Economics and the debate on immigration IIBy Michael Burke

The now notorious UKIP poster which suggested the entire population of the EU might come to Britain for work is designed to whip up racism. But it contains two fallacies that are unfortunately shared by many people who are not racists, and are therefore worth rebutting. Myth 1

The first myth is that Britain is a uniquely attractive place within Europe in terms of pay or workers’ rights, or social security entitlements. The graphic below was produced by the UNITE union in Ireland in their argument for higher pay. But it is such a good graphic it is worth reproducing as it stands.

Graphic 1. Private Sector Hourly Compensation in Western Europe, € PPPs

Compensation includes both pay and social wages such as pensions and other benefits. The data is in Purchasing Power Parity terms, so that they account for price differentials between European countries. The data is drawn from Eurostat database here.

The compensation for British workers is among the lowest in Western Europe. Britain is not a uniquely attractive destination for economic migration within the EU. Therefore it should come as no surprise that Britain has one of the lower levels of immigration of the Western European economies.

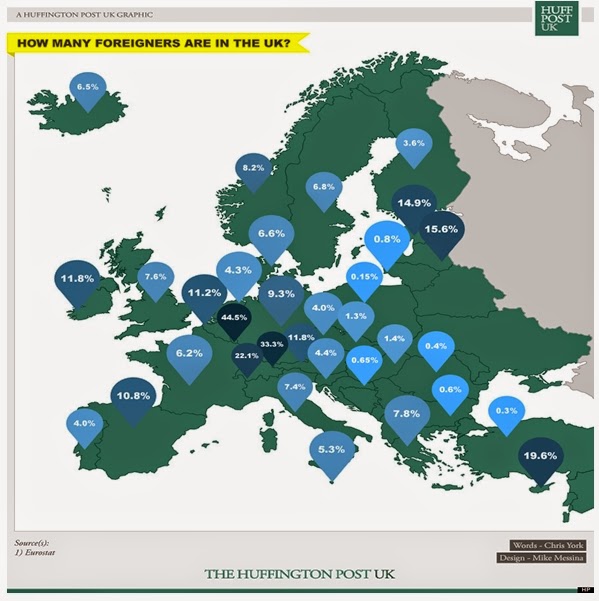

Another graphic, this time from the Huffington Post, illustrates this point very neatly. It shows the level of immigration (the total stock of migrants) as a proportion of the total population. (The data source is also Eurostat).

Graphic 2. Immigrants as a proportion of total population, %

Although there are a series of cultural, historical and legal factors which are important, in general the higher the level of workers’ compensation, the higher the level of immigration. Britain is nearer the bottom on both measures.

Myth 2 The second myth is that immigrants ‘take’ jobs or drive down wages. If that were true, then the introduction of the single market in the EU and with it the provision for the freedom of movement of labour would have led to a convergence of both unemployment and pay rates across the EU.

But we have already noted that the highest pay is in many of those countries with the highest levels of immigration. The same can be said of unemployment too. Immigrants have neither increased unemployment nor driven down pay in those countries. In fact, there has been a divergence in rates of pay in the EU over a prolonged period despite increased mobility of labour.

The argument about immigrants ‘taking jobs’ or driving down pay has strong echoes of (male-dominated) labour movement opposition to women’s entry into the workforce. Exactly the same arguments were used. From an economic perspective the country of origin or the gender of the worker is immaterial. What is relevant is the skills and adaptability of the workforce as a whole.

This is because there is not a fixed ‘lump of labour’ in the economy, which immigrants, or women (or young workers) detract from. If there was a fixed amount of available labour no economy would ever be able to grow, even via the birthrate. Instead, economic activity grows and prosperity increases with what Adam Smith identified as the division of labour and what Marxists understand as the socialisation of production. In the fastest-growing economies of the word, such as China and India, workers frequently migrate internally over vastly greater distances than is required in a move from one small corner of Western Europe to another. Sometimes too, the cultural and even language barriers are also greater.

This migration is a key factor in the growth of all economies. It is primarily responsible for the somewhat better performance of the US economy compared to the EU over a prolonged period. The absence of immigration also partly accounts for Japan’s long-term stagnation.

This is because the movement of labour is a necessary counterpart to the increase in the division of labour, or the socialisation of production. It increases both the size and the capacity of the whole economy. This in turn means that effects of the division of labour are magnified. As a result, immigrants increase jobs as whole. In Britain, 14% of new jobs are created by immigrants (approximately double their proportion of the population).

Consequently, any restrictions on the freedom of movement of labour within Europe will not create jobs but destroy them. They will not underpin pay, but will serve to drive it down. Labour MP Frank Field, who is strongly anti-immigration and in favour of restricting free movement of labour within the EU is explicit on this matter. If migrants are stopped from entering Britain to work, those on benefits can be forced to do the work instead. His anti-immigration agenda has nothing to do with protecting workers rights or pay. It is an agenda which supports the interests of capital, not those of labour.

There are some who mistakenly believe there is a genuine left-wing case for curbing immigration. But this is completely wrong. Immigration is a function of increasing prosperity and tends to reinforce it. The only effective way to reduce immigration in Britain is to lower living standards, reduce real pay and increase poverty. It is Britain’s relative decline in living standards which explains which it has lower immigration than most of Western Europe. There is no genuine left-wing case for reducing immigration.

The alternative is a policy aimed at increasing prosperity which is necessarily accompanied by increased immigration. Prosperity and immigration versus poverty with immigration curbs. That is the real policy choice.

No More Austerity – National Demonstration 21 June 2014

Organised by the People’s Assembly Against Austerity

No More Austerity – demand the alternative

National demonstration and free festival Assemble 1pm, BBC HQ, Portland Place (Tube: Oxford Circus) March to Parliament

Speakers and performers include: Russell Brand Comedian Francesca Martinez Comedian Owen Jones Journalist Christine Blower National Union of Teachers Jeremy Corbyn MP Sam Fairbairn People’s Assembly Stephen Morrison Burke National Poetry Slam Champion Kate Smurthwaite Comedian Sean Taylor Singer / songwriter Caroline Lucas MP Len McCluskey Unite the Union

It is the Tories who have a 30% strategyBy Michael Burke

Ed Miliband is accused of having a ‘35% strategy’, meaning that he is banking on doing only just enough to win an overall majority at the next general election. Polling models suggest that 35% would be enough for Labour to achieve an overall majority in Parliamentary seats. This is because the Tory vote is increasingly concentrated, while Labour’s is far more widely spread geographically.

Since Labour’s electoral strategy has not been divulged to SEB, it is idle to speculate on it, although this has not prevented others from doing so. Instead, it is possible to demonstrate that the Tory policy is based on an electoral strategy that is focused on an even narrower section of the electorate. It is the Tories who have a 30% electoral strategy.

The map below (which the present author first saw published by Ian Wright MP) shows the cumulative effect in English constituencies of cuts under the Coalition government during this parliament. The Tory Party is a fringe grouping in Scotland and is headed in that direction in Wales. Despite repeated attempts it has also failed to resurrect Conservative Unionism in Ireland.

Chart 1. Cumulative effect on change in spending power 2010/11 to 2015/16

The areas in beige have been barely affected by government cuts (although these are averages, there will be many people living in those areas who are badly affected by austerity). The areas in green have experienced no net cuts at all.

By contrast, areas coloured in red have seen a fall in living standards of between 15% and 20%. Those areas coloured deepest red have seen falls of greater than 20% and take in all the large cities, including London. The economic map almost precisely coincides with the electoral map of Britain. The Economist and others are keen to argue that this is a North-South divide in British politics. To that end, they are obliged to perform some logical contortions. In order to make the main divide in British politics North versus South, The Economist excludes the Midlands from the North and excludes London from the South!

The economic response of the Coalition government led by the Tories is to protect and promote those Tory heartlands, as shown in Chart 1 above. SEBhas previously shown how a minority of society, the owners of capital and the rich, are benefitting from the ‘recovery’ in which most people’s living standards continue to fall.

Perhaps the most flagrant policy in this regard is Osborne’s ‘Help to Buy Scheme’. The entire policy of increasing demand for housing while doing nothing to increase supply inevitably leads to higher prices. A number of commentators and economists from the Right have attacked the scheme as an absurd policy, designed solely to boost property prices rather than housing availability. It is a ‘help to get re-elected’ scheme. The resulting property price bubble is concentrated in London and the South-East, and even here there is growing resentment at the unaffordability of housing, not a feel-good factor.

Politically and economically, the Tories are pursuing a core vote strategy. This may not amount to much more than 30% at the next general election, and will certainly be less than the 36.9% they received in 2010. As a result, support for the LibDems has collapsed as this does not at all coincide with the interests of their electoral base, higher-paid workers, professional classes and small business owners.

Labour’s winning electoral strategy should be equally clear and substantially broader. In terms of political geography it should embrace the democratic demands for greater national rights within the British state, as well as finally ending the British presence in Ireland. It needs to have a programme of economic regeneration for the North and the big cities. It should adopt a very large scale programme of council house building with London at its centre-piece. Socially, it needs to be a champion of equality and democracy, tackling the huge inequalities faced by women and tackling the endemic racism of British society, which cannot be done while promising to be tough on immigration.

Above all now, it needs to reverse the policy of austerity which is lowering the living standards of the overwhelming majority and will continue to do so. The Tory policy, of government spending cuts and inducements to the private sector to invest has not worked. A policy of government-led investment is required, combined with other policies that will directly lift standards. The Tory party is pursuing a narrow electoral strategy to shore up its support. Labour can offer something better.

A new situation requires a new analysis, and each new factor in the situation requires a specific and concrete analysis, placing it and its weight correctly in the overall situation.

In world politics, the new situation is that the US was unable to bomb Syria, it finds itself negotiating with, rather than bombing Iran, and its coup in the Ukraine may not be entirely successful in drawing Russia’s neighbour into NATO’s sphere of influence.

This overturns recent history. The overthrow of the Soviet Union in 1991 was accompanied by the US-led Gulf War. Since that time, the US and its various allies have bombed, invaded or intervened in Somalia (twice), Yugoslavia, Haiti, Afghanistan, the Philippines, Liberia, Iraq, the Maghreb, Yemen, Libya, Pakistan, Libya and South Sudan. The US has also led, organised or outsourced countless other interventions, overthrown governments and destabilised economies in pursuit of its interests. There has also been a series of coups and attempted coups in Latin America with varied success, and the so-called ‘colour revolutions’ in Eastern Europe to install pro-US, pro-NATO governments, as well as the US hijacking of the Arab Spring.

However, the economic rise of China has warranted a strategic ‘pivot’ towards Asia in an attempt to curb the rise of the only economy that could rival US supremacy in the foreseeable future. Given this absolute priority and the reduced circumstances of the US economy, it has been necessary to suspend new large-scale direct military interventions elsewhere.

This curb on US power has had immediate and beneficial consequences for humanity. Syria could not be bombed and neither could Iran. In these, Russian opposition to US plans was a key political obstacle, especially as the US wanted to deploy multilateral and multinational forces to do its bidding and needed the imprimatur of the UN Security Council. The US response to this blockage has been to increase pressure on Russia, most dramatically with its ouster of the elected Ukrainian government in a coup and its attempt to breach the country’s agreed neutrality by bringing it into NATO.

This curb on US power, however limited or temporary, should be welcomed by all socialists, by all democrats and simply by all those who desire peace. Instead, we have the strange spectacle that some on the left have raised the charge that Russia is imperialist, or that China is, or countries such as Brazil, or India or South Africa are‘sub-imperialist’!

This is not a coincidence. In the US State Department’s frustration it has produced every type of calumny against Putin, including that he is an imperialist[i] and akin to Hitler. Self-styled socialists who simply echo these charges are not highly amenable to logical argument. But it is vital for socialists to understand the nature of imperialism and its current manifestation[ii].

Lenin’s stated aim in writing the work was to demonstrate that the 1914-1918 war was imperialist (that is an annexationist, predatory, war of plunder) on the part of both sides; it was a war for the division of the world, for the partition and repartition of colonies and spheres of influence of finance capital, and so on.

Furthermore, he argued, that the character of the war, its class character, was determined by the position of the ruling classes of the warring countries and of the whole world, as the ruling classes of the belligerent countries had between them annexed almost the entire world. Therefore, he concluded imperialist wars are absolutely inevitable under such an economic system, as long as private property in the means of production exists[iii].

However, Lenin was categorical in warning that this was a study of imperialism in a given historical epoch and this was specifically (or concretely) ‘a composite picture of the world capitalist system at the beginning of the twentieth century’. As shown below, he also highlighted how this composite might change, as it was already changing.

Therefore it completely contravenes Lenin’s injunctions in this and other works, indeed it is completely alien to the method of Marxism, to abstract from his pamphlet one or two important features of imperialism at this point, and use them as a measuring rule for modern imperialism. Imperialism, like all phenomena, must be analysed concretely, and only after taking all the main factors into account, and so establish its laws of motion. Changing politics

Three decisive changes in world politics have occurred since Lenin wrote his great work. As we shall see, the world economy has not stood still either, like all phenomena it too has continued to ‘flow’, in Lenin’s words.

The first decisive political change was in the contest over who would be the dominant imperialist in the world, which began in 1914 was resolved by 1945. The US had become the single dominant imperialist power and would countenance no serious rivalry from other imperialists. The best they could hope for was to play some subordinate but mutually beneficial role as a junior ally of US imperialism.

The second decisive change took place between in the short period between Lenin’s writing the pamphlet and its later Preface. The Russian Revolution meant that for the first time the working class was able to lay hold of and maintain state power. Since that time, and notwithstanding the overthrow of the Soviet Union, there have been continuously some parts of the globe where the working class holds state power, including Cuba, Viet Nam and Venezuela. Of these workers’ states by far the weightiest in the world economy is China. In all these cases, private property in the means of production is not the dominant form of ownership in the domestic economy. However, all are obliged to operate in a global capitalist system in which imperialism dominates.

Taking advantage of this contradiction, the third change is that the anti-colonial and national liberation struggles were able to free the great bulk of humanity from burden of direct colonial rule, and in some cases this led ultimately to socialist revolution.

These three facts, US supremacy within the imperialist bloc, the continuous existence of workers’ states and the wave of direct decolonisation, are entirely new factors. They are decisive in understanding that the main antagonism in the world is no longer inter-imperialist competition (which has certainly not been abolished).

Now, the pre-eminence of the US and the existence of workers’ states with real political and economic weight means that principal contradiction in world politics is between the US and its imperialist allies versus the workers states and the countries oppressed by imperialism (including the semi-colonial world and the remaining colonies). Of these, the biggest, the weightiest threat to US economic interests is the rise of China. Changing economics

In Imperialism the Highest Stage of Capitalism, Lenin sums up the main economic features of imperialism in that period. To some readers these are well-known, but they are worth repeating here. Worth repeating too is his own characterisation of this definition, which is that it was a special stage in the historical development of capitalism (which has continued to develop).

The five features identified by Lenin are as follows: (1) the concentration of production and capital has developed to such a high stage that it has created monopolies which play a decisive role in economic life; (2) the merging of bank capital with industrial capital, and the creation, on the basis of this “finance capital”, of a financial oligarchy; (3) the export of capital as distinguished from the export of commodities acquires exceptional importance; (4) the formation of international monopolist capitalist associations which share the world among themselves, and (5) the territorial division of the whole world among the biggest capitalist powers is completed.

Lenin’s starting-point is the concentration of production into monopolies, which is the basis of imperialism. This concentration is the inevitable outcome of ‘free competition’ between capitalists and has as a result risen exponentially since the pamphlet was written. Concentration means capitalist rivals are eliminated, and so increased profits require expansion overseas.

The increase in concentration of production and trend towards monopolisation can be illustrated by the fact that the largest companies in the world are now larger than most countries. The tenth largest company in the world has revenues of well over US$200bn, and only 40 countries in the world have a greater level of annual GDP. In Lenin’s time, 44% of all US industrial output was carried out by just 3,000 firms. Now the output of just 130 firms is equivalent to 48% of US GDP[iv].

Concentration of production within the imperialist bloc has also increased. The dominance of the US is evident from the fact that it boasts nearly one-third of the leading Fortune 500 global firms, the same as its next three imperialist rivals together. At the turn of the twentieth century US Steel was the largest company in the world, with average net profits of US$34million. This is equivalent just under US$1 billion in today’s terms. In 2013 the most profitable company in the world was Apple, with profits of US$42bn. Aside from the few loss-makers, most companies in the Fortune 500 had profits far in excess of US$1 billion in 2013.

The role of banks has also increased, but in an even more pronounced way. Lenin uses detailed data to show that the 9 leading banks in Germany held deposits of 10 billion German Marks. Two banks in the US, owned by the plutocrats JP Morgan and Rockefeller had deposits equivalent to 11 billion German Marks. These were equivalent to US$2.4 billion and US$2.6 billion in 1913 exchange rates. In today’s terms these are equivalent to US$56 billion and US$62 billion respectively. In 2013, Germany’s largest bank Deutsche Bank alone had deposits equivalent to US$727 billion. JP Morgan Chase is the biggest bank in the US which in 2013 held deposits of US$ 1,288 billion. At the same time, Lenin identifies the growth in traded securities to the equivalent of 479 billion French Francs. This is the equivalent of US$ 2,700 billion in today’s terms. But this is a fraction of the current level of international claims held by banks in the imperialist centres, of US$32,859 billion[v].

Taken together these data show that the main features identified by Lenin, the concentration of capital and monopoly and the increasing dominance of finance capital have both become more pronounced and more dominant features of imperialism.

However, value can only be extracted if it is produced. Just as imperialism is a parasitic extension of capitalism, the dominance of finance capital is a parasitic characteristic of imperialism, which leads to its decay. Parasitism and decay

Under a system of super-exploitation, the capitalist has a diminishing incentive to develop the productive forces of the economy as profits can be increased simply by increasing the scope of territory and the number of slaves held by the slave-owners. This was noted by Marx in his analysis of the Southern slave states of America.

In a different context, imperialism too is a system of super-exploitation, one which attempts to embrace the whole world. Marx had earlier shown that the first imperial power, Britain in Ireland, had benefited from a higher rate of exploitation in its colony, with the imperial power ‘pocketing the excess’ profits even beyond the rate of exploitation in their own domestic market. As the brutality and rapaciousness of the regime increases, so too does its parasitical nature. This leads to decay and its vulnerability to competition from a more vigorous system of production.

At the beginning of the twentieth century Britain was the premier trading nation in the world, via its empire. However, Lenin points out that Britain’s profits from its foreign and colonial trade was just one-fifth of its profits derived from its overseas financial investments. Britain had already become a ‘rentier state’, primarily living off these investments.

Britain had run a trade deficit, the value of imports exceeding the value of exports for most of the period from the 1890s to the outbreak of the 1914-18 war[vi]. But the very high level of interest income (or rent) on its overseas possessions meant that the balance on the current account (the combined balance of trade in goods and services plus overseas interest payments) remained in surplus. This overall surplus on the current account ended in the 1930s. Repeated devaluations of the overvalued pound frequently redressed this imbalance by making exports cheaper and increasing the value of overseas interest payments in pound sterling terms. The discovery of North Sea oil also gave a temporary boost, but deficits on the current account have become such a fixed feature of the British economy since that in some official data it is sometimes referred to as the current account deficit, rather than the current account balance.

The deficit on the current account must have an off-setting item to balance it. This is the capital account, the net flows of capital rather than of interest payments or dividends. When Britain fell into a current account deficit in the 1930s it was obliged to become a net importer of capital to off-set it.

As noted above, Lenin had identified the export of capital as one of the key features of imperialism at the beginning of the twentieth century. Only the most hide-bound or scholastic reading of Lenin would then argue that in the 1930s Britain passed from being an imperialist nation to an oppressed one. Instead, the parasitism and decay of British imperialism has led it into a new and more decrepit, leech-like phase. Where Britain has trod the United States has followed. Capital importers

The much greater size of the US domestic market, the consequent scope for increasing the division of labour and the greater productivity of its industries all meant the capitalist mode of production retained a degree of vigour there that had long become a distant memory in Britain. This was reinforced by the pre-eminent position of the US following the 1914 to 1945 world wars.

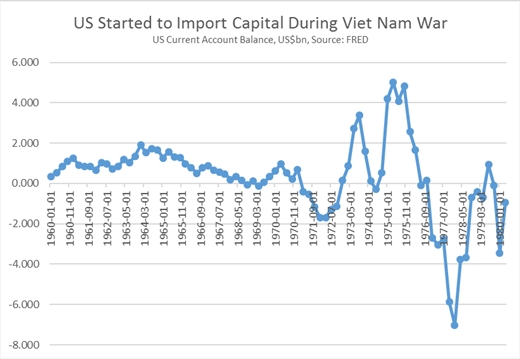

However the US too has become a net importer of capital over a different timescale. This is shown in Chart 1 below. The US became an importer of capital because the growth of the economy was insufficient to maintain both the growth in living standards of the population and to fund the Viet Nam war. The US became an importer of capital in the course of the Viet Nam war and in order to pay for it.

Chart 1. US Current Account Balance 1960 to 1980, US$ billions

Source: Federal Reserve Economic Data

The US did not become an economically oppressed nation while it

was raining more bombs on Viet Nam, Laos and Cambodia than were dropped in the

whole of the Second World War. Instead, imperialism

and the dominant imperialist power has entered a new phase, where it sucks in

capital from the rest of the world. It does so without in advance being

either a net exporter of goods or of capital.

As Lenin and a host of commentators had shown, in an earlier phase imperialism

had been an exporter of capital. By the early 1970s the US (and Britain, long

before) had become importers of capital.

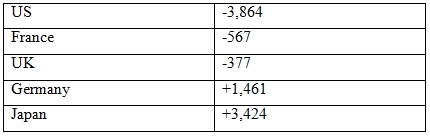

Persistently incurring new net debts will tend to run down any existing net

stock of overseas capital. This is precisely what has happened. The US, as well

as France and Britain are imperialist powers who own no net overseas assets, that is to say, their

overseas debts are greater than their overseas assets. This is shown in Table 1

below.

Table 1. Net International Investment Position 2012, US$ billions

Source: IMF, International Financial Statistics[vii]

The US is the world’s biggest net overseas debtor. It requires

capital inflows to support the living standards of the population while

maintaining the same level of military spending as the rest of the top 10

nations put together. These debts in return require interest payments, which in

turn piles up further debt.

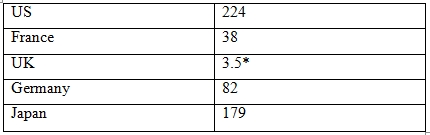

Yet the most remarkable feature of the current economic aspects of imperialism

is that the US, a country which has no net assets but only net debts, achieves

a surplus on its investment income account. The net flows on the investment

income account are shown in Table 2 below.

Table 2. Investment Income Account, Net Flows, 2012, US$ billions

Source: World Bank, Data, Net Primary Income[viii]

Taken

together these five imperialist powers have effectively no net overseas assets,

as the net assets of Japan and Germany are effectively balanced by the net

debts of the US, France and the UK. Yet in 2012 they received a net US$526

billion in net payments of interest and dividends from the rest of the world.

Within this bloc, the US is clearly pre-eminent. It extracted more

interest from the rest of the world than Japan, despite having net debts

greater than the level of Japan’s net assets. France and the UK were junior

partners in this role. By contrast, both Japan and Germany are able to sustain

trade surpluses because of accumulated levels of productivity (and in Japan’s

case severe restrictions on imports). For them, there is no imperative to

engineer investment income surpluses, these are a natural outcome of their

trade-driven accumulation of overseas assets. Even so, along with France and

the UK, they too play a supporting role in the global system of imperialism and

benefit from it.

[* The UK is undergoing a particular period of turmoil in its overseas

accounts, associated with the continuing crisis of its banking system and their

overseas operations. In the prior year the surplus was $42 billion. But it

remains to be seen to what extent the UK can recover this position].

Finance Capital

A capitalist economy is one in which there is generalised commodity production.

Money is the universal commodity, standing in for all other commodities in the

process of exchange. The control over the direction or allocation of money

capital therefore becomes decisive in the development of capitalism itself. The

medium for this allocation is the banks[ix].

As a result, the degree of concentration of capital and the dominance of

monopolies depends on the financial capacity of the banks. The scale of

necessary investment requires access to large-scale savings. The elimination of

rivals requires financial resources. So, the creation of Ford Motors, Standard

Oil and AEG relied on the emergence of JP Morgan, Rockefeller and Deutsche Bank

respectively. This control over the allocation capital places the banks in an

increasingly dominant position in the capitalist economy. Dominance over the

global financial system is the essential condition for dominance over an entire

economic system dominated by finance capital.

As the dominant force in the global financial system, the US directs resources

for its own needs. It charges vastly higher rates of interest when it recycles

capital overseas than it is willing to pay. This explains how it is possible

for the US to draw in interest income when it owns no net assets. At the same

time, the US and its junior partners in France and the UK have not grown as

rapidly as the world economy over a prolonged period, and yet they are

continually able to draw in capital from the rest of the world. This too is

only possible because of the US dominance over the global financial system,

with Britain and France playing an important subordinate role.

The US dominates all global transactions through the trading pre-eminence of

the US Dollar, which accounts for approximately 85% of all foreign exchange

transactions.[x] Firms seeking to raise capital

privately are inspected by the US-dominated ratings’ agencies. Governments are

frequently obliged to apply to the IMF or World Bank, where the US dominates.

The obligatory criteria under which these finances are disbursed, or not,

comprises privatisations, reduced government spending, lower living standards

and financial ‘liberalisation’. These have the effect of allowing greater

access to domestic markets for the imperialist powers, their firms and their

banks, and most especially allows access to domestic savings, which are

required to fund the external deficits of the US and the other imperialists. It

is no accident that the ideology underpinning these criteria is called the

‘Washington Consensus’. It amounts to dominance over the financial system which

dominates the world and gives the US privileged access to its resources.

This is far removed from the era of ‘free trade’, between firms and nations

which ended by the turn of the twentieth century. In any event this frequently

involved robbing the colonies of goods or raw materials for far below their

value, or in many cases simply outright plunder. It is even further removed

from the trade of one large country with another, say Brazil with Venezuela or

China in Africa. These can be mutually beneficial trading relationships, even

while governed by laws of the capitalist market.

Instead, the parasitic imperialist powers are able to conjure capital and

interest from the rest of the world, seemingly out of thin air and on a

repeated basis. It is comparable to free trade only in the way that an armed

robber is akin to a market stallholder. In both cases money changes hands, but

US dominance over the global financial system leaves as little in return as the

robber. And this is not a one-off, but it is a continuous flow of capital.

It is only possible to rob someone repeatedly if a knife is held to their

throat. The extraordinary US expenditure on its military and the willingness of

its French and British aides de camp to support its military adventures (even

their disappointment when the US was obliged to refrain from bombing Syria) is

explained by this imperative to plunder the rest of the world. Military dominance and repeated

shows of military force are necessary to underpin a system of global financial

extortion.

The negative effects of imperial domination are not most frequently felt

through war. This is just the most extreme symptom. Instead, a consequence of

the dominance of the US and its interests in global finance is that even any

changes in the economic or monetary conditions of the US reverberate globally.

Abrupt changes in the US repeatedly manifest themselves as regional or even

global crises. This is shown in Chart 2 below.

Chart 2. US Long-Term Interest Rates and Financial Market Crises

Source: Federal Reserve Economic Data

The

chart above shows long-term US interest rates and some of the main financial

market crises. The yields on US government debt change if there is an

alteration in the balance of supply and demand for capital in the US. This was

the case when Reagan came to office and hugely expanded the US budget deficit.

It has also been the case with (increasingly modest) economic revivals in 1994,

in 1997 and the very mild economic upturn in 2012. In all cases the increased

demand for capital in the US led to a rise in US long-term interest rates.

The consequence was that capital flowed out of the semi-colonial

world and into the US, leaving the former in crisis. This occurred with the

Latin America debt crisis of the early 1980s, the global financial crisis in

the early 1990s, the Asian financial crisis of 1997 and 1998. The recent

‘emerging market’ slowdown is only milder to date because the rising demand for

capital in the US to fund rising consumption has been extremely modest by

historical standards. Yet among the countries most affected by this slowdown

include Brazil, Russia, South Africa, Turkey[xi],

and so on, precisely those countries which are foolishly described as

sub-imperialist, or even in Russia’s case, without the diminishing prefix.

It is only those countries who are able impose capital controls that can partly

insulate themselves from being a store of savings for the US (and face fierce

opposition from the US for doing so). This imperial dependence on capital

inflows is the reason that the US, and its proxies like the IMF are so adamant

that capital movements be ‘liberalised’.

In each case after these major crises the subsequent outflow of capital from

the semi-colonial countries restored the US domestic balance of supply and

demand for savings and so US long-term interest rates declined. But the outflow

of capital left devastation in its wake in the semi-colonial countries

affected.

Increased parasitism, further decay

The impact of US dominance is felt not only in the colonial and semi-colonial

countries but also in the subordinate imperialist countries themselves. As

noted above, in 1994 there was a global financial crisis provoked by an

increased demand for capital in the US which affected all countries unevenly.

While the UK and France attempt to benefit directly from the dominance of the

US and the role of global finance, Japan and Germany remain more closely

related to the archetypal imperialist power of the early twentieth century.

Highly competitive industries and persistent trade surpluses have previously

allowed the build-up of a stock of overseas assets from which German and

Japanese imperialism draw interest from the rest of the world. Consequently,

they have had less incentive to support domestic finance at the expense of

domestic industry. As a result Japan and Germany have much less to gain from

the increased dominance of US-led global finance in the worldwide system of

imperialism.

After 1945, the US aim of bolstering capitalist allies as a bulwark against the

Soviet Union prioritised the rebuilding of war-ravaged Japan and Germany. This

was state intervention to preserve the capitalist system. But it was only after

the US had established its supreme dominance over the rest of the world,

including the subordination of these other imperialist powers through war.

The weight of the imperialist economies is not static, either as a group or

individually. They have undergone a series of dramatic changes. The only

constant is US dominance. Chart 3 below shows the relative weight of these five

imperialist economies in the world economy, both individually and as a group.

The data is shown in the table below.

Three distinct dates are chosen. 1913 represents a snapshot of the world

economy on the eve of 1914-1918 war. 1951 represents the post-1945 settlement.

This is also the highest recorded point of imperialist power on a world scale

as accounted for by share of world GDP and is also the highest recorded level

for the weight of the US in the global economy. 2008 is the final data

available from Maddison before his death, and of course coincides with the

onset of the global financial crisis.

Chart 3

Source: Author’s calculation from Maddison data

The

high-point of these imperialist powers in terms of share of world GDP was 1951.

There has been a sharp decline since that time (which has almost certainly been

deepened by the effects of the crisis). Within that bloc, the US has returned

to its former starting point a century ago, whereas most of the other

imperialist powers have declined in a more marked way. The UK has experienced

the most spectacular fall of all, its weight in the world economy declining by

two-thirds in a hundred years. Japan is the partial exception to this rule,

having been only on the verge of becoming an imperial power at the beginning of

the twentieth century and being utterly devastated by war and nuclear bombing

by the early 1950s.

This still left just 9.5% of the world’s population in these 5 countries to

enjoy the benefits of one-third of world output in 2008. Within those countries

a tiny minority of the population takes the lion’s share. All manner of

chauvinist and racist explanations are advanced for this unequal distribution

of global income, and the accumulated wealth it brings. But in reality it is

only possible if most of the world is dominated by a global system of imperialism, the forcible transfer of incomes

and wealth from most of the world to a minority of it. This system includes

ideological, legal, institutional, commercial and financial strands. All of

these are underpinned by the aggressive exercise of military dominance, led by

the US.

A century ago, Britain had already become a ‘rentier nation’, living off its

overseas income. The factual verdict on this strategy in terms of delivering

growth is devastating. By contrast, Japan’s post-War success was built on very

high levels of investment and favoured nation status in its trade relationships

with the US. Japanese investment as a proportion of GDP rose to what was then

an unprecedented level of 30% of GDP and in consequence GDP growth accelerated

to over 8% per annum.

However this period is already at an end. The Japanese domestic economy has not

been accumulating net new capital for some years and the structural trade

surpluses have become deficits. Growth has also stagnated for 25 years and it

seems probable that like the US, France and the UK, Japan’s net overseas assets

will dwindle towards zero (or below).

A decisive blow was struck by the US against both Japan and West Germany in the

late 1960s. Both countries had been growing more strongly than the US over a

considerable period based on much higher levels of investment. Using the

pressure of its military relationships, in a series of measures the US forced

sharp revaluations of both the Japanese Yen and the Deutsche Mark. It suspended

the convertibility of the US Dollar and finally collapsed the entire post-WWII

Bretton Woods financial system. In this way it was able to disguise a

substantial devaluation of the US Dollar as a widespread but piecemeal

revaluation of other major currencies, while its grip on Middle East oil

ensured this did not lead to an outright balance of payments crisis in the US.

The effect was not to increase US growth but to slow both the Japanese and

German economies for a generation, just as it had used the combination of its

military and financial muscle to devastating effect against France and the UK

during the Suez crisis in 1956. The US later repeated this feat particularly in

relation to Japan, by redirecting Japanese capital towards the US arms race to

bankrupt the Soviet Union in the 1980s. The most important outcome was the

overthrow of the Soviet Union and its reduction to the status of a

semi-colonial country, primarily producing raw materials for the (US-dominated)

international markets. A side-effect was to foster the collapse of Japanese

growth into stagnation, which has been unaltered since 1990.

Inter-imperialist rivalry has not been abolished. But the US has used a

combination of its financial and military dominance to ensure its own dominance

within the imperialist bloc, even as that bloc has been in relative decline.

Conclusion

The concentration of capital and the dominance of finance capital have both

become more pronounced features of global capitalism in the current phase of

imperialism.

Simultaneously, the decayed and parasitical ‘rentier nation’ that Britain had

already become over a century ago is now the norm for the imperialist countries

as a whole and for its dominant country, the United States.

Like an ancient despot, the US and its allies draw in tribute from the rest of

the world in the form of a continuous inflow of capital. There is even a

substantial net inflow of interest income, even though they possess no net

overseas assets, only liabilities.

The main mechanism for this worldwide extortion is the US dominance over the

global financial system, which is itself the dominant sector of capitalism.

This is only possible because it is underpinned by the vast military resources

of the US, which are far greater than all its major rivals combined, and which

it exercises repeatedly and brutally.

Like Britain before it, the US has become a ‘rentier nation’, whose main

overseas income is derived from the exaction of interest and other payments

rather than net trade. But this has entered a new phase, where the tribute of

interest income continues to flow even though there are no assets on which it

is based. Without any net overseas assets, this is only possible because of its

status as imperial power. Imperialism

is a global system of super-exploitation, directed by control over finance

capital and supported by military dominance. The

sole imperial super-power is the US, supported by its allies.

Because imperialism has entered a more decrepit phase does not make it more

benign. On the contrary. The US relentlessly seeks to extend its interlocking

systems of military alliances, trade treaties and financial predominance

because it is in relative decline. The vampire always seeks fresh blood.

Using ‘imperialism’ as a term of abuse, or even as a synonym for a large

trading nation, albeit one possessing nuclear weapons, is to rob it of all

scientific value. The fact that US imperialism can occasionally be challenged

or stymied by some combination of semi-colonial countries and worker’s states

acting in concert does not alter the essential meaning. Instead, these

challenges are a reflection of the relative economic decline of the imperialist

powers in general combined with a growing and related war-weariness on the part

of the population. The US insistence on its own supremacy within the

imperialist bloc has only exacerbated that collective decline, while preserving

its own dominant status.

Rather than echo the frustrations of the US State Department, socialists and

communists welcome the current impotence of the US, for however long it lasts

and however limited it is. In 1997 a triumphalist US imperialism set out its

bold plan to brook no global or regional opposition and to be able to fight two

major wars simultaneously[xii].

In 2013 the US and its allies were unable to begin bombing Syria.

Imperialism is the enemy of all humanity and its set-backs or defeats are a

cause for celebration as they represent an advance for all humankind and the

struggle for socialism.

[ii] As

the US became free to engage in increased military adventures with the collapse

of the Soviet Union, there arose a concerted effort to disguise this by arguing

that ‘imperialism’ was a diffuse and unspecific phenomenon. Hardt and Negri led

the way in ‘Empire’arguing that ‘imperialism has no

address.’ Imperialism is a global system of exploitation, but it has a sole

superpower protagonist which is headquartered in Washington DC.

[iii] This

essay cannot possibly do justice to the scope of Lenin’s work, which relied on

exhaustive and voluminous research in a host of languages. The notebooks for

his pamphlet encompass hundreds of works, in Volume 39 of his Collected Workshttps://www.marxists.org/archive/lenin/works/cw/volume39.htm . However, with access to modern and

publicly available databases it is possible to analyse some of the most

important features identified by him and to update them in light of factually

altered conditions. This can be done without the volume of work that Lenin was

obliged to do, and should be done by socialists seeking to understand the

development of capitalism.

[ix] Lenin

drew on Hilferding’s ‘Finance Capital’http://www.marxists.org/archive/hilferding/1910/finkap/ which analysed the dominance of

finance capital beginning with the role of money which ‘stands in the place of’

all other commodities.

Facts can be a very severe judge. Either economic structures, the models used to explain them and economic policies work, or they don’t. The factual verdict alone can determine who was right, what was successful, what economic system works best.

The chart below is reproduced from The Economist. It shows the change in the IMF’s own estimates and forecasts of the level of US and Chinese GDP. Previously the IMF’s projections were that China would surpass the US as the world’s largest economy in 2019. Its revised estimates are that this will now occur at the end of this year. From 2015 onwards, when anyone refers to the world’s largest economy this will be China, not the US.

Chart 1. IMF Estimates & Projections of US & China GDP, PPP $ trillions

By any standards, this is a momentous econmic event. The leading position in the world economy does not change with great frequency. The US surpassed China’s GDP at some time around 1890, having already overtaken Britain in in 1872. (The Financial Times is incorrect to place this earlier data as the key turning-point- it seems to have ignored China altogether).

In this sense the current reversal is a return to the norm. China’s economy, with a population of 1.3 billion people should be larger than the US. At the same, this higher population level means that per capita GDP is still much below countries like Britain or the US, although this gap too is narrowing rapdly.

As a result, it would be foolish to argue Britain should ‘copy’ China. Different geographies, different relationships with the world economy, different histories and different levels of current economic development would make that an impossibility.

But the Chinese economy has delivered exceptionally strong growth, and grown much more rapidly than the Westen economies over a very prolonged period. In 30 years of the process of reform and opening up from 1978 to 2008 it has raised average living standards from the British level of the 15th century to the same as Britain in 1948. No doubt the advance since 2008 has been equally impressive (probably to something like the early 1960s in Britain).

Larry Elliott in The Guardian points out that Chinese per capita incomes are still way below those of the US. This is true. But the divergence in these trends is also marked. The population of the US has been growing more rapidly than China, while the US economy has been growing much more slowly. This had led to two effects. The first is that in the same 40-year period Chinese per capita GDP has gone from being approximately 5 per cent of the US level to over 20 per cent by 2008.

The second effect is that the growth in population is only a small fraction of the overall contribution to Chinese growth and is a very large contribution to US growth. This is shown in the Table below.

Table 1. US, China, GDP, per capita GDP and population growth 1990-2008

(average annual compound rate, %)

Source: Maddison

The result is that Chinese GDP has been growing by over 5% more than the US over a prolonged period and that Chinese per capita GDP has been growing by over 5.5% more than the US. This growth gap increased during the slump but was resumed again in 2013, when Chinese GDP grow by 7.4% and the US grew by 2.3%.

Mathematically, the effect of compounding is anything that grows annually by 5% will double in size every 15 years. On relative terms, if the current growth gap were maintained the Chinese economy would be double the size of the US economy by not later than 2030. Living standards will catch up later, only because the starting-point is lower.

It would seem foolish to wait until China has achieved living standards comparable to the richest countries in the world before recognising that something could be learnt from its continuous growth.

This is especially pertinent in Britain. The relative decline of the British economy has taken place over such a prolonged period, and had been so pronounced that there is an entire cottage industry devoted to discussing it. A Google search for ‘book + British economic decline’ yields an enormous number of results.

Yet the reality of Britain’s spectacular economic decline barely registers in public debate about the British economy.Currently a short-lived and debt-driven rise in consumption has been enough for public commentary to become dominated by claims about the strongest recovery in the G7. This is despite the fact that this is the weakest British recovery on record, and (except Italy) all the rest of the G7 have recovered more strongly than Britain.

In reality, economic analysis has mainly become a branch of commentary on the electoral fortunes of the Tory Party. It is no accident that both the electoral support for the Tory Party and the British economy have been in relative decline since the beginning of the 1950s.

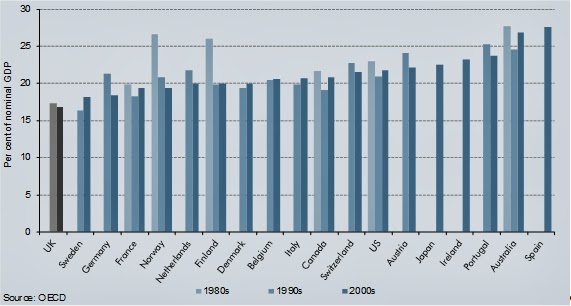

By contrast, anyone wishing to produce policies that would improve British economic performance should study what has been happening in China for decades. There are a number of factors but the key driving force behind continued Chinese growth and improving living standards and British stagnation and relative decline is the proportion of GDP directed to investment. This is illustrated starkly in the chart below from the Office of National Statistics. This shows the proportion of GDP devoted to investment is selected major economies.

Chart 2. Gross Fixed Capital Formation, % of GDP

Source: ONS

Britain has had the lowest share of GDP directed towards investment for many decades and it has been on a downward trend since the late 1980s. The Chinese ‘reform and opening up’ process began with exceptionally high levels of investment as a proportion of GDP and this has been on a rising trend. Although other factors are important, this is the main driving force behind the differential in growth and the change in living standards.

There is nothing inevitable about learning from the successes of others. It is quite possible to continue to muddle along with stagnation and decline for a very prolonged period. But ignoring reality cannot change it. The facts are that China is an astonishing economic success, and Britain has experienced one of the most spectacular relative declines in economic history. Learning from the Chinese experience, and applying its lessons to the specific conditions of other national economies will be an important contribution to economic policy around the world in the decades to come.

If this is a recovery, why are we getting poorer?By Michael Burke

At a certain point this year GDP will finally recover its pre-recession peak, 6 years or more after the recession. This will be the longest British slump in living memory and the most severe downturn since the Great Depression.

The government and supporters of austerity are keen to emphasise the fact that the economy is growing. The latest piece of supportive commentary comes from the IMF, which is projecting 2.9% GDP growth for the British economy in 2014, the fastest growth projected for any G7 economy.

Politically this is entirely understandable. Yet the problem remains that support for the Tory Party continues to flat-line at around the low 30s as a per cent of the opinion polls. Economically this reflects two different forces at work in the economy.

The economy is expanding at a very moderate pace, especially in light of the depth of its previous slump. But the majority of the population are continuing to experience a decline in living standards. Logically, it follows that as total output is growing, a minority must be experiencing a rise in living standards.

This is exactly what is happening currently. This widespread disaffection with or hostility to the government is fuelled by the general decline in living standards. The minority bedrock of support for the Tory party currently is cemented by a rise in living standards for a certain proportion of the population.

The chart below (Figure 1) shows the level of per capita GDP and Real Adjusted Household Disposable Income (RAHDI). RAHDI takes into account all the income of households, interest, rent, and social security as well as wages, after inflation and direct taxes are deducted. It is adjusted for the change (reduction) in public services.

While GDP per person peaked at just under £25,500 in 2007, RAHDI continued to grow and even in 2010 it was still above the 2007 level. That is, wages and benefits grew a little in the first part of the recession and taxes did not increase. The effect of the austerity policy is to push down both wages and social security entitlements so RAHDI fell continuously from 2010 onwards and it fell again in 2013.

Fig.1 GDP Per Capita & RAHDI, £ Thousands (Source: ONS)

Yet the ONS also reports that real household wealth has risen by £1,560 billion between 2007 and 2012, reflecting the rise in financial assets such as stock markets as well as the rise in home prices. This is an increase in financial wealth equivalent to one year’s GDP in Britain in the space of just 5 years. A further rise seems certain to have taken place in 2013.

This increase in financial wealth (shown in Figure 2 below) has occurred at the same time as living standards for the majority have fallen, as measured by RAHDI. The dual effect is a function of government policy in which VAT has risen, public services have been cut and public sector pay and pensions been cut in real terms, while the corporation tax rate has fallen from 28% to 20% and there are innumerable schemes to subsidise consumption, most notoriously ‘Help to Buy’ which has fuelled a further overheating of house prices. Only owners of two or more homes have any direct interest in rising house prices.

While this situation has highly negative and potentially dangerous economic consequences, the current dynamic in the British economy does serve to illustrate an important point about economic theory, with immediate and significant consequences for the incoming Labour government.

There is no such thing as ‘consumption-led economic growth’. Economic growth is a function of the amount and quality of the capital and labour deployed, as well as some contribution from technological change (‘Total Factor Productivity’). As consumption is not an input to growth, it cannot ‘lead’ it.

Most of the population is currently experiencing falling living standards while GDP is edging higher. This is because the main component of growth is consumption. This is shown in Figure 3 below.

In the latest data for the 4th quarter of 2013 GDP is still just over £22bn below its pre-recession peak. The only major expenditure component of GDP which is still significantly lower is investment (Gross Fixed Capital Formation). Investment is nearly £51bn lower. By contrast, government spending and net exports are both higher than when the recession began and household consumption is just under £7bn below the pre-recession peak. Consumption, including consumption by government has recovered. Household consumption by itself will recover at some point in 2014.

Fig. 3 Real GDP & Component, Q1 2008 to Q4 2013

At the most fundamental level all output can only either be consumed or it can be saved for investment. If output stagnates and consumption grows this can only be by reducing investment. Borrowing to consume simply postpones the reduction of investment in exchange for increased current debt.

This also explains why the current dynamic in the economy cannot be sustained. The accumulation of debts to finance consumption cannot continue indefinitely. The debt will be regarded as unsustainable either by the borrower (currently households) or by the lender (banks or their credit card companies).

At the same time, the continued shortfall in investment means the capacity of the economy is barely growing at all. Unless the capacity of the economy increases, that is the productive forces of the economy are developed, then there can be no increase in living standards.

In Figure 4 below the contribution of private non-financial firms (PNFCs) to the development of the economy’s productive capacity is shown. The red line shows their level of investment (GFCF). The blue line shows their level of capital consumption, which is used up in the production process, through consumption of machinery or equipment, wear and tear and dilapidation. The net contribution is the difference between these two, which could also be regarded as the Net Fixed Capital Formation (NFCF), after taking account of capital consumption.

Fig.4 PNFCs Capital Consumption & Investment (GFCF)

So, in nominal terms the PNFCs net addition to productive capacity was just over £29bn in 1997. On this measure, Net Fixed Capital Formation rose to just under £43bn in 2008. It fell by more than half to £21bn in 2009. But it has continued to decline and fell to a new low of just £14.7bn in 2013. This is less than 1% of GDP.

The ideology that private sector will deliver prosperity is evidently false. The policy of government ‘getting out of the way’ of the private sector is manifestly a failure. Cutting corporate taxes and attempting to finance them by government spending cuts (or increased VAT) has simply led to a debt-fuelled upturn and a net decrease in firms’ investment. The increased reliance on consumption and decreasing role of investment is making most of the population poorer.

To prevent absolute declines in GDP in the near future, net investment (NFCF) must rise. That requires an outright increase in investment. Yet the private sector is clearly unwilling to do this. Therefore only the state can play the leading role in providing the necessary investment that can alone lead to prosperity.

The Campaign for Nuclear Disarmament has produced a new pamphlet, People Not Trident. It argues against the colossal waste of funding needed to a replace the Trident nuclear weapons system. It makes the case that the £100bn saved could be used to invest in a whole host of sectors, housing, education, international development, the switch to renewable energy, and so on.

Almost no area of government spending has been spared from the axe of austerity. Housing, health, education and social security payments have all been cut. Pay and pensions, public sector jobs, even support for people with disabilities have all been hit.

Yet the one important exception to this is the government’s commitment to the replacement of the Trident nuclear weapons system. Yet the total cost of replacing Trident amounts to £100 billion.

To put this in context, £100bn on replacing Trident is approximately equivalent to a full year’s public sector deficit, on current performance.

Chart 1. Budget deficits and Trident replacement costs compared

In the most recent Financial Year the underlying deficit[i] was £110bn. Yet the proposal is to spend £100bn on replacing Trident – almost exactly equivalent to a single year’s budget deficit. This is despite the fact that the stated aim of the Coalition has been to reduce that deficit.

A wide variety of organisations, campaign groups and activists (including the current author) have contributed to the pamphlet to show what could be done with all, or even a fraction of the £100bn that would be wasted on replacing a weapons system of mass destruction,.

Crucially, investment in all these areas has a beneficial spin-off on output in other sectors, on prosperity and on jobs. In the jargon these are known as the ‘multiplier effects’. By contrast, Trident and its possible successor has none of these effects. The economic effect of nuclear weapons systems is a fraction of the initial outlay. This is because immensely high-tech equipment such as this can only be used in the event of global nuclear conflagration. It cannot be used to improve economic activity.

Only a government which wanted to intimidate the rest of the world would waste £100bn in replacing an unaffordable nuclear weapons system. A government committed primarily to the well-being of its citizens would not even consider it.

[i] These data are for underlying deficit. In line with Office for National Accounts practice they exclude two important accounting items; changes to the treatment of the Royal Mail Pension Fund and the impact of the purchase of UK government securities by the Bank of England

.702ZLabour will inherit a crisis not a recoveryBy Michael Burke

For once it seems that the widespread reaction to a Budget was correct. Chancellors usually bury bad news in the detail of a Budget released long after their speech. However the dire electoral position of the Tories means that the main changes were announced with a flourish. The personal income tax rate threshold was raised to £10,500 a year, which the Institute for Public Policy Research has shown mainly benefits the highest earners. In addition, the annual amount of tax-free savings was boosted to £15,000 a year, which is actually close to the average (mean) disposable income in Britain. This was a Budget to shore up the Tory vote among higher earners and savers and staunch the defections to UKIP.

Osborne did nothing to address the economic crisis. This is not because the crisis is over or a self-sustaining recovery is underway. That is a dangerous delusion. Even the forecasts from Office for Budget Responsibility (OBR), which has proved to be significantly over-optimistic on growth since it was established, project only an annual average growth rate of approximately 2.5% over the next 5 years. Embedding poverty SEB has previously shown that a huge gap has accumulated between the current level of economic activity and the previous trend rate of growth. Even if 2.5% GDP growth materialises that gap will not close. At best it will not widen further. The poverty and misery arising from the current crisis will become embedded in the economy.

To arrive at its forecasts the OBR has made the following assumptions:-

Wages will only rise half as fast as GDP growth

Average real wages (after inflation) will not rise at all, yet

Non-wage incomes (salaries, interest and rent) will rise sharply

House prices will rise by over 30%, and

Stock markets will rise by 27%

Even under the OBR’s forecasts it is clear that all the benefits of projected growth are claimed by high earners, the rich and the owners of capital. Even if all these gains were spent by the rich (which is never the case) this would be insufficient to power the growth the OBR is projecting. The main contribution to growth envisaged by the OBR over the next period is a rise in household debt. This is shown in the chart below (Chart 3.33 in OBR data).

Fig1. OBR Projection of household debt

Reversing the post-crash trend, the OBR assumes that households will increase their debt on average from 142% of their incomes currently to 166% by 2019, close to levels preceding the crash. Under these officially-sanctioned forecasts most households will see no rise in incomes, only a rise in debt. They will be worse off in 5 years time than they are now.

It is not necessary to enumerate all the ways in which this forecast might be proven wrong, if for example there are increases in interest rates or inflation picks up because the currency falls, and so on. The key point to note is that for most people the crisis will be an enduring one, at least a decade long. Causes unaddressed

The crisis will continue because its root cause has not been addressed. Currently the fall in investment is approximately three times as large as the entire fall in GDP since the begnning of 2008. Investment has fallen by £58bn and GDP is still £21bn below its previous peak in the 1st quarter of 2008.

In fact, while GDP inches ahead in the longest-ever recession, investment (Gross Fixed Capital Formation) continues to decline. In addition, as the statisticians refine their understanding the most accurate position, the data for investment has mainly been revised lower. This is shown in the chart below (Chart in the OBR data).

Fig. 2 Business investment & its revisions

Total investment in Britain is one of the lowest of all the industrialised economies over a prolonged period (as shown in Fig.3 below, Chart G in OBR data). Business investment is currently equivalent to just 8% of GDP, also one of the lowest. Yet the OBR is effectively forecasting that the problem will disappear.

Fig.3 Total investment as % of GDP in industrialised countries

The OBR forecasts that business investment will rise by 50% in the course of the next 5 years- which has never happened in Britain outside of war. This means investment will be growing approximately 5 times as fast as the rest of the economy- even though, according to the OBR, there will be a tremendous profits squeeze, with profits falling from 33% of GDP in 2012 to 27% in 2018. These are outlandish forecasts. Only a policy to control and direct investment could produce such results.

Meanwhile, minimal wage growth, rising household debt and the investment slump are all related. It is impossible to create new, high-skilled high pay jobs without investment. The government can boast that one million jobs have been created in the last two years. But less than half of these have been for full-time employees and many of those are on zero hours or minimum wages. In order to finance any increase in spending at all, workers whose real wages are falling are obliged to drawn down savings or take on new debt.

This is the mess that the Tories will bequeath to Labour. Only a thorough break from the policies of austerity can solve it.

.260ZThat Tory recovery in perspectiveBy Michael Burke

This week George Osborne will announce his latest Budget. The specific measures in this Budget were not published at the time of writing. But it is a fairly safe assumption that he will boast that the economy is on track, and that there is a recovery. This is simply an exercise in redefinition.

The economy grew by just 1.9% in 2013. This is following a period of historically slow growth, the deepest recession in living memory and the weakest recovery on record. Yet many commentators and not just explicit supporters of austerity seem to believe this means we are automatically on track for a genuine recovery with all that means for growing jobs, rising real pay and improving living standards.

Unfortunately both the celebrations and the optimism are misplaced. Of course this does not mean that the economy will never grow again. It is even possible that growth will be a little better in 2014 than it was in 2013. But after most recessions the economic rebound is usually fairly strong. After a very steep recession the recovery should be very strong. That is not the case currently.

Annual growth in GDP of just 1.9% in 2013 is the best since 2007. But that is really a measure of the crisis of the economy and how badly policy has failed.

Prior to the current crisis, in the 20 years to 2008 the average annual growth rate of GDP was a little under 3%. In the same 20 year period from 1988 to 2008 only 3 years have seen worse growth for the British economy than last year’s 1.9% and all of those were associated with the recession under the Tories in the early 1990s (the ERM crisis).

So, a growth rate associated in the past with crisis is now redefined as recovery and heralded as success. Crisis is redefined as success; stagnation is now growth.

Current growth rates also remain well below the previous trend. That means the gap between where we are and where could or should have been is actually getting wider. It would take many years of sustained growth above that 3% rate in order to close the gap between the actual level of GDP and its previous trend. No major forecasting body suggests anything like that is going to happen over the next few years. The chart below shows the trend growth of Britain’s GDP in from 1988 to 2008.

Fig.1 Trend GDP Growth From 1998

This growing gap matters because it effectively means living standards cannot significantly recover without altering the current structure of the economy. Instead, the misery of the economic slump will become embedded as a long-term feature of the economy.

In all probability living standards for most people will not rise for several years and for many they will fall further unless growth accelerates significantly. Austerity policies have the effect of ensuring that the lion’s share of any recovery goes to a minority of the population.

Most Budget coverage is a deluge of minutiae about minor changes to the tax system. But the most important fact is this: talk of recovery is entirely misplaced. For the overwhelming majority of the population austerity policies mean that living standards will continue to decline.

Conference Highlights include: National Union of Teachers General Secretary, Christine Blower, will be discussing how we make the teachers’ strikes a success and how we bring that energy into the demonstration on 21 June. Kirstine Carbutt, a leading Unison member in Doncaster who has just organised a seven day strike against Care UK, will be relaying her experiences on how to organise successful workplace action. PCS general secretary Mark Serwotka and the People’s Charter will be proposing an alternative to austerity.

Francesca Martinez will be closing the conference talking about why we need a mass movement. Steve Turner, Unite the Union Assistant General Secretary, will report from Unite’s community membership strategy and will be chairing part of the day.

Natalie Bennett, leader of the Green Party, will be addressing the conference about how we bring climate change issues into the anti-austerity movement.

Dr Jackie Davis will propose plans to campaign against the sell off of our NHS.

Lindsey German from the Stop the War Coalition will talk about why the anti-war campaigns need to remain high on the agenda.

And trade unionists, community activists, students and pensioners will be debating the next steps in the campaign against austerity.

Register: https://padelegateconf.eventbrite.co.uk As well as being the democratic body of the People’s Assembly, we want to use the conference as a way to strengthen and grow the organisation. So please do get in touch with trade union branches, campaigns and community groups locally and ask them to send delegates. We will be sending out a formal invitation and model motion which can be adapted to send to local organisations in a following email over the next few days.

We have set the delegate entitlement for local People’s Assembly groups quite high to ensure newer activists are able to attend the conference.

Details in brief:

People’s Assembly Delegate Conference

Date: 15 March 2014 Time: 10am – 5pm

Venue: Emmanuel Centre, Marsham Street, London, SW1P 3DW Nearest tubes: Westminster, St. James’ Park, Pimlico Buses: 88, 87, 3, 11, 24, 211, 148, 507, 53, 453, 12, 159

How to book your delegates places: Book your places through our eventbrite page for the People’s Assembly Delegates Conference now: http://padelegateconf.eventbrite.co.uk

Should you require another format please let us know. Please do get in touch if you have any questions. We have set up a special email address for all communication to do with this event: conference@thepeoplesassembly.org.uk

{kind=link}

{kind=link}

Recent Comments