The rise in inflation is a global trend, but some countries have experienced far worse inflation than others. Britain is one of those; the only country in the G7 where inflation is not currently subsiding. This is because of fundamental economic reasons, related both to G7 policy and to Britain’s economic history.

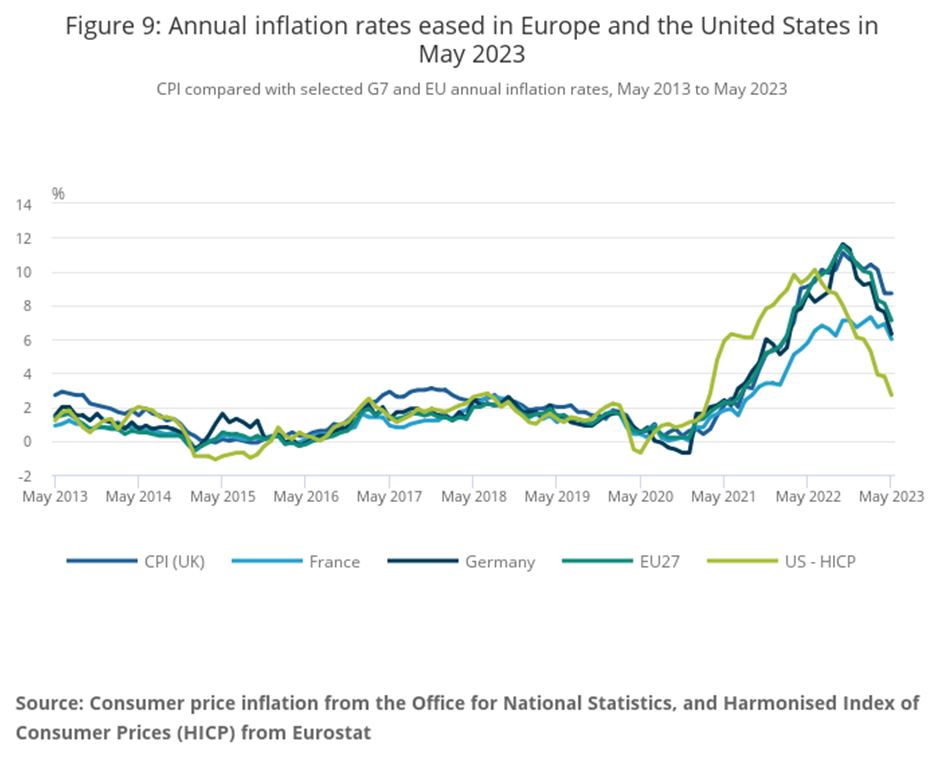

In the near-term the outlook for inflation in Britain is grim. A number of commentators pointed out that in the most recent monthly data to May the annual rate of inflation was unchanged at 8.7%. This means inflation is now higher than France, Germany and the EU as a whole, and much higher than the US, as shown in Chart 1 from the Office for National Statistics (ONS).

Chart 1. Declining Inflation rates in the G7 but not UK

They also point out that ‘core’ inflation, which excludes food and energy prices because of their volatility actually rose on an annual basis in May. Worse, and mostly overlooked, in the latest 4 months data consumer price inflation (CPI) data have risen by 3.9%. That is an annualised inflation rate of over 12%!

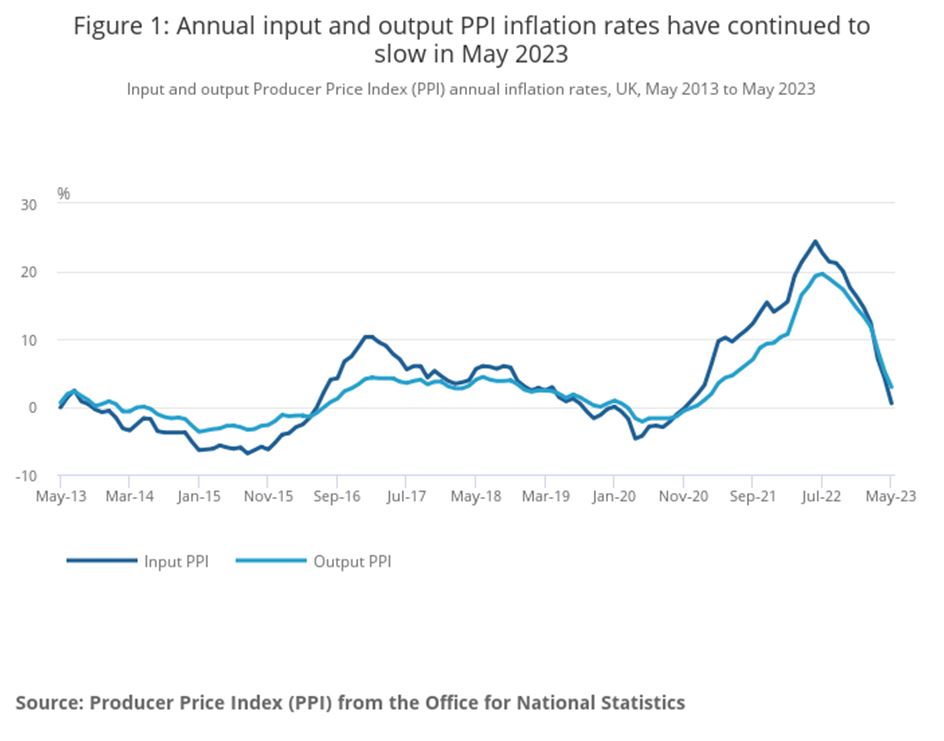

Yet it is a startling fact that cost pressures on producers have been falling for over a year. Producer price inflation (PPI) records changes in the prices of goods bought and sold by British manufacturers including price indices of material and fuels purchased (input prices) and factory gate prices (output prices). Both of these peaked in June 2022, and have now been falling for almost a year. In the most recent monthly data input prices had risen only 0.5% from a year ago and the decline in output price inflation was only moderately less dramatic at 2.9%.

Chart 2. Annual UK input and out PPI inflation rates

SEB has previously shown that all explanations which place the Ukraine war at the centre of the global inflationary trend fall apart confronted with the fact that global inflation began in the US in Spring 2020, almost 2 years before the war began.

That evidence is confirmed in Chart 2, with input price inflation in Britain rising from -4.7% in the 12 months to April 2020 to a peak of 24.4% in June 2022.

This data also explodes the myth that there is any ‘wage-push’ inflation in the economy (in fact a recent study shows that there is barely any historical evidence of wage-push episodes at all). Currently, private sector wages are running ahead of those in the public sector, although both are falling in real terms. It is logically impossible for falling real wages to contribute to rising prices. If there were any evidence of it, it would be shown above all in manufacturing output prices. As shown, output price inflation is low and declining rapidly.

Therefore, the situation in this country is one where price pressures on producers are declining rapidly, yet price pressures on households are rising rapidly. For example, it is virtually impossible now for the Sunak government to meet his pledge to halve the inflation rate to 5% by December. Average monthly rises in the CPI index would need to be 0.2% for the rest of this year, compared to average monthly rises of almost 1% in the last 4 months.

Of course, the key variable between low output prices and rapidly rising consumer prices is profit margins. These have been soaring over recent months. This has become known popularly as ‘greedflation’, and is acknowledged as a real or even the dominant factor by a string of mainstream bodies such as the European Central Bank (ECB), the IPPR, bankers at UBS (pdf), as well as in the pages of the Financial Times (£).

The rise in profit margins has been conclusively demonstrated in research from University of Massachusetts Amherst, which shows US (after-tax) profit margins for non-financial firms at their post-World War II highs. The researchers’ chart is reproduced below.

Chart 3. Soaring profit margins in the US

It should be noted that this surge in US profits is not mirrored elsewhere in the G7, where profits in some cases are stagnating or even declining. It seems as if the US profits’ recovery is largely at the expense of G7 countries, and others.

The fundamental driving force behind the global inflationary wave was the policy mix adopted by the G7 countries coming out of lockdown, led by the US. Both monetary and fiscal policy were used, sometimes in an unprecedented way, to stimulate Consumption without any corresponding policy to boost Investment. The words of Agustin Carstens, General Manager of the Bank for International Settlements bear repeating,

“….monetary and fiscal policy stimulus deployed during the pandemic gave inflation an even larger, and certainly more enduring, unexpected push. As a reminder, policy interest rates were lowered to zero, and often below. Central bank balance sheets ballooned. Fiscal stimulus since the start of the pandemic has exceeded 10% of GDP in many advanced economies – a push previously seen only in wartime.”

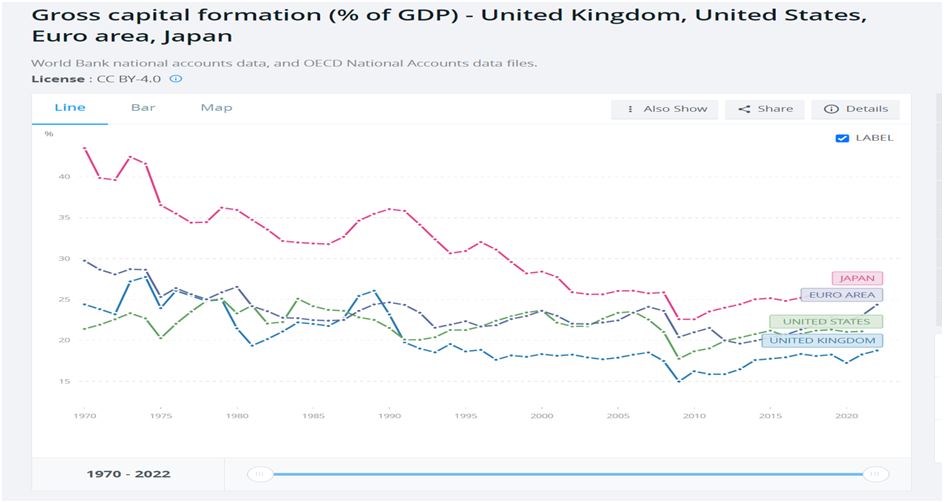

This stimulus to Consumption without any Investment to meet it sparked the global inflation wave. In the G7 countries themselves it also followed a prolonged decline rate of Investment (Gross Fixed Capital Formation), as shown in Chart 4 below

Chart 4. Decline In Rates of Investment (GFCF) in US, Euro Area, Japan, and UK

Source: World Bank

In a country such as Britain, with the persistently lowest level of Investment of all, the inflationary wave has naturally been one of the strongest of all. This is because the gap between the stimulus to Consumption and the structural level of Investment is the widest of all.

In terms of the policy response, the approach of the government was to provide huge fiscal benefits to companies in the form of tax breaks in each of the Budgets since lockdown.

The central bank response has been to realign Investment and Consumption by decimating the latter through high interest rates. As this fails to tackle the underlying cause of the crisis, a dearth of Investment, the only way for this policy to succeed is through potential slump. In neither case has there been any recognition of the cause of the crisis, just lots of propaganda about ‘wage-price’ inflation. As a result, the outlook for the economy is that inflation will remain persistently high and will be broken only by slump or outright recession. The result is that British economy is facing either high inflation or economic contraction or even some combination of the two.

Irrespective of what stance you take on the war in Ukraine, or anywhere else, in March last year, US author Meehan Crist wrote the following in the London Review of Books, “One of the worst outcomes of the war in Ukraine would be an increasingly militarised response to climate breakdown, in which Western armies, their budgets ballooning in the name of “national security” seek to control not only the outcome of conflicts but the flow of energy, water, food, key minerals and other natural resources. One does not have to work particularly hard to imagine how barbarous that future would be”.

Crist’s point is simply to describe the world we already have, but a bit more so; and her prediction is exactly what is happening.

The US has raised military spending to $858 billion this year; up from $778 billion in 2020.

France has announced an increase from a projected E295 billion to E413 billion in the next seven years (an average of E59 billion a year).

German spending is rising sharply, from E53 billion in 2021 to E100 billion in 2022 and is set to go further.

Japan aims to double its military spending by 2028 and is also debating whether to start deploying nuclear weapons.

In the UK, the government’s aim to increase military spending from 2.1% of GDP to 2.5% by 2030 comes on the back of what is already among the highest per capita military spends in the world.

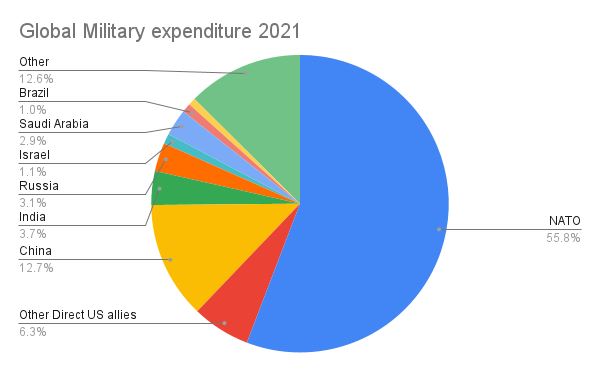

NATO, the core alliance of the Global North, already accounted for 55.8% of global military spending in 2021 before any of these increases.

Other direct US allies – with a mutual defence pact – accounted for another 6.3%.

So, the direct US centred military alliances account for three fifths of global military spending and yet they are now raising it further at unprecedented rates. These are the world’s dominant imperial powers, acting in concert to sustain a “rules based international order” in which the rules are written in, and to suit, the Global North in general and Washington in particular.

The carbon boot print of these militaries is not measured under the Paris Agreement. It is, nevertheless, huge and growing; and we can’t pretend it isn’t. At the moment, the carbon boot print of the US military alone is the same as that of the entire nation of France. This is incompatible with stopping climate breakdown; both in the direct impact of production and deployment, the diversion of funds which are urgently needed to invest in the transition, and the potential impact of their use – which could kill us all very quickly; particularly if nuclear weapons are used. John Bellamy Foster’s Notes on Exterminism for the Twenty First Century Ecology and Peace Movements should be required reading for both movements.

Because this military is not sitting idle. The first phase of the Wars for the New American Century – in the form of the War on Terror since 2001 – have been calculated by Browns University at 4.5 million people; three quarters of them civilians killed by indirect impacts of US and allied military interventions. The scale of this is because doctrines like “shock and awe” are not simply an impressive displays of explosive power, but specifically designed to smash energy and water systems, both clean water supply and sewage treatment, within the first twenty four hours of an intervention to reduce surviving civilian populations to a state of numbed misery and demoralisation. “Why do they hate us?” I wonder. 4.5 million people is about half the population of Greater London, or three quarters of the population of Denmark and twenty two times as many as have died in the Ukraine war so far (assuming total casualties of 200,000, most of them military on both sides). It’s a lot of people. *

Their deployment and use more widely against opponents that are more resilient than Iraq, Afghanistan or Libya- which this escalation of expenditure and increased integration of alliances makes possible – would, even if it did not go nuclear, be catastrophic both in its direct loss of lives but also in the disruption of global supply chains leading to widespread economic unravelling. According to the Australian Strategic Policy Institute, a war in the South China Sea that closed down shipping lanes would have a rapid impact regionally – “Taiwan’s economy would contract by a third, while Singapore’s economy would fall by 22%, according to the baseline estimate. Hong Kong, Vietnam, the Philippines and Malaysia would suffer falls of between 10% and 15%” – but would have a knock on effect everywhere else affecting 92% of global trade. The attempt in the Global North to set up “secure supply chains” – defining economic policy increasingly around military imperatives (“securonomics”) is not to avert such a conflict, but to make it economically manageable, and therefore more likely.

This scale of military expenditure also dwarfs their domestic investment in combatting climate change, urgently needed because the wealthiest countries put the heaviest weight of emissions on the rest of the world, both historically and through their per capita footprints now: let alone helping Global South countries develop without reliance on fossil fuels. This has a wider implication, with the UN Sustainable Development Solutions Network reporting that progress towards the UN Sustainable Development goals has been static for three years.

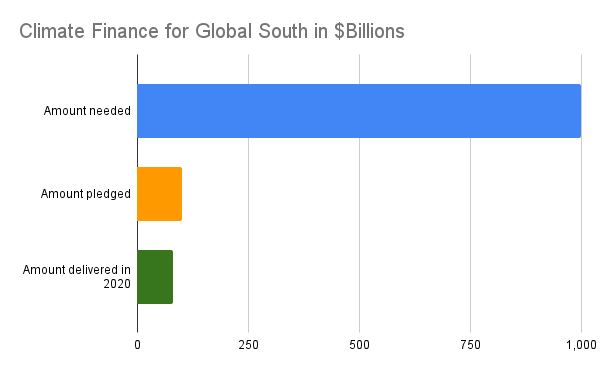

Pledged to commit $100 billion a year to help the transition in the Global South, more than ten years ago, they have never been able to eke out this money, have never hit the target, have tried to use loans (debt trap) instead of transfers, sought to apply conditions and control. The US contribution to that is now aiming for just over $11 billion by 2024. This is now reckoned to be a tenth of what’s needed. This is despite 66% of their populations agreeing that this support should go in, and only 11% against. The contrast with the $77 billion they have stumped up to fight the Ukraine war with no trouble at all in the last year is quite startling. News that Finland is planning to cut development aid to countries in Africa that don’t line up behind the Western line on Ukraine is an ominous sign of how far backwards this could begin to go; with any attempt at global governance through structures like the UN abandoned and notions of international obligation and mutual humanity giving way to even more overtly colonial attitudes and practices than we already have. Although the notion that the Global North can “build a wall” and keep the human consequences of climate breakdown out is a fantasy – as the climate is breaking down behind the wall too – it probably won’t stop them trying.

The USA and its allies pose themselves as “Global Leaders”. They could and should be, as they are the countries with the greatest concentrations of wealth, power and technical know how, communications and education, but they are falling horribly short; because they see leadership as the same thing as dominance – and subordinate everything else to that.

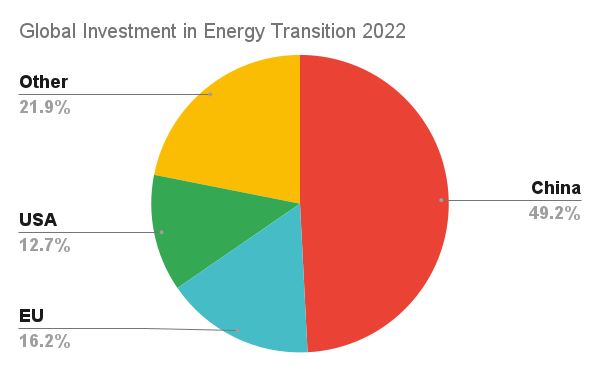

In fact, in 2022, China – usually presented in our media as a negative force on climate – invested 70% more in renewable energy generation than the USA and EU combined, just under half the global total on its own. Next year, according to the International Energy Agency, China will account for 70% of new offshore wind, 60% of new onshore wind, and 50% on new solar PV installations. So, the “international leaders” have a lot of catching up to do.

The US and EU are some way behind, and nowhere near where they need to be. Instead of investing on the scale needed to hold the global temperature increase below 1.5C, they are tooling themselves up militarily to try to deal with the consequences of failing to do so; in an effort to sustain their global dominance. If they are leading us anywhere, its to Armageddon.

A report from the US military in 2019 sums up the paradox. Reflecting that, if climate breakdown continues at its present rate, countries that are already water stressed will be getting beyond crisis point within two decades and that this will lead to “disorder”. Their conclusion was that this means that

1. they will be intervening in these crises, and

2. will therefore need to build themselves in a secure supply chain of water so that the troops who are dealing with people in crisis because their environment has run out of it, will have enough to keep them going in the field!

Reflecting further, that on our current trajectory, climate impacts within the United States itself would lead to infrastructure breaking down, followed by the social order breaking down, followed by the military itself breaking down; as it faced overstretch trying to maintain order as civil society failed. Nevertheless, they also note that the rapidly increasing melt of the Arctic ice shelves and permafrost means that new sources of the fossil fuels that are causing the crisis in the first place to be available for exploitation and that a key task for them would be to make sure that the US gets the lion’s share of them. As a study in self defeating thinking, it can’t be beat.

To repeat the point at the beginning, regardless of anyone’s stance on any given war taking place now, and who should “win” it, its this drive and acceleration of military spending that the climate and peace movements should be combining to hold back – both to avert the growing risk of conflict, because arms races tend to end in wars on the momentum of their own dynamic (which requires a lot of demonisation and conflictual stances to fuel and justify it) and to allow saved funds to be used to avert the climate crisis itself. A bottom line demand is that the military carbon boot print must be accounted for in the Paris Process and a mechanism agreed for reductions to a common per capita level, combined with common measures and investments for increased global cooperation in lock step with it.

*Casualty figures in Ukraine are easy to come by but hard to trust. 200,000 assumes a parity between the Ukrainian and Russian militaries; whereas figures from Mossad, among others, indicate significantly lower Russian losses (at perhaps a fifth to a third of the Ukrainian level) so 200,000 may be a high estimate. One notable feature of this war is that civilian casualties have been a fraction of the military losses – the opposite of the trend from the mid twentieth century onwards; during which “there has been an increase in civilian fatalities from 5% at the turn of the 19th century to 15% during World War I (WW I), 65% by the end of World War II (WW II), and to more than 90% in the wars during 1990’s, affecting more children than soldiers”. From https://www.frontiersin.org/articles/10.3389/fpubh.2021.765261/full#B12

The above article was originally published here on Urban ramblings.

In March Ipsos last published polling outlying public attitudes towards strike action but hasn’t followed up, despite rail strikes ongoing into June 2023 and nurses and junior doctors engaged in ballots for pay and against the under-funding of the NHS. Much of the media coverage has trailed off too. We can assume this is because all the trends show that working people standing up for fair pay through their trade unions still have support from the public.

It was clear at the height of the cost of living, trade union fight back when inflation was high and pay offers were low or non-existent that the Conservative government hoped to rely on the old tropes of blaming hard line unions and that the public would fall in line and agree with how inconvenient it all was. This has led the Tories to putting the Minimum Service Levels Bill through Parliament instead of focus on the job at hand of talks to resolve the disputes.

The public however didn’t agree and vox pop after vox pop showed the general public reluctant to disagree with the trade unions. Faced with a barrage of scandals from the Tory party over their handling of the pandemic, aided and abetted by a decade of Conservative austerity, when asked to choose on balance who they side with, the side that has come out winning in 2023 is trade unions.

What the polling says

YouGov provides some evidence of the trends over the last year, all pretty much saying the same thing.

When asked a series of questions from several angles about support for trade unions, which sections of industry should be allowed to strike and where the Labour Party – the party set up by the trade union movement – analysis of the results point us in the same direction.

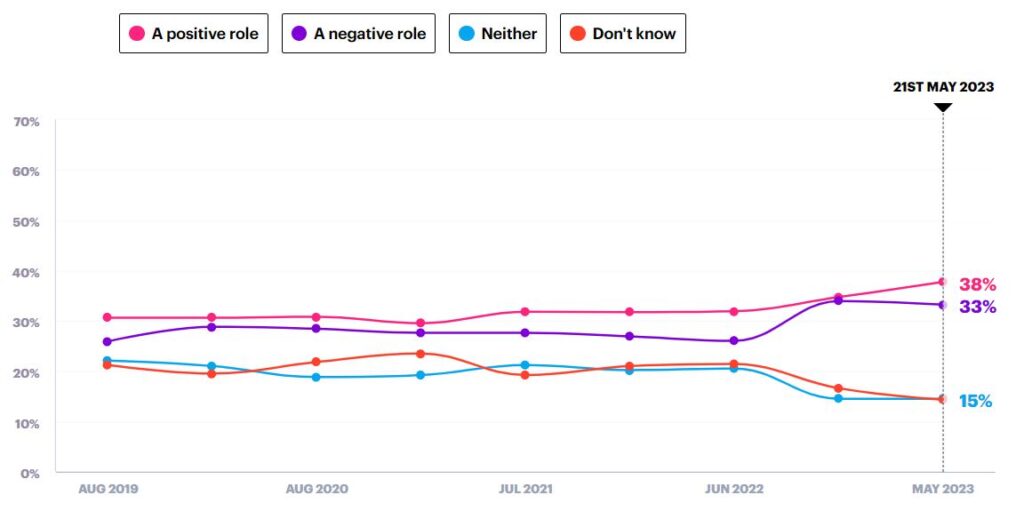

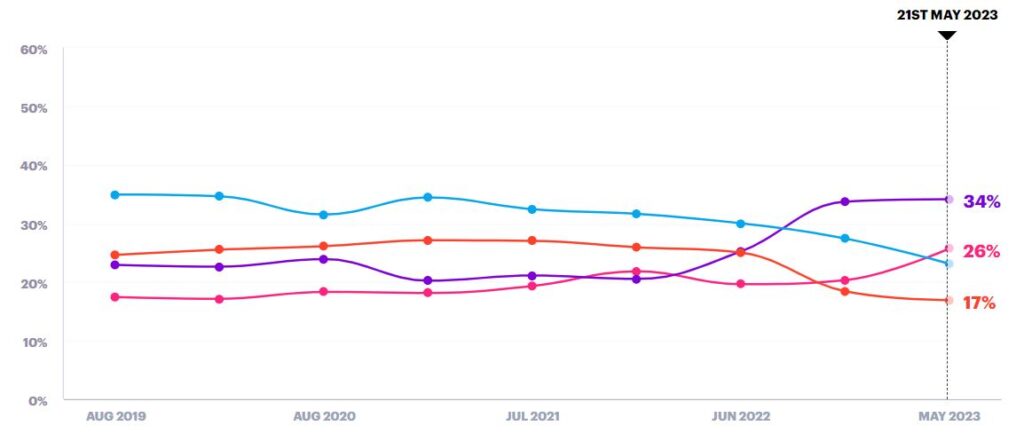

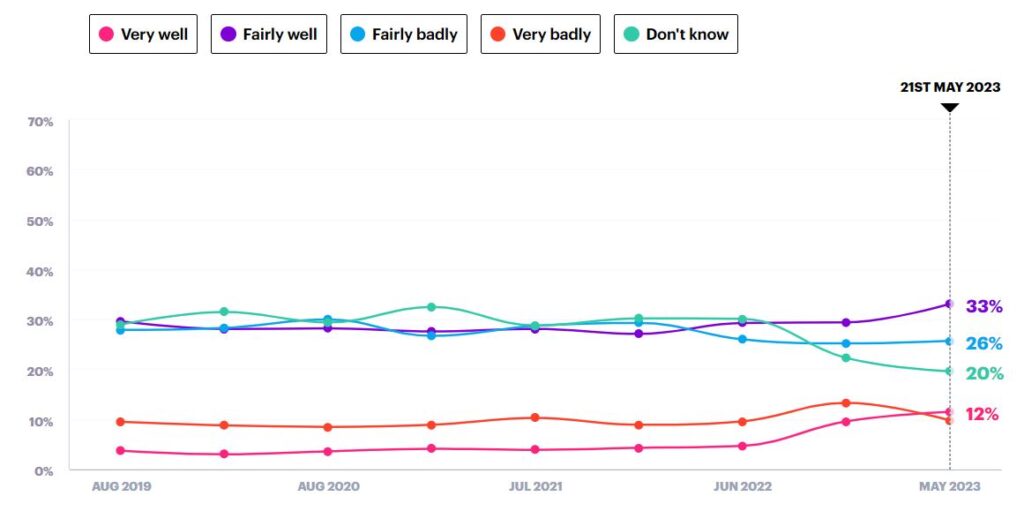

The view that trade unions play a positive role has had greater support than the view that they play a negative role this last 12 months. Those thinking they play a positive roll edging up from 32% – 38% since June 2022 and those thinking trade unions play a negative role has also risen, from 26% to 33%. Despite the negative trend going up over 12 months, this has dipped since November 2022, the period which saw most of the strikes.

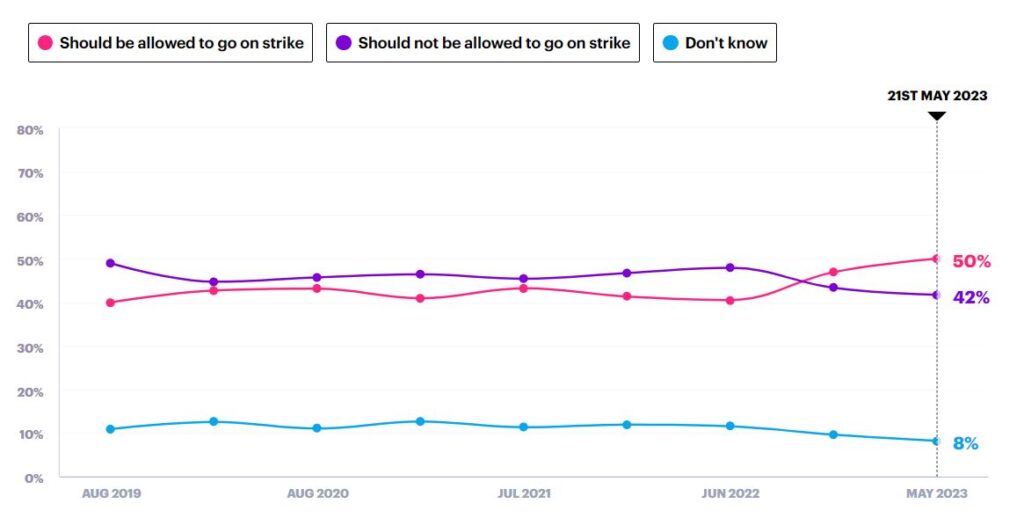

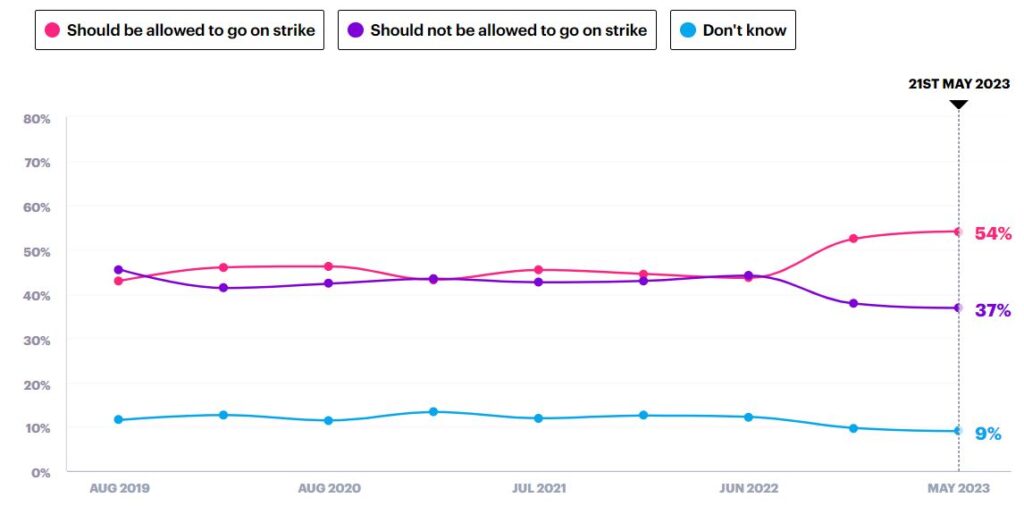

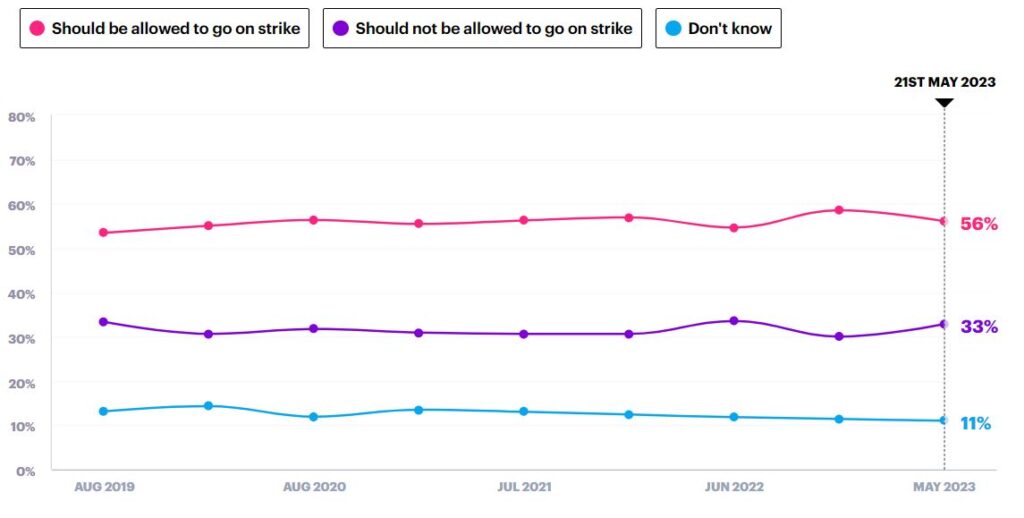

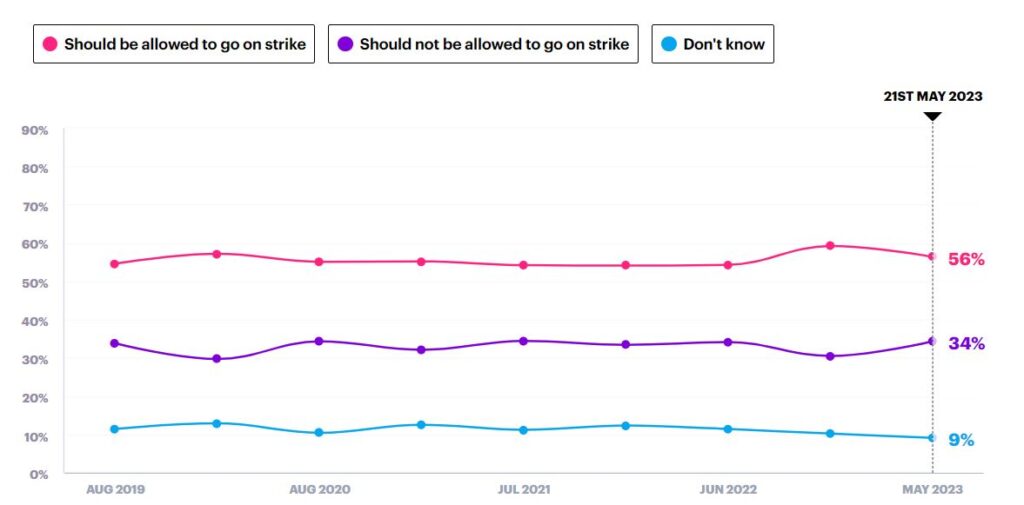

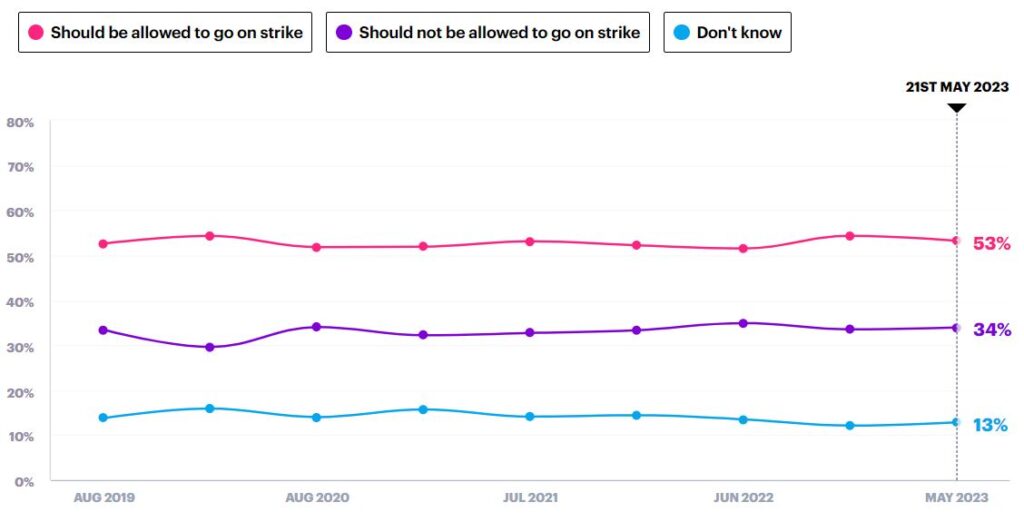

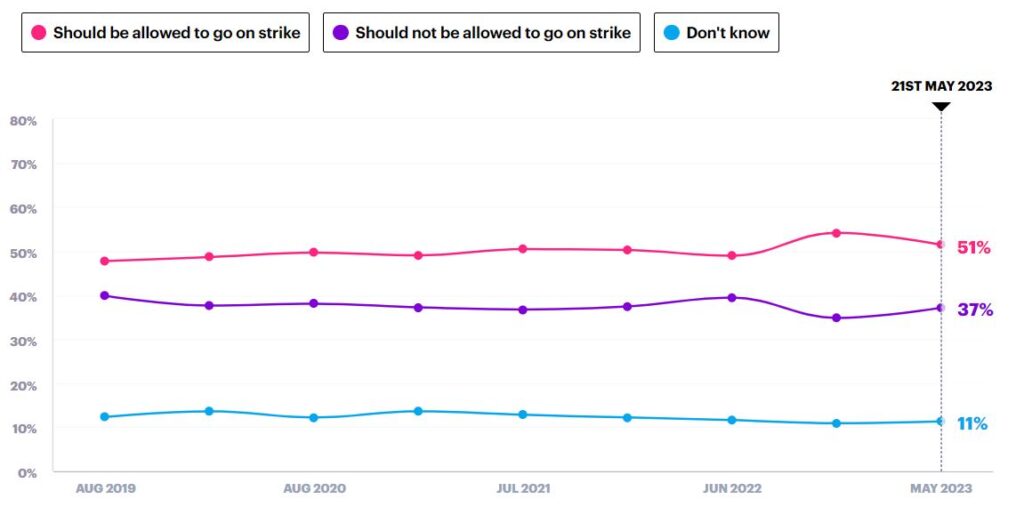

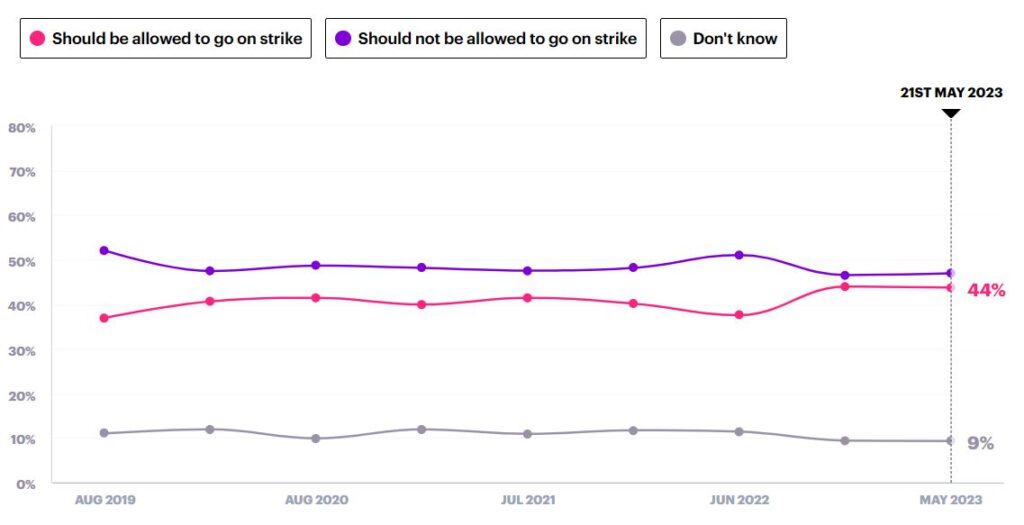

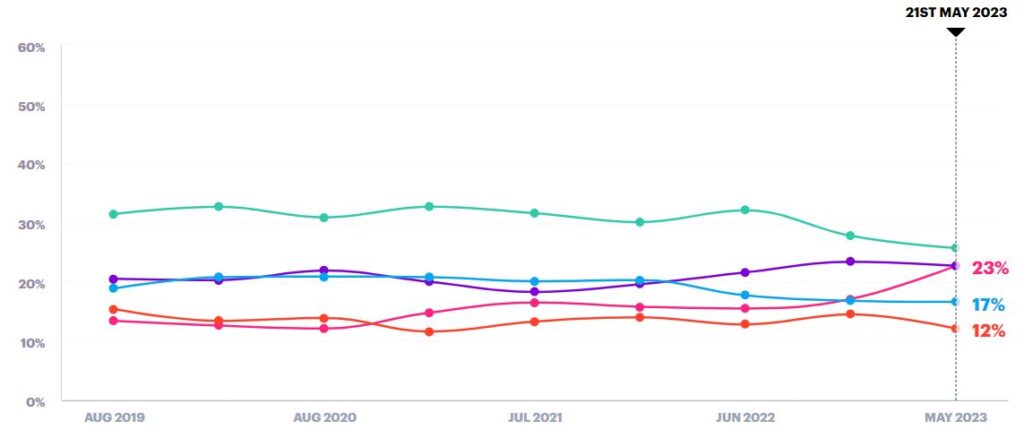

When YouGov asked for a breakdown of which workers should be able to strike, all groups of workers who’ve taken strike action over the last year were supported by 50% or more in May 2023, including doctors, nurses, rail and Tube workers, teachers, civil servants and air traffic controllers. In each of these groups of workers more people thought they should be allowed to take strike action than those who thought they should not be allowed. The only group of workers where more thought they should not be allowed to take strike action were police officers, however even here those who support police being allowed to strike has increased this past year from 38% to 44%. The charts below, from YouGov, tracks the opinions of all adults. For further details visit the YouGov site here.

When asked if trade unions face too many restrictions, public opinion has marginally more shifted towards the government’s view than the union as to whether it is too hard or too easy for the unions to take strike action, meaning slightly more have believed the government than the trade union side in the media battle of words on this issue. The chart below, from YouGov, tracks the opinions of all adults. For further details visit the YouGov site.

Whether the Labour Party – the party set up by the trade union movement – should align more closely with the trade unions. Analysis of the results point us in the same direction (see here: What relationship should Labour have with the Trade Unions?) And whilst it’s true that the highest percentage was ‘don’t know’. From those who did answer, those who think there should be a closer relationship has gone up starkly from 16% in June 2022 to 23% in May 2023 and those who think the link should be more distant or broken have gone down significantly losing 5 points and 4 points respectively in the same time period. The chart below, from YouGov, tracks the opinions of all adults. For further details visit the YouGov site.

The case is made by the government that trade unions are anachronistic and out of touch, however the public think differently. When asked Do Trade Unions reflect ordinary working people in Britain today? support for trade unions has gone up marginally in a year. Considering this has been a year of a huge upswell in strike action that has undoubtedly affected British people in the pocket, their travel and their healthcare, this is no small trend. And those saying they don’t think trade unions reflect working people has dipped since the strikes got going. The chart below, from YouGov, tracks the opinions of all adults. For further details visit the YouGov site.

The world economy as a whole is suffering a period of significant economic slowdown and surging prices. The effects of these trends are uneven. In general workers and the poor in the richest countries are getting poorer as real incomes fall. In many countries of the Global South the situation is much worse, with outright misery commonplace along with the growth in hunger.

The causes of the crisis have generally been obscured. A number of spurious explanations have been put forward as to the cause of the crisis; the war in Ukraine, ‘bottlenecks’, wage inflation, even bad weather.

The true cause of the crisis was the synchronised economic stimulation policies of the G7 countries, both monetary and fiscal policy, without any corresponding increase in Investment. Equally, as the G7 countries have largely been unwilling to unwind or reverse these policies the crisis has persisted for far longer than many had hoped or forecast. Inflation has generally remained persistently higher than forecast, and the policy response of higher interest rates will only exacerbate the slowdown without addressing the underlying cause of inflation.

Unless that policy mix in the G7 changes, prices will continue to rise at a destructive rate even as inflation slows and the world economy will remain sluggish or stagnant. Yet there is no sign of current policy being reversed.

Instead, there is a general trend, which began in the US to add protectionism to the toxic mix. This was marked by the introduction of the US’s ironically named ‘Inflation Reduction Act’, which is thoroughly protectionist. Other G7 countries and the EU as a whole are responding in kind. This is a recipe for deepening economic crisis, not alleviating it.

Exploding Myths

The myths about the causes of the crisis are now so well-established in both economic debate and popular discussion that it is necessary first to debunk them. Fortunately, this is a relatively easy task, by reference to the facts.

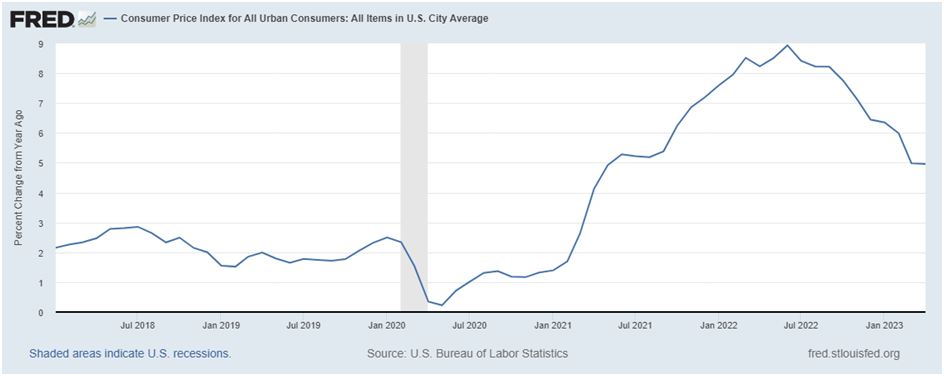

Chart 1. below shows the year-on-year growth rate of consumer prices (CPI) in the US economy. US CPI growth hit a low of 0.2% in May 2020 as the economy had slowed sharply following the failed attempts in curbing the Covid virus and lockdown. But once lockdown was ended and (as we shall see) economy policy changed, then US prices started to rise rapidly. By February 2022 CPI had reached 8%, and eventually peaked a few months later at 8.9%.

Chart 1. US Consumer Price Inflation (percentage change, year-on-year)

February 2022 is an important date in the mythology of the current crisis, because it was at the end of this month that Russian forces moved into Ukraine and began this phase of the military conflict. The logical problem with ascribing the surge in prices to the war, as most Western commentators have done over a prolonged period, is that the inflation wave began almost two years earlier, in May 2020 as the Chart shows.

In addition, the bulk of the rise of in prices took place before the war, from 0.2% to 8%. Finally, inflation has actually been subsiding for most of duration of the war, from June 2022 until now.

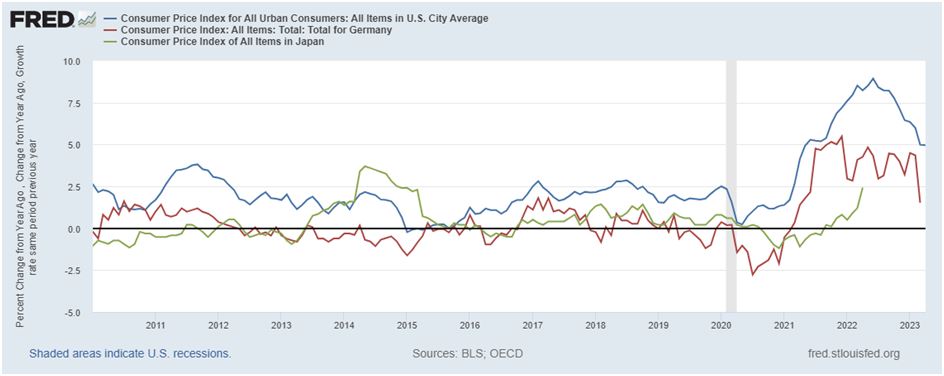

A similar pattern is identifiable in the other advanced industrialised economies, with some national variation, as shown in Chart 2 below. The rise in inflation was not caused by the war. So the claims by President Biden and other who have called it, ‘Putin’s gas price rise’, are simply to deflect responsibility.

At most, some prices of some important commodities received an initial push higher because of the war, but that effect has long subsided.

Chart 2. US Consumer Price Inflation (percentage change, year-on-year)

The rise in inflation was not caused by the war

Another of the widespread false explanations offered is that there was a sharp rise in ‘bottlenecks’ that occurred during the lockdowns in the G7 countries and elsewhere. All manner of supply disruptions did take place during the lockdowns. But it is possible to discount genuine factors such as the difficulty of shipping finished goods, for example. An unwanted build-up of unsold finished goods would have the effect of lowering prices, as producers discounted prices to shift goods.

Conversely, if producers cannot easily access either basic commodities or intermediate goods (goods which require further manufacture before they become a finished good), then they will tend to bid up prices and so add to inflationary pressures.

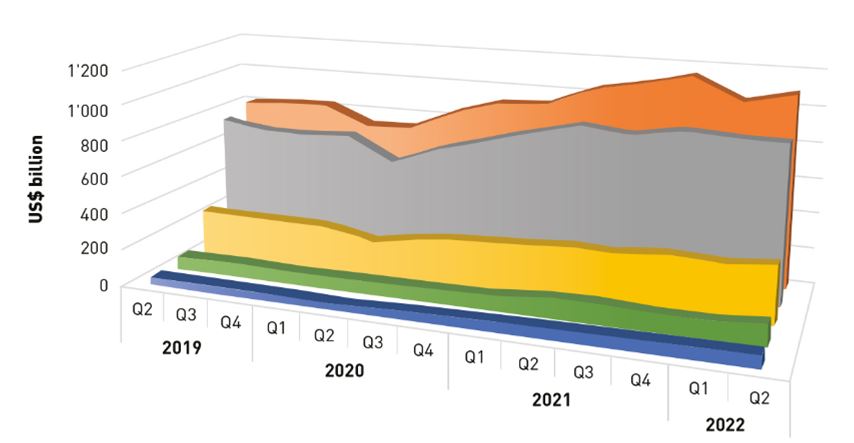

Yet, according to data from the World Trade Organisation (WTO) the shortage of these inputs was both shallow and short-lived. Production bottlenecks did not cause the rise in global prices, as shown in the WTO chart reproduced below.

Chart 3. World Exports of Commodities and Intermediate Goods, quarterly, US$ trillions

Source: WTO

The remaining explanations advanced include the weather and wage inflation. It seems inevitable that climate change will cause large-scale and severe economic disruption. But the climate crisis is a continuous process and there are no specific weather patterns which would have caused such a sharp, global rise in prices. This is especially true as the major commodities initially leading prices higher were oil and gas. Climate change cannot explain the slow decline in inflation which is under way.

In contrast, there has been the rise in widespread labour shortages reported in many countries, and a genuine labour component of what can be described as ‘bottlenecks’. However, in the G7 countries which have led prices higher, there is no evidence of an effect on prices, particularly the price of labour.

Instead, what has taken effect is a large downward pressure on real wages in many of the G7 countries. This is inexplicable to those who argue that wages are set by the laws of ‘supply and demand’. If that were true shortages of labour would lead to higher wages. In reality, wages are set through the all-round struggle between classes. The policy pursued by the G7 governments is to lower real wages.

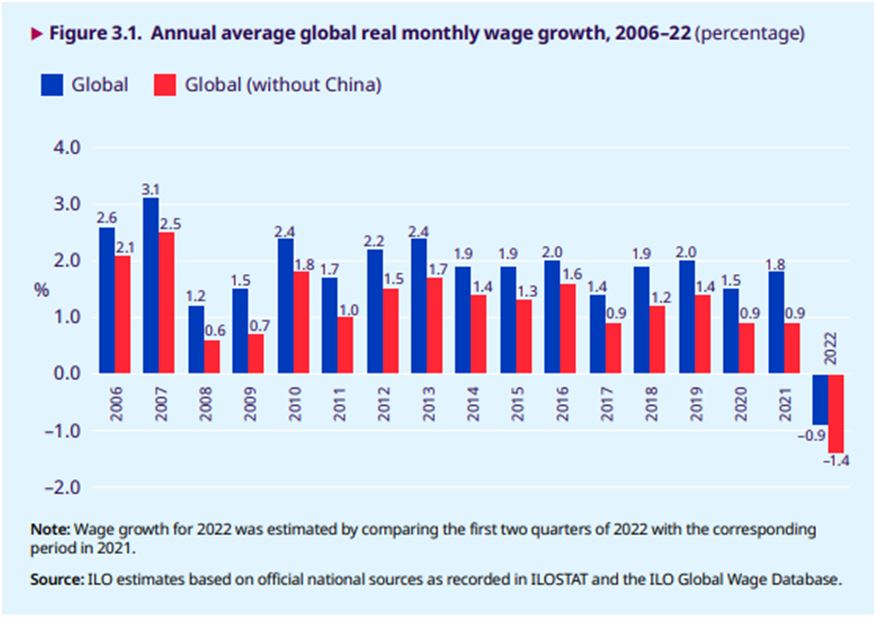

Chart 4. below is reproduced from the International Labour Organisation (ILO) Global Wage Report 2022-23.

It shows the medium-term growth in real wages globally. 2022 was unprecedented in falling global real wages. This did not occur even in the Global Financial Crisis of 2007-08. (Note too that global real wage growth in real terms is on average 0.6% lower when China is excluded. So much for the idea that China’s high levels of Investment are detrimental to popular prosperity).

Chart 4. Global Wage Report 2022-23 (ILO)

G7 policy caused this crisis

This factor is crucial in understanding the dynamic of the current crisis. Through the mechanism of inflation, in which real wages and other fixed incomes are lowered while profits are allowed to rise sharply, there is a sharp redistribution of incomes from workers and the poor towards big business and the rich.

The subsequent policy of raising interest rates by the central banks is billed as curbing an inflation that was created by official policy. But the further effect of those interest rate rises is to transfer incomes and wealth from small businesses, mortgage-holders and consumers to banks, big businesses and the owners of capital.

Naturally, G7 governments themselves are reluctant to accept the blame for the crisis. This leads to the string of explanations that have been offered that do not at all correspond to the facts.

However, in some of the more secluded areas of public debate where policy is discussed by those who advise policy makers in the leading economies and away from mass access, the veil has occasionally been lifted to reveal the true picture.

Below are small extracts from two research papers, which speak for themselves:

“Our findings suggest that fiscal stimulus boosted the consumption of goods without any noticeable impact on production, increasing excess demand pressures in good markets. As a result, fiscal support contributed to price tensions. Indeed, focusing on inflation through February 2022 which does not capture many disruptions associated with the war in Ukraine, we show that countries with large fiscal stimulus, or with high exposure to foreign stimulus through international trade, experienced stronger inflation outbursts.” –

“To mitigate the health and economic fallout from the COVID-19 pandemic, governments worldwide engaged in massive fiscal support programs. We show that generous fiscal support is associated with an increase in the demand for consumption goods during the pandemic, but industrial production did not adjust quickly enough to meet the sharp increase in demand. This imbalance between supply and demand across countries contributed to high inflation. Our findings suggest a sizable role for fiscal policy in affecting price stability, above and beyond what a monetary authority can do.” –

Here the central bank economists and analysts could not be clearer: It was the role of G7 governments in stimulating the economy without any corresponding increase in production which caused inflation. Or, it can be put in another, starker way. The policy in the G7 was to stimulate Consumption, not Investment and the result was inflation.

However, it has been left to one of the world’s most senior central bankers to admit the role of the central banks’ monetary policy, not just government fiscal policy, in causing inflation:

“….monetary and fiscal policy stimulus deployed during the pandemic gave inflation an even larger, and certainly more enduring, unexpected push. As a reminder, policy interest rates were lowered to zero, and often below. Central bank balance sheets ballooned. Fiscal stimulus since the start of the pandemic has exceeded 10% of GDP in many advanced economies – a push previously seen only in wartime.” –

Monetary and fiscal policy as anchors of trust and stability, speech by Agustín Carstens, General Manager, Bank for International Settlements, at Columbia University, New York, 17 April 2023.

In fact, it has for some time been shown that it was G7 policy, both excessive government Consumption and monetary stimulus without Investment, which was the real cause of the crisis. Under the self-explanatory title, Global economic destabilisation was made in the US not in Ukraine, John Ross demonstrated that it was the reckless monetary and fiscal policies of the US which was the main cause of the crisis.

To this we can now add the following subsidiary but important points:

This completely reckless policy was shared across the G7 in varying degrees

All other explanations for the crisis have been shown to be false

That the crisis was caused by G7 policy is now admitted, discreetly, by the central bankers themselves.

What next?

The G7 central bankers have decided to attempt to curb inflation by increasing borrowing costs rather than reining in excessive monetary stimulus or publicly suggesting that governments do the same with fiscal stimulus (which has overwhelmingly gone to big business). Never once have they suggested addressing the ‘demand-supply’ imbalances they have identified by increasing supply, that is, by significantly increasing Investment.

In the process of pushing interest rates higher, it is widely understood that interest rates charged to borrowers have risen far greater than the savings rates. The result is a huge increase in the profit margins of the banks. Just as with the profiteering of energy firms and both food producers and retailers who have taken advantage of the initial price surge by fattening profit margins, G7 governments could step in and impose price controls and windfall taxes, nationalising those who will not comply. But they have chosen not to.

This itself reveals that the current crisis is an all-round class offensive, which in a period of economic stagnation blatantly enriches further big business and the rich at the expense of impoverishing workers and the poor.

As noted earlier, this same offensive now includes increasing protectionism. Biden explicitly sold the Inflation-Reduction Act as a measure to protect household incomes and American jobs. It will do precisely the opposite.

Trump’s earlier protectionism raised prices and did nothing to protect jobs. As tariffs are paid either by importing businesses or consumers, domestic prices rise. At the same time, jobs tend to be exported to lower-tariff markets. Trump boasted that his protectionism would push GDP growth to 4% or above. In reality, average annual growth in his presidency was under 2.3% and continued the long downtrend in US growth rates.

This was predictable and predicted. That type of protectionism (of existing industries) has never worked, and the last time it became universal policy in the industrialised countries in the 1930s it led directly to slump followed by world war.

Bidenomics embraces Trump’s protectionism on a larger scale. European and British leaders pretend to welcome the measures while pleading for special treatment and exemptions. The upshot of this protectionism will be slower growth, fewer good jobs and higher prices than there would have been otherwise.

Global South debt

Yet, despite this level of economic difficulties, it is many countries in the Global South which will bear the brunt of the G7-induced crisis. In its recently released Global Economic Prospects the World Bank suggests that the economic growth of the Global South excluding China will fall from 4.1% in 2022 to 2.9% in 2023. The expectation is that the number of countries experiencing debt distress (and rising risk of default) will rise from the present number of 14.

The World Bank is clear that rising interest rates in the US are the cause of the nascent Global South debt crisis, even titling one chapter, ‘Financial spillovers of rising US interest rates’. This is a valid assessment of the process, reflecting the fact that the overwhelming bulk of Global South international borrowing is denominated in US Dollars.

When US domestic interest rates rise, Global South borrowers are obliged to increase the premium they must pay over US debt. But this comes at a time when, as previously noted, growth is also slowing markedly. This economic slowdown also tends to depress US Dollar-denominated export earnings in the Global South economies. This in turn reduces their capacity to meet interest payments on existing debt or renew existing borrowing.

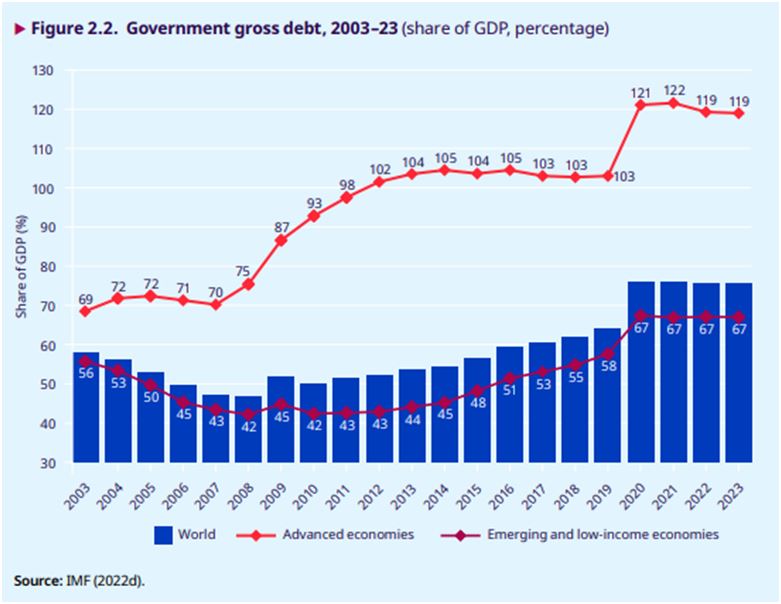

It is not the case that in general the Global South economies are relatively highly indebted. Taken in aggregate public debt in the Global South has been relatively stable and much lower as a proportion of GDP than in the advanced industrialised countries. This disparity is shown in Chart 5 below.

Chart 5. Public debt as a proportion of GDP in the advanced industrialised countries and in the Global South

Source: ILO

Naturally, there are specific instances of much higher public debt of some countries in both regions. But it cannot be said that it is generally high Global South indebtedness which is the cause of the debt crisis. It is the combination of factors of dependence on the slowing G7 economies, the impact of higher US interest rates and above all the existing levels of very high interest rates on public debt, whose gap over US domestic interest rates tends to rise even as US rates are rising.

In short, the crisis is caused by US dominance of global financial markets and the impact that has on the borrowing costs of the Global South. This aspect of the crisis is still developing and may have much further to run, depending on the trajectory of US domestic interest rates.

We are all going to pay the price for the failed economic ideology and reckless policies of the G7 governments and central bankers. But some will pay more heavily than others.

The chief economist for the Bank of England has let the cat out of the bag. Huw Pill (estimated salary £190,000) has told us that we should all accept we are poorer and stop trying to fight for wages that at least match inflation.

This is the official policy, from the government and the central bank — workers and the poor should pay the price for getting the economy out of its crisis. This is their strategy.

In Pill’s words, “What we’re facing now is that reluctance to accept that, yes, we’re all worse off and we all have to take our share; to try and pass that cost onto one of our compatriots and saying: ‘We’ll be all right, but they will have to take our share too’.”

But this is completely misleading, as shown by his additional remarks: “Someone needs to accept that they’re worse off and stop trying to maintain their real spending power by bidding up prices, whether through higher wages or passing energy costs on to customers etc.”

This is the notion that inflation is somehow comparable to a natural disaster, like an earthquake or tsunami, and that we are all equally affected. This is nonsense and he knows it.

Recent data from the Office for National Statistics (ONS) demonstrate that this is self-serving rubbish. Over the 12 months to March this year, electricity prices rose 67 per cent and gas prices more than doubled, rising a whopping 129 per cent. At the same time, average earnings growth was just under 6 per cent for all workers.

The suggestion that in some way we are all equally affected by surging inflation is false. Workers’ pay in both the private and public sectors is falling in real terms; failing to match the rate of inflation.

But the incomes of energy firms and their executives and shareholders are growing at a hugely faster rate than the rate of inflation, where the CPI currently stands at 10 per cent. Their real earnings are soaring, as are profits.

All of this has nothing to do with underlying energy prices on global markets or the Ukraine war. Both gas and oil prices are now significantly below where they were when the war began in February 2022. Energy companies are not “passing on energy costs,” which are falling; they are profiteering, pure and simple.

The same applies in many other sectors, such as banking, food, and even rent, which of course have nothing to do with the war.

Even mainstream economists now point out that the Bank of England is covering up its own role in the global inflationary surge. At the end of the pandemic-related lockdown in the spring of 2020, the governments and central banks of the G7 economies embarked on a co-ordinated effort to stimulate their economies by ramping up government consumption and by increasing the supply of money (sometimes called printing money).

This effort was not at all secretive; there were numerous press releases, reports and publications announcing and analysing it. It was led by the US, where the central bank the US Federal Reserve created money at a rate never before seen in history.

At the same time, the federal government was spending on consumption at the fastest-ever rate in US peacetime. It was done in two rounds, one from the Trump and the other from the Biden administration.

Much of this was in the form of direct support to businesses, which was always their priority during the pandemic. Rishi Sunak’s disastrous “eat out to help out” scheme was in this vein; research by De Montfort University suggests it was responsible for a spike in deaths.

In the US, one clear indication of the failings of this policy came in the housing sector. As part of an enormous $1.9 trillion Covid relief package, Biden sent $30 billion in cheques directly to households to help pay the rent.

On the face of it, this seems like a good policy. But the result was that landlords simply put up the rents and evictions actually rose.

This is because the policy of hugely boosting demand by spending government money and increasing the money supply is bound to backfire unless investment is also increased. To lower rents, investment in new housing is required. Without that, more money going into housing just leads to higher property prices or rents. And without regulation, evictions rise.

This enormous error sparked the global inflationary wave. It is being used to drive down the real incomes of workers and the poor in the G7 and beyond. It has also proved to be disastrous in the global South, leading to even greater economic difficulties and even widespread hunger as the price of necessities has soared.

This is even admitted by the central bankers themselves, although, for obvious reasons, their research findings have not been given a wide airing.

One branch of the US central bank wrote: “By stimulating demand without boosting supply, our results suggest that fiscal support contributed to increased excess demand pressures in goods markets.”

In plainer language, boosting demand without investment in the means of production caused inflation. Notably, the central bank researchers are only criticising government spending policy. There is no self-criticism about the role of monetary policy, but the same logic should apply.

There is one final and important fallacy in official thinking that is vital for the labour movement to grasp, and to understand its own power. Workers and the poor are under a ferocious attack. Banks, energy, food and other companies as well as landlords are laughing all the way to the bank. Arguments for wage restraint are blatantly biased by class interest.

Facts speak otherwise. The wide gap between public and private sector wage growth has narrowed considerably. This is largely due to the fightback by hundreds of thousands of public-sector workers.

In March and April last year, the gap between the annual growth in public and private-sector wages was an enormous 6.4 per cent. That pay growth gap has now narrowed to just 0.8 per cent, driven mainly by better pay settlements in the public sector.

The government has attempted to use its position as by far the largest employer in the country to set a going rate below inflation across the board. The fightback by workers, mainly in the public sector (or overseen by ministers, like rail and the Royal Mail), has resisted those efforts.

Strikes work, despite what central bank economists might say. The more determined that workers have been, the less they have been made to pay for the crisis. But they are still burdened by falling living standards. Only an even greater determination can push the burden back where it belongs, on huge multinationals and banks —and the politicians who represent them.

The above article was initially published here by the Morning Star.

Webinar: The new cold war is making us poorer 7pm Wednesday 19 April

Speakers: Kate Hudson, General Secretary CND Roger McKenzie, Morning Star International Editor Bob Oram, No Cold War Britain Micaela Tracey-Ramos, UNISON activist Michael Burke, Socialist Economic Bulletin

Co-chairs: Fiona Edwards and Sequoyah De Souza (No Cold War Britain)

Socialist Economic Bulletin has previously published material on Britain’s outsized military spending, for example recently here. This webinar is an important opportunity to further discuss these issues.

Information about the meeting from No Cold War Britain

This webinar will explore the many ways in which the new cold war against China and Russia is making us poorer.

The British government’s obedience to the foreign policy agenda of the United States is leading Britain to pursue an increasingly aggressive cold war policy that is totally against the interests of the British people. Britain’s hostility towards Russia and China, two nuclear armed states, is not only directly contributing to the huge cost of living crisis engulfing the country but is also destabilising the global situation at the expense of peace and prosperity worldwide.

Britain helped scupper the peace negotiations between Russia and Ukraine in April 2022 – negotiations in which an interim settlement seemed possible.

Britain’s excessive military budget is the fourth largest in the entire world and was higher than Germany, Belgium, Denmark and the Czech Republic combined in 2021.

Britain’s military budget stands at £48 billion – this is draining vital resources away from public services. The billions of pounds that Britain has spent in the past year sending weapons to prolong NATO’s proxy war against Russia in Ukraine could be financing fair pay rises to settle the many pay disputes in the public sector or creating new green jobs to tackle the climate crisis.

Britain’s opposition to peace negotiations and its support for the economic war on Russia are acts of self-harm. The sanctions on Russia have hit living standards in Britain as cheaper Russian energy is being replaced by more expensive US liquefied gas.

The cold war agenda is leading Britain to have poorer relations with China, the world’s most dynamic and fastest growing major economy, which inevitably damages the opportunities for win-win cooperation and comes at the expense of jobs, trade, investment and access to the best and cheapest technology.

This No Cold War Britain webinar will explore the many ways in which the new cold war is making us poorer and why a new path towards global cooperation not confrontation is desperately needed to achieve both peace and prosperity in Britain and across the world.

With inflation rising unexpectedly in February (and at one of the fastest monthly rates since the beginning of the crisis) the question being increasingly asked is: are profits driving inflation? And the evidence increasingly suggests yes.

It’s certainly not wages. The IMF’s historical study of the relationship between wages and prices (79 periods of rising inflation, including Ireland’s experience in the 1970s) found almost no evidence of a wage-price spiral – an alleged phenomenon used to justify rising interest rates and wage ‘moderation’ (i.e. real wage cuts).

‘Wage-price spirals, at least defined as a sustained acceleration of prices and wages, are hard to find in the recent historical record . . .’

This is confirmed by Ireland’s recent experience. In 2022, inflation rose by 7.8 percent. Wages rose by 3.4 percent. No wage price spiral there. If anything, wages have had a disinflationary effect. But what about profits?

In the US, the Economic Policy Institute found that in the 18-month period between mid-2020 and the end of 2021, profits made up 54 percent of the increase in prices; wages made up only 8 percent.

In the UK, Unite the Union reported similar findings in the six-month period between October 2021 and March 2022: 59 percent of price rises due to increased profits; 8 percent for wages. The further found companies with increasing profits well above pre-covid levels.

The Australia Institute argued that the economy was experiencing a ‘price-profit spiral’ with wages contributing only 15 percent to higher prices.

The Financial Times recently looked at this phenomenon in an article headlined, ‘Unchecked corporate pricing power is a factor in US inflation,’ (behind a paywall). They published this graph on the front page. It shows after-tax profit margins in the US rising higher than at any time since 1945.

The ECB has acknowledged this phenomenon. Isabelle Schnabel, a member of the Executive Board of the European Central Bank, stated:

‘. . . on average, profits have recently been a key contributor to total domestic inflation, above their historical contribution . . . To put it more provocatively, many euro area firms, though by no means all, have gained from the recent surge in inflation . . . Poorer households are often hit particularly hard – not only do they suffer from historically high inflation reducing their real incomes, they also do not benefit from higher profits through stock holdings or other types of participation.’

And staying with the ECB, Reuters reported that at a recent retreat in Finland for the ECB’s Governing Board:

‘Data articulated in more than two dozen slides presented to the 26 policymakers showed that company profit margins have been increasing rather than shrinking, as might be expected when input costs rise so sharply . . . An ECB spokesperson declined to comment for this story.’

‘Some of the surprise stickiness in inflation was coming from goods inflation. This should have come down with the reopening of supply chains but has remained stubbornly elevated, a trend he (Philip Lane, ECB chief economist) associated with increased corporate profits. Yesterday his boss Christine Lagarde also raised the notion of companies profiteering on the back of inflation . . . ‘

Eurostat’s quarterly sector accounts gives us an aerial view of profits and wages in the non-financial sector. Focusing on our EU peer-group (other high-income countries) over the last two years up to the 3rd quarter in 2022 we find that:

Profits increased by 25.9 percent

Employee Compensation increased by 12.8 percent

Profits over this period increased at twice the pace as wages. We find a similar pattern if we go back over three years – starting in the pre-covid period of 2019.

What about Ireland? Irish profits data can be as unreliable as Irish GDP. It incorporates income that is produced in other jurisdictions but booked here to take advantage of our low tax.

These measure year-on-year averages. On average, profit margins made up over 60 percent of prices. It should be emphasised that this data relates to the domestically-owned sector – it doesn’t factor in multi-national profits.

However, it is certainly the case that the multi-national sector is more profitable than our domestic sector. And if we use corporate tax revenue as a proxy, we find that it has more than doubled between 2019 and 2022, implying that multi-national profits have more than doubled.

* * *

This price-profit spiral raises a number of questions for policy. If prices are not being driven by wage-fuelled demand, what is the point of ECB’s interest rate increases? The Reuters report went on to quote Paul Donovan, chief economist at UBS Global Wealth Management:

’It’s clear that profit expansion has played a larger role in the European inflation story in the last six months or so. The ECB has failed to justify what it’s doing [increasing interest rates] in the context of a more profit-focused inflation story.’

It is important to note that rising profits are not uniform across the board. We have less insight into the sectoral breakdown of profits than we have wages. The ECB’s Schnabel noted that it is larger, export-oriented firms that are benefitting the most with many smaller firm – in particular, in contact-intensive services (retail. Hospitality, transport, entertainment, etc.) – still struggling.

But there’s a more fundamental question: what is the point of profits? If profits are being direct into increasing dividends and senior executive pay, rather than its social utility (investment), then economies are suffering from a double whammy: profit-fuelled price increases and ECB interest rate increases.

Answering that question, however, calls for a far more radical review of how we run our economies. But the quicker we start that review, the quicker we can begin addressing a myriad of problems, including profit-fuelled inflation.

The above article was originally published here on Notes On The Front. Michael Taft is a researcher for SIPTU (Services, Industrial, Professional and Technical Union) in Ireland.

Hard up? Who is to blame? The economic consequences of the anti-union laws Online meeting 7pm Monday 27 March

Speakers: ● John Hendy KC, Campaign for Trade Union Freedom ● Diane Abbott MP ● Michael Burke, Socialist Economic Bulletin ● Alex Gordon, President of RMT Union

Chair: Sarah Woolley, General Secretary, Bakers’ Food & Allied Workers’ Union and Co-chair, Campaign for Trade Union Freedom

A joint event by the Campaign for Trade Union Freedom and Socialist Economic Bulletin. Details of this online event can be found on Eventbrite here.

About the Campaign for Trade Union Freedom The Campaign For Trade Union Freedom was established in 2013 following a merger of the Liaison Committee For The Defence Of Trade Unions and the United Campaign To Repeal The Anti Trade Union Laws. The CTUF is a campaigning organisation fighting to defend and enhance trade unionism, oppose all anti-union laws as well as promoting and defending collective bargaining across UK, Europe and the World.

Almost the only merit of the first Budget from Jeremy Hunt is the fact that it clarifies how austerity works. This austerity Budget, like all its predecessors, is not simply cuts, although these are numerous and deep. It is the transfer of incomes from poor to rich and from workers to business shareholders and executives. It is a conscious government policy; a class offensive.

So, a key reason why there was any money in the Budget is because of the renewed austerity offensive combined with very high inflation. Where Cameron and Osborne (and later May and Johnson) tried to force big cuts in spending, a combination of popular resistance and their own political weakness limited the effects to a degree. But the current inflationary wave magnifies the effects of austerity policies by cutting pubic spending in real terms.

Restraining public spending, including pay, while inflation is high puts a huge burden on both public services and public sector workers struggling with real pay cuts. But at the same time inflation raises government revenues such as income tax, self-assessment payments and VAT. It is that discrepancy -paid for by workers and all those who rely on public services, which allowed Hunt’s giveaways.

These giveaways amounted to £88.8 billion over the next 5 years, which is sizeable amount, about 0.75% of GDP each year. However, almost none of this will benefit ordinary households.

The big winners are companies. £29 billion is used in a revival of the failed idea that tax breaks will incentivise private sector investment. Polluters will also benefit through the fuel duty levy freeze (£15.1 bn), and the MoD will have an extra £11 bn to part-fund its adherence to US war policy against Russia and now China.

The sole vaguely progressive measure in the Budget is £18.1 billion to help with childcare costs. But this is over a 5-year period, which amounts to a cut-price, piecemeal and private sector set of measures that are much less effective than Sure Start, which the Tories have effectively abolished.

The aim is a purely political one, as the Tories are 33 points behind Labour among women (compared to 13 points among men). But even this has been botched for purely ideological reasons. Without new state provision and relying on private childminders means prices will be pushed higher as demand outstrips supply. Nurseries are actually forecast to close as a result.

The claim that consultants are leaving the NHS because they cannot top up their pensions is a blatant lie. It is a general benefit to the highest tax payers, so that they can shield their pay from income taxes. Pensions are also generally exempt from Inheritance Tax too. The class war aspects of this Budget are rather stark.

The Treasury documents show that the Tories will continue to squeeze public sector spending across the board – excluding Defence – and total public spending is projected to consistently fall as a percentage of GDP over each of the next 5 years.

Notably, they also intend further cuts in real pay in the public sector. There is a somewhat optimistic forecast of an average of 4.1% CPI inflation over the next year, especially as the starting-point could be close to the current 10%. But they have budgeted for just 3.5% for public sector workers’ pay in departmental spending, meaning another year of real pay cuts, bigger ones if inflation remains higher than forecast for longer.

They also specify that matching their forecast for inflation with pay rises would cost an extra measly £2bn (when they have just given away £88bn), but they refuse to do it. This indicates that they are aim for a permanent reduction in real terms pay, and are quite content to see further industrial disputes which they will make a key part of the next general election campaign.

The Tories have drawn a lesson from Cameron and Osborne years. It is not to give up on the policy of driving down the living standards of workers and the poor in the hope of boosting profits. Instead, it is to use inflation as a weapon in that fight, creating very deep cuts in public spending, and public sector pay.

This attack is what is funding the repeat of the failed policy to boost Investment by giving companies tax breaks. The British economy has an abysmal level of Investment – the lowest in the OECD as a percentage of GDP over 20 years. But the policy of tax incentives failed under Cameron and Osborne and there is no reason to believe this time will be different. Companies aim to make the level of Investment that is profitable. That does not tend to change at all with tax breaks – they are just pocketed, as Investment is driven by anticipated profits.

The £29bn could have been used for direct Public Investment. But cutting Investment is also a key part of the austerity policy. It is the counterpart to privatisation; the State ‘getting out of the way of the private sector’ in an effort to maximise the private sector’s profits.

It is notable that the reception to this Budget is much more hostile than previous similar packages, even from liberal circles. This owes almost everything to the breadth and militancy of the current strike wave. It is almost nothing to do with the Labour front bench, which has committed solely to reversing the changes to pensions and has failed to explain that it is a benefit for the 1%, while the entirety of the £88bn giveaway could have been used for pay, progressive redistribution and Investment.

However, that strike wave has created a new situation. The mass of the population feels they will be worse off. There is too a growing awareness that this is an orchestrated attack on living standards. The strike wave itself shows that there is not only an understanding that the government is responsible for the attack, but the working class is engaged in a counter-offensive of its own.

We are currently facing the most prolonged economic crisis in recent history, the most vicious attacks by a government determined to decimate living standards and clamp down even further on trade unions, and the biggest trade union resistance to that for decades. Naturally, each of these three is related.

The government has shown itself to be both intransigent and preparing for the long haul with renewed anti-union legislation. The labour movement is responding in kind and will need to be equally resolute and strategic.

There is no accident about the timing. Tories have long cherished the idea that there should be even greater curbs on trade union activity. But now we are in the middle of a huge strike wave and a prolonged economic crisis.

The anti-union laws already in place in this country are some of the most draconian in any advanced industrialised country. Research from ITUC, the international TUC, shows that this country is among the worst offenders in Europe when it comes to violating trade union rights.

The new additional minimum service level agreements to be imposed across large parts of the public sector are intended to ratchet these up. Notably, the legislation is not designed to have any impact on current disputes. The government clearly intends future fights.

The backdrop is that the British economy is experiencing a “stagflation” crisis, the combination of a stagnating economy and surging prices. In the most recent monthly data, the economy registered zero growth from a year ago, while consumer price inflation remains painfully high at over 10 per cent.

Worse, the current economic crisis is an extension of much longer trends, with no end in sight. Inflation will probably subside to some extent at some point but prices will not fall back. At the same time, British government subsidies and handouts to firms while cutting public spending and investment in real terms are a recipe for prolonged stagnation.

In response to the crisis, the government is trying to shift the burden of it onto the shoulders of workers and the poor. It has been intransigent on pay, interfered to block negotiations, in many cases refused to talk and is clamping down on trade union rights.

It has focused on the sectors the government directly or indirectly controls. It hopes that this will set a “going rate” across the economy well below inflation, for both the private and public sectors.

With this, the government hopes to both lower real wages across the board and keep them there by limiting the effectiveness of trade unions.

While the government is seeking longer-term solutions to the economic mess, so too the labour movement and its allies should examine alternative longer-term strategies, to keep the burden where it belongs, with big corporations, banks and landlords.

To some extent, this is a repetition of history. The inspiration for the current Tory policy stretches back to Margaret Thatcher. Then, as now, there was a string of legislation curbing the rights of workers to form unions or the rights of unions to organise their members for industrial action.

Thatcherism was also a response both to an economic crisis and a wave of trade union militancy which had resisted efforts to impose “pay restraint” which were designed to lower wages in real terms (after inflation).

Thatcherite ideologues claiming success for those policies ignore two key facts. The first is that Thatcherism benefitted from an extraordinary windfall of North Sea oil revenues that amounted to approximately 15 per cent of GDP during her time in office.

Secondly, taken as a whole, the three decades of Thatcherism and its legacy produced significantly lower growth than the three decades that preceded it. In the post-World War II period before Thatcherism, the British economy’s growth rate was about 3 per cent on average. Post-Thatcher it was less than two-thirds of that and has since slipped to below 1 per cent under austerity.

Yet the government is now doubling down on a policy which has failed.

The policy amounts to transferring incomes and wealth from poor to rich and from workers to big business. But the recent experience of the British economy is that this falling labour share of national income has also been accompanied by a private-sector investment strike.

The private sector does not feel compelled to invest if it is able simply to squeeze workers harder.

This is common across the G7 economies. But Britain is the worst example. The British economy lags behind even comparable countries which themselves have experienced a declining rate of investment.

According to the Organisation for Economic Co-operation and Development (OECD) from 1997 and 2017, the proportion of GDP directed towards fixed investment in Britain was the lowest in the OECD as a whole, at 16.7 per cent of GDP. The next lowest are Italy and Greece, both at 19.6 per cent of GDP.

This is a private-sector failure to invest in the means of production. It leads directly to an inability to increase production in any significant way. This in turn has produced economic stagnation.

It would be very difficult for any government to raise living standards and improve public services in these circumstances. But austerity deepens the crisis for the mass of the population while public services are in crisis. Take-home pay and welfare benefits have both been cut in real terms.

This chronic private-sector failure has now become acute. Therefore, the state must take the lead role in reviving the economy through investment while sharing incomes more equitably through redistribution.

The state has no compulsion to distribute returns to shareholders. It can raise its own level of investment and deliver the same effects as falsely promised on behalf of the private sector.

It can also borrow for investment as the private sector does, or should.

But public investment must also be restored. It has amounted to only 1 per cent of GDP for most of the last decade, compared to up to 5 per cent of GDP in the pre-Thatcherism period of much stronger growth.

A bold public investment programme would be a truly green and just transition in energy, transport and housing, with taxes on the banks and big firms to pay for the restoration of public services, a massive increase in publicly owned housing, and renationalised public services.

A key part of the revival of public services must be inflation-plus pay rises to recruit and retain workers. This should also apply to those sectors the government effectively controls, but where the private sector rakes off subsidised profits, such as rail, post and telecommunications.

In addition, existing and planned anti-union legislation should be scrapped, to allow organised workers to bargain collectively for decent settlements.

The government should also outlaw zero-hours contracts and other casualisation measures, and offer those on the minimum wage and benefits something like the pensioners’ triple-lock.

The fight-back against the government has begun and it is determined to block it. Everyone with an interest in opposing austerity and cuts to living standards should also oppose government anti-union legislation.

The Campaign for Trade Union Freedom and Socialist Economic Bulletin have jointly organised a meeting to develop the links between the anti-austerity struggle and the fight for union rights. Join us online on Monday March 27 at 7pm to find out more.

Recent Comments