yesDon’t be fooled: Tory austerity will continueBy Matt Willgress

AT THE recent G20 summit, the new Tory Prime Minister Theresa May refused to rule out more austerity — including cuts to welfare — if the British economy suffers as we approach Brexit, and last week’s Conservative Party conference has confirmed that the new government is still tied to the failing, ideologically driven austerity agenda of the Cameron and Osborne years.

Even ex-chancellor George Osborne had announced in March that he had “no further plans to make welfare savings” before the 2020 general election.

Last month May said: “Obviously we have to look and see what happens in the economy and how the economy does start to move — if there is any further movement post the Brexit result.

“Obviously anyone will be looking very carefully at how the economic situation pans out.”

May also made it clear that there will be no end to Tory austerity, saying: “What I’m clear about is we’re going to continue as we have done in government over the last six years — ensuring that we’re a country that can live within our means.”

This followed the new Chancellor Philip Hammond saying that he may have to “reset” the government’s tax-and-spend policy if the economy starts to go downhill this autumn.

Indeed, the government has also said that the decision on whether to make such changes to tax-and-spend policy will be made in time for the Autumn Statement on November 23.

Contrary to many mainstream media reports that austerity is now over, which were repeated again throughout the Conservative Party conference, the government is not only refusing to offer any guarantees regarding further cuts, but it should also be remembered that this is despite the continuous Tory attacks and cuts since 2010, and the fact that deep further cuts are already underway or due to come.

Last week’s Tory conference further showed that the government is still tied to austerity and has no grasp of the scale of the challenge facing the British economy in terms of chronic under-investment. Take for example housing.

The Tories then announced £2 billion of public money for housing and £3bn in private-sector loans to small builders.

This would only build 33,000 houses over five years and is totally inadequate. This is in a situation where we need 200,000 new homes to be built a year just to stand still.

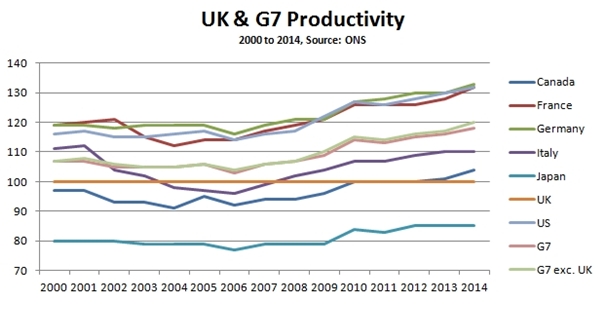

In contrast to this approach, what most serious economic analysts are agreed on is that the economic uncertainty following the EU referendum result means that the British economy needs more investment, not more cuts.

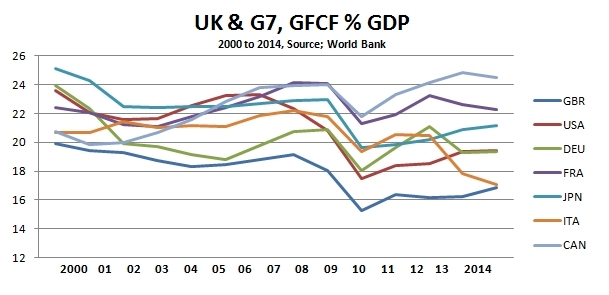

Investment has fallen in all G7 economies, but British levels of investment are 4 per cent of GDP below the average.

Just to make investment in Britain up to this level you’d need £80bn additional investment per year over a parliament. In contrast to the failed Tory approach, Jeremy Corbyn’s re-election and the policies set out at this year’s Labour conference have seen us stake out how a Labour government would deliver a £500bn public investment programme to build our infrastructure, manufacturing and new industries, moving us to a low-carbon economy, delivering good jobs and tackling the housing crisis.

This is the credible — and transformative — economic strategy that Labour needs for a general election victory and will raise living standards in Britain.

Therefore, our urgent work in both opposing the cuts nationally and in our communities, and popularising a progressive alternative to ideologically driven austerity, becomes even more vital, alongside building electoral support for Labour.

Following this summer’s leadership campaign and party conference, the Labour Assembly Against Austerity (which brings together support for the People’s Assembly Against Austerity movement within the Labour Party) will continue a series of campaign initiatives and events to bring about this change and win the argument that austerity is a political choice, not an economic necessity. Please join with us!

· The Labour Assembly Against Austerity is hosting a major national conference on Saturday October 22 entitled Winning With Jeremy — Labour’s Alternative to Tory Austerity. Initial speakers include: Jon Trickett MP, Diane Abbott MP, Richard Burgon MP, Catherine West MP, Professor Victoria Chick, Christine Shawcroft of Labour NEC, TSSA general secretary Manuel Cortes and Unite assistant general secretary Steve Turner. 10am to 5pm at Student Central, Malet St, London, WC1E 7HY. Register online at www.labourassemblyagainstausterity.org.uk or on the door (Tickets £10/7).

This article was first published by the Morning Star, where it can read here.

Recent Comments