such step forward was taken in countries which declare themselves

capitalist. But it is also necessary to understand the profound consequences.

If ‘capitalism’ is capable of lifting more than 850 million people out of poverty

then capitalism is not reactionary but is a profoundly progressive system. This

foolish so called ‘left’ criticism of China therefore turns out to be…. a

justification for the progressive role of capitalism!

But the practical consequences of confusion on the left on

this issue are extremely serious. China has an economic system which

demonstrably delivers in practice, not merely in theory, enormous improvements

in the living conditions for the overwhelming majority of the population and in

particular the poorest sections of society. It is based on the socialisation of

the dominant sectors of China’s economy – that is the ability of the state to

control the level of investment in China. As it was stated at the 3rd Plenum of

the Central Committee of the 18th Congress of the CPC, the latest comprehensive

statement of China’s economic policy: ‘We must unswervingly consolidate and develop

the public economy, persist in the dominant position of public ownership, give

full play to the leading role of the state-owned sector.’ Any study of how

China’s economy is regulated confirms that decisive role of the state sector.

The left should be using this model to explain that it is

the most effective method to raise living standards and eliminate poverty. In

Latin America, for example, where the left was unable to deal with the

consequences of the downturn in commodity prices after 2014, this is decisive.

As Brazilian socialist Elias Jabour put it recently: ‘The rise of

China means that Brazil and Latin America has a real alternative to

neo-liberalism. It provides the possibility for greater economic integration

outside the orbit of imperialism. It is impossible to imagine the existence of

progressive governments in Latin America without the existence of socialist

China.’ This applies both to the support that economic interaction with China

can give to Latin American, and other developing, countries and to how the

Chinese economic model provides a proven practical alternative to

neo-liberalism within Latin American countries.

The left in China

But also, internationally, it is necessary to understand

that the biggest left in the entire world is in China. The best way to

understand that is to read Weibo, the Chinese equivalent of Twitter, or to

follow websites such as Guancha.cn – something it is entirely

possible for anyone who does not read Chinese to do with modern translation

software. And for those who do not trust anything produced in China, or find it

too tiring to use translation software, they can get a distorted but not wholly

inaccurate vision by reading Jude Blanchette’s China’s New Red Guards. No where else but

China do you find obviously left-wing leaders who have 3 million, 5 million, 6

million followers on social media. And these huge left-wing forces are

unequivocal in their support of the overall path, naturally not every specific

policy, of the CPC. They are ‘Maoist’ in their overall world outlook. The

Fidelista left in Latin America is undoubtedly the other mass socialist/Marxist

current in the world, but even that is much smaller than the left in China.

Understanding the actual reality of China, and the impact

this has on its population, will immediately lead to realities the ‘Western

left’, in particular the left in Europe and North America, finds very hard to

immediately understand. But they are based on the social realities analysed

below. For example, this is the evaluation of Fidel Castro, the greatest

Marxist/socialist leader ever to have lived in the Western hemisphere, of

China: ‘If you want to talk about socialism, let us not forget what socialism

achieved in China. At one time it was the land of hunger, poverty, disasters.

Today there is none of that. Today China can feed, dress, educate, and care for

the health of 1.2 billion people.

‘I think China is a socialist country, and Vietnam is a

socialist nation as well. And they insist that they have introduced all the

necessary reforms in order to motivate national development and to continue

seeking the objectives of socialism.

‘There are no fully pure regimes or systems. In Cuba, for

instance, we have many forms of private property. We have hundreds of thousands

of farm owners. In some cases they own up to 110 acres. In Europe they would be

considered large landholders. Practically all Cubans own their own home and,

what is more, we welcome foreign investment.

‘But that does not mean that Cuba has stopped being

socialist.’

Of China’s current president Xi Jinping this was the evaluation of Fidel

Castro: ‘‘Xi Jinping is one of the strongest and most capable revolutionary

leaders I have met in my life’. The left in China clearly supports Xi Jinping –

naturally not without abandoning their specific views but clearly as regards

the overall course of China. For exactly the same reason the capitalist press

in the West is particularly full of bile and hatred against Xi Jinping –

innumerable articles spewing out attacks on him as the 70th

anniversary of the creation of the PRC approached.

It is not necessary for the Western left to become involved

in detailed assessment of China’s leadership – although for China this is

extremely important. What the international left does have to understand is

that the greatest rapid improvement in the condition of the greatest proportion

of the world’s population in human history has taken place in the 70 years of

the PRC.

The role of the socialist left

For the mass of the population who live in Europe or North America it is difficult for them to imagine what it meant to make a socialist revolution, and to commence constructing a new society, from an economic starting point lower than their own countries in the Middle Ages and in only 70 years to achieve a standard of living and a life expectancy that is on the verge of high incomes economies. Only China’s continued development will convince the mass of hundreds of millions of people. That is why there is a much wider and more understanding of China’s stupendous achievements in Africa, developing Asia, and Latin America than there is in Europe or North America. But what there is no excuse for is that parts of the so called ‘intelligentsia’, who are supposed to understand the course of human history, do not grasp such facts.

The following article, written for China for the 70th anniversary

of the creation of the People’s Republic, focuses not on the data on GDP but on

the most important factor or all – the impact of the 70 years of the Peoples

Republic of China on the life of the Chinese people.

* * *

‘The Chinese people have stood up,’ the title of this famous

speech by Mao Zedong in 1949 embodied a promise made by the Communist Party of

China to the people of China. This promise was that if China adopted the

socialist programme and methods of the CPC the Chinese people would be

progressively lifted from more than a century of poverty, foreign invasion,

foreign oppression, and humiliation by foreign powers to regain a position in

which no country or people in the world was superior to China.

Measuring China’s social progress

There are numerous ways to measure whether the promise by

the CPC was kept. A number specifically relate to China’s specific national

identity and its situation in 1949. For example, in a total transformation of

China’s position from the preceding century, no country any longer dares

militarily attack China – due to the strength of the People’s Liberation Army

(PLA) and the economic and technological power that now sustains it. China has

now also completely regained its territorial integrity – all former foreign

concession territories in China have been abolished, Hong Kong and Macao have

reunified with China, only US controlled Taiwan province still remains to be

regained practical control of and that is only a matter of time. Numerous

foreign countries now seek friendly and equal relations with China. That the

socialist path of the CPC has delivered its 1949 promise on the field of

China’s national integrity is beyond doubt.

But it is also legitimate to make international comparisons

by more universal and less specifically national criteria – those regarding the

development of the overall social position of the Chinese people compared to

other countries. Fortunately, since 1949 the situation of humanity as a whole

has advanced – the old colonial empires have been destroyed, living standards

have improved, life expectancy has increased. How has China developed in

comparative terms? Has China improved its social conditions more rapidly than

other countries – justifying the CPC’s promise that its programme and methods,

based on Marx-Lenin-Mao Zedong, were the best to achieve China’s rejuvenation –

or do the facts show that other countries have achieved superior social

progress in the 70 years since the creation of the PRC?

Why life expectancy is the most sensitive measure of social progress

Among the different potential criteria that could be used to

measure China’s relative social progress compared to other countries one is in

reality decisive. The declared aim of the CPC is to ‘Serve the People’. In

policy terms its framework is ‘people centre development’ – which is

necessarily integrated with China’s national rejuvenation because China’s

people are overwhelmingly its greatest power and resource. How much, therefore,

in overall terms has the overall condition of the ordinary people of China

improved since 1949? Has the CPC delivered on its promise that its methods

would deliver improvement in the conditions of the ordinary people of China in

a way superior to any other?

One single criterion is in reality sufficient to

dramatically demonstrate the superiority of the socialist path China embarked

on 1949 compared to alternatives. This is the increase in the life expectancy

of the Chinese people compared to other countries. This fact also entirely

adequately demonstrates that the slogan of the CPC, ‘Serve the People’, is not

empty words but is the precise result of the party’s activity.

The reason the criterion of life expectancy is decisive and

chosen for analysis is not simply, or even primarily, that increase in life

expectancy is a universal wish of human beings – although it certainly is! It

is because it is well known to economists that life expectancy is the most

comprehensive and sensitive measure for judging the overall impact of changes

in social and environmental conditions. This is due to the fact that average

life expectancy summarises in one single figure the effect of all positive

social developments (high quality consumption, good health care, improvements

in education, environmental protection etc.)

and subtracts the negative ones (poverty, poor health care, lack of

education, environmental degradation etc. Life expectancy is therefore a more

adequate measure of social well-being than purely per capita GDP – significant

as the latter is, and despite per capita GDP being the single biggest

determinant of life expectancy. As Nobel Prize winner Amartya Sen summarized

regarding the relation between these variables:

‘Personal income is unquestionably a basic determinant of

survival and death, and more generally of the quality of life of a person.

Nevertheless, income is only one variable among many that affect our chances of

enjoying life… The gross national product per head may be a good indicator of

the average real income of the nation, but the actual incomes enjoyed by the

people will also depend on the distributional pattern of that national income.

Also, the quality of life of a person depends not only on his or her personal

income, but also on various physical and social conditions… The nature of health

care and the nature of medical insurance – public as well a private – are among

the most important influences on life and death. So are the other social

services, including basic education and the orderliness of urban living and the

access to modern medical knowledge. There are, thus, many factors not included

in the accounting of personal incomes that can be importantly involved in the

life and death of people.’

By studying the development of life expectancy during the 70

years of the People’s Republic of China therefore in fact what is being studied

is the overall development of the Chinese people’s standard of life compared to

trends in other countries.

The conclusion of such comparative study of international

facts is simple and clear. The CPC has delivered on its promise that its

methods and programme would create results superior to any other – in

particular China’s socialist path of development has achieved results which are

superior to any capitalist alternative. These are not empty boasts, or purely

nationalist rhetoric, but are simply the objective results of the study of

global development since 1949.

Resolving historical debates on China’s development

Carefully establishing the facts on this question also casts

a clear light on key issues in China’s own history, on international discussion

regarding China’s success, on understanding of China’s perception of itself,

and in grasping the role of the CPC and the socialist path of development that