When is an essential worker not an essential worker? According to this government and the media that supports it, when they ask for their real take home pay not to be cut. If they do, they are selfish and greedy layabouts led by Marxist extremists.

Of course, this propaganda is simply rubbish. Much more importantly it seems to have little traction with the public, where polls and vox pops tend to show strong and rising support for those taking action. This is almost unprecedented in terms of popular support. The likelihood is that this support arises because so many people are experiencing the effects of the attacks on living standards that they feel they are in the same boat.

It also does not seem to matter much that there is genuine public inconvenience -strikes are not very effective if there is not some disruption. Yet, even though the media have tried their usual campaigns against workers, unions and their leaders, the public is not buying what they are selling.

Unfortunately, current public opinion alone will not determine the outcome of strikes. And this is a government that not only seems intent on defeating the strikes, they also want a once-in-a-generation defeat of the power of organised labour altogether.

Yet the attack itself, from a viciously right-wing government also tells us something about where we stand – and the power of striking workers that worries the Tories and their supporters so much. There is an important lesson for workers, especially those operating in the public sector (like NHS workers, teachers, civil servants, firefighters, lecturers and others) or in sectors where the government is still effectively in charge of the industry and of negotiations (such as post and rail).

There is an old myth that only industrial unions have industrial power. But at the height of the pandemic we learnt something else. This is that workers in areas like health and education have become essential, even indispensable. This is because structurally the economy itself has become more complex and more interdependent, or socialised.

This is why it became obvious that teachers and NHS workers and others were essential at the height of the pandemic. If they are not working, for reasons of health, or health and safety or because they are on strike, then many others cannot work.

One and half million people use NHS services every day. There are also well over six million children aged 5 to 14 years old who are at school every day. By comparison, the undoubted power of the rail unions rests primarily on the fact that there are an average of 2.7 million train journeys per day.

As the Financial Times has recently fretted, if workers in those sectors are not at work, large parts of the rest of the economy start to shut down very rapidly.

The City, big business, and the government have all come to the conclusion that non-industrial workers really are essential. That is why they are prepared to force them into work with new legislation, even while they are not prepared to offer decent wages.

On our side, we should recognise the same truth, that huge numbers of public sector workers and others have great economic power. And we can use it for a just cause, stopping cuts to pay and conditions, against job losses, and to save public services.

This is an expanded version of a piece which first appeared here on the website of the People’s Assembly Against Austerity

This government talks about growth, as Jeremy Hunt recently did, but will only deliver further stagnation and renewed attacks on the living standards of the majority. Any plan for sustainable growth and prosperity must include a radical break from current policies. Yet there is no sign that this Labour leadership is prepared to deliver that.

The 2023 forecasts for the British economy are grim. The latest IMF forecasts have received significant attention, with ministers attempting to rubbish the Fund’s forecasting track record. It is quite true that the IMF’s forecasts are patchy at best. But it actually has an inherent bias towards the US economic model and regularly overstates US GDP growth relative to outcomes. As Britain is the nearest European follower of that US, a smaller upward bias is also evident in its British forecasts too.

The IMF forecasts that the British economy will barely grow at all in 2023 and 2024, and that its performance will be much worse even than Russia’s. Over the medium-term, out to 2027 the IMF expects average growth in the British economy to be less than 1.4% annually.

But ministers should be aware that this gloomy outlook for the British economy is shared by private sector forecasters. Goldman Sachs is one of the latest to weigh in, arguing that a contraction of 1.2% in real GDP this year will be the worst in G10 group of countries, and that it will be followed by a rebound of just 0.9% in 2024. This is only marginally better than their forecasts for Russia, which is at war and suffering under Western sanctions.

In essence, Hunt’s prescription is to try everything to spur growth except what is known to work. Boosterism, unsubstantiated claims and special pleading for business are fantasy economics and will not work. In fact, even Hunt does not seem to believe in them, arguing that he has a ‘framework for growth, not a growth plan’. He has neither.

Only Investment in the means of production allows a sustainable increase in production of goods and services. These are what are required in order to achieve any sustained rise in either growth or prosperity.

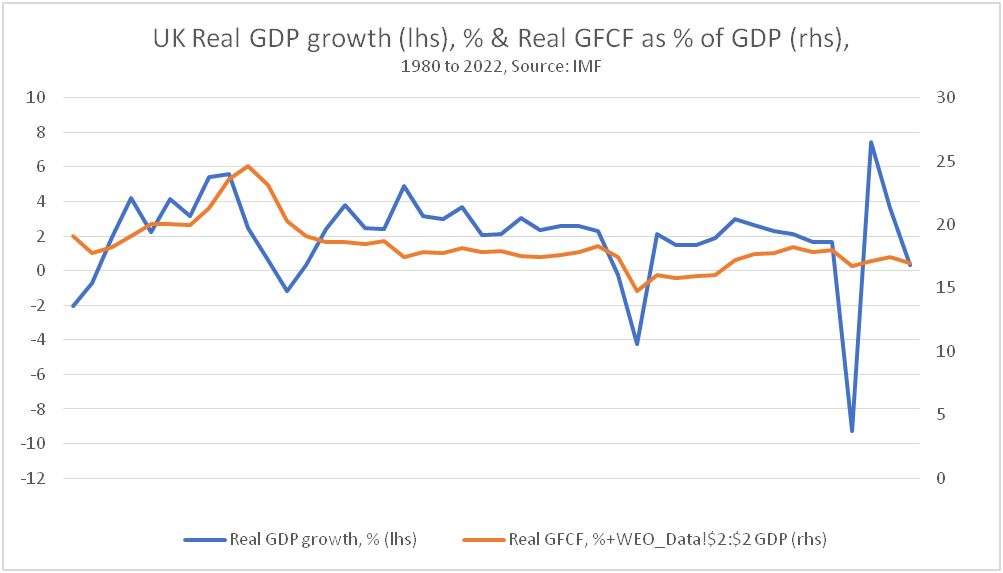

The decline in the British economy over several decades has been driven by a decline in the rate of Investment in Gross Fixed Capital Formation (GFCF). To take an obvious contrast, in the 5 years to 1990 GFCF averaged 23.4% of GDP each year and real GDP growth averaged 3.5%. The equivalent data for the latest 5 years, including IMF projections for 2023 is GFCF at 17.25% of GDP and real GDP growth of 0.75% annually.

Investment is decisive. But successive governments over decades have refused to engage in the large-scale public sector Investment that would spur growth and induce the private sector to investment at a greater rate, or a least prevent the decline in Investment that has taken place.

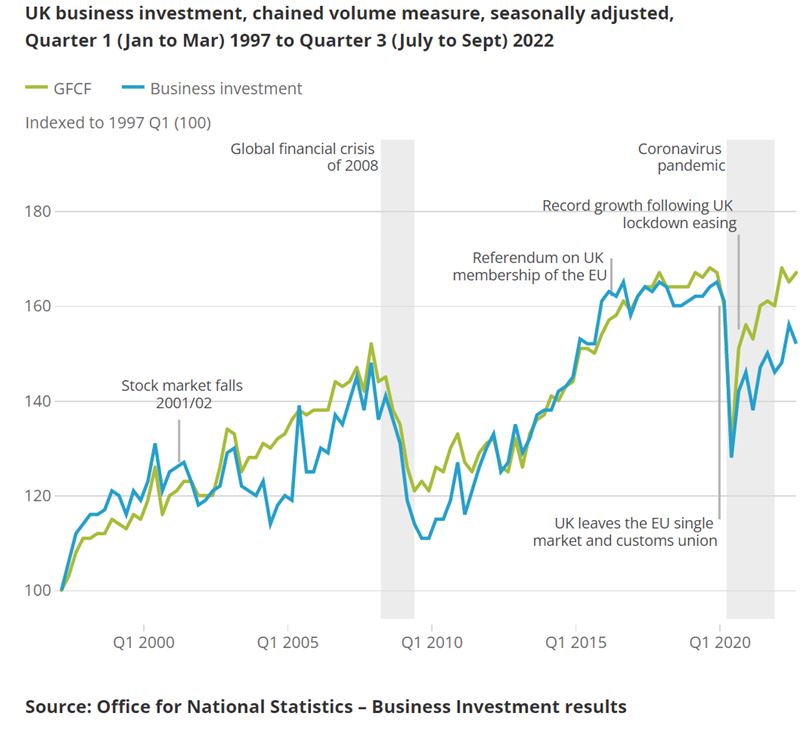

Within that total, the main factor is the weakness of business Investment, which has never properly recovered from the Global Financial Crash in 2007 and 2008. Business Investment was £52.4 billion in 3rd quarter 2022, compared to £50.9 billion in 4th quarter 2007. The economy is on course for a lost generation of Investment, because of a business investment strike by firms based in this country.

However, the absence of a Hunt growth plan (or even the correct framework) does not mean that there is no economic policy. That policy is played out daily in the street and on the news programmes. The government’s plan is drive down wages, increase the rate of exploitation and thereby hope to increase the rate of profit. This is true across the whole economy.

This begins with the mantra that they need to oppose a ‘wage-price spiral’. Nonsense that wage rises cause inflation was completely refuted by Marx 150 years ago, in Value, Price and Profit. Marx argued that there was nothing fixed about either the value of production, or wages, or the relationship between the two. In effect, the level of wages and the level of prices (or the level of real wages, which is the same thing) is set by the class struggle between two major classes and in all its forms.

The blatant hypocrisy of this campaign, which is not gaining traction in the public, is highlighted by a recent report that shareholders’ dividends are rising by 16.5% a year to £84.8bn. Of course, this is a far faster than wages which are falling in real terms. It is also a refutation that wages are driving prices higher (where you would then expect to see falling dividends). It shows the fruits of the efforts of the drive to lower real wages, increased exploitation and boosted profits.

In the drive to lower real pay the government can directly determine the rate of public sector pay. It is clearly also trying to determine the settlements in large parts of the economy which were formerly in the public sector, such as post and the railways. The aim is twofold. First is to drive down pay across the economy as a whole, using the public sector to ‘set the going rate’ for below-inflation wage settlements. Secondly, it is redirect as much of the total social product from labour to capital as possible, in effect driving down real pay and using the savings to fund cuts to corporate taxes.

To this is added draconian legislation in the right to strike, to picket, to assembly and to vote. This is an all-round offensive on the working class and its allies, to curb their economic and political power. It is a fight the government is determined to win, as the ruling class has no other plan to arrest its own decline.

Yet, just as there no crisis that cannot be resolved by loading the burden of it onto the backs of workers and the poor, so too there is no crisis of living standards for workers and the poor that cannot be alleviated (at least temporarily) by making capital pay for the crisis.

So, this is the question posed for the next government, which increasingly looks like it may be a Labour-led one. It was essentially the same question that was posed for the Corbyn-led Labour party in 2017 and 2019.

The question is not, How do we introduce socialism? Socialism requires first the seizure of state power by the working class. This is not on the agenda in Britain in any foreseeable future. Instead, the pertinent question is, What policies are required to reverse the attacks on the living standards of the majority, and to sustain that increase in prosperity?

Some combination of redistribution and Investment-led growth is required to achieve that. That must be the starting-point of any serious discussion on the left on economic policy over the next period. Otherwise the danger lies in reworking the garbage coming from Hunt and others, who have no intention of improving the living standards of the majority.

Part of the false propaganda about the cost of living crisis that we are being subjected to by the government is the line that there are “global headwinds” beyond their control that require the working class to get worse off; possibly indefinitely.

The “headwind” most often identified as causing the increase in the cost of energy is the war in Ukraine.

It is – however – never suggested that a better course for the UK government would be to seek to resolve and deescalate the war – so that people in Ukraine and Donbass can live in peace, and a mutual security arrangement made with Russia; to allow decreases in military spending on both sides which could be spent on solving the problems humanity has rather than adding to them.

This will be even more the case next Winter if there is no end to the war in the meantime, or sanctions are maintained as a form of self-harming pressure in the aftermath. The OECD projects that inflation will slowly subside through 2023 to 2024, but also notes that next Winter is likely to see a further spike in oil and gas prices if the war continues and also if China’s continuing economic growth raises demand for energy. This is very likely, and puts the OECD prediction in question.

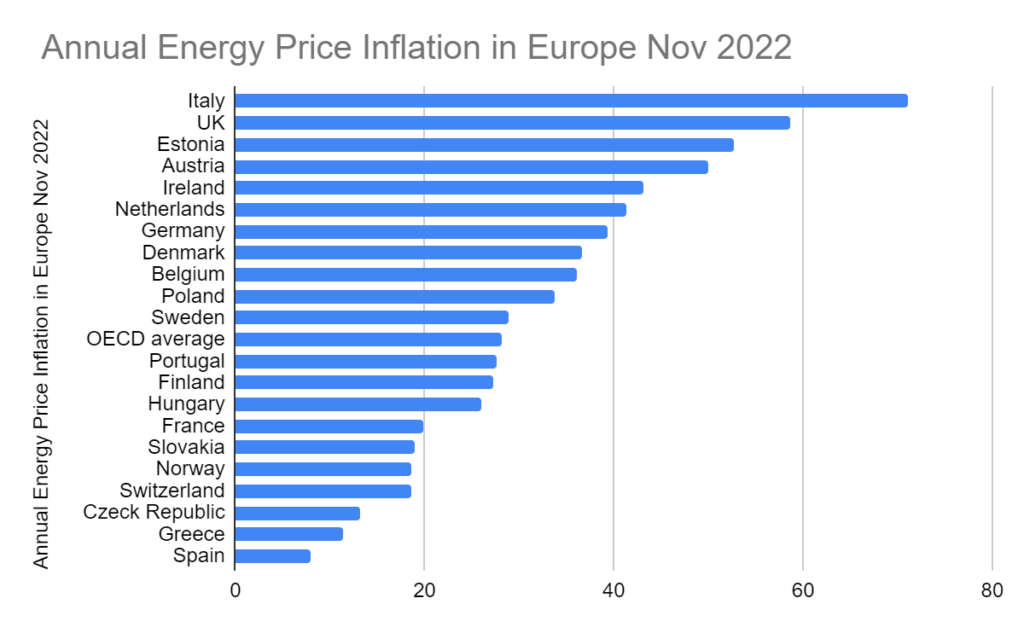

In the meantime these “global headwinds”, that the British government blames for high energy prices, seems to affect some countries far more than others, in particular the UK. As we can see from this table, there is a range of annual energy price inflation in Europe that rises from 8% for Spain to over 70% for Italy, with the UK as second worst. These figures can be further investigated and compared with other countries globally here.

See below for this in graphic terms that are easier to see at a glance. The UK energy consumer price inflation rate, in fact, is more than double the OECD average. Spain is in a particular position because it gets 90% of its gas from Algeria and is not connected up to the rest of the EU, but Germany in December 2021 got 32% of its gas from Russia compared to the UK’s 4%, so, why are prices rising so much faster here?

The UK got just 4% of its gas supply from Russia before the war, whereas Italy got 40%, which was average for the EU. At present the UK imports 50% of its gas, mostly by pipeline from Europe, but increasingly in the form of LNG, which arrives by ship from the USA, Qatar. This will increase quite quickly as North Sea production runs down; which could hit zero by 2030. It is already down to a third of what it was in 2000.

As the price of gas is set globally, regardless of where it is produced, enhanced domestic supply would have practically no impact on prices; which disposes of another myth used to try to drum up support for more North Sea gas fields or fracking. Local supply is not cheaper.

The price of gas also fixes the price of electricity, even when generated by far cheaper renewables. This is because the sources with the lowest marginal costs will be on stream all the time. This will be renewables because, once the turbines are up or the panels in place, there is no charge for the wind or sun, whereas fossil fuel plants have to pay for burning their fuel. But, although capacity is rising sharply, with six times as much as in 2010, we do not yet have enough renewable capacity to cover most of the demand most of the time. So, more expensive sources have to be brought online to fill the gaps. As the price in every half hour period is set by the marginal cost of the last generating unit to be turned off to meet demand – which is invariably a gas power plant with high marginal costs – that keeps the cost of electricity that high regardless of how it is generated. A different method of pricing to take account of the lower costs of renewables, could reduce prices and would be facilitated by public ownership of power generation.

The dizzyingly high level of energy price inflation in the UK is down to government policy choices.

As the OECD points out: “The untargeted Energy Price Guarantee announced in September 2022 by the government will increase pressure on already high inflation in the short term, requiring monetary policy to tighten more and raising debt service costs. Better targeting of measures to cushion the impact of high energy prices would lower the budgetary cost, better-preserve incentives to save energy, and reduce the pressure on demand at a time of high inflation.”

The energy price guarantee amounts to a subsidy paid to energy suppliers to avoid taxing the windfall profits of the energy producers. With these companies netting £170 billion in profits, a serious windfall tax at 100% on these, with no loopholes encouraging suicidal fossil fuel exploration, could more than meet the cost of the existing cap – £39 billion up to April 2023. If done preemptively it would cut that cost out of the inflation rate. A choice not to do this indicates that the government wants inflation to bite into the incomes of the working class as a means of levering resources up towards profits.

A better targeted measure that would meet social need and cut inflation is the TUC’s proposals for a fairer energy system which would:

Take the Big 5 energy retailers and other failing retailers into public ownership, at a similar cost (under £2.85bn) to what Government already spent on keeping failed energy supplier Bulb in business;

Task publicly-owned energy providers with offering a social tariff capped at 5% of income for low-income households;

Recognise that energy is a common good: restructure tariffs to provide all households with an initial free energy allowance, and increase the cost per unit for high-consumption households.

This would:

Protect all low-income households with fairer bills and a social tariff

Deliver lower bills and a faster climate transition through the rapid rollout of fully-funded home energy efficiency retrofits

Ensure that energy is a public good and that energy retail is both democratically accountable and transparent

The collapse of the Truss and Kwarteng economic project was one of the most swift and spectacular in modern history, which has left its mark in terms of inflation, interest rates on government debt and perhaps most of all on the private pensions sector, which was caught out by speculative investments that went badly wrong.

Given the far-reaching consequences of the failed experiment, the Truss/Kwarteng period has been strangely under-analysed. Perhaps this is because leading figures on the economic right were implicated in the debacle, such as Patrick Minford and various acolytes in the City.

But one central aspect of the policy, known by its supporters as ‘deficit-financing’ is also widely advocated on the left, and is a mainstay of ‘keyenesian’ economic thinking. In fact, it was this central part of the policy which was the immediate cause of the spectacular blow-up. As a result, it is worth examining in some detail.

The long tail of ‘deficit-financing’

‘Deficit-financing’ is actually government borrowing to fund Consumption. Almost no serious economist of any school believes there is any rational basis for concern about borrowing for Investment.

As long as the average returns on Investment exceed the average rate of interest on government debt, Investment returns will be positive and the economy will benefit. In addition, government has a very significant advantage over the private sector as a proportion of all Investment outlays will be returned in the form of taxes (income tax, National Insurance, VAT and other revenues).

In contrast, government borrowing to fund Consumption was the norm across the advanced industrialised countries in the period after World War II. This was billed as ‘demand management’, where governments believed they could manage the cyclical turns in the economy by raising/lowering their level of borrowing and so adjust the level of total Consumption in the economy. It did not prevent steady economic slowdown and occasional crises over that period.

At the beginning of the 1980s the Reagan/Thatcher offensive included efforts to cut government Consumption. Although the rhetoric against the previous consensus was severe, along with the effects on some components of government Consumption, the attempts to curb either total Government Consumption or public sector deficits met with only patchy success. On the political right, the Reagan/Thatcher ideology has remained largely dominant.

However, much of the Western political left, seeing the effects on public services or unemployment from the attempts to curb government spending, have tended to hanker after a return to the post-War consensus. The left has favoured government Consumption, or ‘deficit-financing’ as a result. Furthermore, some on the left have even tended to judge government policy favourably if the deficit is rising, and unfavourably if they are falling.

Apart from not producing prosperity, the left supporting government Consumption and rising deficits is very strange for another reason. The level of government borrowing is actually a key prop for the financial sector, a large part of whose income is interest payments on government debt. Persistent government borrowing for Consumption has allowed the finance sector to become bloated in many leading economies, not least in Britain.

Borrowing and prosperity

The increase in the productive capacity of an economy is the prerequisite for sustainable growth in prosperity. Without increasing the amount of labour in the economy, the productive capacity must be increased by Investment. Aside from labour inputs, Investment is the single main determinant of growth and prosperity.

In contrast, Consumption is not an input to growth and its growth will not cause greater prosperity. The post-World War II consensus and much of the Western left still labours under the illusion that the opposite is the case. This can be demonstrated in a real world experiment.

At almost the same time as the Reagan/Thatcher offensive in the leading Western economies there was also adopted the ‘reform and opening up’ process in China. As a result, we now have a global economic experiment lasting more than 4 decades on whether growth in prosperity is Consumption-led or Investment-led.

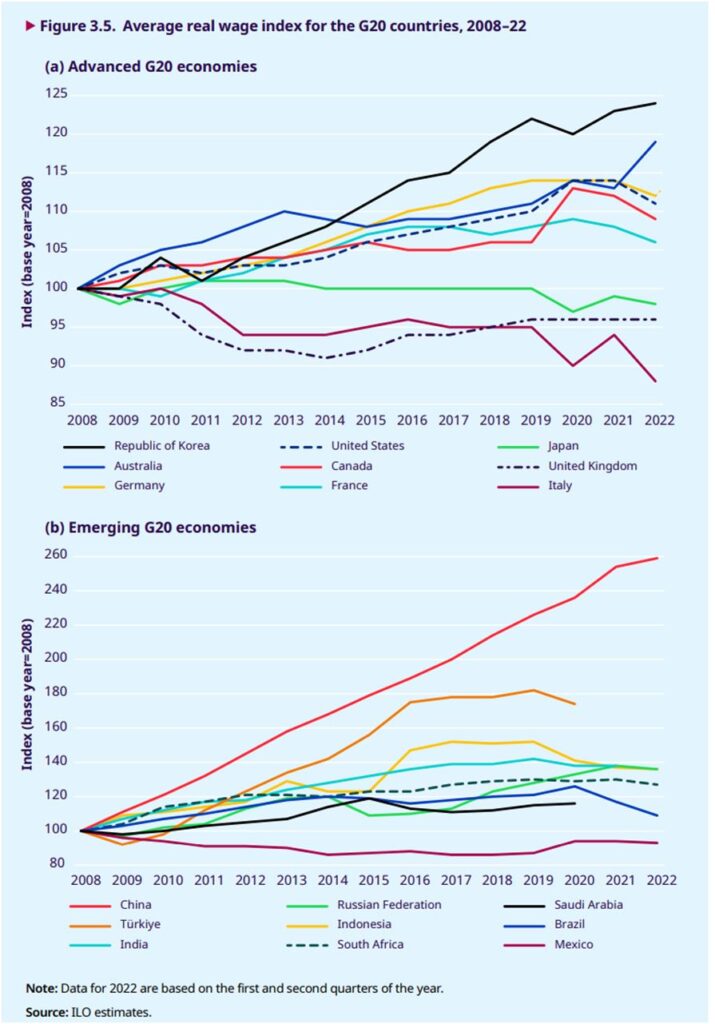

Charts 1 & 2. Average real wage index for the G20 Advanced & Emerging economies, 2008 to 2022,

Source: ILO

Here, real wages can be taken as a proxy for general prosperity, including the capacity for growth in household Consumption (comparable data for total government Consumption is not available across countries).

What is clear is that the growth of real wages in the G20 advanced economies has been extremely weak ever since the global financial crisis. No country in that group has reached 25% real wage growth. The US has achieved just 11% real wage growth over that period and is currently falling. In Japan, Britain and Italy real wages have actually fallen outright over that period.

There is a very different pattern in the emerging G20 economies. Indonesia, Russia, Turkey and India all have real wage growth above the best performer among the advanced economies, South Korea. And all of them are vastly outpaced by China, where real wages have risen by 1.6 times over that period.

At the same time, it is widely known that China has a significantly higher proportion of GDP devoted to Investment than the leading Western economies. It is frequently attacked in the Western financial press for its ‘excessive investment’. In fact, this is the official US position over many years, with the US Council on Foreign Relations arguing that not only China’s Investment but also its savings are too high!

However, it has already been noted that China’s wage growth is far in excess of the wage growth in the G20 advanced economies. Yet it can also be shown, so too is China’s Investment rate far higher. This is shown in Chart 3, below.

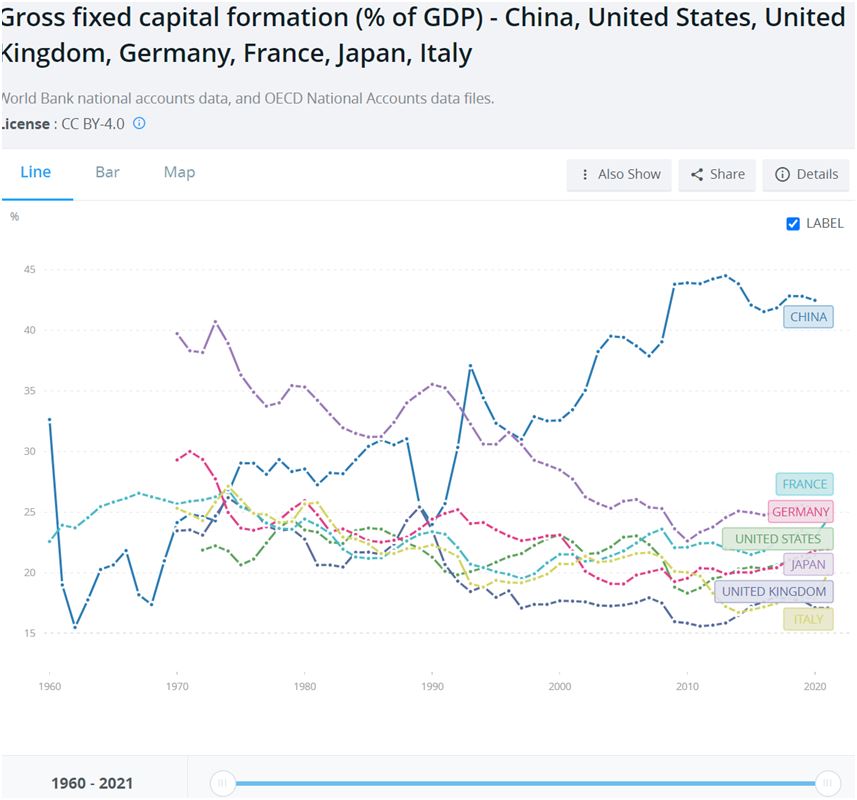

Chart 3. Gross Fixed Capital Formation, % GDP, in China and the G7 economies

Source: World Bank

Over the period shown, there is a general downward trend in the proportion of GDP devoted to Investment (Gross Fixed Capital Formation, GFCF) across the G7 economies. This was accompanied by the significant deceleration in the GDP growth of these economies over the same period, which is still taking place.

Lower Investment as a proportion of GDP accompanied by lower GDP growth is not coincidental. Bearing in mind that net Investment adds to the productive capacity of the economy (the ‘means of production’) it is entirely logical.

Yet at the same time, the trend in China has been in the opposite direction, with all the positive consequences for growth and prosperity that should be widely known. Naturally, as the proportion of GDP devoted to Investment in China has risen, the proportion of China’s GDP devoted to Consumption has necessarily fallen.

This apparent paradox, rising wages and Consumption taking place while Consumption falls as a proportion of GDP raises crucial questions of both economic theory and policy. In fact, there is no paradox.

The crucial point is that proportions are not the same as growth rates. Consumption and prosperity have grown at extraordinarily impressive rates in China because an increasing proportion of the economy is devoted to Investment. This rising proportion of the economy for Investment means a greater increase in the means of production, which allows the greater production of goods and services both for Consumption and for re-Investment.

Naturally, under certain specific and limited circumstances stimulating Consumption can induce growth, if it supports a rise in Investment. This might include examples where consumers had lost confidence because of some shock, and required a catalyst to Consume more or save less. But these incidents are time limited and based on a certain set of conjunctural circumstances. Consumption cannot drive growth because it is not an input to it. All strategies based on the assumption that it can have tended to result in failure.

The effectiveness and sustainability of all borrowing, whether for government, business or households is determined by these fundamental points. If borrowing is conducted for Consumption (from which, by definition there is no monetary return) it cannot be sustainable. If borrowing is conducted for Investment, as long as the return on Investment exceeds the cost of borrowing, then it will be effective and sustainable.

Under those circumstances there should the greatest optimal amount of borrowing, in order to maximise the rate of Investment growth, and ultimately maximise the growth in prosperity.

For government, Consumption, or current spending should be financed by taxation. In advanced industrialised economies it will be generally the case that good levels of public services generally need high levels of taxation.

Three different increases in the public sector deficit

There are three recent examples of deficit-financing, government borrowing for Consumption, from which there can be drawn important lessons.

In the current period, the pandemic and the Western governments’ disastrous response to it has produced a challenge to the Reagan/Thatcher ideology. The lockdown policies were too negligently porous to prevent the spread of the virus. As a result they were also extremely damaging economically. This was lethally damaging to public health and highly negative to economic activity.

A combined public health and economic crisis ensued. Western governments have been focused on the economic crisis.

One immediate consequence of this failed pandemic policy was to produce an extraordinary increase on Government Consumption spending. This was supposed to deal with some of the health consequences of the pandemic, to bail out firms and to boost Consumption in specific sectors (from hospitality, to restaurants, to housing, to car production and other areas). As we will see, the policies adopted were very far from a success.

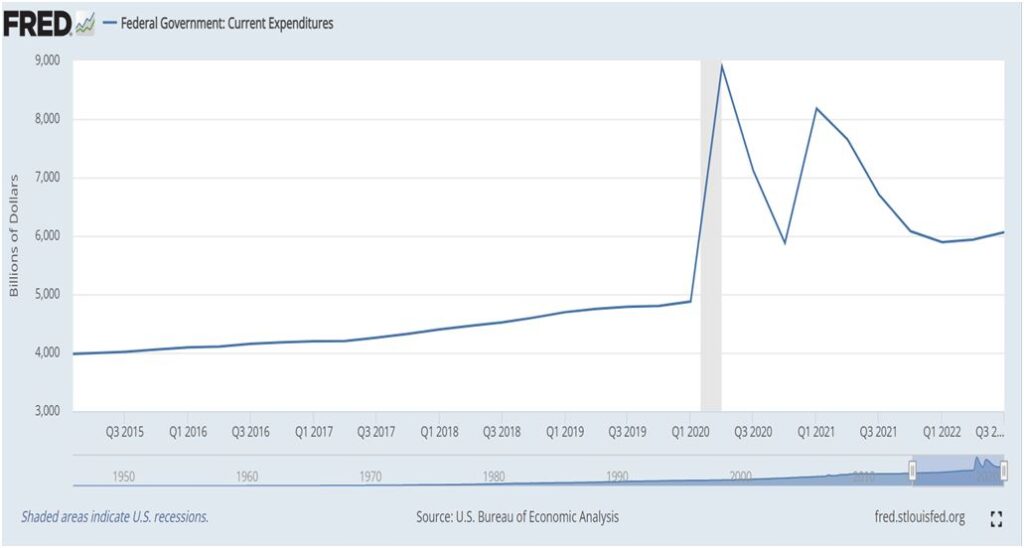

In the US, this huge boost to Government current spending during the pandemic was repeated shortly afterwards, in order to boost the economy coming out of lockdown. These huge increases in US Government Consumption are shown in the chart below.

Chart 4. US Federal Government Spending, US$bn

Source: FRED

In the 4 years prior to the pandemic US Federal Government Consumption rose gently from $4trillion to $4.8 trillion. In the following year it surged to $9.8 trillion and is now rising once more, well above the pre-pandemic trend.

It should be noted that there was no comparable increase in Government Investment in any of the G20 advanced economies.

For opponents of all government spending, whether Consumption or Investment, the Truss/Kwarteng experiment seemed to demonstrate that, in an era of free-flowing capital the bond markets will not allow a surge in government spending. Instead, this Reagan/Thatcher argument runs, they will punish profligate governments by refusing to buy the debt and/or demanding much higher interest rates to hold that debt. But this was not the US experience during its twin Consumption and borrowing binges related to the pandemic.

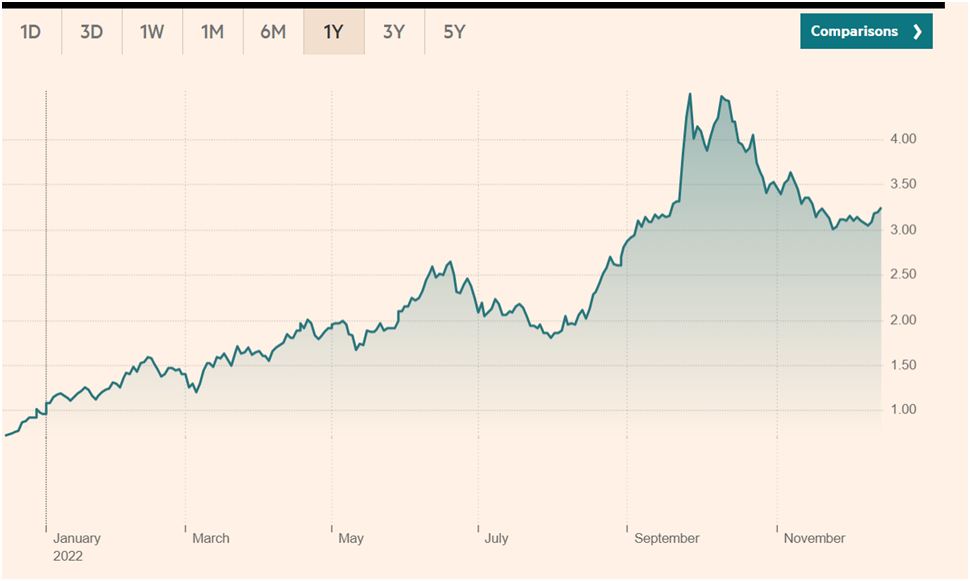

This is shown in Chart 5 below. In fact, there were two very distinct responses in financial market, and movements in government bond yield in opposite directions.

Chart 5. US-10 year Treasuries’ yields, %

Source: FT

The surge in borrowing began in the 1st quarter 2020. However, the first response of US Treasuries’ yields was to fall, not to rise. Two years later, in January 2022 they were still no higher than they had been prior to the pandemic, as shown in the chart above. Over that period, given the emergency nature of the borrowing to prop up the business sector and the absence of viable alternatives, bond yields had not risen.

It was only in the 2nd quarter of 2022, as it became clear that the increase in Government Consumption was not a one-off that yields on US government debt began to rise sharply. This took yields up from 1.5% to 3.5%. Yet these seemingly small numbers, when combined with the total level of government borrowing, represent a huge drain on resources.

The Congressional Budget Office (CBO) estimates that the net effect of increased debt and higher interest rates would drive up net interest costs from well under 10% of Federal government revenues to over 40%. As noted previously, the rise in interest payments in this way naturally supports the growth of the finance sector at the expense of the productive economy. Even the US government eventually found that there was not an unlimited capacity to borrow to finance Consumption.

Closer to the present period, Liz Truss’s premiership became one of the shortest in British history because it was directly brought down by global financial markets’ reaction to her own economic policy. The policy was also a version of ‘deficit-financing’. It may have been modelled on the recent experience in the US. However, this type of increased Government Consumption was not in the form of public services, but on tax giveaways to big business and the rich amounting to £75 billion.

It is widely understood that there was a significant and negative market reaction to that policy. While the currency initially plummeted, it has since recovered after Truss and Kwarteng were both displaced.

Chart 6. UK-10 year Government Bond yields, %

Source: FT

The reaction of the bond market to the British deficit-financing experiment was also swift and brutal. The rout in the bond market was only halted with the ousting of both Truss and Kwarteng, and the equally swift pronouncement from their appointed successor Sunak that he would cancel this deficit-financing (which is sometimes called ‘tax spend’, meaning tax giveaways).

In these two transatlantic experiences, the rise in yields in the US and Britain appear to be rather similar. Both jumped from about 1% to about 3.5%. But this actually masks a very different reaction in the bond markets.

First, the rise in US Federal government spending continues (not least after the military Budget was increased by 8% to $858 billion for 2023). The British government was very rapidly obliged to drop its planned increase in spending/tax giveaways entirely.

Secondly, the relative sums involved are qualitatively different. An increase in the budget deficit of £75 billion is equivalent to approximately 3% of British GDP. In the US, the cumulative rise in Federal Government Consumption Expenditures over the previous trend now amounts to $16.6 trillion (author’s calculations) between 1st quarter 2020 and 3rd quarter 2022. This is approximately equivalent to 66% of current US GDP.

The US government can get away with a certain level of deficit-financing in the current period, although it pays a significant price for that in the form of much higher debt interest payments. The British government, seeking to do a much more modest version of the same policy found it could not do anything at all, with the negative financial market reaction doing away with both the policy and its parliamentary architects.

Conclusion

Investment in the productive capacity is the main determinant of economic growth, so borrowing for Investment is sustainable and is generally required in order to achieve growth (unless Investment can be financed from own resources).

Consumption is not an input to growth. So, borrowing for Consumption will not lead to increased growth and is therefore not sustainable.

The US and other Western economies have allowed a significant rise in the proportion of the economy devoted to Consumption. This has led to weak growth in the economy and in measures of prosperity such as wages over the medium-term. By contrast, China has had much stronger growth based on increasing Investment as a proportion of the economy. This in turn has enabled strong economic growth, as well as growth in real wages and in prosperity.

The policy of deficit-financing, or increasing borrowing to finance Government Consumption, in the Western economies has not led to improved growth over the long run. In the recent period, Western governments borrowed to save the economy form the effects of their lockdown policies in the pandemic. There was no negative impact on government borrowing costs in response.

However, there was a costly negative response when the US repeated the borrowing, and interest payments will now consume a greater part of government revenues as government borrowing costs have risen.

Even so, is the current era this type of deficit-financing is only open to the US because of the role of the US Dollar which continues to dominate global capital flows. This includes global bond portfolios. In a certain sense, many investors are compelled to buy US government debt, although they may demand a higher interest for doing so.

This is not an option that is available at all to other countries, such as Britain, whose currencies do not play that role, who have very few forced buyers and who have removed all capital controls.

This is a key lesson for the Western left. It cannot advance on economic policy by clinging to the failed nostrums of the post-World War II consensus. In particular, borrowing for Consumption is counter-productive in terms of growth and prosperity. Therefore it cannot at all be used to transform the economy to operate in the interests of working people and the poor. Consumption must be financed from taxation, heavy taxation if appropriate.

Growth and prosperity are determined by Investment. Therefore ,borrowing should in general be reserved for Investment, which should be utilised to the maximum sustainable capacity to optimise growth. This in turn leads to growth in prosperity, Consumption and wages.

The Covid-19 crisis is not over. Over 400,000 people a day globally are contracting the virus and about 1,500 a day are dying, according to the ‘Our World in Data’ website which uses John Hopkins University data.

Naturally, for countries and governments which claim to have defeated the virus these terrible data represent a very uncomfortable truth. This fiction is quite widespread but throughout the pandemic has largely been most widely circulated in the richest countries grouped in the G7.

The reason for this was relatively straight forward. Quite contrary to most medical and social practice over several hundred years, civilisation has demanded that the source of a pandemic must be identified and everything possible be done to contain and remove it. In pre-Enlightenment Europe, for example, there are famous cases of whole villages sacrificing themselves to the bubonic plague in order to prevent its further spread.

This precedent was overturned quite early on in the pandemic in the G7 countries (with the partial exception of Japan). Instead, the authorities at various times but in a co-ordinated manner decided that the economic price of combating this virus was too high, and the interests of business must come before the health of the population. The policy was summed by Dominic Cummings, then an aide to Boris Johnson, who quoted the former Prime Minister as saying the policy was to “protect the economy, and if that means some pensioners die, too bad.”

Johnson claims he did not use those words. But it rapidly became clear that in the richest Western countries, this became the practical content of government policy, and was implemented by numerous agencies.

According to John Hopkins University data the Covid-19 global death toll now stands at over 6.6 million. But the recorded death toll in the G7 is now well over 1.6 million. This is despite the fact that the G7 accounts for less than 10% of the world’s population. Yet it also accounts for just under one quarter of the world’s total Covid-19 deaths.

A similar pattern is evident in terms of cases, where the G7 accounts 247 million of the world’s recorded cases of 638 million. The G7 accounts for more than 3 in 8 of the world’s recorded cases despite representing less than 1 in 10 of the world’s population.

It is possible that a similar pattern can be seen in relation to Long Covid, although the data in this category is less reliable than others. All of these much worse public health outcomes, it should be noted, is despite the advantages of greater access to vaccines, better underlying health of the population and greater access to advanced medical care.

In Britain, 2 million adults report the continuing effects of Long Covid, which is 5% of the adult population. This in turn is contributing to a persistent health crisis, which in turn is hobbling the health services and the economy. Chronic underfunding of the NHS plays a significant role too. But on the key measure of waiting times for elective care, the number of people waiting for care has surged from 4.24 million pre-pandemic to 7.07 million in September 2022.

One factor here will be the impact of the virus on the NHS workforce itself, which was sent into battle without the proper personal protective equipment, which had serious and even lethal consequences for their health. NHS staff will be among those disproportionately effected by Long Covid, as they were for infections.

The other factor was that partial lockdowns, which were prolonged but lax, meant that needed healthcare was postponed while the many different variants were allowed to spread and mutate.

Taken together, the G7 governments’ approach (with the partial exception of Japan) was a public health catastrophe, one which has not ended. Life expectancy is now falling in the US, with ethnic minorities hid hardest. A similar pattern is seen in Britain. This reverses decades of progress on the most fundamental measures of the well-being of the population as a whole.

This is because the priority was the economy. But the economic impact too has been barely short of catastrophic, with analyses now commonplace that the recovery from the effects of the pandemic will be some years in the distance.

The South-East Asian Exception

There is an objection to the John Hopkins data, even though it remains the most authoritative. It is said that the richest countries are accurately reporting their cases and deaths, whereas poorer ones are not.

If this is true at all, it is only by degree. For example the British authorities have given up on reporting cases almost entirely. But the partial exception of Japan invalidates any claims that the G7 data is so skewed as to invalidate all comparisons.

Japan is also a member of the G7. But in mid-January of this year Japan had by far the lowest level of per capita cases and deaths. At that time Britain was the worst in the G7 on both measures. Cases were over 14 times higher on a per capita basis than in Japan and over 18 times higher in terms of deaths.

This was part of a general pattern in South East Asia at the time. It is possible that the recent experience of SARS in the region had generally made the regions’ populations more cautious, more compliant with anti-Covid measures and more likely to wear masks.

However, the same G7 countries that had allowed their own population to die in great numbers had already begun an anti-Zero Covid campaign on the familiar grounds that it was bad for trade and for business. That campaign was gradually and lethally successful. The virus spread rapidly across the region and Japan itself moved up to 6th in the G7 league table of cases.

Of the largest economies now only China maintains a Zero Covid policy. Despite persistent campaigns urging abandoning the policy, China has had far better outcomes both in relation to public health and to economic growth.

Economy unprotected

In broad outline, the mainstream neoliberal view of the economy is that wealth is created by entrepreneurs and that the main role of the mass population is to perform the tasks set by these entrepreneurs, and to consume the goods and services that are produced as a result.

This inverts reality. The main factor driving the economy is labour, and, aside from adding more labour, growth is mainly dependent on the expansion of the means of production through Investment.

The wrong framework contributed decisively to the catastrophic outcomes both in terms of public health and economic well-being. As labour is the decisive input to the economy, protecting the population’s health is a decisive element in maintain economic output and well-being. All misguided attempts to kickstart the economy through increasing Consumption have been damagingly counter-productive.

In Britain Rishi Sunak initiated the policy of ‘eat out to help out’, in effect government subsiding restaurants by paying people to eat in them. Academics at Warwick University found that the government spent £500 million on the scheme, with limited economic impact but causing ‘somewhere between 8% and 17% of all new Covid clusters’ in the summer of 2020.

Not only did these policies fail, they contributed to the long-term ‘scarring’ of the economy in two ways. As already noted, promoting consumption in the middle of a pandemic simply contributed to its growth and all the negative long-term consequences that followed. Secondly, the recklessly negligent approach has not only had long-term health consequences but also damaging economic outcomes too.

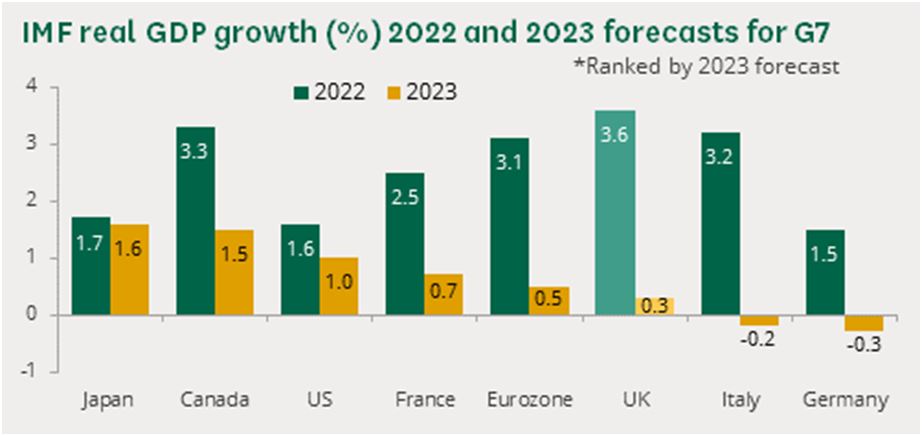

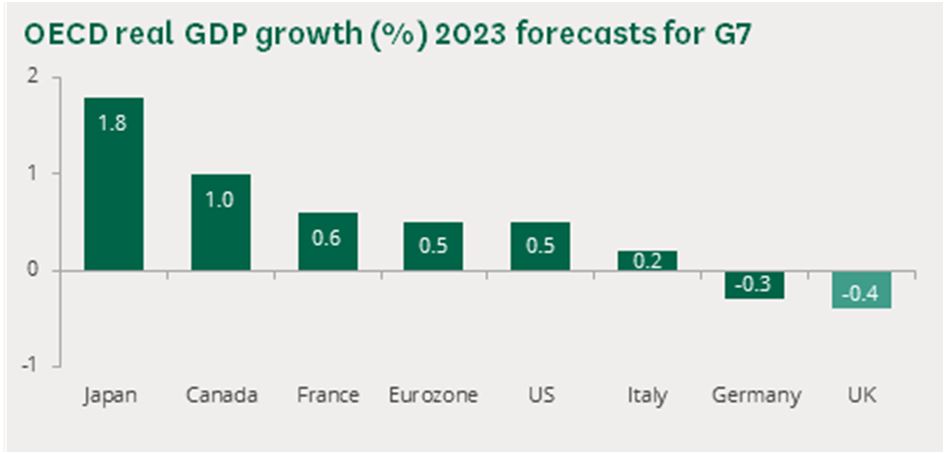

According the G7 governments the pandemic has essentially been over since the end of 2021. This is false, but provides a baseline for assessing the economic outlook. According to the IMF, the US will have the weakest real GDP growth in the G7 in 2022, at 1.6%. Both the OECD and IMF agree that 2023 will be worse, with the best growth in the G7 being Japan’s, which in 2023 is expected only to equal US growth this year. Following one of the sharpest (if shortest) recessions on record, this is a miserable performance.

Two charts on growth in 2022 and 2023

Source: House of Commons Library

There is no economic rebound in the G7, and nothing like a ‘boom’. Everywhere is stagnation or slump.

One factor in the economic weakness is simply the absence of workers. In the US, the Brookings Institution estimates there are up 4.1 million workers who have dropped out of the labour force due to Covid. In Britain, ONS data show that the long-term downtrend in the numbers of people off work due long-term sickness abruptly reversed at start of the pandemic and the total is now over 2.5 million people, a record high. At the same time, job vacancy numbers are also close to a record high of 1.25 million.

As labour-power is the decisive factor in production, any significant reduction in the supply of labour will have serious negative effects. This is what happened as a result of the virus and the disastrous response to it.

Conclusion

The clamour to prioritise the economy ahead of public health showed a callous disregard for human life and well-being. It was not accidental that it was led by the richest countries.

However, their failure of basic morality was accompanied by dangerous misconceptions about how their own economies work, clouded by self-interest. Together this has become a twofold attack on the bulk of the population, in terms of public health and economic prosperity. It is not a model that should ever be emulated or repeated.

It is possible that a much more detailed analysis of Thursday’s Autumn Statement will be required, not least because its impact will dominate both the economy and the political debate for the next period. If so, that analysis can also be informed by insights from others, including the Institute for Fiscal Studies, the Resolution Foundation, the Joseph Rowntree and the Women’s Budget Group. But below is the initial reaction to the Statement.

This was another austerity Budget. Hunt and Sunak say it will amount to a total of £55bn in fiscal tightening. According to the Office for Budget Responsibility (OBR) this is nominally more than the Osborne and Cameron 2010 package, yet less in terms of percentage of GDP.

The OBR economic forecasts are grim, as recession is combined not only with huge inflation currently at 11%, but a forecast of 7.4% average CPI for the whole of 2023. The OBR reckons that living standards will fall by 7% this year and next, which is unprecedented in most people’s lifetimes. Even this is an average, with some pensioners and the super-rich being protected. Most ordinary people, workers and the poor, will see a far larger fall in living standards. Unemployment is also forecast to rise, which is quite something given current labour shortages (which are a function of too low pay). There was no word at all on public sector pay, so we should assume the worst. The government seems to be relying on well-below inflation recommendation from the public pay bodies.

The reason given for the austerity is the impact on government finances of the economic downturn/recession. Inflation was also offered as an excuse. But worsening government finances are inevitable as government receipts fall and unplanned expenditures rise when there is economic weakness. The underlying trend in the public sector deficit is down. Inflation was caused by the unprecedented US economic policy in 2020. So, in the famous and correct phrase, austerity is a political choice not an economic necessity.

There are three ways in which the austerity will be implemented. The first begins immediately as support for household energy bills begins to be withdrawn and public sector is sharply cut in real terms. Secondly, spending is not remotely matching inflation. This means very big real terms cuts when inflation is at 11% and further big price rises are expected next year. Thirdly, many of the big cuts in nominal spending are slated to take place in two years’ time, that is, after the next election.

If it were really necessary to have austerity (it isn’t) there could be an argument for postponing austerity until after a recession is over. But this is a purely political move – a Tory elephant trap for Labour.

Part of this is to postpone announcing decisions that in reality have already been made. So, there were also at least 3 reviews announced by Hunt in his Statement, into Universal Credit, the state pension age and NHS ‘efficiencies’, all to report before the next election. But Hunt has already planned and budgeted for the government cuts to be implemented in advance, so the main thrust of these reviews is already known- more cuts.

The idea is to get Labour to sign up to these same cuts across the board. If Labour does, the Tory hope is that the political gap between them and Labour is narrowed to the extent of giving them a fighting chance of winning the next election (or not losing disastrously as current polling indicates). If Labour refuse Tory spending plans, the claim will be that Labour will put up your taxes. This will be the centrepiece of the Tory election campaign (as well as anti-Corbynism).

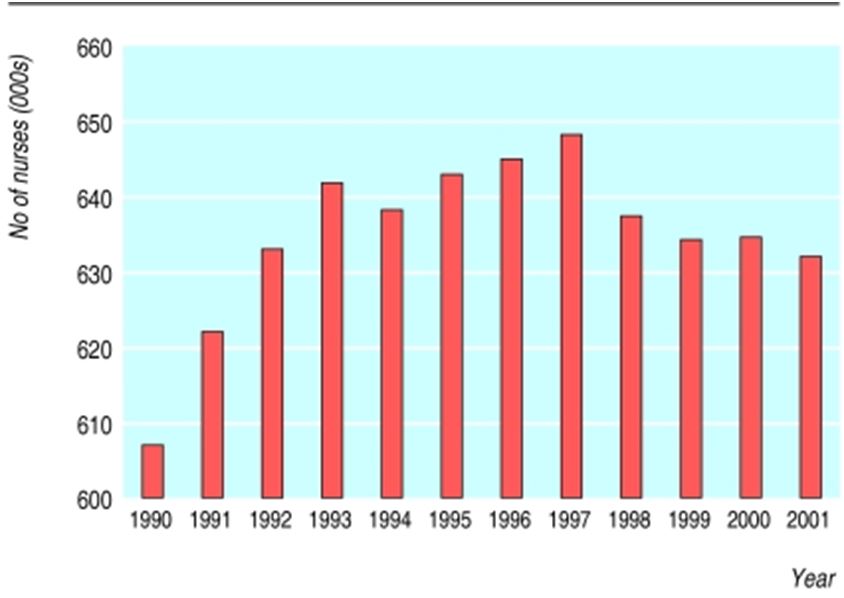

A similar elephant trap was laid by Major and Clarke ahead of the 1997 general election, when they dared Labour to commit to their own eye-watering spending cuts in the first two years. Labour did commit to them which produced a slump in public services, with nurses memorably leaving in droves because of pay restraint (as shown in the chart below).

Source: National Library of Medicine

Strategically, these are small state Tories, intent on deregulation, privatisation, lower wages and lower union rights. This Statement is part of the planned Americanisation of the economy. The determination to pursue this project overrides even the short-term considerations about Tory polling prospects.

However, this analogy with 1997 breaks down in the comparison of economic circumstances and the state public services. In 1997 the economy was growing reasonably well and public services (including employment) had been improving after the debacle of the Exchange Rate Mechanism.

The situation is the opposite now. The economic outlook is dire and public services are in crisis, especially the NHS. The NHS cannot afford the planned cuts, whichever party implements them. They would also lead to widespread popular dissatisfaction or unrest.

There is an alternative. This is highlighted by the fact that that there is a big disparity between the economy and living standards. As Hunt says, even now the OBR still forecasts 4.2% real GDP growth for 2022. Yet living standards are falling. Simple maths means someone else is benefitting from that growth. This is an extreme example of a medium-term economic trend; meagre economic growth has been accompanied by falling living standards.

The beneficiary of that growth has been the big companies and banks, the profiteers, price gougers, landlords and others. Again, Hunt showed the way. His 45% time-limited windfall tax levy on energy producers alone is reckoned to produce £14bn in revenues. This is one-quarter of the total package he announced.

But there is no reason in principle not to raise levies of 100% on windfall profits, especially as energy company investment is already subsidised. Better still, taxes could be increased across the board on all those benefiting from the current crisis.

Of course, nationalisation would deal with this problem permanently. The State could then raise the level of sorely needed investment, remove shareholder dividends and excessive pay and still keep prices low.

Investigators in financial crime tell us to ‘follow the money’. Austerity is an economic crime against the vast bulk of the population. The alternative to Tory austerity is to follow the money to those who have got their hands on what properly belongs to the public, and use it for public investment, decent incomes, and proper public services.

The inflationary surge is global. It is causing severe hardship in the advanced capitalist economies and economic disaster, social and political turmoil in large parts of the Global South. Reversing this crisis requires both identifying its source and adopting policies directed at that source.

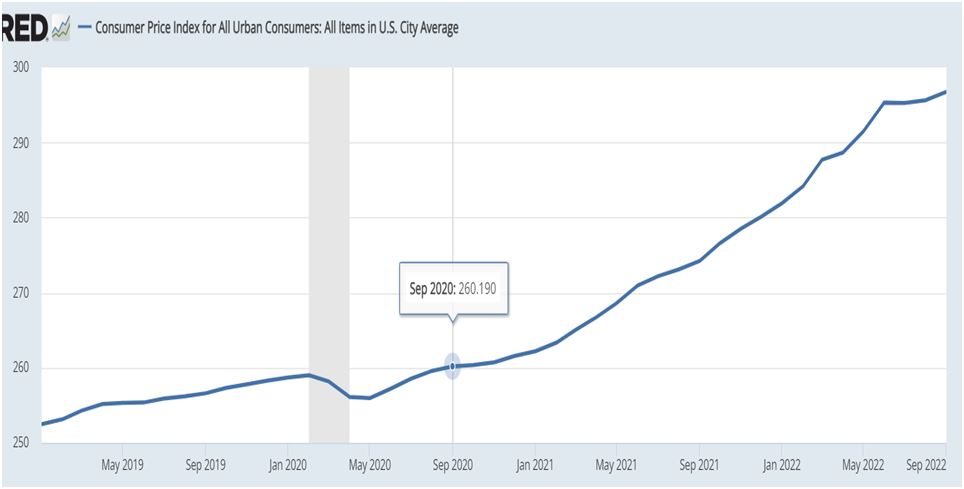

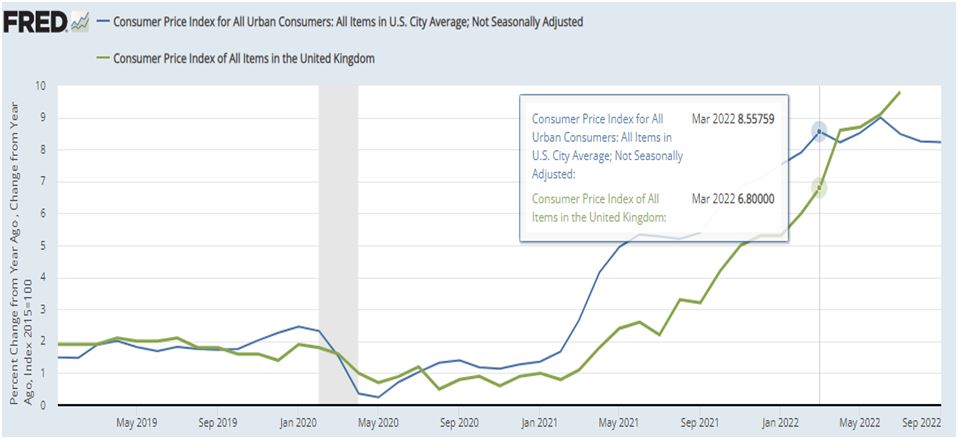

Chart 1. US CPI inflation index, January 2019 to September 2022

Source; Federal Reserve database (FRED)

Over that period of rising inflation, the cumulative rise in the CPI index has been 16%. Three-quarters of the entire rise in US CPI took place before the war began. Even if we assume that that the entirety of remaining rise was entirely caused by the war (which is not a reasonable assumption), then it is still case that the vast bulk of the rise in prices took place before the war.

SEB has also previously shown that the cause of the inflationary surge was the extraordinary and unprecedented expansion of both US Government Consumption and US money supply. As this followed a prolonged period of weak growth in Investment these policies meant a huge stimulus to the economy when there was no capacity to supply an increase of goods and services. The result was first US, then global inflation.

Money creation

There is one argument that should be addressed, not because it is powerful but because it is both widely shared and completely wrong. This is the claim that ‘poor people don’t have too much money, so the cause of inflation cannot be too much money’. This tends to be put forward by various supporters of the idea that money creation is a panacea, and that production is not central to the economy or the well-being of the population.

It was exactly this type of nonsensical think that drove the Biden administration, among other things, to sending cheques to the population to help out with rent, which had the effect of pushing up rents in the US. Rent controls combined with homebuilding are the appropriate response.

Fundamentally, money creation of this type ignores the existence of social classes and the enormous body of research ever since the GFC and the bank bailout, that relying solely on money creation benefits only the rich and the owners of capital (including landlords). It is perfectly true the poor have no money, but vast money creation makes them poorer still as the owners of capital push up prices.

No surprise of persistently high inflation

In recent months financial markets have repeatedly been thrown off guard by persistently high US inflation. This has led to both a rising US Dollar and rising intertest rates.

Both of these market responses have negative consequences for the rest of the world. A stronger Dollar leads to further upward pressures on inflation as most global commodities remain priced in US Dollars. In addition, global costs of borrowing tend to rise at least as fast as US market interest rates. Here the dominant role of the Dollar is also decisive as the US effectively sets the floor for global interest rates. (Other countries can and frequently can do have lower long-term interest rates, but their currencies play nothing the same weight in global lending).

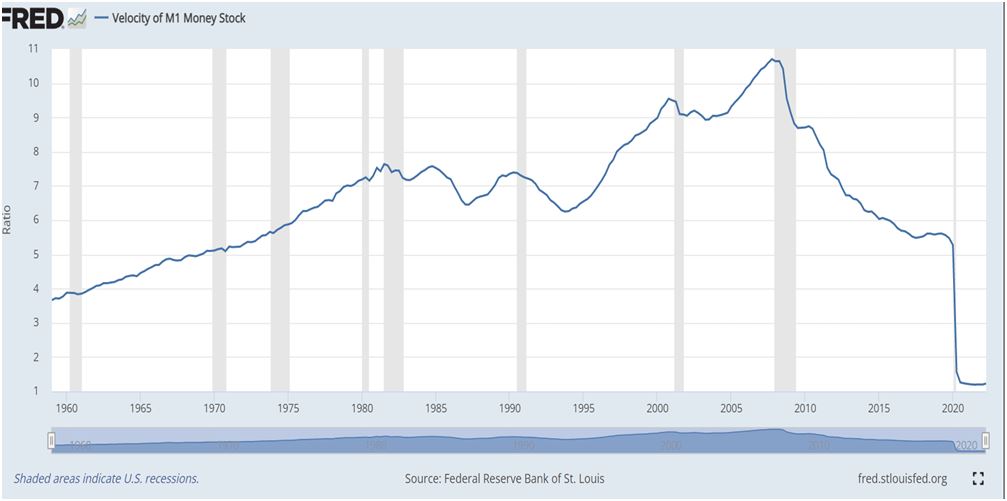

This is shown in the chart below. The velocity of money is a measure used mainly by monetarists, but also others. It is simply the level of money GDP divided by the level of M1 money supply. To return the ratio to its previous lowest ever level would require money supply to be cut by two-thirds from current levels. To return to the previous high-point (and there has been a long-term growth trend in the velocity of money ratio) would require current M1 money supply levels to be cut to less than one-eighth of its current level.

Similarly, while US Government Consumption is not rising as fast as in 2020/21, there is no reduction and may not be, even after the US mid-term elections. Both monetary policy and US Government Consumption remain highly inflationary.

Chart 2. US Velocity of M1 money supply, Q1 1959 to Q2 2022

Source; FRED

Transmission to other countries

As noted above, the global dominance of the US Dollar means that US economic and financial conditions are transmitted to the rest of world. This takes place through a number of related mechanisms; dominance of the US Dollar in global commodities’ prices, setting a floor on global market interest rates and direct currency effects in the exchange rate with the US Dollar.

Even extreme changes in the US are magnified for most countries, but especially for those dependent on overseas capital or who suffer under unequal terms of trade. The countries most badly affected by gyrations in the US economy and financial markets therefore tend to be grouped in the Global South.

International forecasters such as the IMF, World Bank and others have been slashing growth forecasts for world economy including the Global South. In addition, inflation is expected to be rampant in many countries, with double-digit inflation not just last year but forecasts of similar over several years to come. Argentina is one of the worst, with CPI inflation of close to 50% expected for many years to come, close to the hyper-inflation that destroys all fixed incomes and savings.

In the advanced industrialised economies the outlook is not as grim. But Britain is now among those where CPI inflation is above 10%, as is the Euro Area as a whole.

The correlation between US and British inflationary pressures is shown in the chart below. There is a comparable pattern with inflation in the Euro Area. Measured in terms of year-on-year inflation, US CPI began to rise in late 2020. Britain followed a few months later. But British price rises did not exceed those of the US until after the Ukraine war began.

This confirms that the inflationary pressure emerged in the US, especially as the Euro Area price rise is in lock-step with Britain’s. It also completely undermines any idea that inflationary pressures emerged as a result of ‘Chinese supply bottlenecks’ as China itself has experienced no similar rise in prices at all.

Chart 3. US and UK CPI inflation from 2019 onwards

Source: FRED

Almost exactly half the British (and European) rise in prices cannot at all be attributed to the war or its indirect consequences, as they took place before the war began. It is not possible to accurately disentangle the sources of price pressures after that date, but is certainly some combination of US economic policy and the price rises as a result of the war.

But even these are indirect consequences, as it not the case that Russia has cut off Western European countries from energy supplies. Instead, it is those countries that have imposed sanctions on Russia, including a boycott of its energy output.

Reversing the inflation trend

For the world as a whole the two key measures which would see a rapid decline in inflation would be:

A reversal of the US mix of fiscal and monetary policy that created the inflationary impulse

The ending of war-related sanctions.

Naturally, for policymakers in the US there are other priorities. These may have included a misconceived attempt to kickstart the US economy to vault over its rivals, the political impossibility of withdrawing massive stimulus before the mid-terms and the war.

For European and other governments who cannot determine US policy the biggest single contribution they could make to suppressing inflation would be to abandon the sanctions regime. This would also benefit countries from the Global South who suffer not only energy price rises but also grain and fertiliser shortages as part of the sanctions regime.

In addition, they could take specific measures to curb energy prices by windfall taxes or legislation to curb profiteering. Some European countries have taken these measures, such as France.

There should also be significantly increased investment in renewables as well as market measures to ensure that their actual price advantage over fossil fuels, gas in particular, is allowed to operate. There must be no more tying of renewable energy prices to gas prices, to subsidise the gas producers.

Structurally, the inflation burst is a reflection of the long-run decline in Investment in the advanced capitalist economies. The US authorities gave a huge boost to Consumption, but without Investment there was no capacity to meet it. The policy of the central banks is now a disastrous one of pushing down Consumption growth to the low level of Investment; causing a slump to lower inflation.

The logical and far less damaging course is to increase Investment and raise capacity. Done in a timely way this would lead to lower inflation and avoid or at least curtail a slump. The starting point should be the needed investment in renewables plus energy saving and insulation, as well as switching to extensive networks of environmental public transport and public housing.

The current crisis was made by policy choices, and it can be unmade by better ones.

Coming the week after the Tories pledged to resume fracking, Labour’s plans for a publicly owned energy company have been widely welcomed, with parts of the left triumphant at putting public ownership back on the agenda. But beneath the shift in tone, Labour’s proposal fails to understand the deeper causes of the energy crisis, leaves in place the vast majority of Margaret Thatcher’s energy privatisations and is unlikely to deliver significant savings for the public. It also falls drastically short of what is needed to manage the climate emergency.

Coupled with a commitment to decarbonise the electricity system completely by 2030 and pitched as a response to the energy bill and climate crises, Great British Energy (GBE) would invest in new renewable energy generation alongside the private sector. With rising wholesale gas prices underpinning skyrocketing energy bills, this would reduce reliance on gas by helping to increase the supply of renewable energy.

Leaving aside the long-term nature of this solution to what is a very immediate problem (fuel poverty is likely to remain in excess of the 6.7 million households reached in April this year), it is not clear that increased renewable generation will translate into lower bills.

Many energy supply companies are also involved in energy generation: making enormous profits throughout the energy crisis thanks to higher wholesale prices being passed on to customers. Generation and supply are, however, separated by a series of markets, guaranteeing that the prices we pay are determined by demand and supply at an international level. Simply inserting an additional generation company leaves this dysfunctional system intact.

In contrast with the TUC’s proposal to also establish “public ownership within the customer-oriented parts of the energy system”, GBE will have no way of directly affecting bills, and an operator on its scale is unlikely to have much impact on wholesale prices.

Worse still: in Britain’s wholesale electricity market, the most expensive generator – gas – sets the price, as energy Professor Michael Grubb has explained, with households and businesses paying far more for their electricity than what it costs to generate it from renewable sources. Additional renewable generation, while leaving the privatised supply and wholesale market untouched, will not change this.

While the wholesale price of energy has driven up bills, it still accounts for only 51% of a dual (electricity and gas) household bill. 11% of household bills pays for the profits and running costs of energy supply companies and 18% for companies responsible for transmission and distribution. These aspects are will remain in private hands under Labour, despite record profits made by transmission and distribution companies during the crisis. Distribution networks enjoy the highest profit margins of any sector in Britain and use household bills to pay out billions in dividends and interest on intercompany loans. National Grid reported a 19% increase in pre-tax profits from 2020 to 2021, while earnings per share increased from 36.3p to 46.3p. The flipside of this profiteering is poor investment and infrastructure quality.

Starmer rightly asked why the private sector should be the main beneficiaries from the carbon transition, as they were from North Sea oil. But GBE will have little opportunity to change this given its limited scale, the need to establish itself in a large private-dominated market, and a likely mandate to undertake riskier new investments, effectively de-risking climate transition for the private sector. EdF, the French state operator with which it has been compared, is responsible for the vast majority of generation capacity as a result of its history as a state monopoly founded by nationalisation. GBE will have no such advantage.

What, then, about the climate crisis? Any additional renewable generation is not to be sniffed at but here Labour’s commitments are again woefully unambitious. The £8bn pledged for renewables projects (including but not limited to GBE) is the same amount Labour’s 2019 manifesto committed for additional wind power generation alone. The 2030 target for 100% renewable electricity is only five years earlier than the government’s current plans and ignores heat, which is much more gas dependent than electricity.

Labour published 30 by 2030 in 2019, a report written by a team of climate scientists and engineers that set out thirty recommendations to decarbonise heat and electricity at a pace they judged to be the upper limit of technical feasibility. Labour’s 2019 manifesto committed to deliver these recommendations through a £250bn ‘green transformation fund’ and an integrated and publicly-owned system of energy generation, transmission, distribution and supply, largely removing the ‘need’ for competing electricity suppliers to charge prices dictated in international markets.

Starmer’s announcement represents a huge rowing back from these commitments and a tragic wasted opportunity to take historic steps towards solving the energy and climate crises. As encouraging as it is to hear public ownership back in Labour’s lexicon, GBE falls far short of what the public and the planet need.

The above article was originally published here by Labour List.

The ‘mini-Budget’ delivered by Kwarteng and Truss was so devastatingly bad for the British economy and for the key finacial markets that one major international bank ended the day calling for an emergency interest rate rise by the Bank of England!

Of course, this would do nothing to alleviate the economic crisis that underlies this slump, and may be just special pleading by financial speculators. But it is an indicator how far removed this government is from economic reality.

As such they will completely fail to deliver on their stated aim of lifting the long-term growth rate of the economy from abysmally low levels. Instead, they are engaged in fantasy Thatcherism, an effort to Americanise the British economy with a policy of hammering workers and the poor, susbsidising big business and the rich. The are likely do enormous damage before failing.

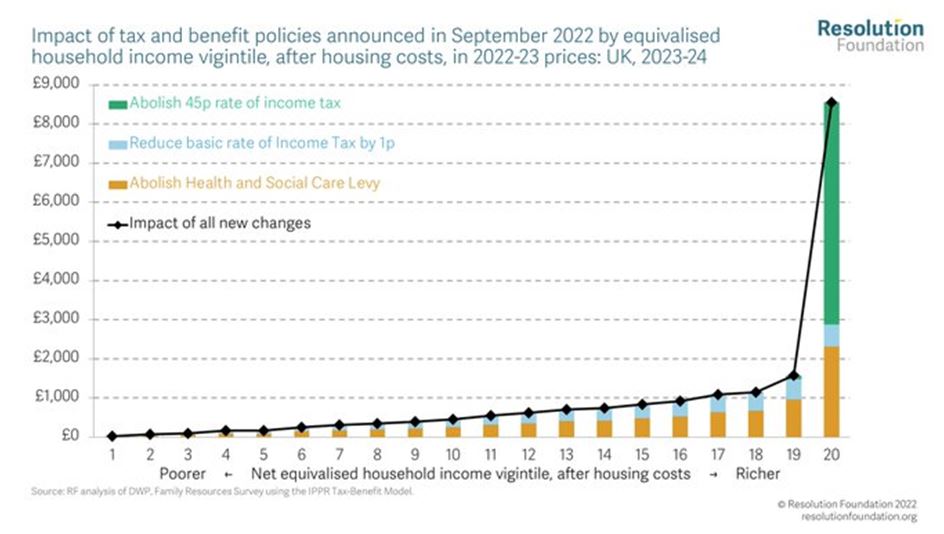

Numerous commentators have pointed how regressive the government’s measures are, in redistributing upwards for high earners and for owners of capital. This is how the Resolution Foundation explained this reactionary redistribution, shown in Chart 1, saying, “Almost half of the gains from tax cuts next year go to the richest 5% of households. The poorest half get an average of £230 vs £3,090 for richest fifth.” Overall, taking into account all changes to tax and National Insurance, “only those earning over £155,000 will be better off.”

This is just 1.4% of all taxpayers. This is economics of and for the 1%.

Chart 1.

Source: Resolution Foundation

At the same time, there is an enormous tax giveaway for businesses, amounting to tax cuts of just under £70bn in taxes on profits over the next 5 years.

All of these measures are being enacted when the mass of the population is struggling with the deepest crisis of living standards in living memory. The message to workers and the poor, ‘Go to hell!’

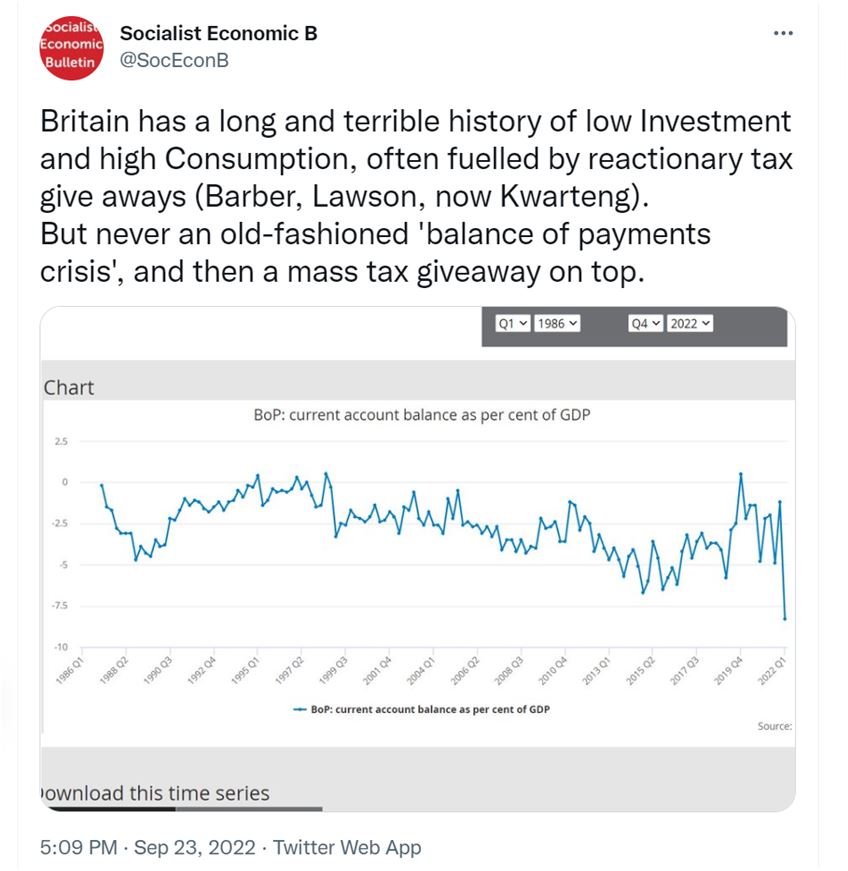

A balance of payments crisis

This wilful disregard of the objective reality is not confined to the issue of the impact on households and the cost of living crisis. The mini-Budget simply failed to take account of the key problems of the British economy, which is why the response of financial markets was panic, rather than horror from the population.

Britain has a long and unhappy history of ‘balance of payments crises’. These reflect the British economy’s chronic lack of Investment, leading to both weak productivity growth and lack of competitiveness.

The catalyst for these long-term trends to turning into an outright crisis of a falling currency and rising interest rates on government (and other debt) has frequently been tax cutting Budgets. These only served to suck in imports further, weaken the pound and make government debt unattractive to overseas investors without offering much higher interest rates. This is what happened in both the Barber and Lawson Booms.

We can now add the name Kwarteng to this rogues’ gallery of Tory Chancellors. However, a key difference with his predecessors is that the current Chancellor implemented the enormous giveaways to business and the rich when there was already an old-fashioned balance of payments crisis under way.

This is how SEB characterised the comparison on Twitter.

The basis for the British economy’s repeated balance of payments crises has the same sources as its weak growth, weak productivity and low wages. This is its chronically weak levels of Investment.

There is too the specific factor of Brexit. But it is not simply a case that Brexit has made it harder to export goods to the EU. It is worse than that, as shown in Table 1.

Table 1. UK Trade Balance in Goods with the EU and non-EU Countries, £bn

EU

Non-EU

Q1 2022

-30.2

-31.0

Q1 2021

-16.9

-12.7

Q1 2017

-24.2

-11.2

Source: ONS

The overall deterioration in the trade performance in goods certainly accounts for more than the overall widening of the current account deficit. The trade deficit has widened significantly. And the UK trade balance with the EU between the 1st quarter of 2017 and the same quarter in 2022 has certainly deteriorated, as shown in Table 1.

However, the widening of the trade gap is more pronounced outside the EU. In addition, UK exports to the EU are slightly higher than they were at the beginning of 2022 than in the same period in 2017, £42 billion versus £39 billion.

But trade is not simply about one country selling a food to another. There are incredibly complex cross-border supply chains that operate particularly in advanced manufacturing. The British economy has been a major importer of these semi-finished goods, as well as a major re-exporter (in European terms) of either finished goods or semi-finished ones, with some value added. There has been a surge in imports of these semi-manufactures from outside the EU without any corresponding rise in exports to the same countries. In effect, it appears as if Brexit has cut out Britain from existing supply chains in Europe, and companies based in this country will have had to replace them with more expensive and/or inferior products.

Naturally, this sharp adjustment in Britain’s place in global supply chains will further depress Business Investment. While virtually all major capitalist economies have experienced a pronounced decline in levels of Investment over decades, the downturn in British Investment has been even greater. This has been a chronic malaise, now made acute ever since the outcome of the referendum in 2016.

Chart 2. Investment (Gross Fixed Capital Formation)as a % of GDP in the EU, US and UK since 1970.

Source: World Bank

Why have they done it?

Clearly this government is not primarily concerned with courting popularity, unlike Johnson, Cameron or even Thatcher who lied about their intentions. Nor have they taken much account of the likely response in financial markets, where a falling pound will add to inflation and rising interest rates will deepen the downturn.

As a result, in deepening the structural failings of the British economy they have created additional problems for themselves politically. So, why do it?

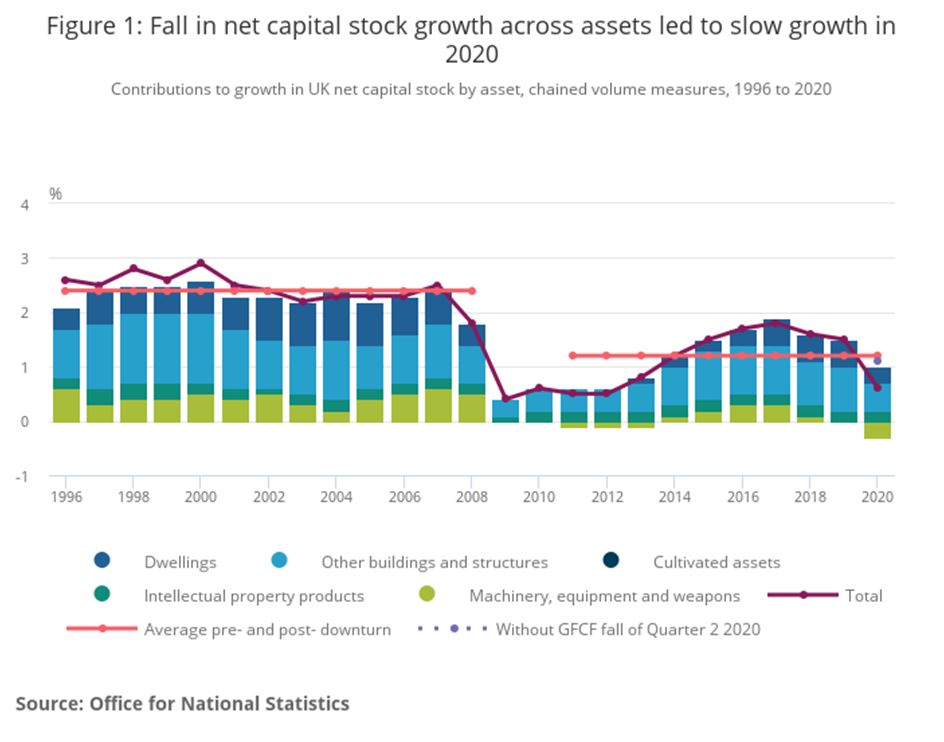

The economic policy is not irrational if the scale and character of the British economic crisis is grasped. A key aspect of this is shown in Chart 3 below.

Chart 3. UK Net Capital Stock and its Components 1996 to 2020.

The net capital stock is the product of Investment in the economy once depreciation and dilapidation are taken into account. It is the means of production. Prior to the Global Financial Crisis in 2007 to 2008 the average annual growth rate for the net capital stock had settled at around 2.4%. In the business cycle since, which is probably ending now, the growth rate of the net capital stock has halved to 1.2%.

It is not coincidental that the net capital stock in both instances is closely related to the real growth rate of the economy over the business cycle, as net investment is the primary determinant of growth.

As we know, Investment has since fallen, led by Business Investment which was 12% lower in 2021 than in 2019. This comes close to an absolute crisis for the British economy and especially for its business sector.

The ‘mini-Budget’ shows that the health of the business sector is clearly the most important priority for this government. The Truss/Kwarteng government differs from its predecessors by stripping way any pretence otherwise. For any government an Investment strike by its business sector would be a matter of grave concern. For this government it is a catastrophe.

Their agenda is to boost the returns to private capital by cutting taxes, cutting wages, deregulation, outsourcing and privatisation. The problem is that this Thatcherite solution does not work. It did not work under Thatcher and will not work by repeating it in much worse conditions.

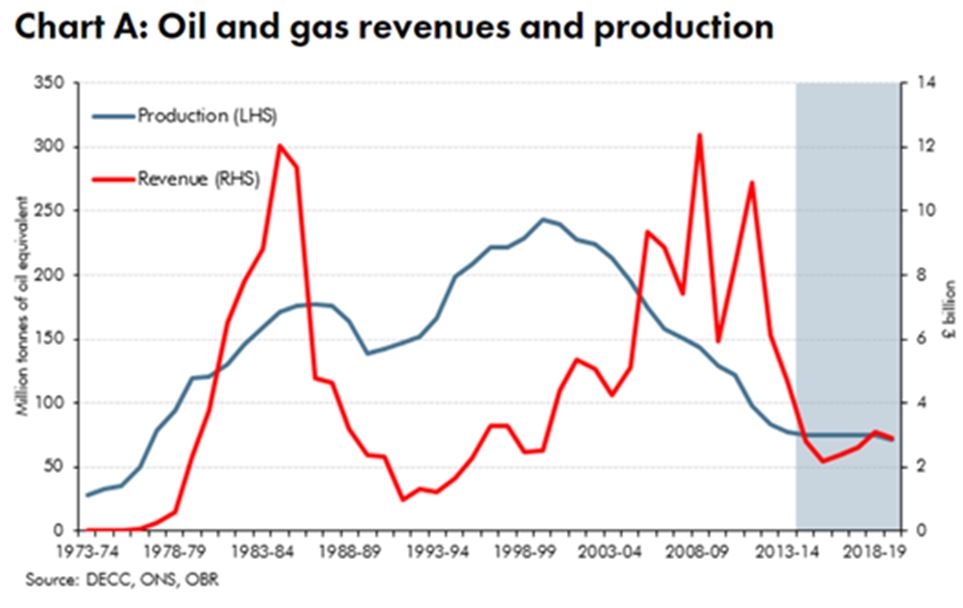

As Chart 4 below shows, Thatcher’s policies benefitted from enormous N Sea oil revenues almost from the moment she entered Number 10 Downing, peaking at 3.4% of GDP in 1984-85.

Chart 4. North Sea Oil Revenues

Source: OBR

This was an enormous windfall. But the policy response was tax cuts and privatisation, even including the main company benefitting directly from the oil bonanza, BP! These tax cuts eventually led to an unsustainable boom (the ‘Lawson boom’) which ended with a crash. But the dominant trends of the Thatcher period were economic slump and mass unemployment. The official unemployment total stayed close to 3 million people for 6 years.

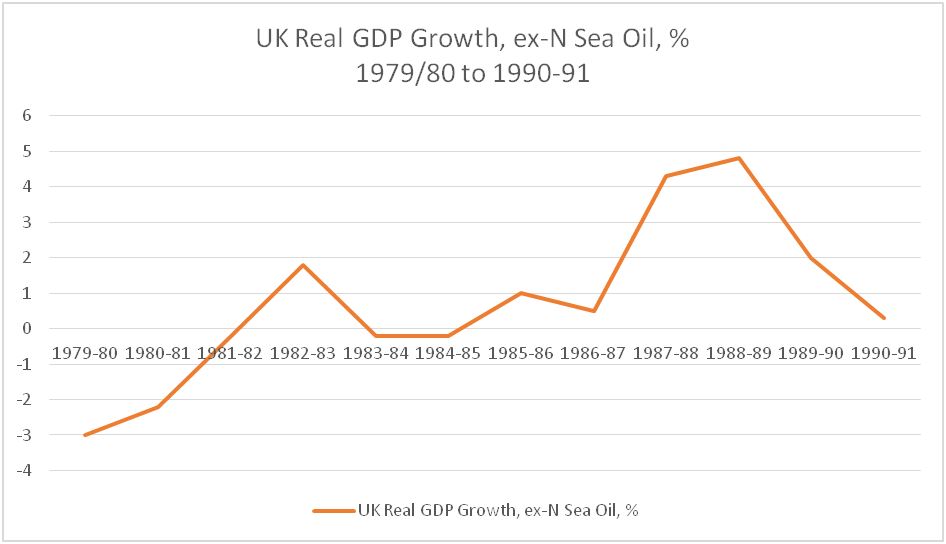

The weakness of the economy is highlighted in the chart below.

Chart 5. UK Real GDP Growth Under Thatcher, excluding North Sea Oil revenues, % change

Source: OBR, ONS data, author’s calculation

Excluding the surge in N Sea oil revenues the economy grew by just 12% over the entire period, making it the weakest period of growth of this length over the entire era since the end of World War II. There was also no net asset creation, as there has been with Norway’s Sovereign Wealth Fund. The revenues were simply frittered away in tax cuts.

These are the policies now being emulated by this government. And it should be stressed that their own, self-made inheritance is far worse on all key economic indicators than Thatcher operated under in 1979.

This government has taken the view that it is impossible to disguise the scale of the attacks that are coming, even with the help of the British media, so they are not going to try.

Instead, they have staked out ground that claims they have the answers to the economic crisis. They will then dare other social forces, most notably the unions, and the opposition, to formulate an alternative. That is the next major challenge.

Recent Comments